The dismal days of Biden/Harris/Yellen are gone. Although Chuck Schumer, Nancy Pelosi, Hakeem Jeffries and my in-laws are all singing “Those Were The Days.” Of immense government corruption and waste.

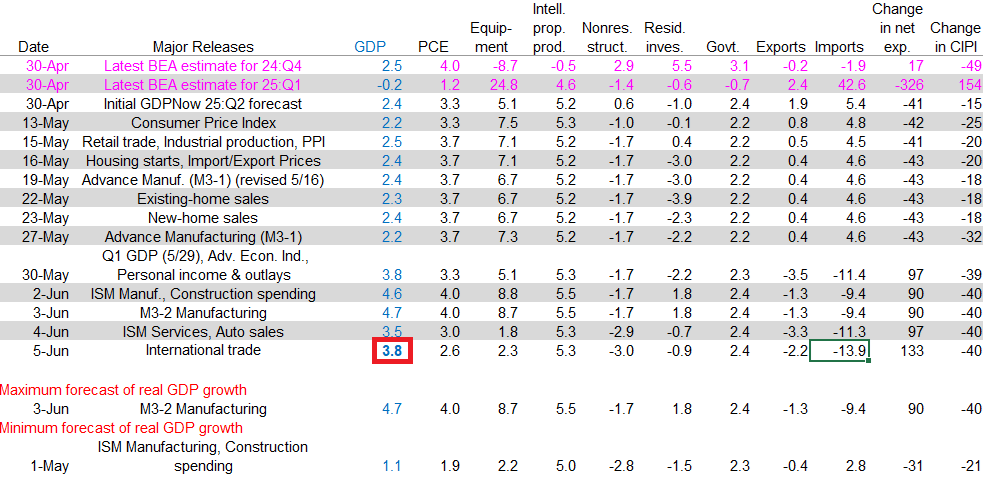

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2025 is 3.8 percent on June 5, down from 4.6 percent on June 2. After recent releases from the US Census Bureau, the US Bureau of Economic Analysis, and the Institute for Supply Management, the nowcasts of second-quarter real personal consumption expenditures growth and real gross private domestic investment growth decreased from 4.0 percent and 0.5 percent, respectively, to 2.6 percent and -2.2 percent, while the nowcast of the contribution of net exports to annualized second-quarter real GDP growth increased from 1.36 percentage points to 2.01 percentage points.

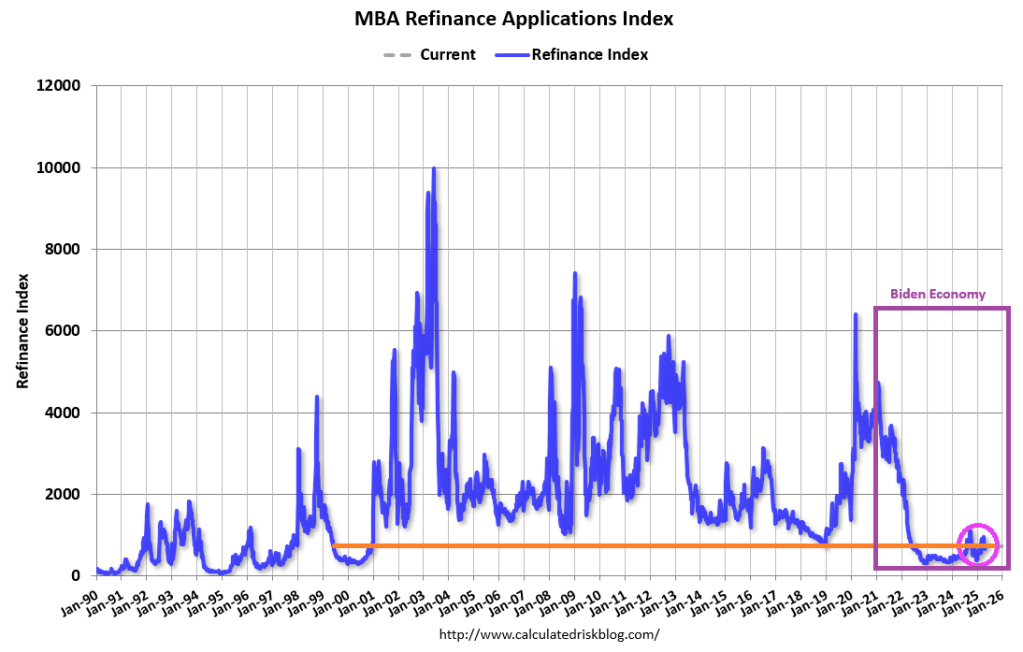

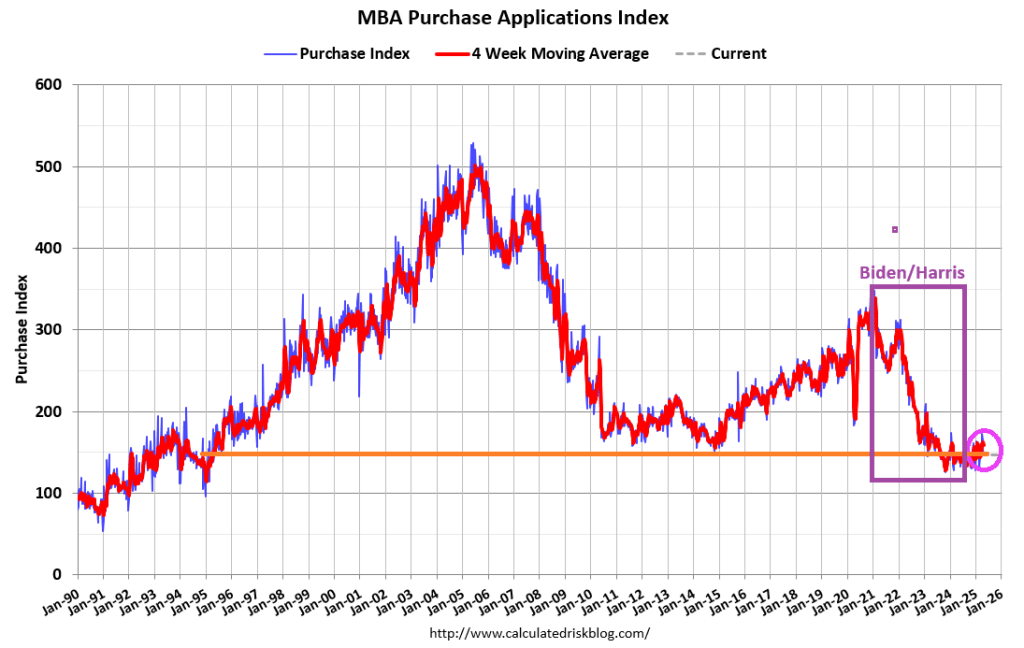

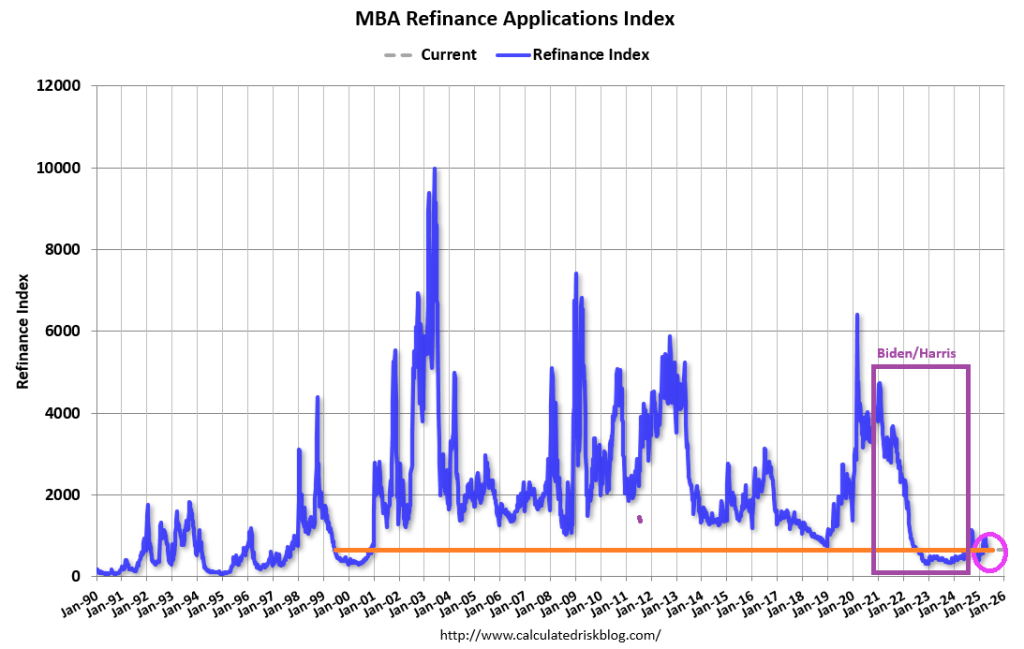

Here is the breakdown.

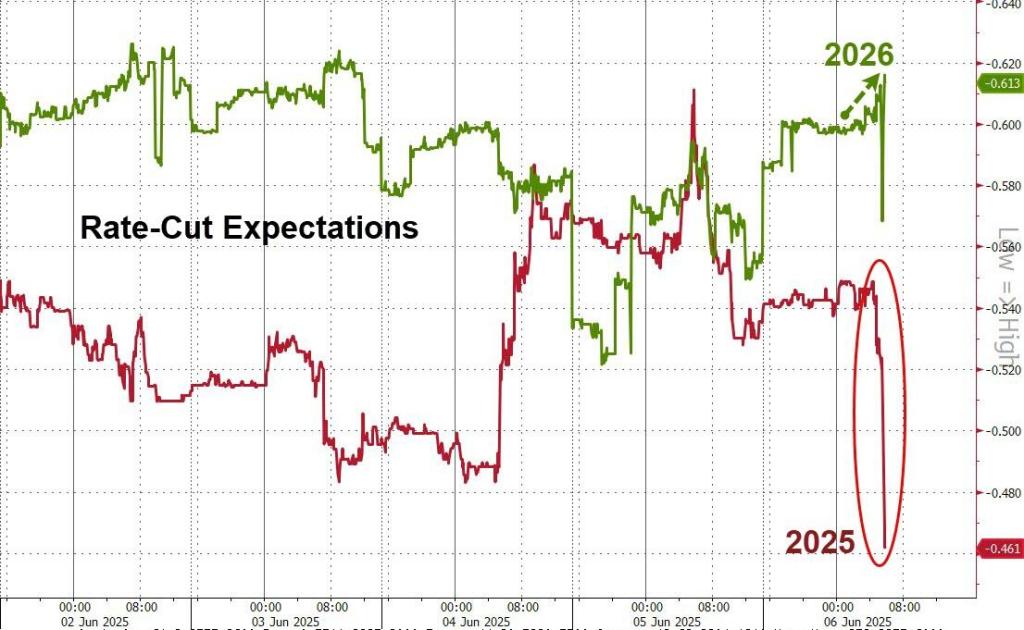

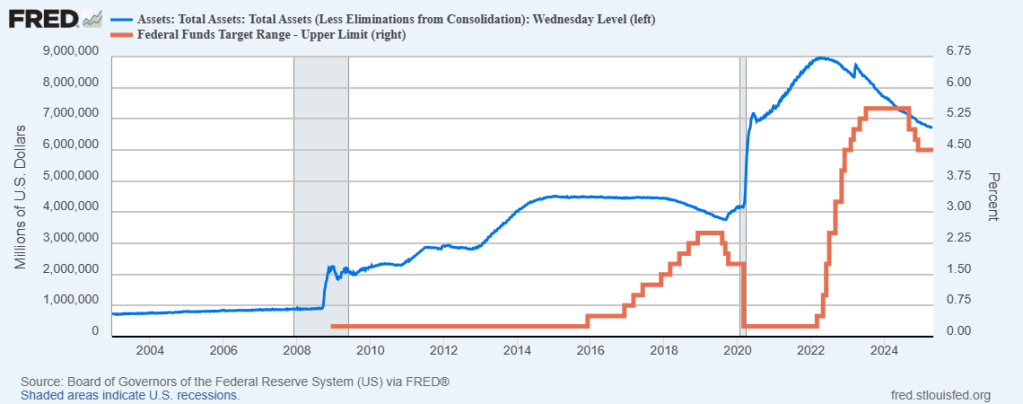

The Fed still needs to lower rates by 100 basis points, but that looks unlikely.

You must be logged in to post a comment.