But, below the hood of the last one we see some more interesting dynamics evolving as revenues and employment decline while prices re-accelerate…

Source: Bloomberg

This is the 25th straight month of contraction (sub-zero) for the Dallas Fed Services index and judging by the respondents’ comments, there is a clear place to point the finger of blame:

Poor national leadership and lack of confidence have eroded the business environment.

The Federal Reserve’s recent announcement of no rate cuts in the near future is concerning regarding the immediate and lag effect it could have on the local economy. We have received direct feedback from many of our clients in various industries, and they are increasingly concerned. They are freezing hires and spending, with many reducing spending. The primary reason is the economic stagnation locally and nationally affecting their businesses.

People are adjusting to new economic realities. Few are expecting salary increases and are instead making lifestyle adjustments to deal with higher living costs. Reality is also setting in for the apartment owners we serve. They understand rents aren’t going up and interest rates aren’t coming down. As rate caps expire and loans mature, lenders are having to adapt as well. Ultimately, a lot of private equity (much in the form of individual retirement savings put into syndications) is getting wiped out.

We need a rate cut before we will see any revenue improvement from home sales.

As elections draw near, the political environment worsens, creating more uncertainty in our business.

We feel inflation and fear of more inflation plus the rise in cost of living are holding consumers back. Hopefully we will adapt to the new realities soon.

Customers are concerned about the election, so they are holding off on large purchases.

The lack of building activity is shutting down the appliance industry.

Affordability has become an ever-increasing problem for new car dealers. The price increases of new cars combined with higher interest rates have put new cars out of reach for more and more people.

[Car] inventories continue to swell, and interest rates remain high. Our grosses are off, and margins continue to decline. Profits are down 20 percent from the prior year.

The economy is slowing. The consumer is more cautious and more reluctant to purchase at higher prices and payments.

And finally, this seemed to sum up just how business-owners feel in general about the current occupant of The White House:

“Our outlook depends heavily on the presidential election.

S&P/Case-Shiller released the monthly Home Price Indices for April (“April” is a 3-month average of February, March and April closing prices). The pace of appreciation has slowed from the previous month, reflecting the toll of 7% mortgage rates and low inventory.

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 6.3% annual gain for April, down from a 6.5% annual gain in the previous month. The 10-City Composite saw an annual increase of 8.0%, down from an 8.3% annual increase in the previous month. The 20-City Composite posted a year-over-year increase of 7.2%, dropping from a 7.5% increase in the previous month. San Diego continued to report the highest annual gain among the 20 cities in April with a 10.3% increase this month, followed by New York and Chicago, with increases of 9.4% and 8.7%, respectively. Portland once again held the lowest rank this month for the smallest year-over-year growth, with a 1.7% annual increase in April. … The U.S. National Index, the 20-City Composite, and the 10-City Composite upward trends decelerated from last month, with pre-seasonality adjustment increases of 1.2%, 1.36% and 1.38%, respectively.

After seasonal adjustment, the U.S. National Index and 10-City Composite posted the same month-over-month increase of 0.3% and 0.5% respectively as last month, while the 20-City reported a monthly increase of 0.4%.

“For the second consecutive month, we’ve seen our National Index jump at least 1% over its previous all-time high,” says Brian D. Luke, Head of Commodities, Real & Digital Assets at S&P Dow Jones Indices. “2024 is closely tracking the strong start observed last year, where March and April posted the largest rise seen prior to a slowdown in the summer and fall. Heading into summer, the market is at an all-time high, once again testing its resilience against the historically more active time of the year.

“Thirteen markets are currently at all-time highs and San Diego reigns supreme once again, topping annual returns for the last six months. The Northeast is the best performing market for the previous nine months, with New York rising 9.4% annually. Sustained outperformance of the Northeast market was last observed in 2011. For the decade that followed, the West and the South held the top posts for performance. It’s now been over a year since we’ve seen the top region come from the South or the West.

Of course, Fed Money Printing is helping drive home price growth. Perhaps too much!

Here is Jerome Powell, Chairman of The Fed Bubble Blowing Machine!!

Where the jobs aren’t! Calfironia under Gavin Newsom and their Marxist elected officials.

Based on the most recent release of the early benchmarks, payroll jobs declined by 32,000 from September 2023 through December 2023. On the contrary, the preliminary monthly reports showed a solid increase in job growth (+117,000 jobs) at the time. With the fourth quarter revision, calendar year 2023 saw essentially no net job growth (+9,000 jobs overall). Data since January 2024 has not yet been rebenched. As such, the figure includes the Early Benchmark Revision for these recent months growing at the same rate as the official CES estimates.

Given Calfornia’s burdersome taxes and regulations, not to mention $20 per hour for fast food workers, it is not surrprising that job growth in California has been minimal.

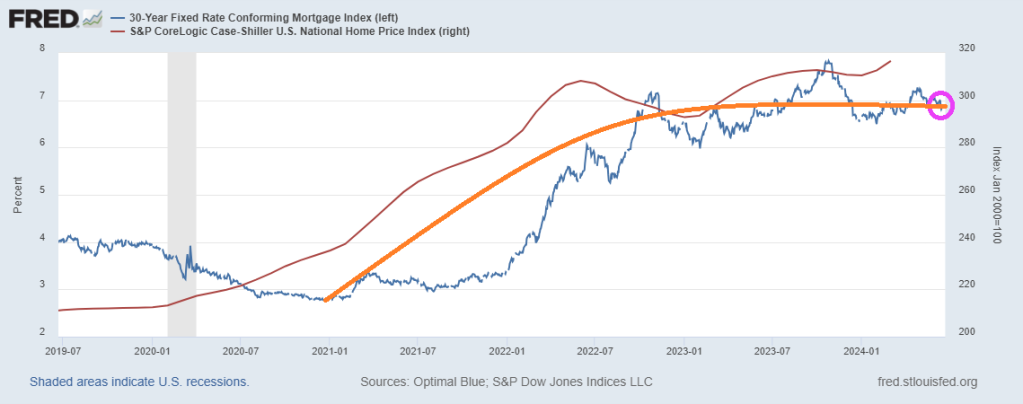

In politics, it is usually discussed whether you are better off today than 4 years ago. Well, not if you are a renter or need to buy a home with mortgage financing.

If you are a homeowner, you are better off in terms of home equty. With the Case-Shiller National home price index up 34% since Biden’s selection as President. That is the good news.

The bad news? Property taxes are soaring and home insurance rates are up.

The worst news? The 30 year conforming mortgage rate is up 147% under Biden.

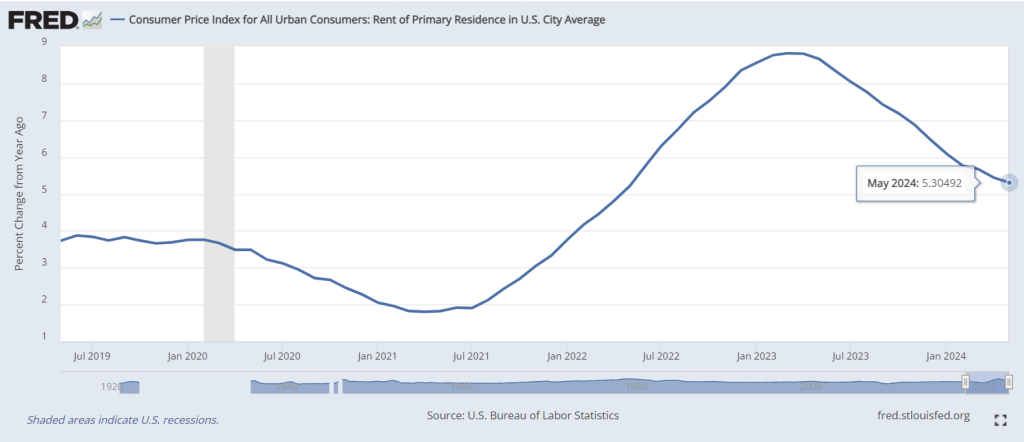

If you are a renter, you are worse off because of rising rents and the diffculty of transitioning to homeowership. Despite slowing, rental CPI is still growing at 5.3% YoY.

Well, perhaps bot a genuine surprise. We are aware that the US economy has been slowing as the massive fiscal and monetary stimulus from Covid is wearing out.

The economics surprise index slumped to -28.10, the lowest since 2022.

I feel like the US economy is experiening a Ragnarok change. With the giants (World Economic Forum/UN. etc) winning.

I am no forune teller, but this doesn’t look to good for old Joe (Biden).

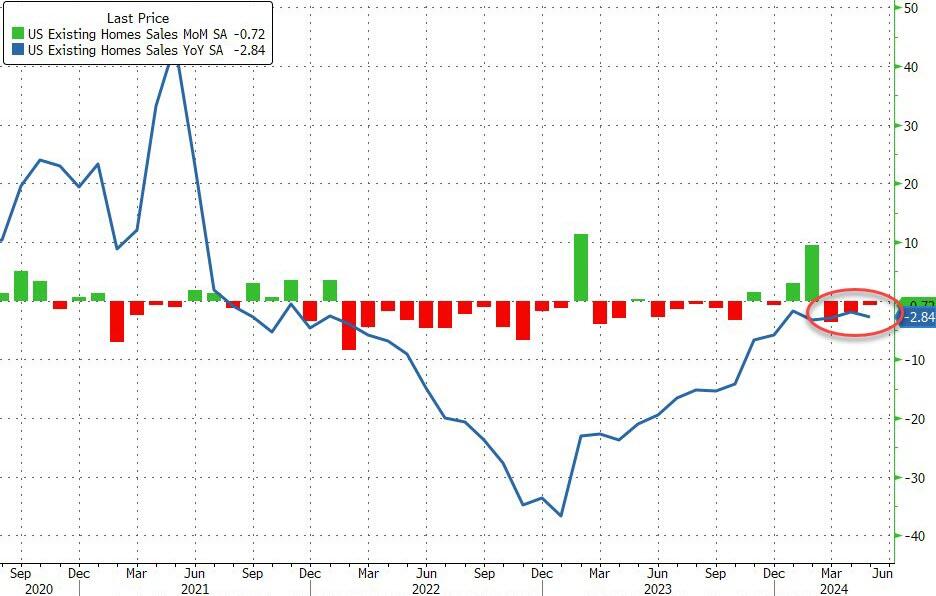

Existing home sales fell -2.8% YoY in May.

US existing home sales fell for the third straight month in May (-0.7% MoM vs -1.0% exp). This left home sales down 2.8% YoY (YoY sales have not increased since July 2021)…

Source: Bloomberg

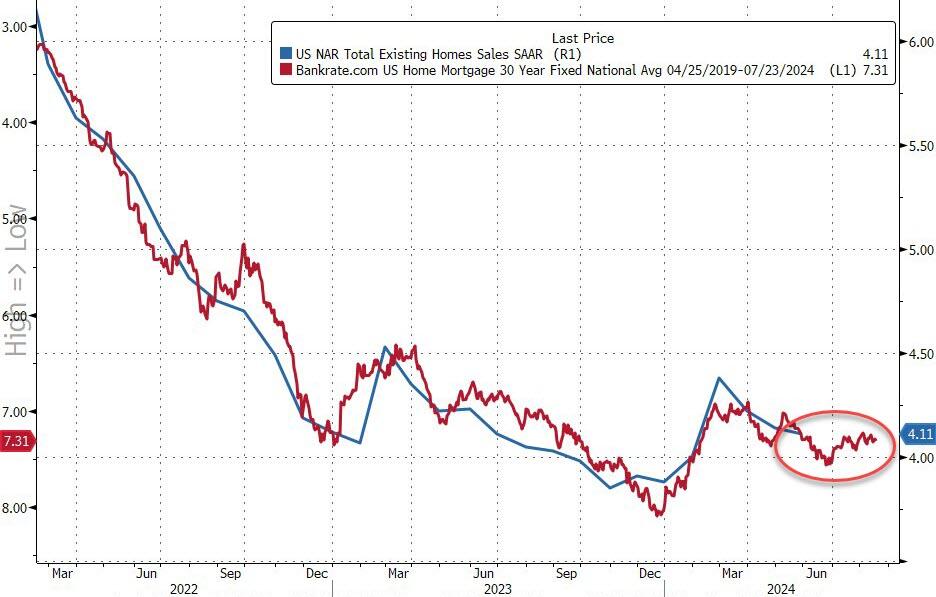

The total home sales SAAR is push back towards COVID lockdown lows once again at 4.1mm, but prices accelerated to a new record high…

Source: Bloomberg

“Home prices reaching new highs are creating a wider divide between those owning properties and those who wish to be first-time buyers,” NAR Chief Economist Lawrence Yun said in a statement.

“Eventually, more inventory will help boost home sales and tame home price gains in the upcoming months.”

And given that mortgage rates remain stubbornly above 7%, existing home sales show no signs of improving anytime soon…

Source: Bloomberg

The supply of homes on the market increased 18.5% from the same month last year to 1.28 million, but it’s still well below the level seen before the pandemic when mortgage rates were much lower.

Source: Bloomberg

About 67% of the homes sold were on the market for less than a month in May, roughly flat from the prior month, while 30% sold above the list price. Properties remained on the market for 24 days on average in May, compared with 26 days in April, NAR’s report said.

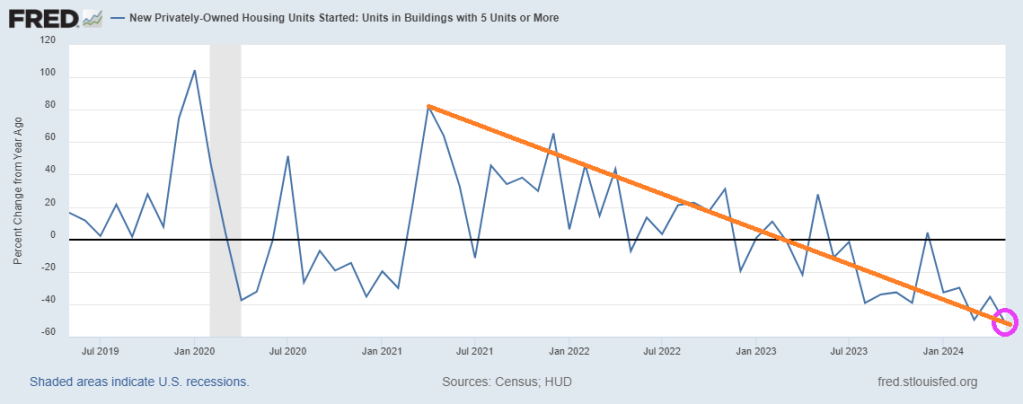

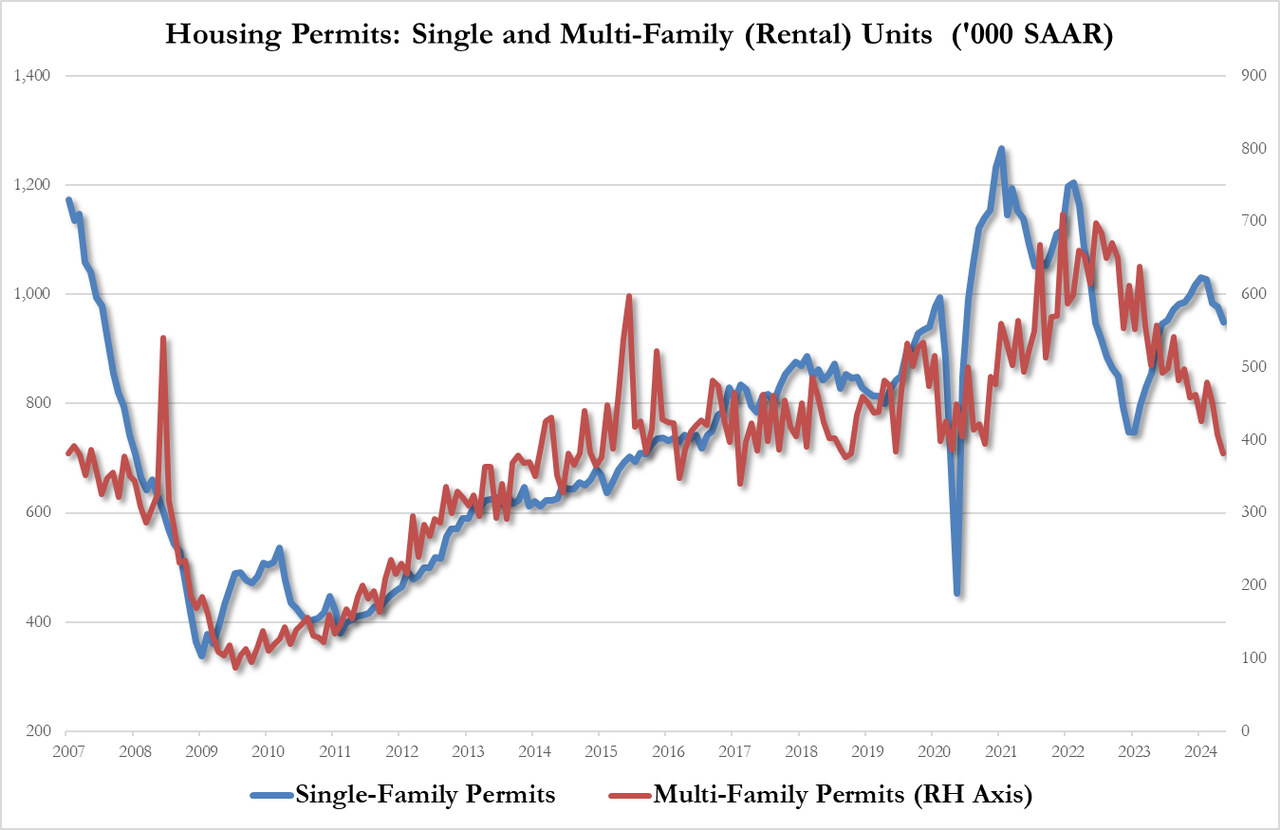

It begs the question: where are the 10+ million illegal immigrants living who have poured over the border under Binden/Mayorkas? Especially when 5+ units housing starts dropped -51.7% since last year (YoY) in May. And the trend under Biden looks terrible!

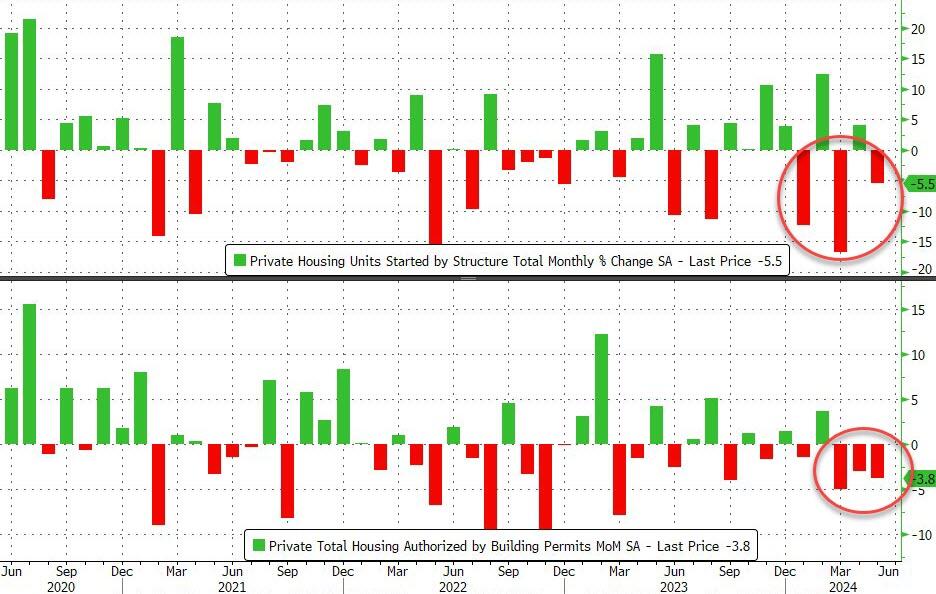

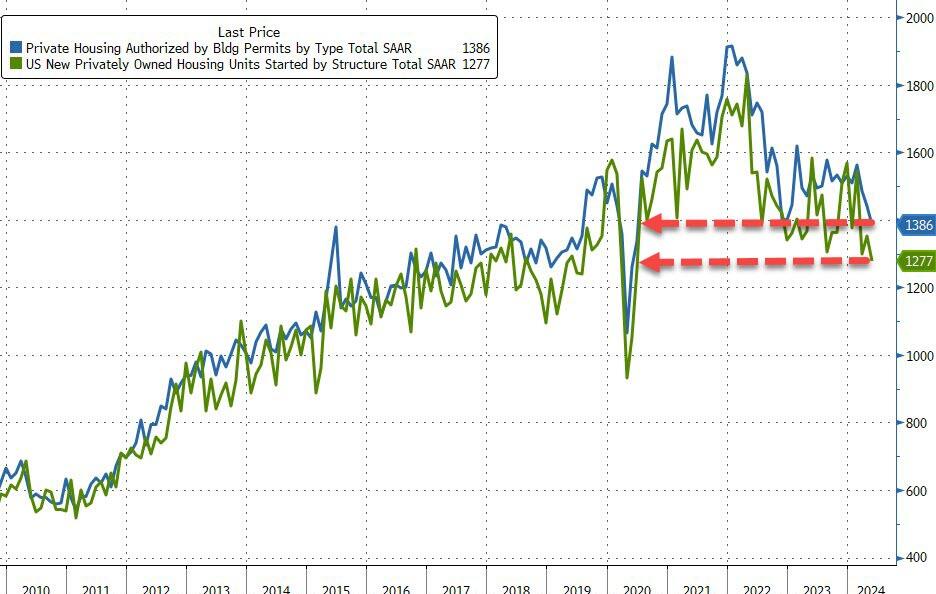

That was the third monthly drop in permits (more forward looking) in a row. Worse still, April Housing Starts were revised lower (from +5.7% to +4.1%), making this miss even worse.

This dragged the SAARs for starts and permits to their lowest since the trough of COVID…

Source: Bloomberg

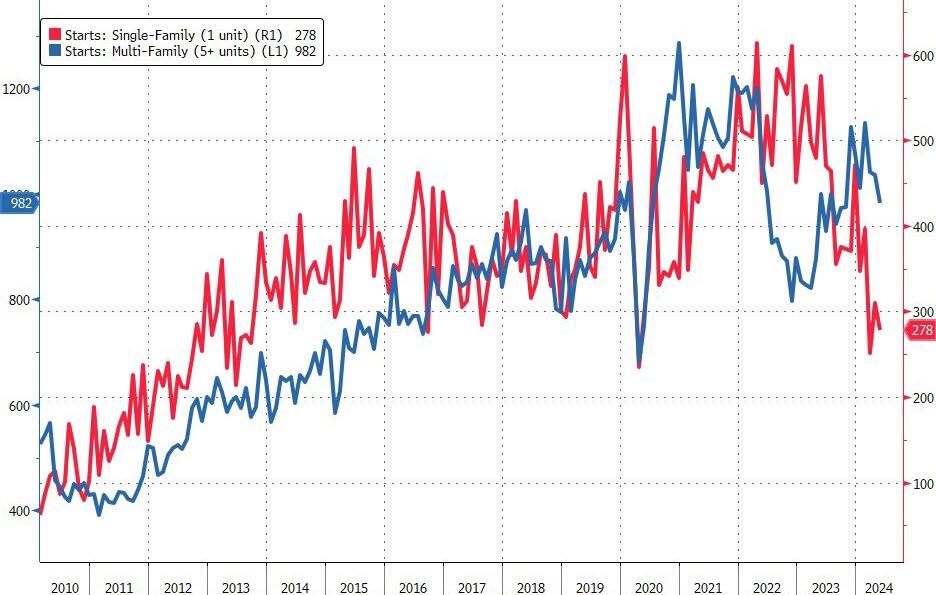

With Multifamily starts falling back near COVID lockdown lows…

Single-Family 982K SAAR, down 4.8% from 1,031K and the first sub-million print since October 2023

Multi-Family 278K, down 13.7% from 322K and the lowest since March’s 245K (which was the lowest print since covid crash)

Source: Bloomberg

And multi-family permits cratering to their lowest since Oct 2018…

Single-Family permits 949K SAAR, down 2.9% from 977K

Multi-Family permits 382K SAAR, down 6.1% from 407K

And with rate-cut expectations holding near their lows, there is no sign of recovery in home-building yet…

Source: Bloomberg

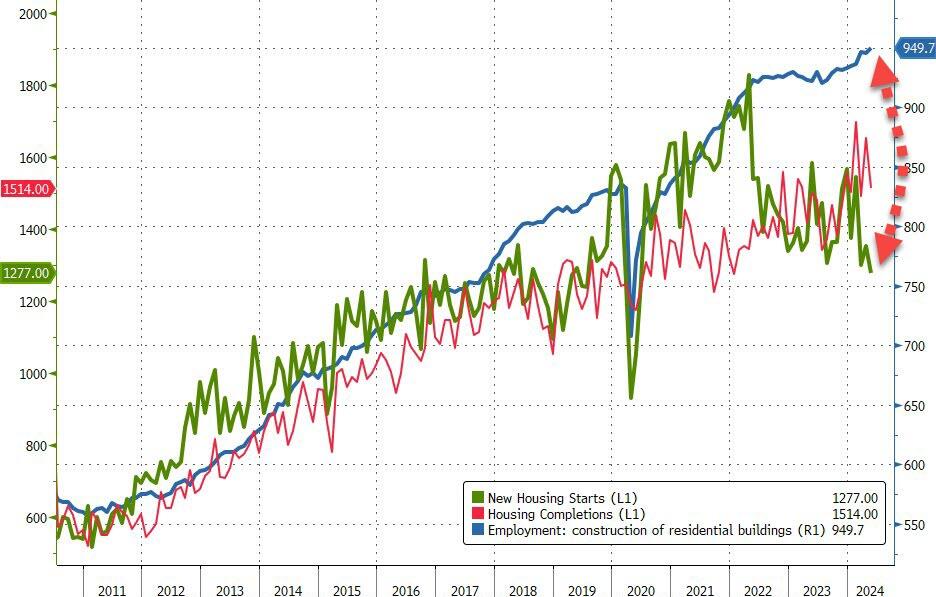

It seems reality is starting to set in for homebuilders…

Source: Bloomberg

As housing starts plummet, jobs seem to keep growing to record highs…

Now you know why Joe Biden has fund raisers in Hollywood and New York where the elites (the top 1%) live. Biden is the President of The Elites, not the middle class.

How bad it is? The top 1% now have more household wealth than the entire middle class. Note that the recent surge occurred under Trump, but Biden is doing nothing about it.

Further evidence? 46% of households are struggling.

In terms of housing prices, home prices are growing FASTER than average hourly earnings. Again!

Politicians. You can’t trust ANY of them with our money. Or a cookout.

Here is New Yprk Senator Chuck Schumer posing as a middle class American cooking gray hamburgers at super low heat with cheese on top of raw meat. What a fraud!

This prediction only got warmer two months later when, inexplicably, Japan’s Norinchukin bank, best known as Japan’s CLO whale, was quietly added to the list of counterparties for the Fed’s Standing Repo Facility, a/k/a the Fed’s foreign bank bailout slush fund.

But if that was the first, and still distant, sign that something was very wrong at one of Japan’s biggest banks (Norinchukin is Japan’s 5th largest bank with $840 billion in assets) today the proverbial canary stepped on a neutron bomb inside the Japanese coalmine, because according to Nikkei, Norinchukin Bank “will sell more than 10 trillion yen ($63 billion) of its holdings of U.S. and European government bonds during the year ending March 2025 as it aims to stem its losses from bets on low-yield foreign bonds, a main cause of its deteriorating balance sheet, and lower the risks associated with holding foreign government bonds.”

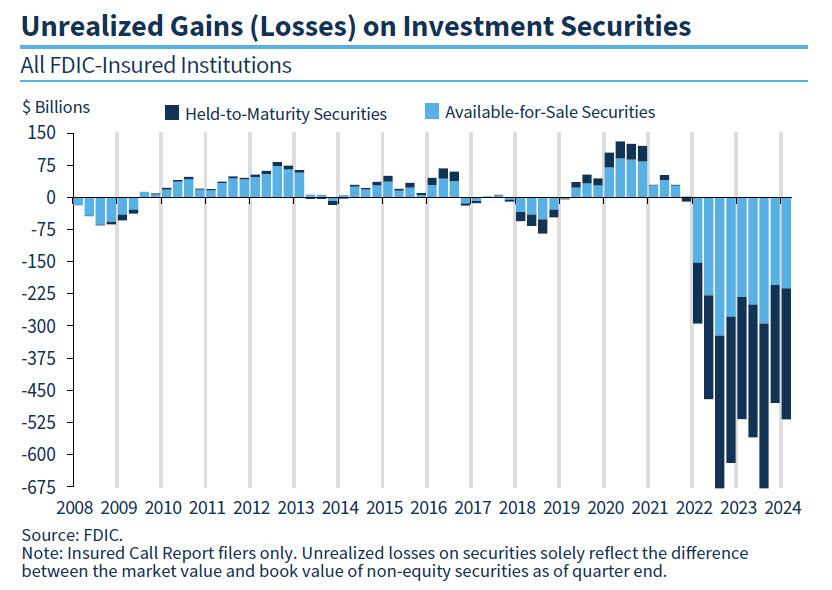

See, what’s happened in Japan is not that different from what is happening in the US, where as the FDIC keeps reminding us quarter after quarter, US banks are still sitting on over half a trillion dollars in unrealized losses, as a result of the huge jump in interest rates which has blown up the banks’ long-duration fixed income holdings, sending them trading far below par and forcing banks (and the Fed, see BTFP) to come up with creative ways of shoving these massive losses under the rug.

And while Japanese rates have barely budged – the BOJ only just raised rates for the first time in decades in April – the move is already cascading into the form of huge losses for domestic banks, which have been hammered twice as hard due to their holdings of offshore debt which until 2021 was viewed as risk free, only to blow up in everyone’s face two years ago when the bull market since the early 1980s ended with a bang.

Enter Norinchukin: according to the Nikkei, the company’s net loss for the year ending March 2025, which was previously forecast to top 500 billion yen, will rise to the 1.5 trillion yen level with the bond sales.

“We plan to sell low-yield [foreign] bonds in the amount of 10 trillion yen or more,” Norinchukin Bank CEO Kazuto Oku told Nikkei, an amount just above $60 billion.

Facing a problem that is very familiar to all US banks, Oku said the bank “acknowledged the need to drastically change its portfolio management” to reduce unrealized losses on its bonds, which totaled roughly 2.2 trillion yen as of the end of March. Oku explained bank’s intention to shift its investments, saying, “We will reduce [sovereign] interest rate risk and diversify into assets that take on corporate and individual credit risk.”

Now, if Nochu, as it is affectionately known by bankruptcy lawyers, was a US bank circa one year ago, it would not have to sell anything: it could just pledge all of its sharply depreciated bonds at the Fed’s BTFP facility, and get a par value for them.

Unfortunately, Nochu is not US but Japanese, and it is not 2023 but rather 2024, when the high-rate disaster of 2023 was supposed to be over. Supposed to be… but instead it’s only getting worse. Regular readers will hardly need it, but for novices Nikkei gives the following quick primer: “Interest rates in the U.S. and Europe have risen and bond prices are down. This reduced the value of high-priced (low-yielding) foreign bonds that Norinchukin purchased in the past, causing its paper losses to swell.”

So faced with no other options, Nochu is doing the only thing it can: an orderly liquidation of tens of billions of securities now, when they are still liquid and carry a high price, in hopes of avoiding a disorderly liquidation and much worse, in a few months when the bond market freezes up.

And yes, the Japanese rates canary is quite, quite massive: as of the end of March, Norinchukin had approximately 23 trillion yen of foreign bonds (about $150 billion), amounting to 42% of its total 56 trillion yen of assets under management.

To get some sense of the scale, according to the Bank of Japan, outstanding foreign bonds held by depositary financial institutions amounted to 117 trillion yen as of the end of March. Norinchukin, which is a major institutional investor in Japan, holds as much as 20% of the total on its own! And those asking, yes: once Nochu begins selling, all others will have to join the club!

But why start the selling now? Because, as we warned last October when we predicted that the next bank crisis will be in Japan, the Japanese mega-bank now believes interest rate cuts in the U.S. and Europe are likely to take longer than it previously expected, it will try to significantly cut its unrealized losses by selling foreign bonds in fiscal 2024.

And so, Norinchukin plans to sell over 10 trillion yen in foreign bonds, in addition to its normal trading activities.

The rest of the story is filler: in attempt to divert attention from the 10 trillion yen elephant in the room, the Nikkei then wastes time discussing the bank’s other “alternatives” to wit:

The company is now considering investment alternatives, including equities, corporate bonds, corporate loans and private equity, as well as securitized products such as corporate loan-backed securities and mortgage-backed securities. By diversifying its portfolio, it aims to prevent unrealized losses from expanding to the point where they become a concern for management. It will also try to replace some low-yielding foreign government debt with other such bonds offering higher interest rates.

What are you talking about? What diversification? Once the selling begins, the bank will be lucky if it can get even a fraction of the proceeds it hopes for (because all the other banks won’t just be standing there twiddling their thumbs, as they wait to see how massively Nochu reprices the market).

And it’s not just banks: if and when the selling begins by a bank that holds 20% of all foreign bonds in Japan, the liquidation cascade will quickly spread to Mrs Watanabe. According to the U.S. Treasury Department, Japanese investors held $1.18 trillion of U.S. government bonds as of March, the largest slice among foreign holders.

Needless to say, but the Nikkei does so anyway, “Massive sales by Norinchukin could have a sizable effect on the U.S. bond market.”

And since we now know what is happening, it is only a matter of time before everyone else frontruns Norinchukin.

What happens next will be even uglier: since the bank will no longer be able to mask its fixed income losses under the guise of accounting sleight of hand, the bank’s financial results for the period ending March 2025 will “deteriorate significantly as a result of the huge divestment of foreign bonds and turn paper losses into real ones.” As of May, Norinchukin put its final loss at more than 500 billion yen, but this is now expected to reach the 1.5 trillion yen level.

A little more context: back in the immediate aftermath of the global financial crisis, in the year ending March 2009, Norinchukin posted a final loss of about 570 billion yen due to impairment of securitized products. The forecast loss for this fiscal year is expected to top the previous record by roughly 1 trillion yen. Nevertheless, Oku said that putting the losses on the books in the year ending next March will “improve [the bank’s] finances and portfolio, thus enabling to move into the black in the period ending March 2026.”

Spoiler alert: no it won’t… and that’s why the bank is now scrambling to share the pain with even greater fools, i.e., “investors.”

According to the Nikkei, Norinchukin Bank is considering raising 1.2 trillion yen to shore up its finances. It has already started discussions with Japan Agriculture Cooperatives, one of its main investors, and others. Of course, the question of who in their right mind would lend the bank good money to plug an even bigger hole that is about to open up, is anyone’s guess.

But that won’t stop the bank from doing what it has to, now that it has picked the liquidation route: and once the selling flood begins, it won’t end as these flashing red headlines from Bloomberg just confirmed:

*NORINCHUKIN TO SELL US, EUROPEAN SOVEREIGN BONDS GRADUALLY

*NORINCHUKIN ALSO WEIGHS LOCAL, OVERSEAS BONDS, PROJECT FINANCE

*NORINCHUKIN EYES ASSETS INCLUDING CLOS, STOCKS AFTER BOND LOSS

There’s a name for this: a firesale, but – drumroll – a “gradual” one, because that’s how firesales supposedly go in Japan.

Luckily, the one thing nobody has to guess, is what happens next: as the wonderful movie Margin Call laid out so very well, once you realize that the music has stopped, you have three choices: i) be first, ii) be smarter, or iii) cheat. In the case of Japan’s Norinchukin, it has decided the time has come to liquidate before everyone else. We wonder how “everyone else” will take this particular news…

US Treasury Secretary (and former Fed Chair) Janet Yellen says the US economy is in excellent shape. Is she a genius and sees something that rest of us don’t? Or is she a partisan thug like Shap Shot’s Gilmore Tuttle?

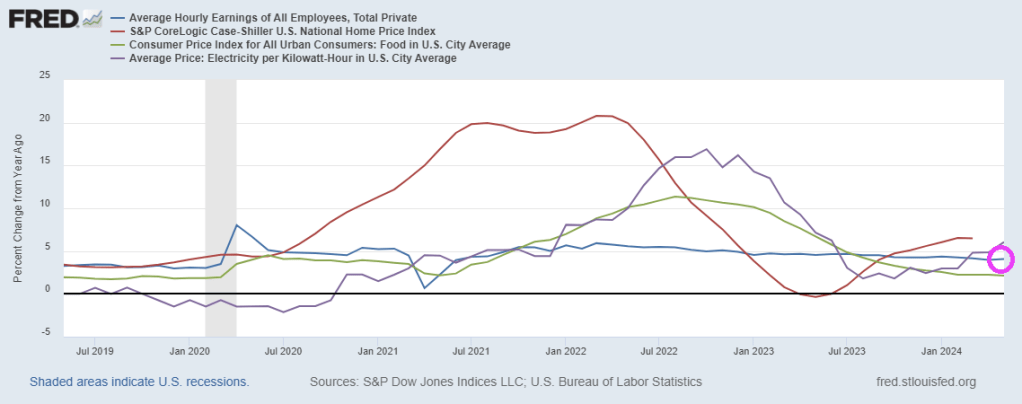

Yellen brags about rising wages and declining inflation. Well, average hourly earnings YoY are now 4.1%. However, home prices are growing at 6.5% year-over-year (YoY) and electricity prices are up 6.1% YoY. Food CPI grew at 2.1% in May. Yellen ignores the string of 10%+ increases in 2022-2023 making eating unaffoprdable for millions.

I doubt if Yellen could run a lemonade stand in my neighborhood. But like Gilmore Tuttle, maybe she could run a donut shop!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.