As of today, the US Treasury 10yr-2yr yield curve is the most inverted since 1981 at -70 basis points.

Meanwhile, equity put/call ratio from CBOE spiked yesterday to highest since 1997.

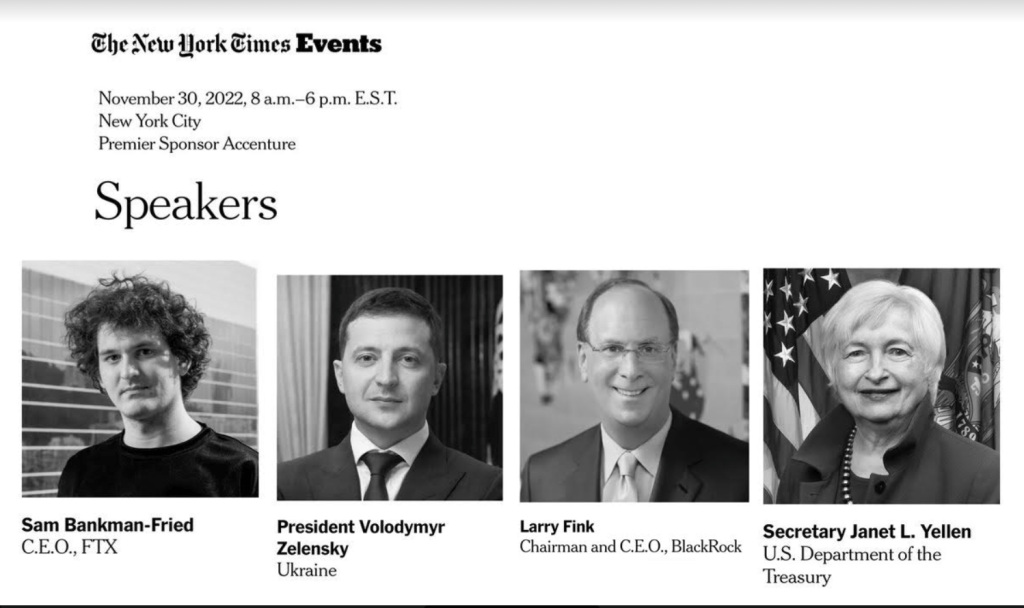

I am disappointed that The New York Times cancelled their $2,400 event to listen to Sam The Sham Bankman-Fried, Vlad “Show my your money!” Zelensky, Larry “The Big Fink” Fink and Janet “We never saw it coming” Yellen. I would have loved to do the New York Times job for them and ask hard questions to Sam The Sham and Zelensky about money laundering.

As I have said before, Sam Bankman-Fried and FTX exemplifies loose Fed monetary policy and its unintended consequences: shoddy investment practices by both sides and ridiculous claims that are unverified.

Like Sam Bankman-Fried tweeting that FTX and his team were held as paragons of running an effective company.

I am sure that SBF’s attorneys (like his parents) are telling Spam to stop tweeting ridiculous defenses. As in its all the fault of crypto volatility. We now know that at best SBF had a total lack of corporate controls and thought risk management was the Hasbro board game. And SBF while virtue signaling failed to mention his twisted relationship to Ukraine funding.

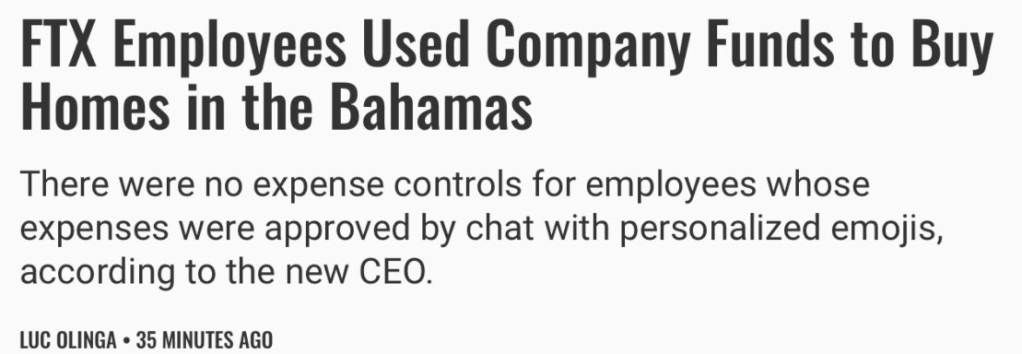

(Bloomberg) — Advisers now overseeing the carcass of Sam Bankman-Fried’s FTX Group are struggling to locate the company’s cash and crypto after finding poor internal controls and record keeping at the now-bankrupt company.

“Never in my career have I seen such a complete failure of corporate controls and such a complete absence of trustworthy financial information,” John J. Ray III, the group’s new chief executive officer who formerly oversaw the liquidation of Enron Corp., said in a sworn declaration submitted in bankruptcy court.

“From compromised systems integrity and faulty regulatory oversight abroad, to the concentration of control in the hands of a very small group of inexperienced, unsophisticated and potentially compromised individuals, this situation is unprecedented,” he added.

Advisers have located “only a fraction” of the digital assets of the FTX Group that they hope to recover during the Chapter 11 bankruptcy, Ray said. They’ve so far secured about $740 million of cryptocurrency in offline cold wallets, a storage method designed to prevent hacks. The company’s audited financial statements should not be trusted, Ray said. Advisers are working to rebuild balance sheets for FTX entities from the bottom up, he said.

FTX “did not maintain centralized control of its cash” and failed to keep an accurate list of bank accounts and account signatories, or pay sufficient attention to the creditworthiness of banking partners, according to Ray. Advisers don’t yet know how much cash FTX Group had when it filed for bankruptcy, but has found about $560 million attributable to various FTX entities so far.

Although restructuring advisers have been in control of FTX for less than a week, they’ve seen enough to depict the crypto company as a deeply flawed enterprise. Lasting records of decision making are hard to come by: Bankman-Fried often communicated through applications that auto-deleted in short order and asked employees to do the same, according to Ray.

Well, this story keeps getting worse and worse and makes Sam The Sham look like a common criminal rather than a Democrat Saint.

Didn’t SBF’s chief economist show this chart to him and his Alameda team? The one where crytpos soars at The Fed and Federal government go wild on stimulus, then back-off? As The Fed tightens, cryptos are getting crushed.

At least Bitcoin rallied a bit today to $16,564.21, but other cryptos are down … again. Litecoin is actually up 4.57% while Solana is down -4.35%.

SBF, like Janet Yellen, will claim he didn’t see it coming.

The Philadelphia Fed’s Business Outlook plunged to 1-9.40% YoY, the worst since 2012. Notice how the Philly Phed Plunge is related to M2 Money growth YoY.

Privately‐owned housing starts in October were at a seasonally adjusted annual rate of 1,425,000. This is 4.2 percent below the revised September estimate of 1,488,000 and is 8.8 percent below the October 2021 rate of 1,563,000. Single‐family housing starts in October were at a rate of 855,000; this is 6.1 percent below the revised September figure of 911,000. The October rate for units in buildings with five units or more was 556,000.

The noticeable trends are the decline in 1-unit detached housing starts relative to 5+ unit (multifamily) start as mortgage rates rise/

Privately‐owned housing units authorized by building permits in October were at a seasonally adjusted annual rate of 1,526,000. This is 2.4 percent below the revised September rate of 1,564,000 and is 10.1 percent below the October 2021 rate of 1,698,000. Single‐family authorizations in October were at a rate of 839,000; this is 3.6 percent below the revised September figure of 870,000. Authorizations of units in buildings with five units or more were at a rate of 633,000 in October.

The housing permits chart looks quite similar to the starts chart above. Single-family starts are now lower than before Covid while multifamily permits are still above pre-Covid levels.

Here is a nice chart as well for total housing starts and permits.

The cryptocurrency market is getting hammered thanks mostly to two things: 1) Sam Bankman-Fried’s horrid failure with FTX (fraud, Enron, front-running, stupid investors, Democrat-Ukraine connection) and 2) Fed tightening to combat high inflation.

Bitcoin, the Mac Daddy of cryptos, is down another 2% today.

The rest of the story.

The NEW face of the US Federal government and why they will sweep the Bankman-Fried fiasco under the rug, just like Hunter Biden’s laptop fiasco.

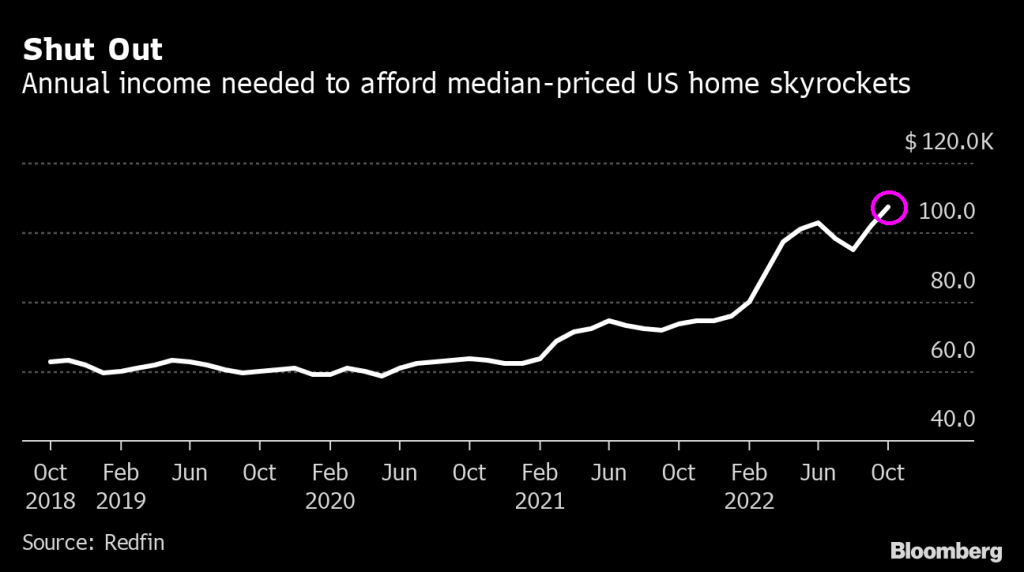

Of course, it is easy to blame the figure on rapidly rising mortgage rates and Federal Reserve tightening.

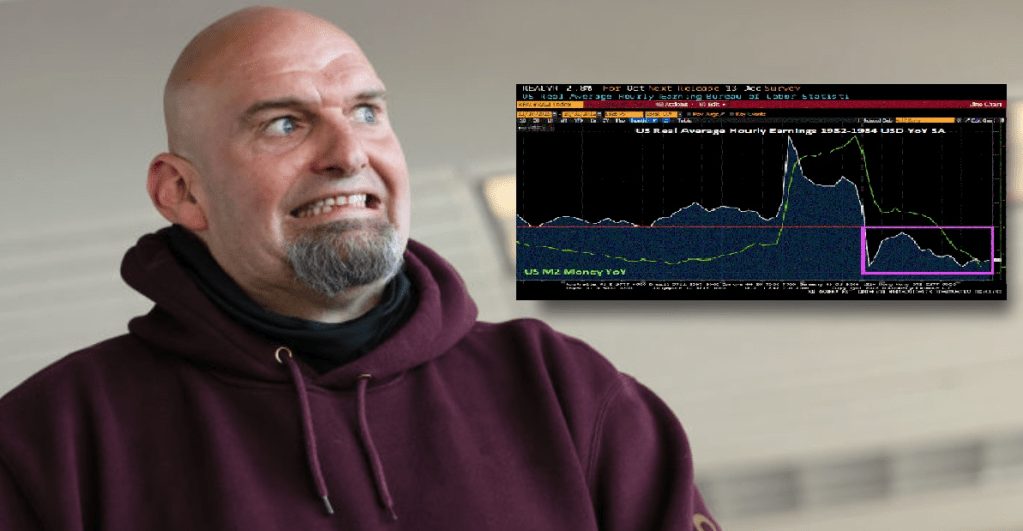

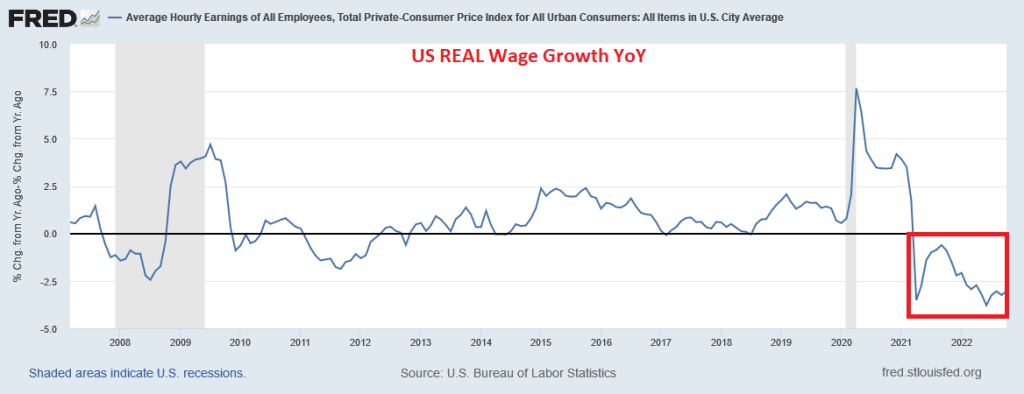

But the rest of the story (as Paul Harvey used to say) is that US REAL wage growth has been NEGATIVE for 19 straight months. This alone makes housing unaffordable for the middle class and low wage workers.

Again, why are Biden and Trudeau wearing Mao jackets in Bali? And why is Biden looking like a robot?? Biden does look like he is saying “Take me to my leader, Pei.”

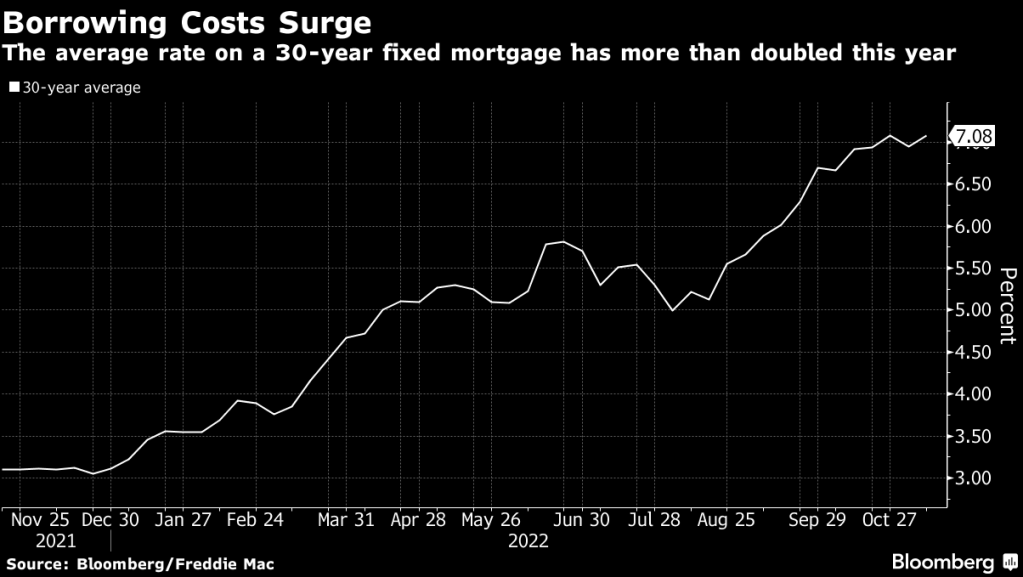

US mortgage rates fell last week by the most since the end of July, slipping below 7% and helping generate a bounce in purchase applications that otherwise remain depressed, but only in the Seasonally Adjusted data. The NON-Seasonally Adjusted data show a hefty decline.

The contract rate on a 30-year fixed mortgage decreased 24 basis points to 6.9% in the week ended Nov. 11, according to Mortgage Bankers Association data released Wednesday. The group’s index of applications to buy a home rose 4.4% — the most since June — but is still near the weakest level since 2015.

But the bounce was in Seasonally Adjusted data only. The NON-seasonally adjusted data remained depressed.

Mortgage applications decreased -10.0 percent SA from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 11, 2022. This week’s results include an adjustment for the observance of Veterans Day.

The Refinance Index decreased -11.44% percent from the previous week and was 88 percent lower than the same week one year ago.The unadjusted Purchase Index decreased -10 percent compared with the previous week and was 46 percent lower than the same week one year ago.

Mortgage purchase applications will continue to fall in NSA terms since it is the Winter and home buying season won’t really start until January. Refinancing applications actually dropped -11.44% even with the drop in mortgage rates.

The data. As my former students know, I like the “raw” data, better known as NON-seasonally adjusted (NSA) data and avoid seasonally-adjusted data (SA) since it hides what is going on.

And on The Fed Futures Front, The Federal Reserve is still looking a hiking their target rate from 4% to just under 5%.

We know that Federal Reserve monetary policy, with the exception of Paul Volcker, has been incredibly loose helping to produce asset bubbles. Particularly under Bernanke, Yellen and Powell.

But cryptos like Bitcoin saw an amazing run-up in price, once in 2017 which came to a halt as The Fed raised their target rate and started to let their balance sheet shrink. Then came Covid in early 2020 and The Fed’s massive overreaction by pushing their target rate to 0.25 basis points (again) and massively expanded their balance sheet. During the Covid “crisis” and the massive Fed response, we saw Bitcoin soar in price.

But starting in 2022, we saw The Fed counterattack inflation by raising their target rate and the expectation of future rate rose rapidly. With this tightening of rates, we saw Bitcoin come crashing back down. I can see Bitcoin crashing further to 7,000 as The Fed continues their counterattack.

My question is … did Sam Blankman-Fried and his team even notice that cryptos were plunging with Fed tightening? Or did he even care? And what were his models? Or Alameda Research’s models? I would love to look at them.

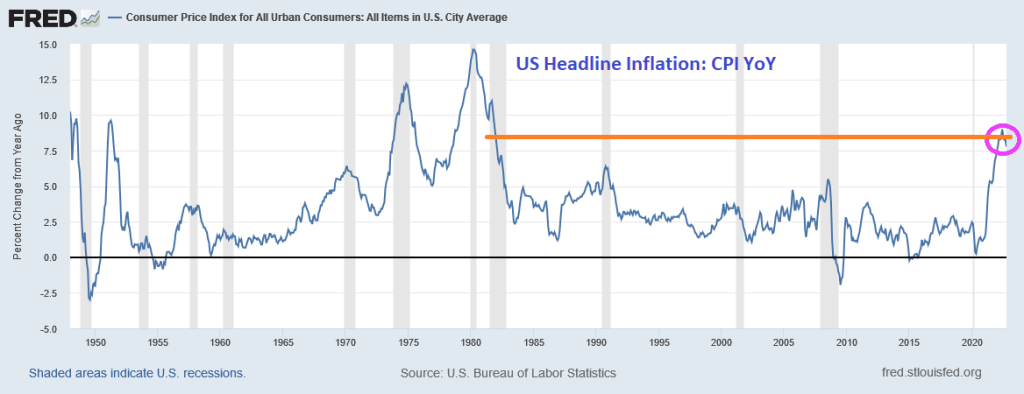

Between Biden’s green energy mandates and the spendathon by the Pelosi/Schumer led Keynesians in Congress (or Kongress), we saw a 40-year high in inflation.

But with roaring Bidenflation, we have the S&P 500 index experiencing, in real terms, the worst performance since 1872.

That is, the worst since President Ulysses Grant.

President Biden is dressed in his Mao outfit with Canada’s Justin Trudeau.

And the WEF’s Klaus Schwab.

At least Biden, Trudeau and Schwab are wearing different colored Mao jackets.

The evidence from the last thirty years is clear. Keynesian policies leave a massive trail of debt, weaker growth and falling real wages. Furthermore, once we look at each so-called stimulus plan, reality shows that the so-called multiplier effect of government spending is virtually inexistent and has long-term negative implications for the health of the economy. Stimulus plans have bloated government size, which in turn requires more dollars from the real economy to finance its activity.

As Daniel J. Mitchell points out, there is evidence of a displacement cost, as rising government spending displaces private-sector activity and means higher taxes or rising inflation in the future, or both. Higher government spending simply cannot be financed with much larger economic growth because the nature of current spending is precisely to deliver no real economic return. Government is not investing; it is financing mandatory spending with resources of the productive sector. Every dollar that the government spends means one less dollar in the productive sector of the economy and creates a negative multiplier cost.

When society decides to use a certain part of the resources generated by the productive sector for non-economic return activities, be it social spending or mitigation of threats, it can only do it by understanding how much of the productive capacity of the economy is able to sustain a larger cost. When costs are not considered as a burden, but considered as entitlements that can only grow, the productive capacity is not strengthened, but weakened.

The main problem of the past decades, but particularly since 2008, is that government spending and monetary policy have become solutions of first resort to any slump in economic activity, even if that decline was created by government decisions, such as shutting down the economy due to a health crisis. Furthermore, government spending increases and loose monetary policy continued even in growth periods. This, in turn, creates an unsustainable public deficit that needs to be monetized or refinanced. Both mean a larger harm for the productive sector as the debt increase leads to higher taxes for everyone but also a soaring cost of living coming from the destruction of purchasing power of the currency.

Government spending does not boost private sector activity, even less so when the entire budget is spent on non-investment outlays. It is even worse when citizens believe that infrastructure or real economic return investments should be conducted with taxpayers’ money. If an investment is productive and economically viable there is no need to involve the government. At best, the government should only participate as a co-investor, as the example of technology and defence shows, but never as a resource allocator for a simple reason. Public intervention is always aimed at perpetuating the existing inefficiencies and maximizing the budget. Efficient resource allocation cannot come from entities that have a core interest in expanding the budget and always perceive any inefficiency or poor result as the consequence of not having spent enough.

Yes, US public debt has exploded, particularly since the 2008 financial crisis and then again the Covid outbreak of 2020.

And inflation is near a 40-year high.

Then we have 19 consecutive months of negative wage growth in the US.

Biden is apparently doubling down on “Green Schemes” now that the US House of Lords (aka, Senate) remain under Keynesian control (aka, Democrat). So watch for inflation to start increasing again.

You must be logged in to post a comment.