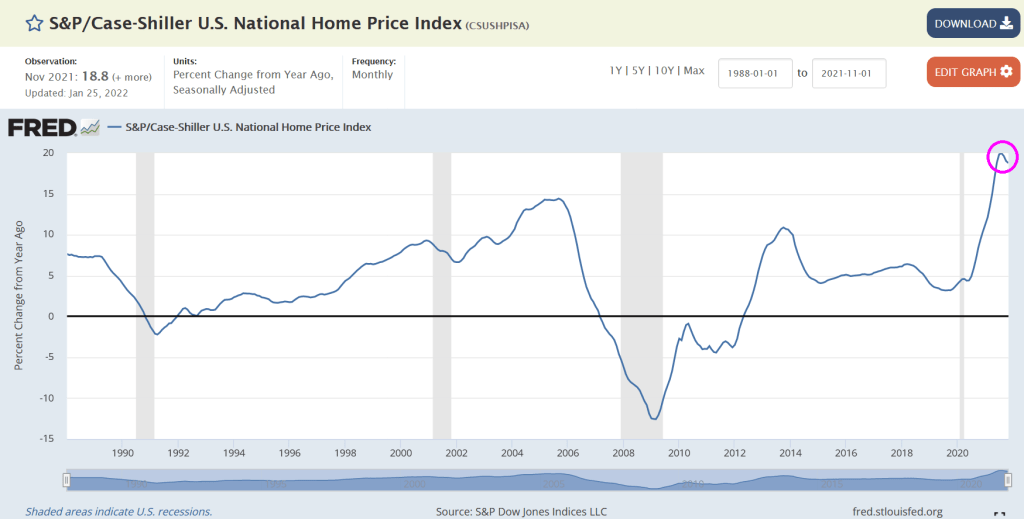

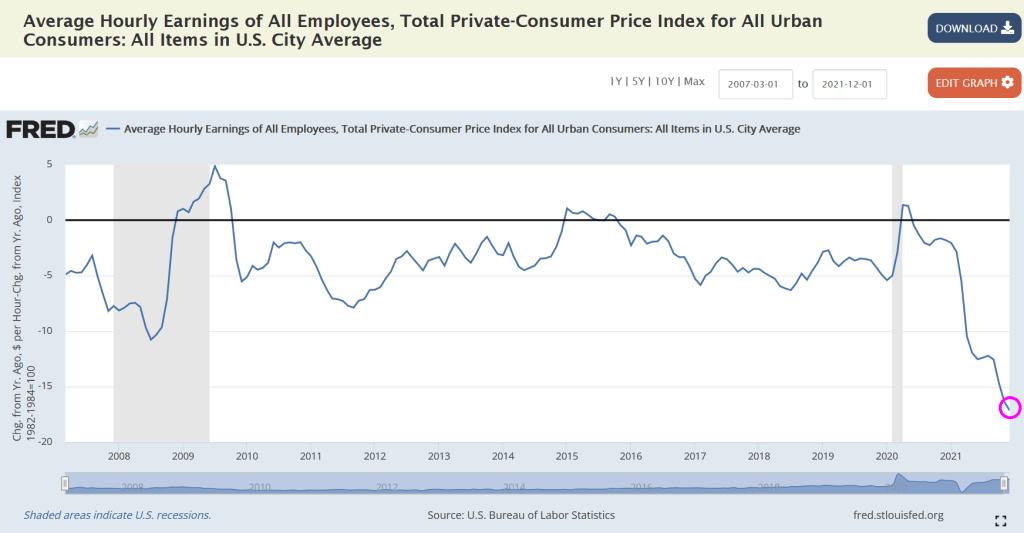

In January 2020, just prior to the COVID outbreak in the US, the Case-Shiller national home price index was growing at 4% YoY, the Zilliow rent index (all homes) was growing at 2.92% YoY and REAL average hourly earnings were growing at 0.52% YoY.

Then COVID struck and the Federal government dumped trillions of dollars of stimulus into the economy and The Federal Reserve massively expanded its balance sheet. Now the US has home prices growing at a 18.8% rate, rents (for those who can’t afford to purchase a home) growing at 14.91% and REAL hourly earnings growing at -1.80%.

The site Apartment List has an even bleaker view of rent growth, with rents in January 2022 having grown by 18% YoY.

Now that COVID is fading, we see New York City rents growing at 33.5% YoY followed by Florida and Arizona cities at 29.3% and higher rates. Irvine CA is seventh at 28%. The slowest growing city is Oakland, CA is growing at only 0.5%.

If The Fed does its expected “shock and awe” (or shock and awful), it will be more than the stock markets will crash. The housing market could crash too.

Take the current US housing situation with its limited inventory of listings combined with massive Fed stimulypto.

US 1-unit housing starts are down -4.1% in January. But heck, it is January! But on a year-over-year basis, 1-unit housing starts are down -2.4%. But what will happen if The Fed ACTUALLY withdraws its gargantuan monetary stimulus (green line)?

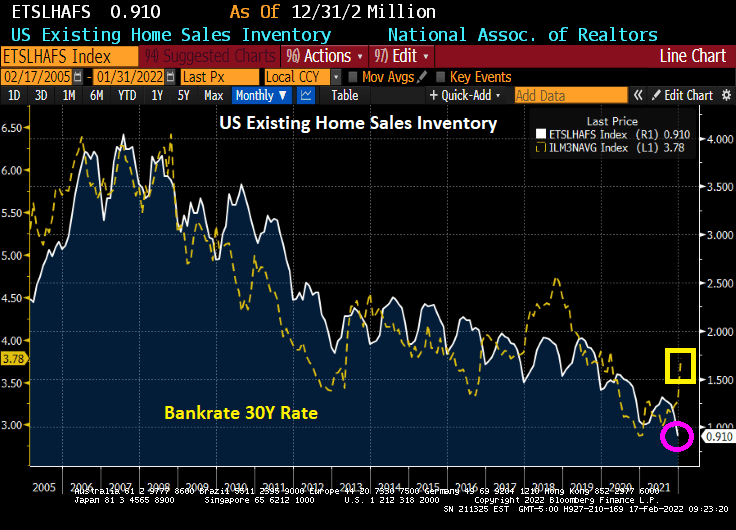

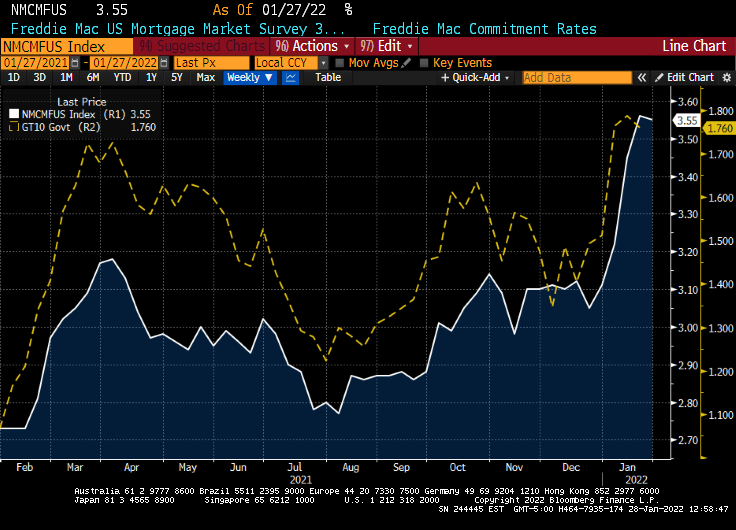

Existing home sales inventory continues to decline as Bankrate’s 30-year mortgage rate starts to climb with expectations of Fed “Shock and Awful.”

Say hello to The Federal Reserve Board of Governors!

How bad is inflation in the USA? Try 18%, based on the Flexible Consumer Price Index.

The Flexible Price Consumer Price Index (CPI) is calculated from a subset of goods and services included in the CPI that change price relatively frequently. Because flexible prices are quick to change, it assumes that when these prices are set, they incorporate less of an expectation about future inflation.

Again, remember that Federal inflation numbers woefully undercount housing and rent inflation. For example, the Case-Shiller National Home Price index (as of November 2021) was growing at 18.8%.

The sad part is that inflation-adjusted average hourly earnings growth of all employees is crashing thanks to inflation.

(Bloomberg) — The White House is lowering expectations for this week’s U.S. jobs report, saying that brief absences of workers due to omicron could overstate the number of unemployed people for last month.

Several White House officials have teed up Friday’s report with warnings, saying that the week when surveys were taken for the January payroll numbers was the height of illness absences in the aftermath of the holidays.

Brian Deese, the director of President Joe Biden’s National Economic Council, said the numbers could be “confusing” as Covid illnesses are recorded as job losses.

“We expect that that will have an impact on the numbers,” Deese told MSNBC on Tuesday. “We never put too much weight on any individual month; this will particularly be true in this month, because of the likely effect of the short-term absences from omicron.”

Biden has repeatedly touted employment data as an indicator of a robust economic rebound, and highlighted the tumbling jobless rate to blunt criticisms about overheated inflation. Friday’s report may still show historically low unemployment, which is based on a separate survey from the one for payrolls and counts temporary, unpaid sick leave differently.

LaborSecretary Marty Walsh and White House Press Secretary Jen Psaki have also delivered warnings that the official January jobs gain may be poor.

If a worker was out “and did not receive paid leave, they are counted as having lost their job,” Psaki said Monday. Nearly 9 million people missed work due to illness in January, when the data were being collected, she said.

“So we just wanted to kind of prepare, you know, people to understand how the data is taken,” she said. “As a result, the month’s jobs report may show job losses in large part because workers were out sick from omicron.”

Economists expect nonfarm payrolls to rise by 150,000 for January — the weakest reading since the end of 2020. The U.S. unemployment rate is seen remaining unchanged, at 3.9%, according to the median estimate of forecasts compiled by Bloomberg.

So, are Dreese and Psaki saying that US GDP will roar back … from 0.1% … if Omicron fades away? And that all the fiscal and monetary stimulypto are going to cease creating problems??

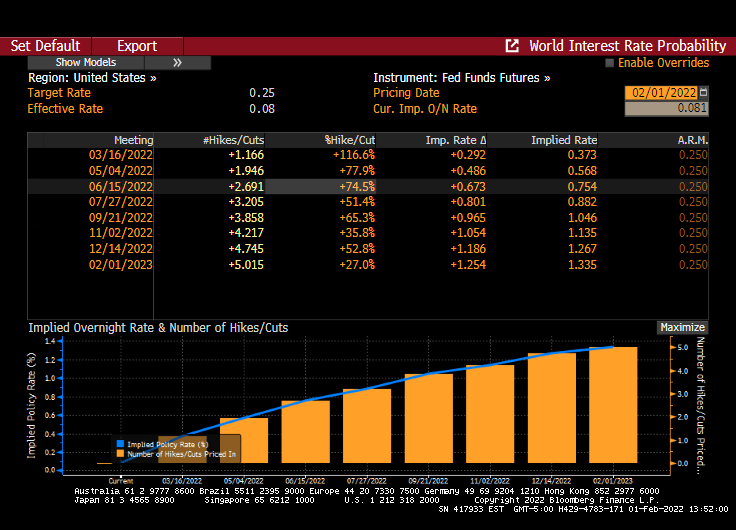

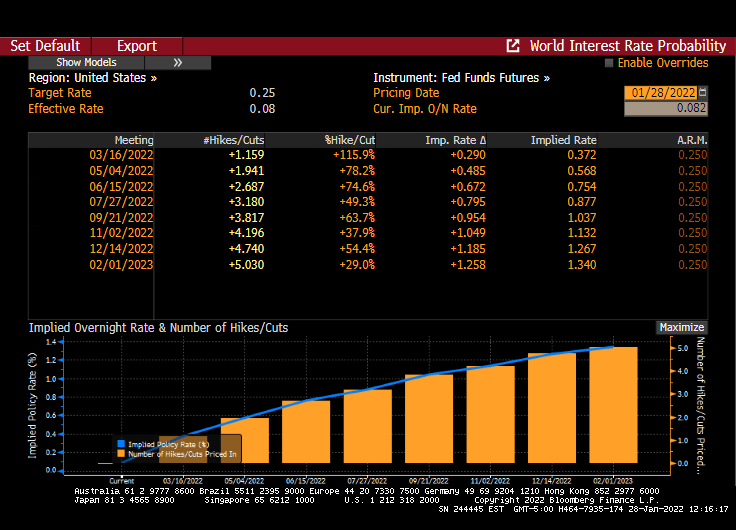

Despite the fear of Omicron in the upcoming jobs report, there are still 5 rate hikes on the horizon to combat inflation … created by the Biden Administration and Federal Reserve as they combated COVID with massive fiscal and monetary stimulus.

But don’t worry, the Biden Administration ordered rapid test kits from China … and they have arrived!

Yes, its a cold one out there. But the Biden Administration is engaging in reducing fossil fuel supply and pushing towards “green” energy such as inefficient solar panels, eagle-killing wind turbines, and ocean turbines.

As a consequence, natural gas futures are up 93% from January 1, 2021 while coal futures are up 133% and WTI Crude spot price is up 82%.

Any wonder why food prices are up 40%?

Stay warm. It’s a cold one out there today. And The Federal government doesn’t care.

Raphael Bostic and Goldman Sachs are both calling for dramatic rate increases to fight inflation … that they helped cause with their monetary stimulypto. I call this The Fed’s March of the Toreadors as The Fed now attempts to kill the bull market.

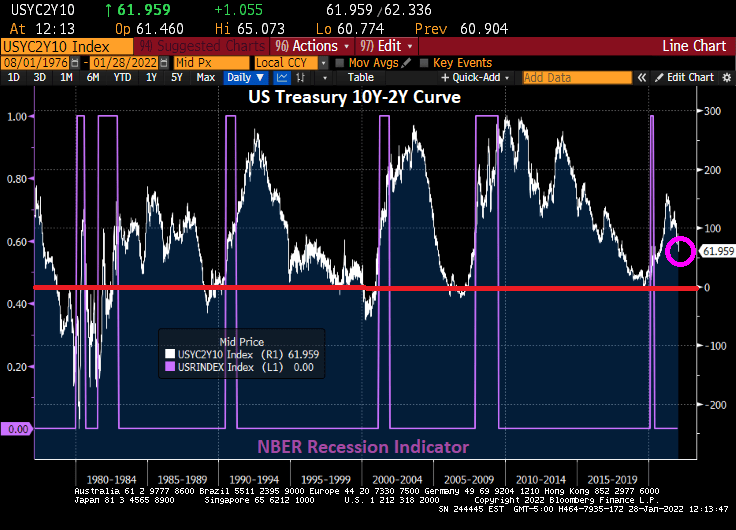

(Bloomberg) — The Treasury yield curve flattened to the lowest level in over a year on Monday as the prospect of a super-sized Federal Reserve rate increase in March gained traction, weighing disproportionately on shorter-dated tenors.

Two-year U.S. yields climbed as much as 4 basis points after Raphael Bostic, the president of the Fed’s Atlanta branch, said the U.S. central bank could raise its benchmark rate by 50 basis points if a more aggressive approach to taming inflation is needed.

That narrowed the gap with ten-year counterparts — which rose about half as much — to the least since October 2020. The last time the Fed delivered a half-point increase to borrowing costs was at the height of the dot-com bubble in 2000.

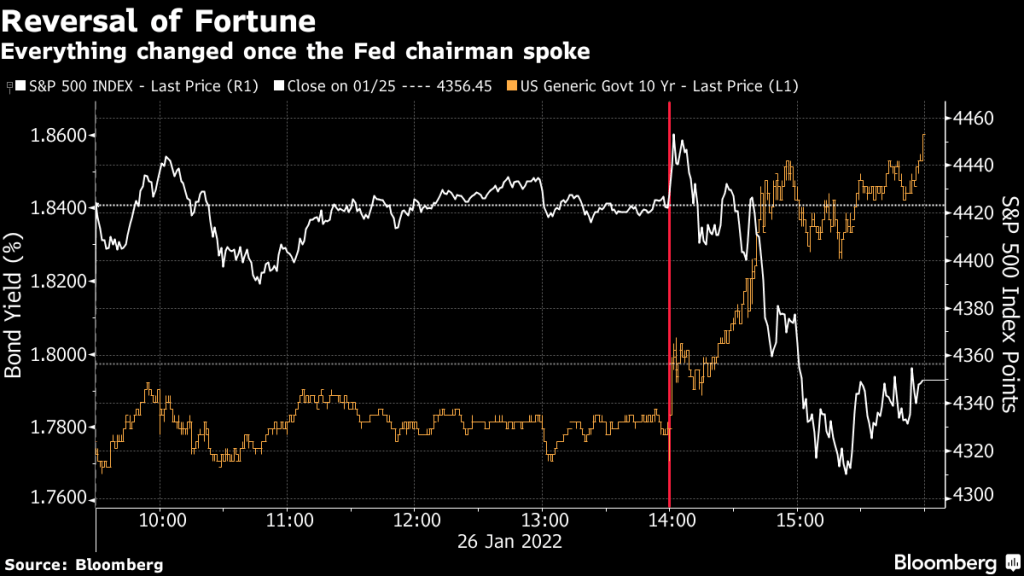

The repricing extended a move spurred last week, after Fed Chair Jerome Powell underscored the policy maker’s determination to put a lid on inflation. The market positioning may have been exacerbated by hedge funds that had been leaning the wrong way before Powell’s address.

Traders are currently betting the Fed will deliver 32 basis points of tightening in March, more than fully pricing an increase of a quarter-point. That puts the implied probability of a 50-basis-point increase at almost 30%. The odds of such a move in December were zero.

Consumer prices rose an annual 7% in December, the fastest pace in almost four decades. Powell left the door open to increasing rates at every meeting, and didn’t rule out the possibility of a 50-basis-point hike.

In an interview with the Financial Times, Bostic stuck to his call for three quarter-point interest rate increases in 2022, while saying that a more aggressive approach was possible if warranted by the economic data. Bostic is a non-voting member of the FOMC this year.

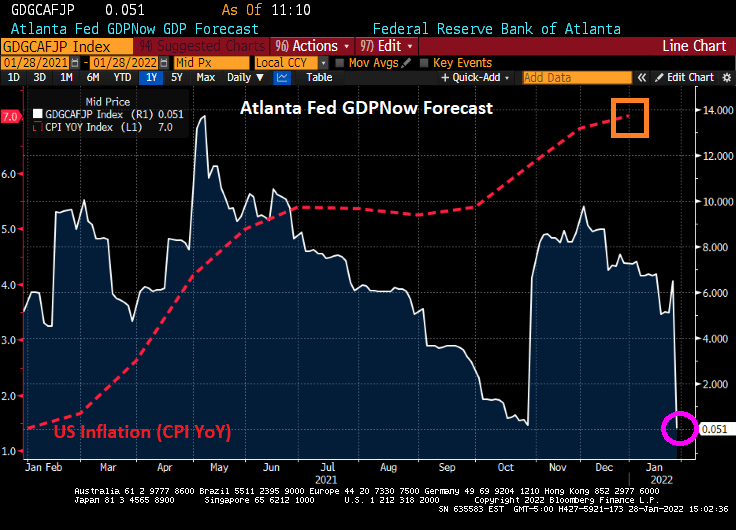

Since the rapid growth in inflation was caused by a combination of too much Fed stimulus, too much fiscal stimulus and “green” energy policies, it is unclear whether an increase of 50 basis points will do much, particularly if Bostic’s own Atlanta Fed GDPNow forecast of 0.051% is accurate. Raising ratesif the economy is slowing??

To be clear, Bostic and others are trying to signal The Fed’s intent well in advance to avoid a surprise knock-down of the stock market. Or a killing of the bull market.

No, not the Klaus von Bulow type of “reversal of fortune” (when he killed his wife). I am talking about a reversal in fortune for America.

Let’s look at the 10Y-2Y Treasury curve. It typically falls below 0 basis points before every recession. Except the mini-COVID recession of 2020. But notice that the Treasury curve did not recover from the COVID recession as it typically did. More along the lines of 1984-1985.

Speaking of Reversal of Fortune, everything changed once Fed Chair Powell started to speak after Tuesday’s FOMC meeting.

Hmm. Midterm elections, possible Russian invasion of The Ukraine, further problems in China, etc. While The Fed Funds Future data implies that The Fed may raise their target rate 5 times over the coming year, we’ll see.

If 2021 was a great year for the US housing market, 2022 faces “a new normal” marked by a slowing down of home price rises, job layoffs in the mortgage industry, and concerns over rising inflation and interest rate hikes, according to Douglas Duncan (pictured), Fannie Mae’s senior vice president and chief economist.

Duncan said “a shift” was underway in the market and the wider economy, which would result in far more moderate home price appreciation, expected to be between 7% and 7.5% this year due to the ending of fiscal and monetary stimulus.

“One of the elements of the shift is that you’re going to see house prices up, but not nearly as far as they were in the last two years because that was driven hugely by the fiscal and monetary stimulus (now) being removed,” he told MPA.

Ominously, he added that low interest rates “may never be seen again”. Or at least until Biden appoints more doves to The Federal Reserve Board of Governors.

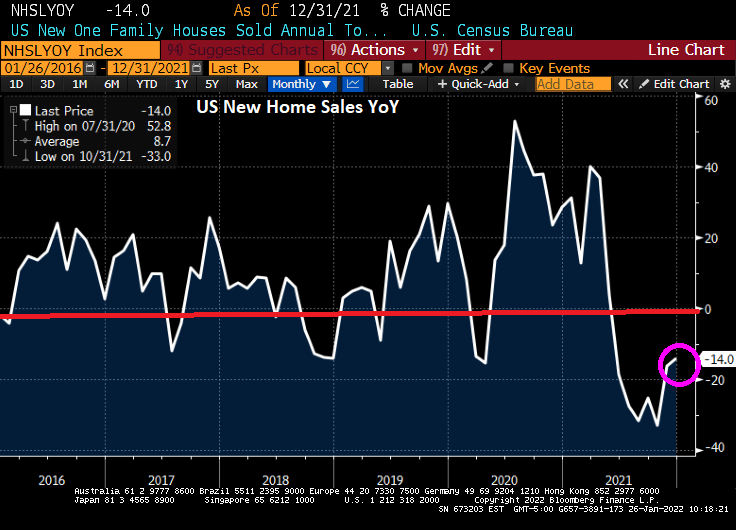

US new home sales spiked in December by 11.9% from November, but were down 14% year-over-year.

But the median price of new home sales (YoY) declined to 3.4%.

The Midwest saw a surge in new home sales (+56%).

The MBA’s mortgage applications index shows declining purchase applications (-1.83%) and declining refinancing applications (-12.60%) as mortgage rates increased from 3.64% to 3.72% for the week of 01/21.

Now, mortgage purchase applications rose for the week of 01/21 if we used non-seasonally adjusted data.

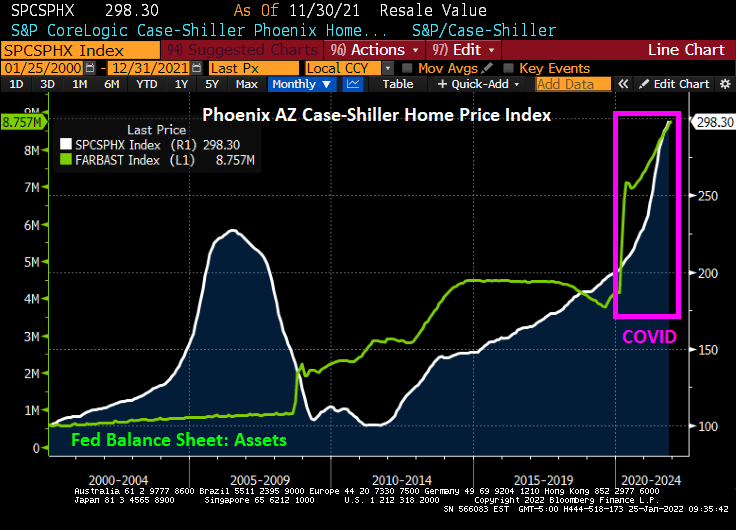

The Case-Shiller National home price index “slowed” to 18.81% YoY in November as The Fed continues its monetary stimulypto. Notice that The Fed is easing even when there is limited inventory available. Result? Hideous home price inflation.

Which metro area is growing the fastest, making housing even more unaffordable for renters? Phoenix AZ is growing at a 32.2% YoY clip while Washington DC is the slowest growing metro area at 11.1% YoY. The second faster growing metro area in Tampa FLA.

Phoenix AZ is growing at the fastest rate in the nation as The Fed still has its monetary stimulus at FULL SPEED AHEAD.

Is this the bubble burst many were expecting once The Federal Reserve starting raising rates?

Well, if today’s market opening is an indication, the answer is yes. The NASDAQ Composite Index is down 1.36% and West Texas Intermediate Crude Oil futures prices are down 2%.

The S&P 500 index is down over 10% since January 3rd.

Drawdown is taking place.

But if you think the US equities are deflating, look at European equities. The Euro Stoxx 50 index is down 4.04%.

You must be logged in to post a comment.