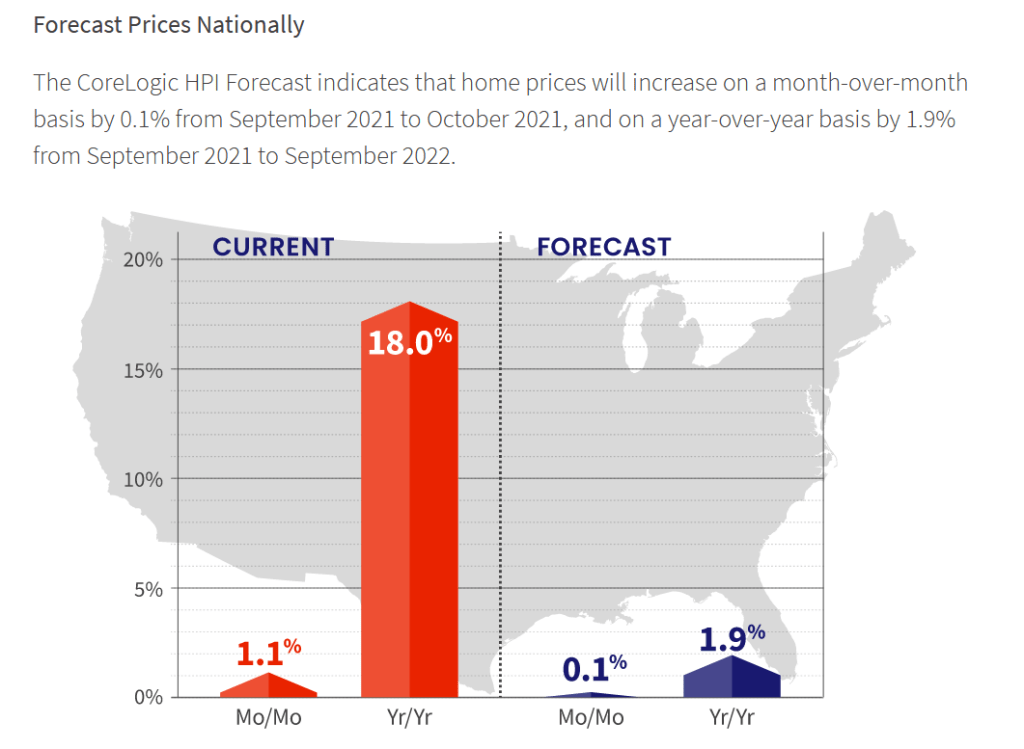

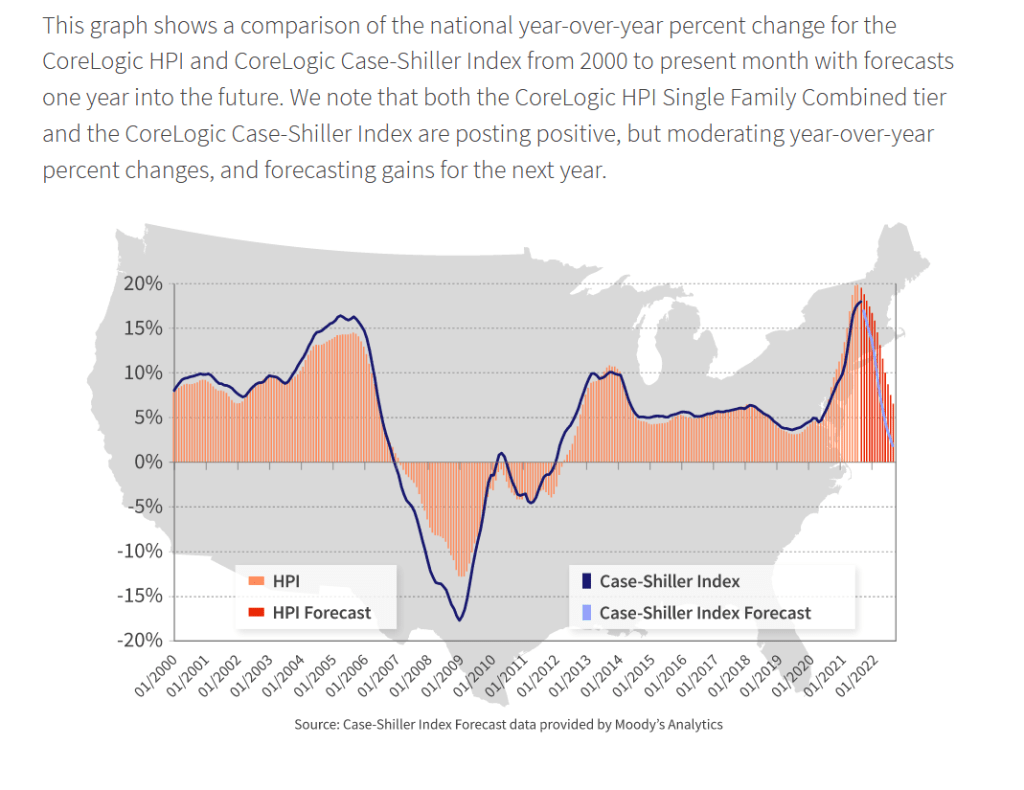

But the forecast for home price growth is for 1.9% YoY in 2022.

As home price growth crashes back to earth as wages don’t keep pace with home prices.

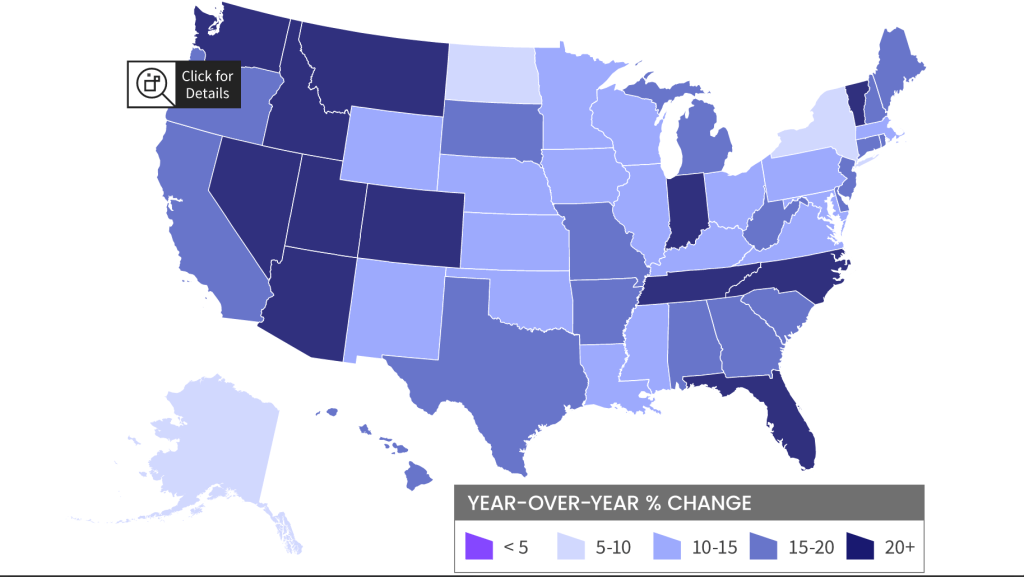

Home prices have been growing in most states out west where The Fed’s money pump has resulted in a boom in second homes and people escaping high tax California and Oregon for Nevada, Idaho, Arizona (again), Utah and Montana. The east coast is seeing the Carolinas booming along with Florida and Indiana. Escape from New York?

Escape from LA … to Arizona, Nevada, Idaho and Utah?

Federal Reserve Chair Jerome Powell sounded a note of heightened concern over persistently high inflation as he made clear that the central bank will begin tapering its bond purchases shortly but remain patient on raising interest rates.

“The risks are clearly now to longer and more persistent bottlenecks, and thus to higher inflation,” Powell said Friday during a virtual panel discussion hosted by the South African Reserve Bank and moderated by Bloomberg’s Francine Lacqua.

“I would say our policy is well-positioned to manage a range of plausible outcomes,” he said. “I do think it’s time to taper and I don’t think it’s time to raise rates.”

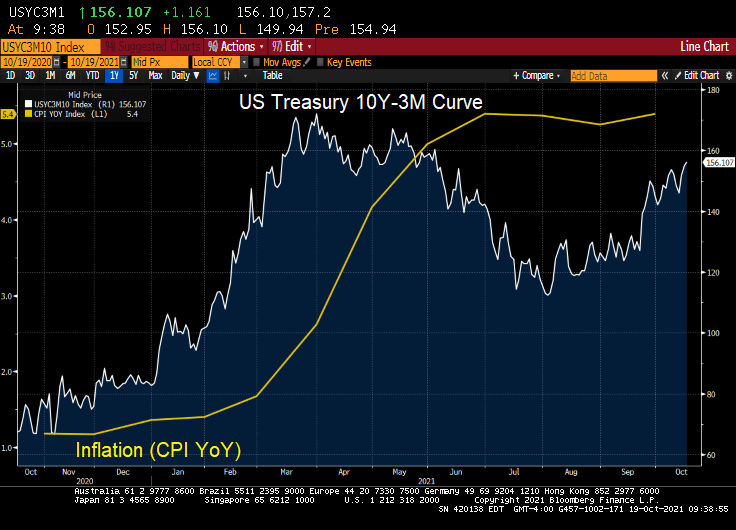

Good luck with that, Jay! You are going to raise the short-end of the yield that will lead to a flattening of the Treasury yield curve. But you are going to continue to buy Treasuries and Agency MBS in order to monetize the rampant spending by Congress and the Biden Administration? C’mon man!

You can see where Powell spoke today. It is when gold tanked along with the 10-year Treasury yield. Both rebounded a bit, but the 10-year Treasury yield continue its fall to 1.6324%.

The US dollar (green) fell when Powell opened his pie-hole. But Bitcoin (blue) fell in advance as if they knew what Powell was going to say.

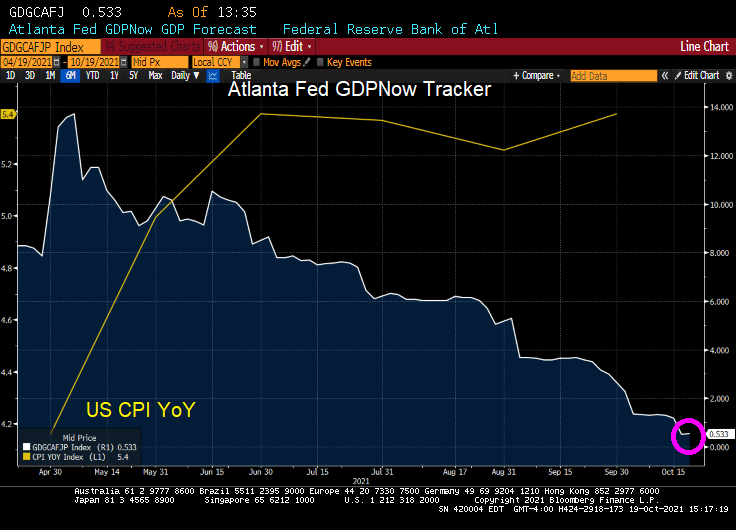

The Atlanta Fed’s GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2021 is 0.5percent on October 19, down from 1.2 percent on October 15. After recent releases from the US Census Bureau and the Federal Reserve Board of Governors, the nowcasts of third-quarter real personal consumption expenditures growth and third-quarter real gross private domestic investment growth decreased from 0.9 percent and 10.6 percent, respectively, to 0.4 percent and 8.4 percent, respectively.

US real GDP nosedived to 0.5% according to the Atlanta Fed GDPNow real-time tracker.

Again, The Fed and Federal government pumped trillions of stimulus into an unprepared economy resulting in massive bottlenecks. So, we are getting declining GDP and rising inflation.

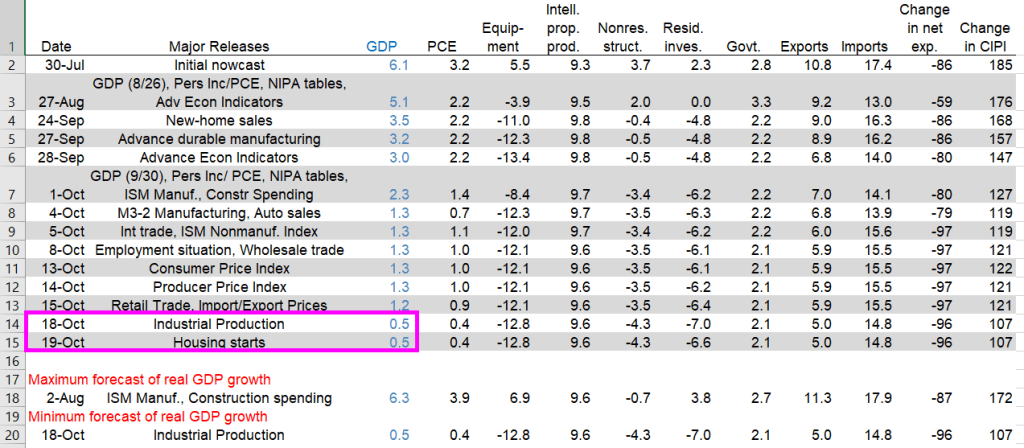

Yesterday’s industrial production dove leading to the 0.5% GDP figure. Today’s housing starts didn’t impact GDP in a meaningful way.

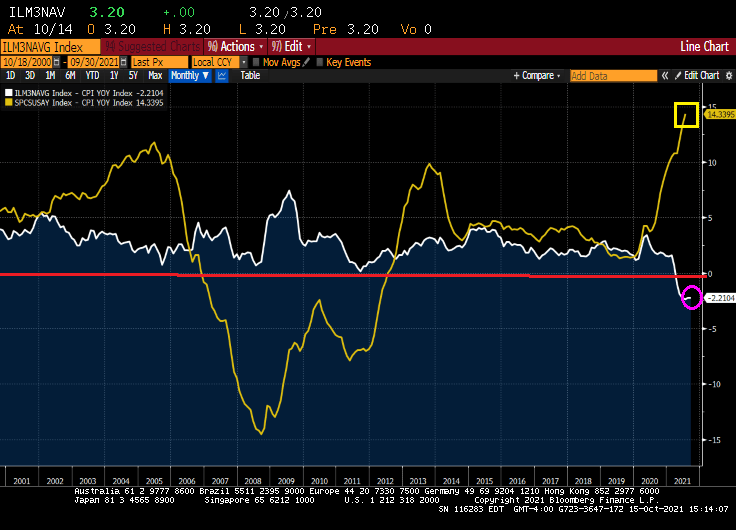

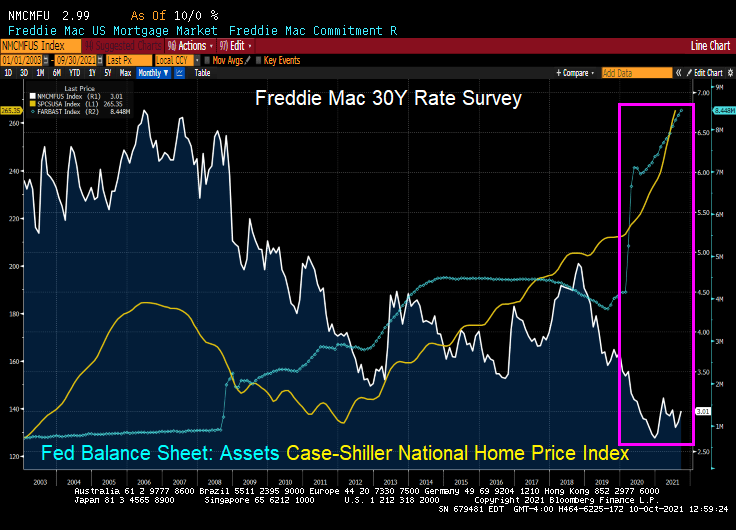

This is a time even unlike the disastrous housing bubble of the 2000s that led to the financial crisis and Great Recession. Even during the housing bubble years, we still had positive REAL mortgage rates: Bankrate 30Y Fixed rate – CPI YoY. But today we have even FASTER REAL home price growth and NEGATIVE mortgage rates!

And yes, REAL home price growth is 14.34% YoY while REAL hourly earnings growth is -0.79%.

The University of Michigan consumer survey came out today and buying conditions for housing improved to 75. Which means that more people were negative than positive due to skyrocketing home prices.

With negative 30Y mortgage rates and rising apartment rents, is it time to buy? Just remember what happened to Leon in Blade Runner.

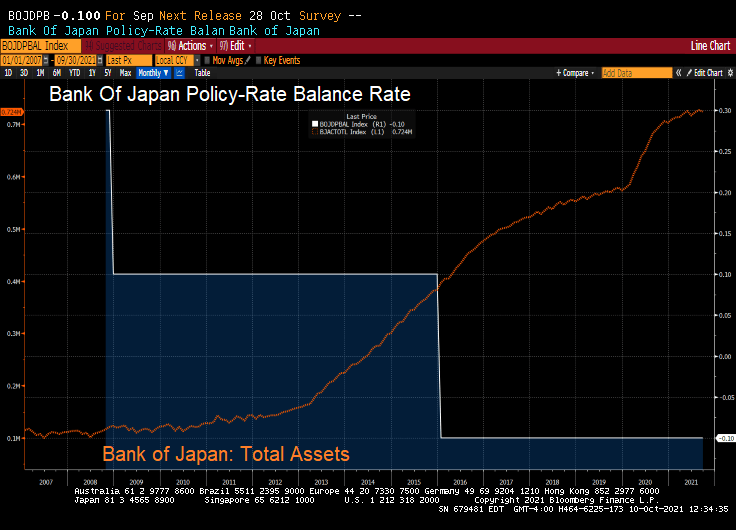

What’s left of it is that the BoJ (and Bank of Japan Governor Haruhiko Kuroda) now holds about half of the huge pile of the central government’s debt. With their target rate at -0.10% and a gargantuan balance sheet, what could go wrong?

But BOJ’s QE has ended. The BoJ’s overall assets stopped growing, and its holdings of government bonds have started to decline.

As of the BoJ’s balance sheet dated September 30, released on Thursday, total assets declined to a still monstrous ¥724 trillion ($6.4 trillion), below where it had been in May 2021.

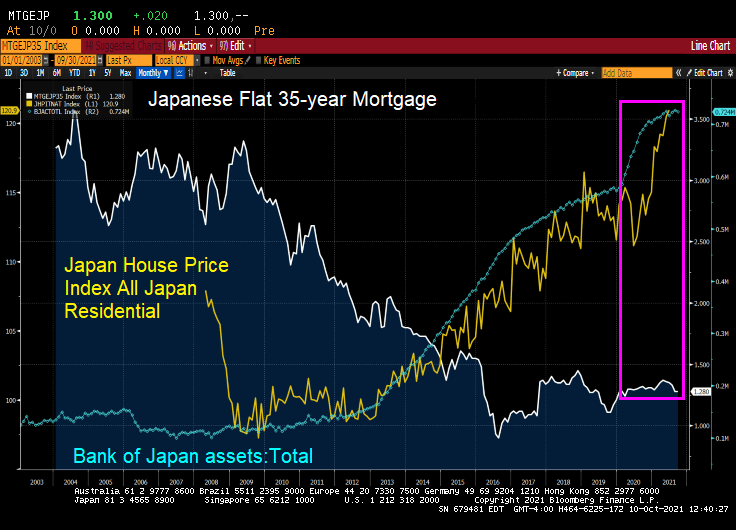

But look at Japanese home prices with the growth of the BOJ’s balance sheet and general decline in mortgage rates. Like the USA, there was a balance sheet spike associated with Covid and a resulting spike in home prices.

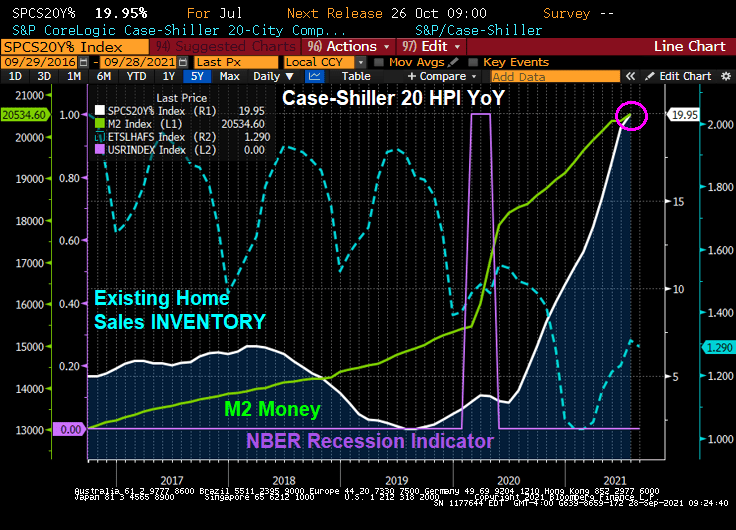

The USA? We also saw a surge in home prices following The Fed’s monetary “stimulypto.”

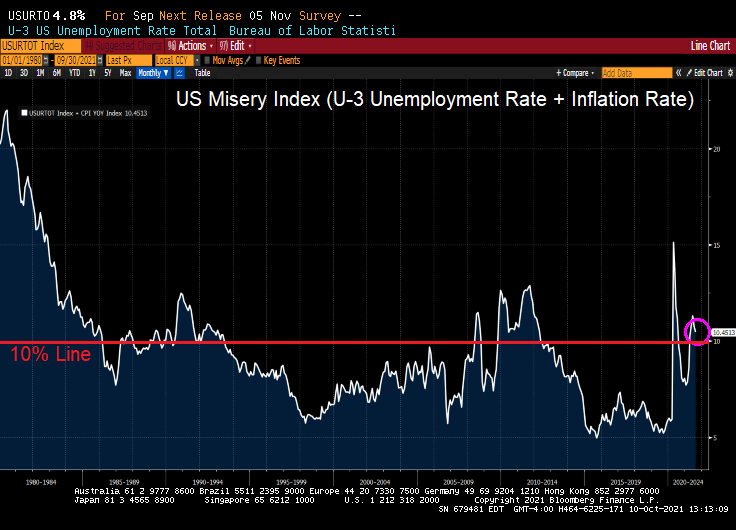

Bear in my that the US Misery Index is above 10% (U-3 unemployment + inflation).

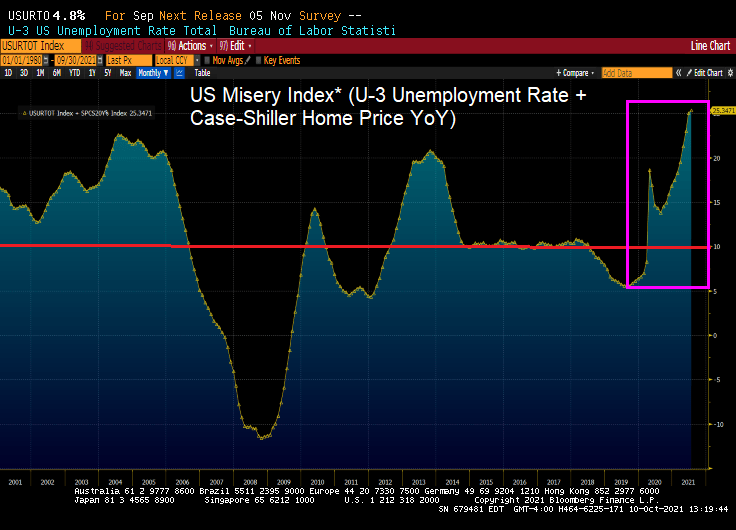

And if I define the US Misery Index as U-3 unemployment + home price growth, we can see we are at record misery rates. Miserable for households that don’t own a home or are trying to move to a higher housing price area).

So much for the transitory inflation that The Federal Reserve keeps spouting on about.

(Bloomberg) — The pace of rent increases is heating up in the U.S.

Rent data for the past two months show no sign yet of the usual seasonal dip at this time of year, following peaks early in the summer, when many lease renewals come due.

A Zillow Group Inc. index based on the mean of listed rents rose 11.5% in August from a year earlier, with some cities in Florida, Georgia and Washington state seeing increases of more than 25%.

Since the start of the pandemic, the median rent for a two-bedroom apartment has soared 13.1% to $1,663, Zumper data show.

But rent on newly-signed leases rose 17% from the previous tenant’s lease.

For the New York market, landlords are raising rent prices as much as 70% now that people are flooding back into the city as offices and entertainment venues open up. In July, the median asking rent in New York City surged to $3,000, compared with the pandemic low of $2,750 in January 2021, data from StreetEasy showed.

Of course, rent surge is not surprising given that home prices have surged since Covid given limited inventory and massive Fed stimulus.

Perhaps if The Fed and Federales (Federal government) start reducing their apocalyptic-level stimulus, THEN we will see inflation as transitory.

(Bloomberg) — The Federal Open Market Committee directed the New York Fed’s Desk to increase the size of the counterparty limit for the overnight reverse repo facility, according to a statement.

Per-counterparty limit increased to $160b/day from $80b/day, with the change taking effect Sept. 23

“The increase in the per-counterparty limit from the current level of $80 billion per day helps ensure that the ON RRP facility continues to support effective policy implementation,” according to statement. “All other ON RRP operation parameters remain the same”

And banks didn’t wait long to park $135.2b overnight at The Fed.

When combined with the ongoing expansion of the Fed’s balance sheet, we are seeing to see the expansion of the United States on Liquidity.

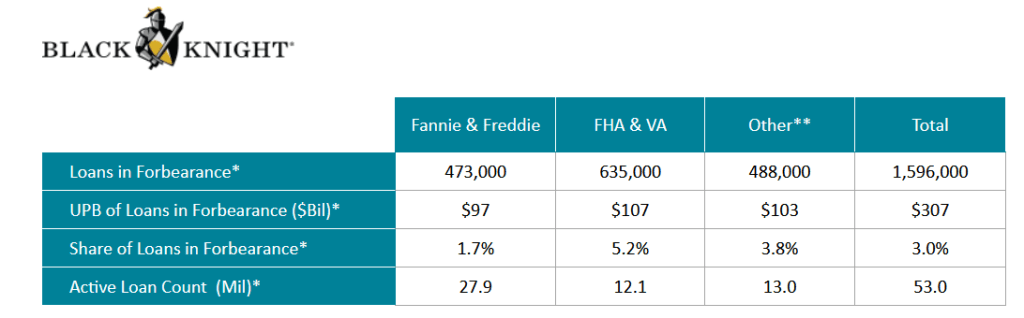

The Covid epidemic hit the single-family mortgage market hard in early 2020, leading mortgage lenders and servicers to offer FORBEARANCE to borrowers who were having trouble making their mortgage payments due to loss of hours or a loss of job.

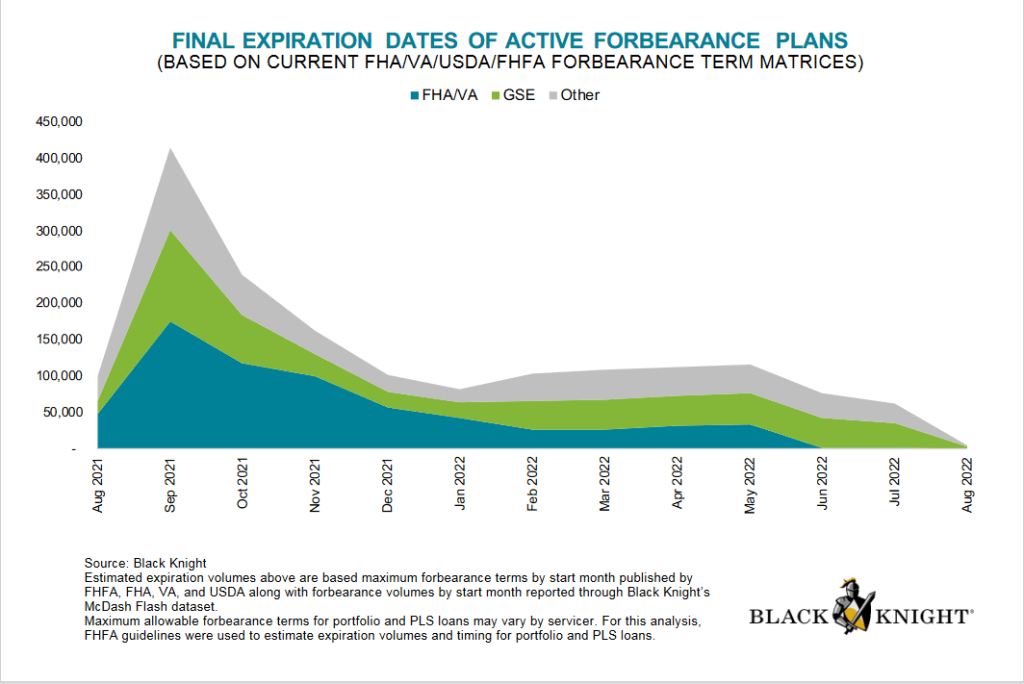

The good news? Active forbearance plans are much lower today than at their peak after the Covid epidemic struck in early 2020 with active forbearance plans peaking in May 2020.

Forbearance plans are due to expire in

What is forbearance, you ask? Forbearance is when a mortgage servicer or lender allows a borrower to temporarily pay their mortgage at a lower payment or pause paying your mortgage. The borrower will have to pay the payment reduction or the paused payments back later.

Despite forbearance, Fannie Mae still reported $7.2 billion in net income in Q2 2021. Notice the difference between single-family SDQ and the SDQ rate without forbearance. Freddie Mac reported $3.7 billion in Q2 2021 net income.

Here is a look at Fannie Mae’s net income over the past year and SDQ rates.

Under the existing seller/servicer eligibility requirements, the Agency SDQ Rate is defined as 100 multiplied by (the UPB of mortgage loans 90 days or more delinquent or in foreclosure for Fannie Mae, Freddie Mac, and Ginnie Mae/Total UPB of mortgage loans serviced for Fannie Mae, Freddie Mac, and Ginnie Mae). Beginning with the financial quarter ending Jun. 30, 2020, the Agency SDQ Rate will include an adjustment for mortgage loans in a COVID-19-related forbearance plan that are 90 days or more delinquent and were current at the inception of the COVID-19-related forbearance plan. The UPB of such mortgage loans shall be multiplied by .30 and added to the UPB for SDQ mortgage loans for the purposes of determining the numerator in the calculation of the Agency SDQ Rate.

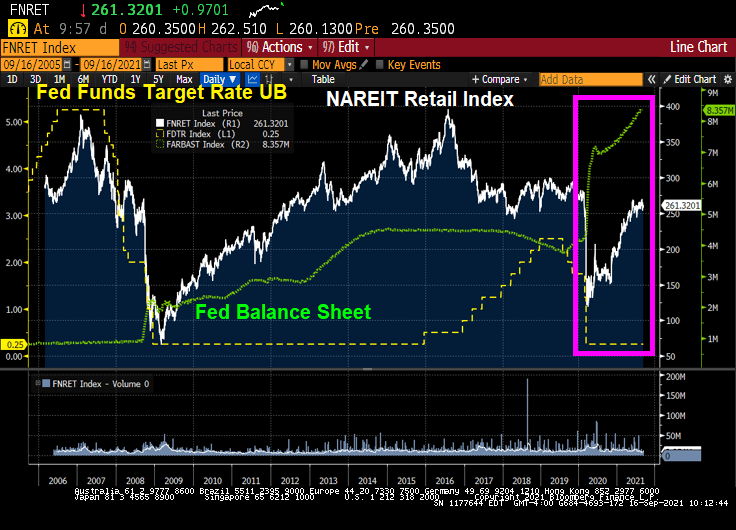

It is tough to operate a retail Real Estate Investment Trust (REIT) in the face of the triple whammy that hit retail shopping. First, there was the housing bubble/subprime crisis of 2008-2009. Then there was the advent of on-line shopping, then COVID.

I look at the NAREIT retail index and two retail REITs for comparison: Simon Property Group and Washington REIT. And as a proxy for online shopping, I compare them to Amazon. Both Washington REIT and the NAREIT retail index were at loft valuations at the peak of the housing bubble, but crashed with the onset of the housing bubble burst and ensuing financial crisis. But following The Great Recession, both recovered by 2016 (along with Simon Property Group which actually far exceeded their pre-Great Recession peak.

ii

But then retail mall disaster struck. In the form of on-line shopping. I use Amazon to represent on-line shopping. While NAREIT Retail and Simon fell from their 2016 peak, Washington REIT got clobbered.

Then Covid struck. When combined with on-line shopping and fear mongering by Anthony Fauci, retail REITs got hit hard. But all three have rebounded slightly since their nadir in 2020.

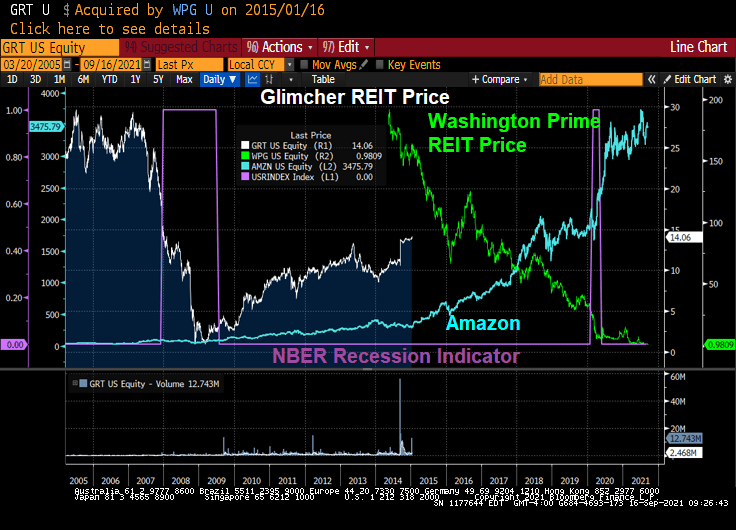

An interesting case study is Glimcher REIT, a formerly privately-held commercial real estate development company from Columbus Ohio. Like other retail REITs, Glimcher was crushed by the financial crisis and Great Recession. Glimcher’s share price fought back to $14.06 per share (down considerably from $29.28 in February 2007).

Washington Prime Group Inc. acquired Glimcher Realty Trust for $4.3 Billion in stock and cash Including the assumption of Glimcher’s debt. Right as on-line shopping took off. And the Covid struck a death blow leaving Washington Prime trading at $0.98. Washington REIT is transforming into a multifamily REIT given the overbuilding of DC area office space and the triple whammy of retail centers.

Retail REITs have almost recovered from Covid, thanks to the massive monetary stimulus from The Federal Reserve. Not to mention fiscal stimulus from DC.

Yup, a triple whammy has hit retail REITs with some faring better than others.

But the NAREIT RESIDENTIAL Index has exploded with Fed stimulus.

You must be logged in to post a comment.