Tavi Costa at Crescat Capital (founded by my former MBA student at University of Chicago Kevin Smith) produced this excellent chart of silver prices showing the cup and handle of silver prices.

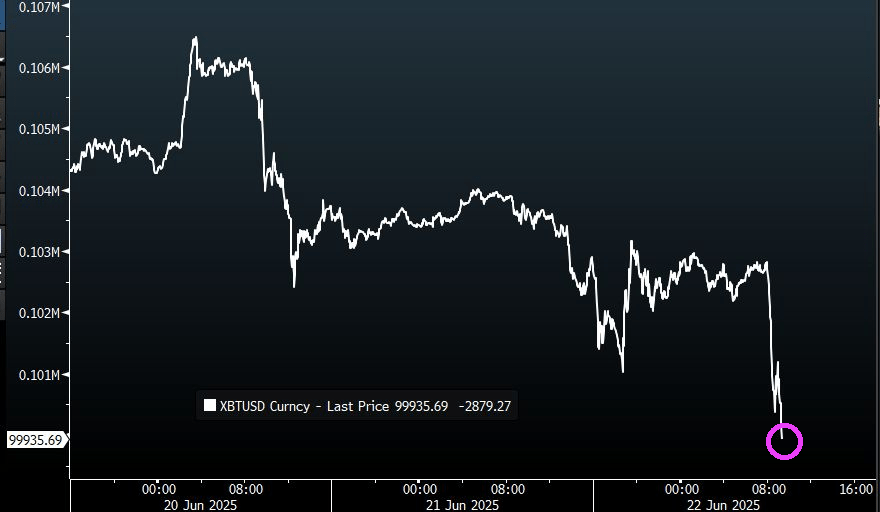

The rise in silver prices corresponds with a deterioration of the US bond market. Look at Treasury futures courtesy of Bravos Research.

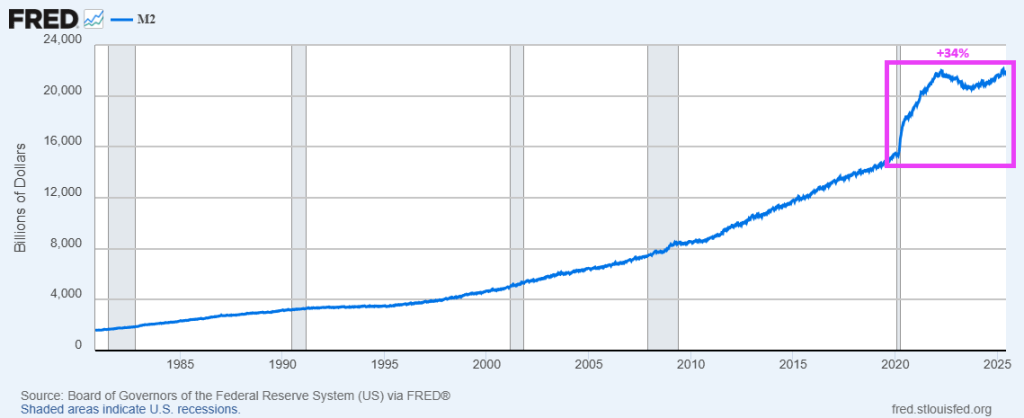

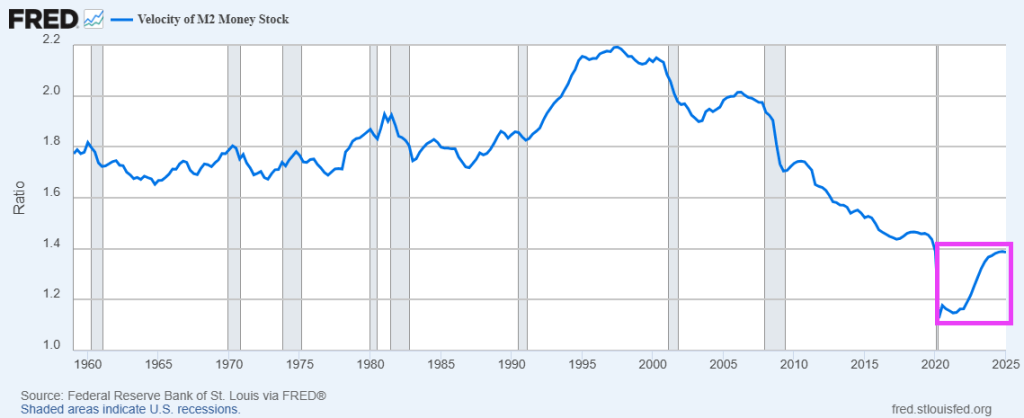

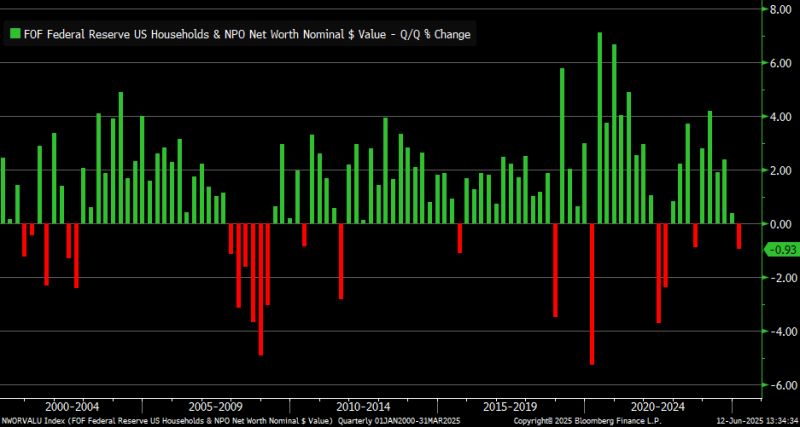

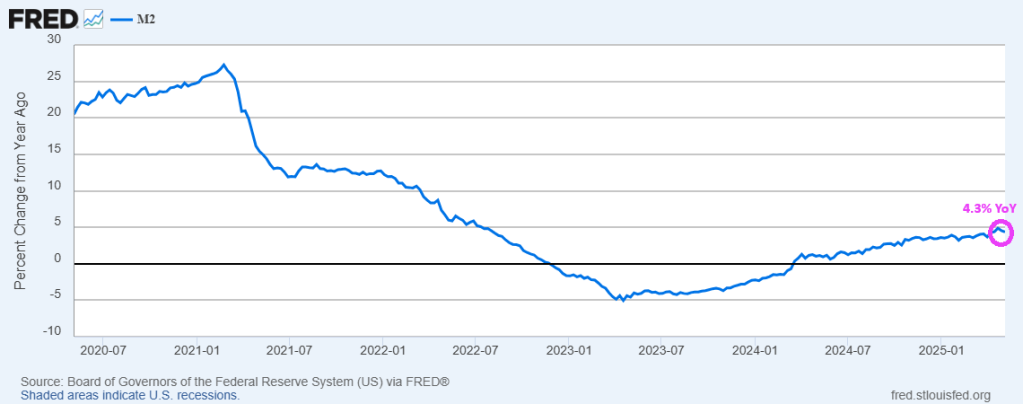

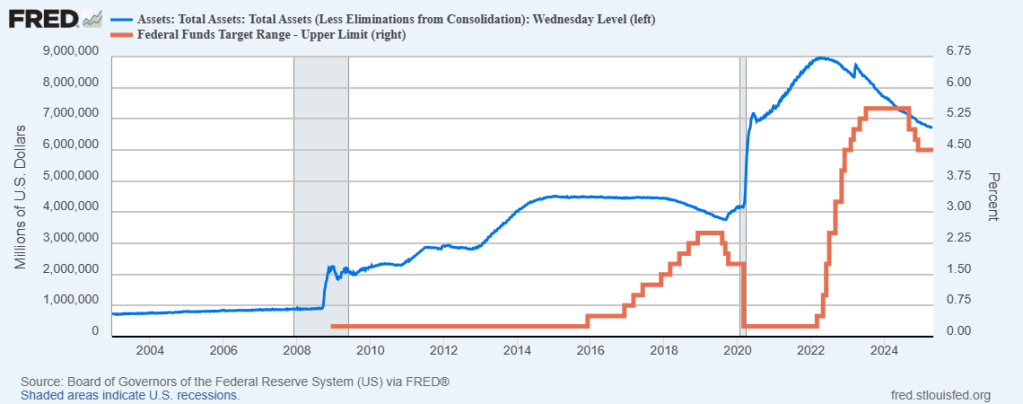

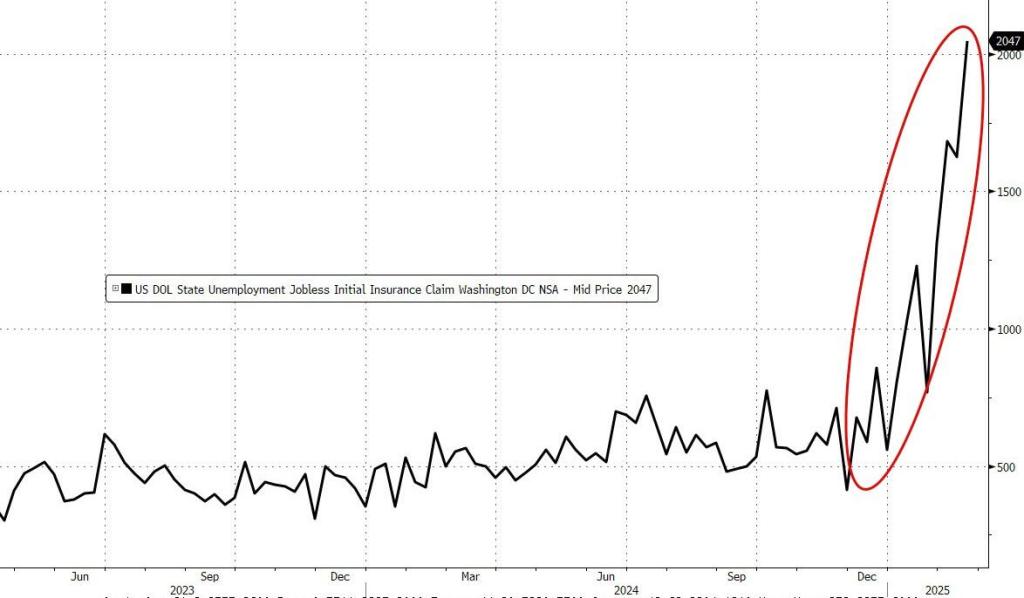

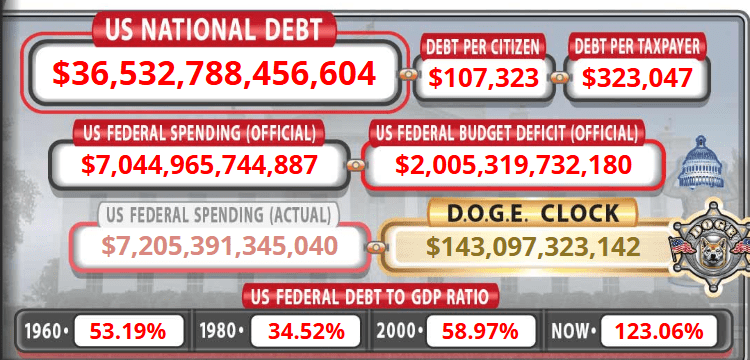

Of course, Washington DC’s insane spending has led to insane money printing by The Feral Reserve.

Everyone in Washington DC deserves a “Silver Cup of Failure” for uncontrolled government waste and spending and mismanagement by The Feral Reserve.

You must be logged in to post a comment.