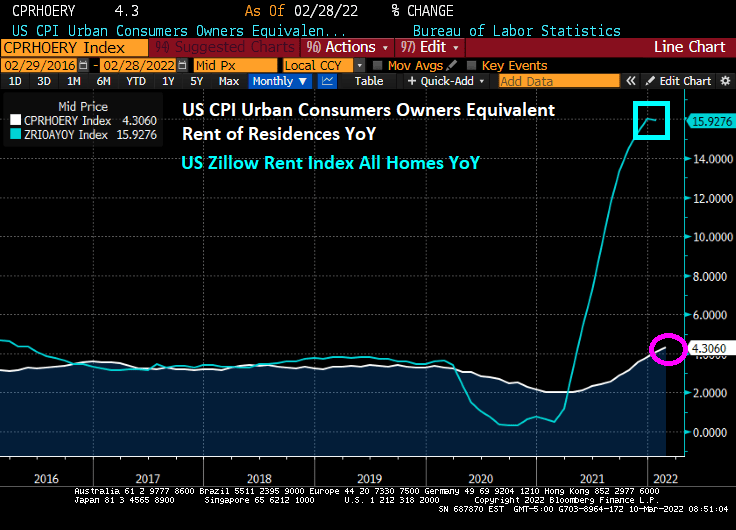

US rent inflation (owner’s equivalent rent of residence YoY) surged to 4.30%. However, Zillow’s rent index last month was 15.93% YoY.

But if we look at US Monthly Rent YoY, we see that rents are climbing at a 17.6% rate.

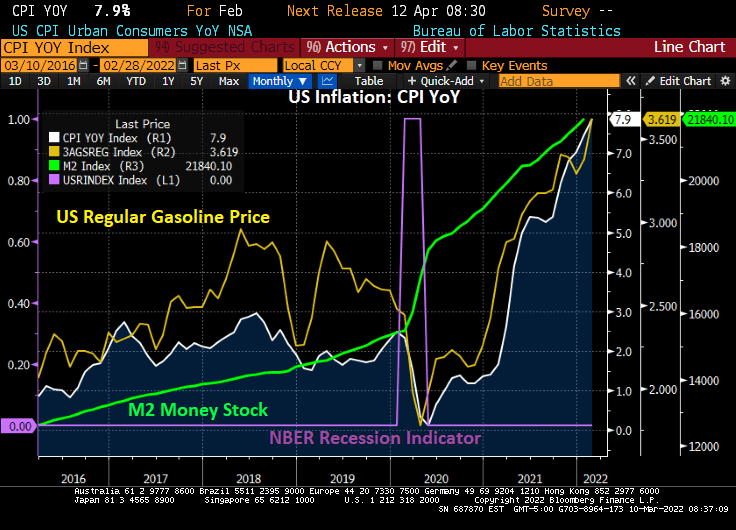

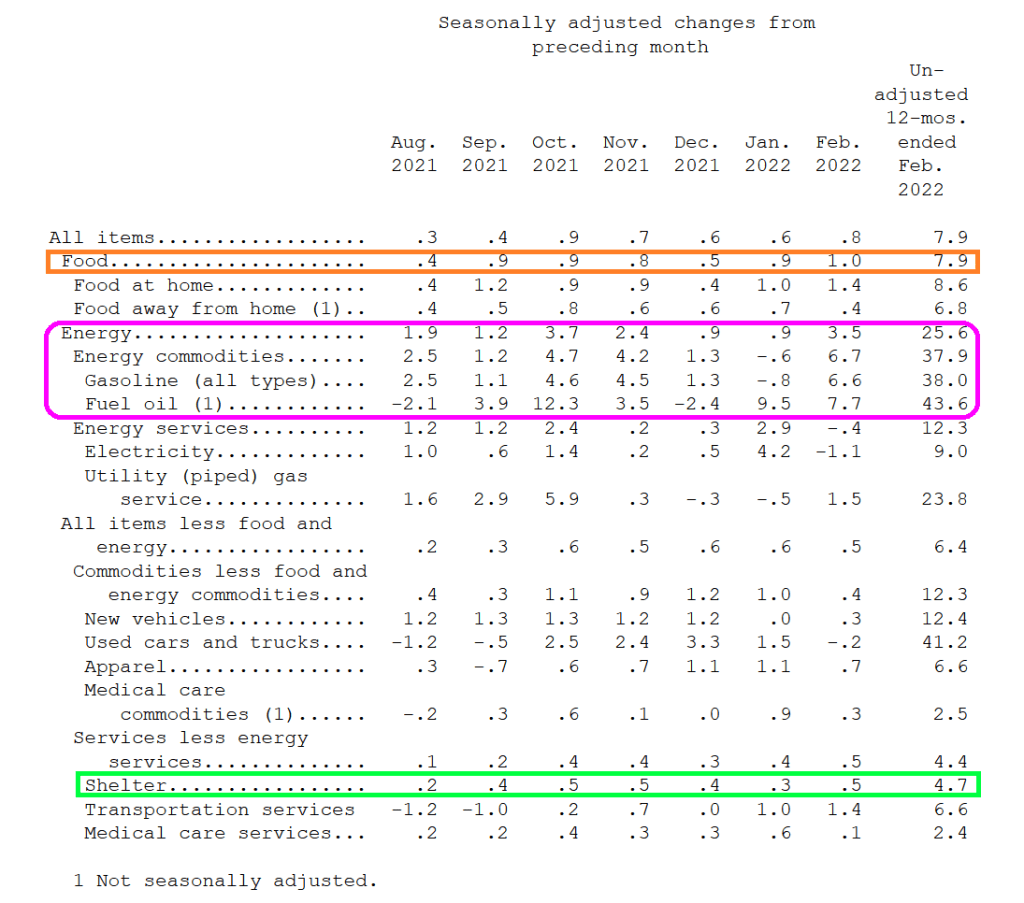

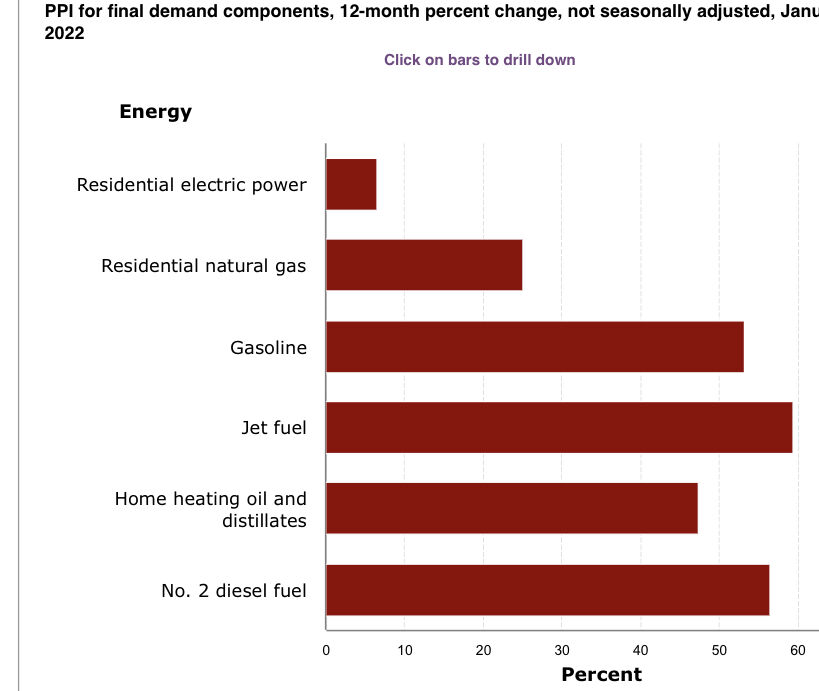

Energy costs soared in February YoY. Gasoline was up 38%. Fuel Oil was up 43.6%. Food was up 7.9%.

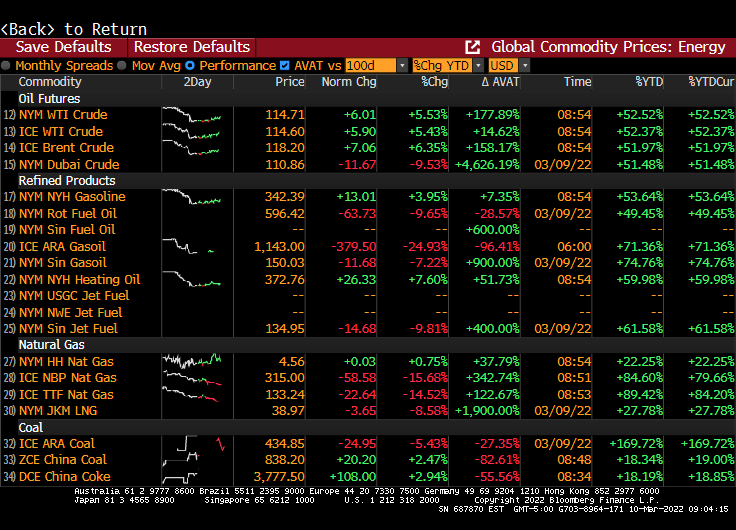

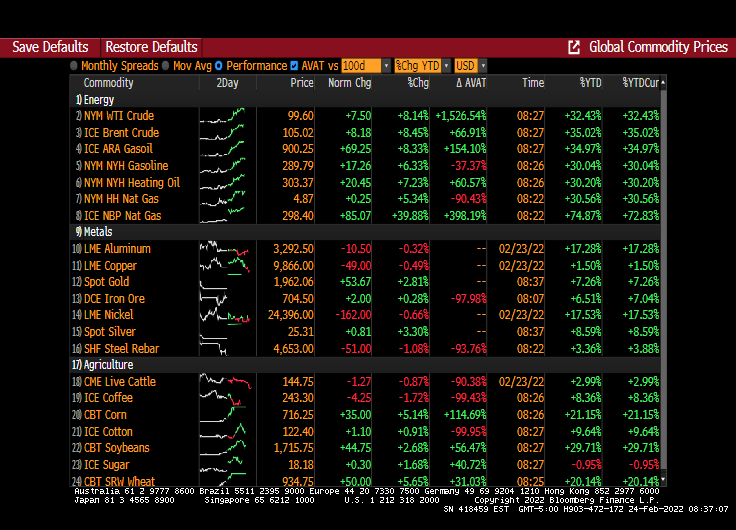

Volatility (AVAT) rages in the energy sector.

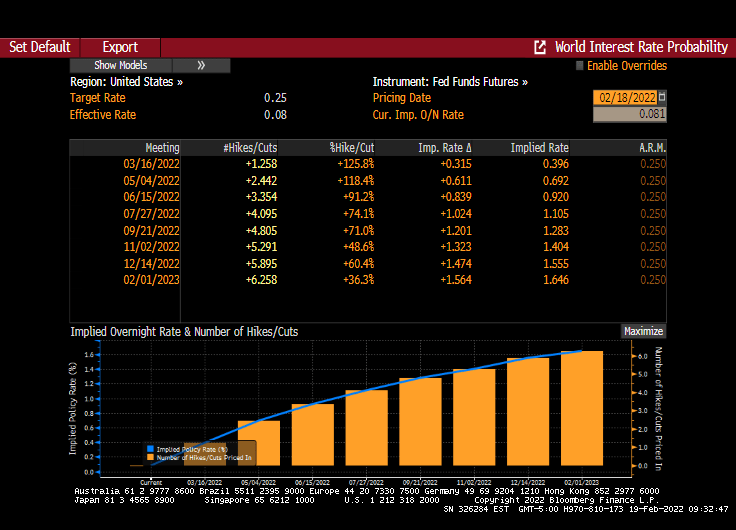

There are still 7 rate hikes in the cards from The Federal Reserve.

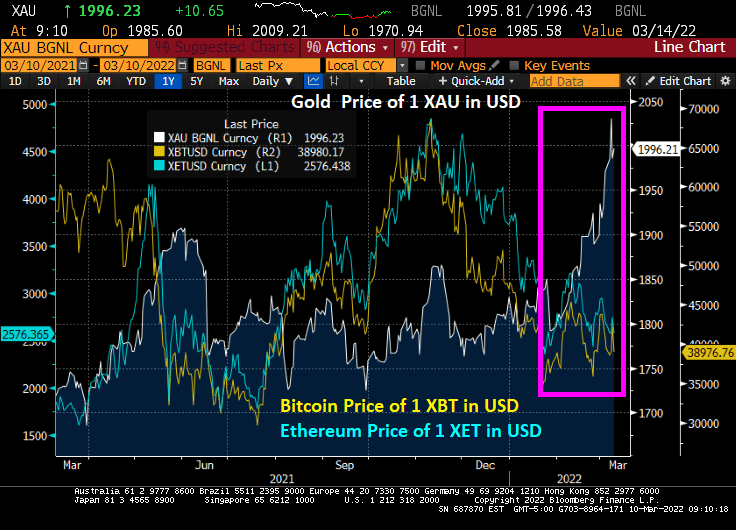

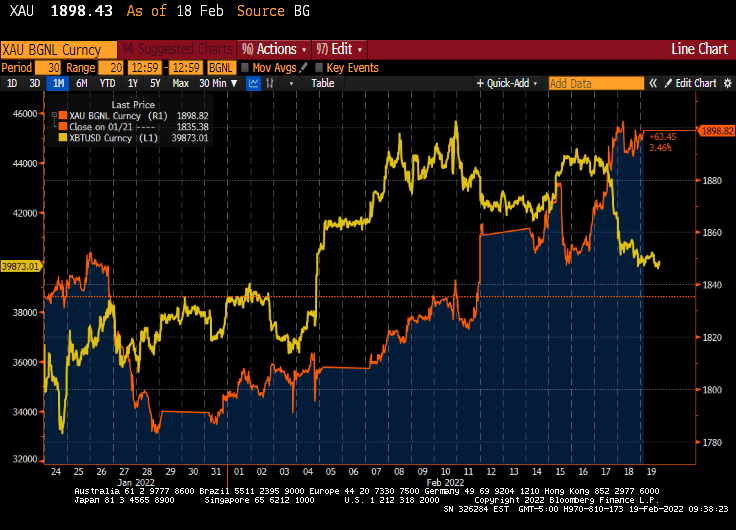

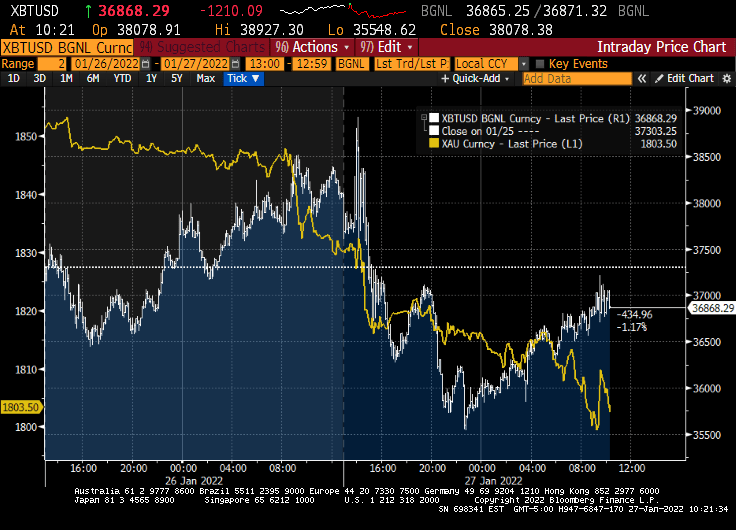

Gold has been climbing as Russia invades Ukraine. Cryptos Bitcoin and Ethereum are steady, even as the Biden Administration issues an executive order to “study” cryptocurrencies.

I admit, I follow market data to get a signal of what is happening to mortgage rates and I got one. With Putin and Russia invading Ukraine, markets are in turmoil

WTI Crude is up 8.14% this morning, Brent Crude is up 8.45% and NBP (UK) Natural gas is up 40%.

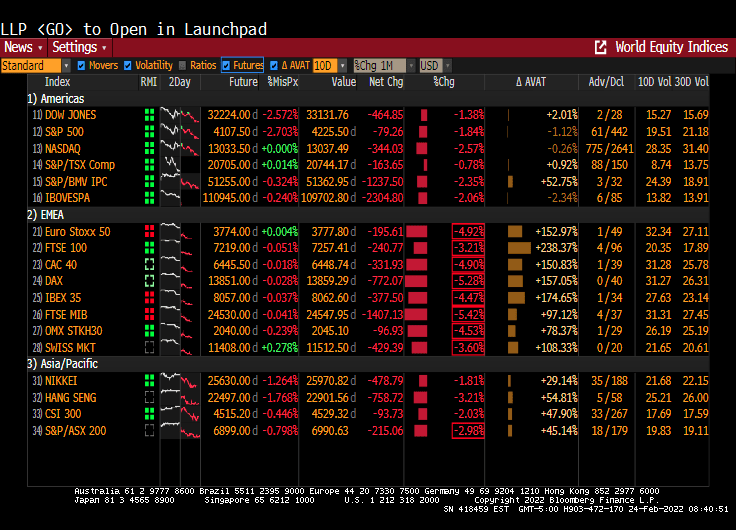

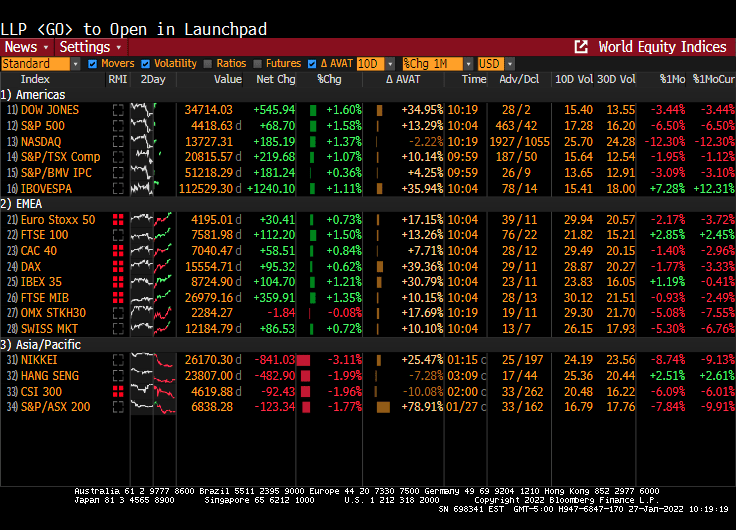

Europe is having a bad day equity market-wise. Eurostoxx 50 was down 4.92%. The US Dow is braced for a 2.5% opening.

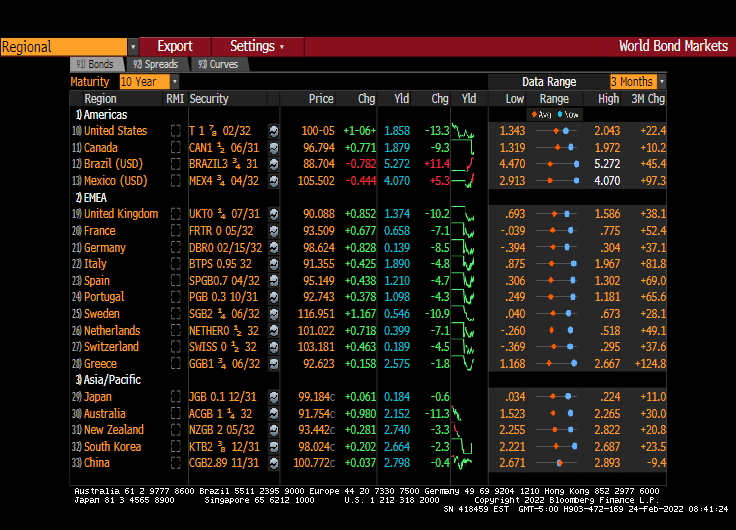

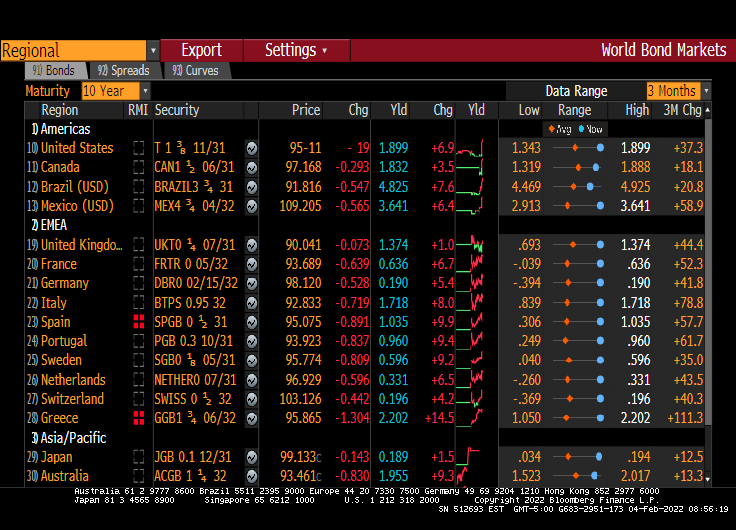

Now to bonds. The 10-year Treasury yield is down 13.3 bps this morning. Sweden and UK are down 10 bps as well.

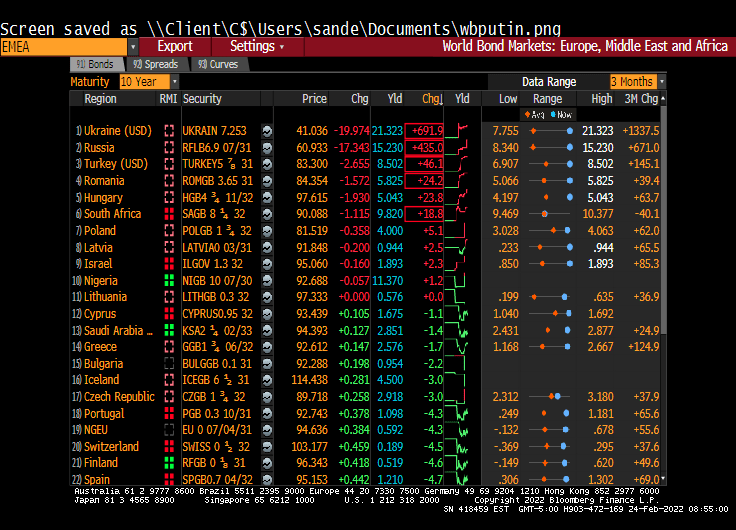

How about the new Russian front? Ukraine’s 10y yield rose 691.0 bps while Russia’s 10Y yield rose 435 bps.

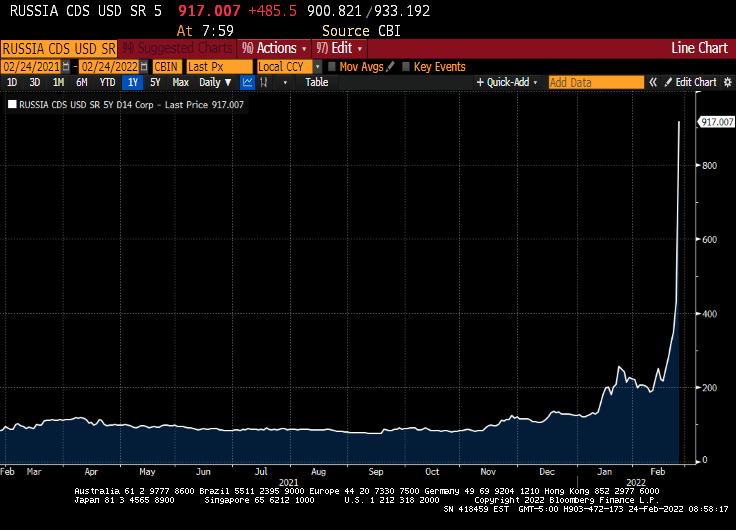

Russian 5Y Credit Default Swaps (CDS) leaped to a Greek-like 917.

Well, it looks like the sanctions imposed by Winken (US VP Harris), Blinken (US Secretary of State) and Nod (US President Biden because he always looks half-asleep) apparently didn’t work as intended.

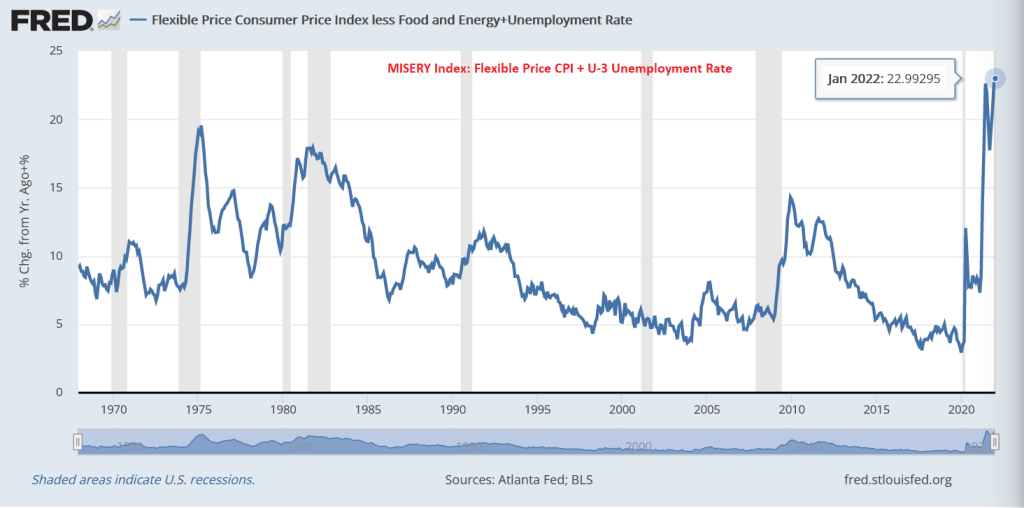

It is truly a miserable time for many Americans as demonstrated by the Misery Index (inflation rate + unemployment rate). But rather than using the CPI YoY measure at 7.5%, I am using the FLEXIBLE CPI YoY to compute the misery index. And is it ever miserable!

In January, the CORE flexible CPI YoY + U-3 unemployment rate hit a modern high at 22.99%. Or at least since 1967.

Like the movie “50 Shades of Gray,” we have 50 shades of inflation. Examples?

How about hardwood? Producer Price Index for hardwood is up 30.8% YoY.

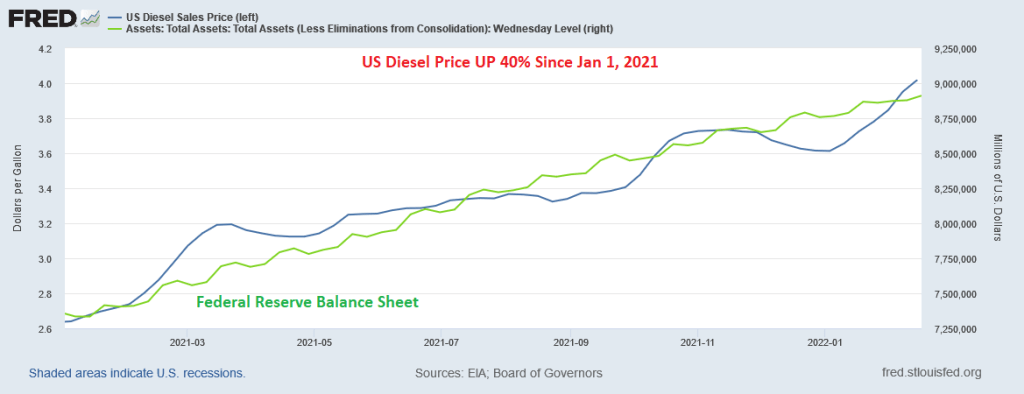

How about diesel fuel prices? They are UP 40% since January 1, 2021.

How about housing? UP 20% YoY according to Zillow’s home value index.

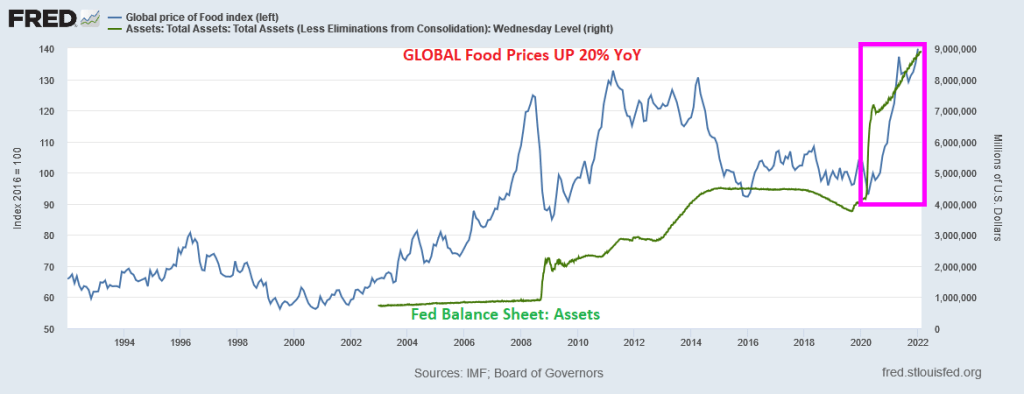

Global food prices? UP 20% YoY.

I could go on and on, but you get the picture. Rising energy, food and construction materials are soaring making many Americans miserable.

But Powell and The Fed have promised to whip inflation. Whip it good … with interest rate increases.

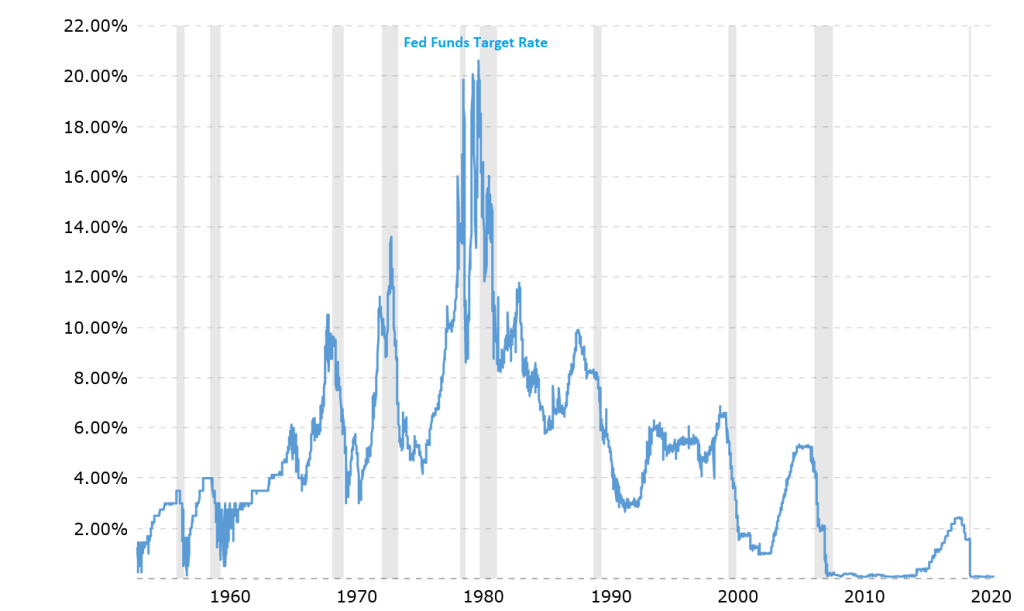

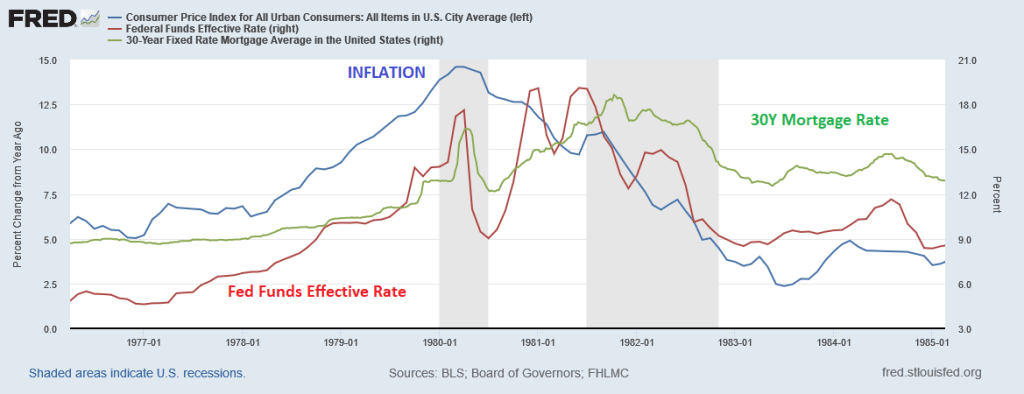

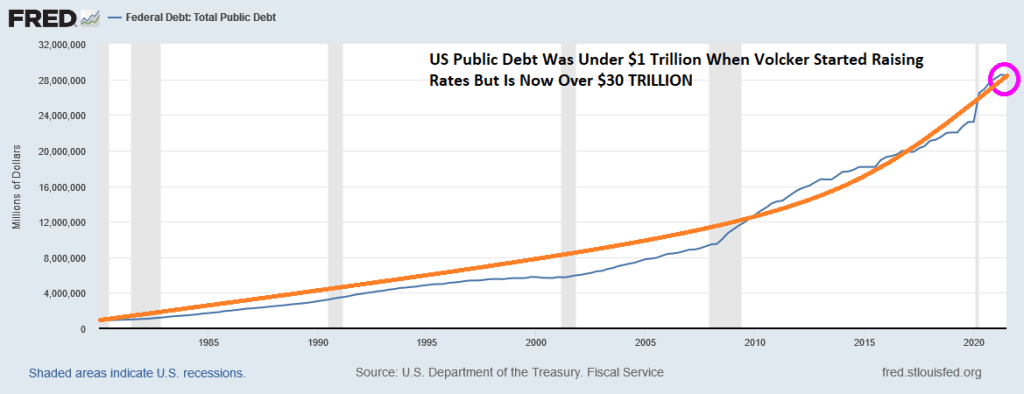

In August 1979, when Paul Volcker became chairman of the Federal Reserve Board, the annual average inflation rate in the United States was 11%. Inflation peaked in 1980 at 14.6%. Volcker raised the federal funds rate from 11.2% in 1979 to 20% in June of 1981.

Inflation (defined as CPI YoY) declined from over 14.6% in 1980 to 3.6% by 1985. But 30-year mortgage rates resumed their upward trajectory and peaking in October 1981 at 18.63 before beginning a gradual decline as inflation was tamed.

But will Powell enact another Volcker moment by raising the target rate abruptly?

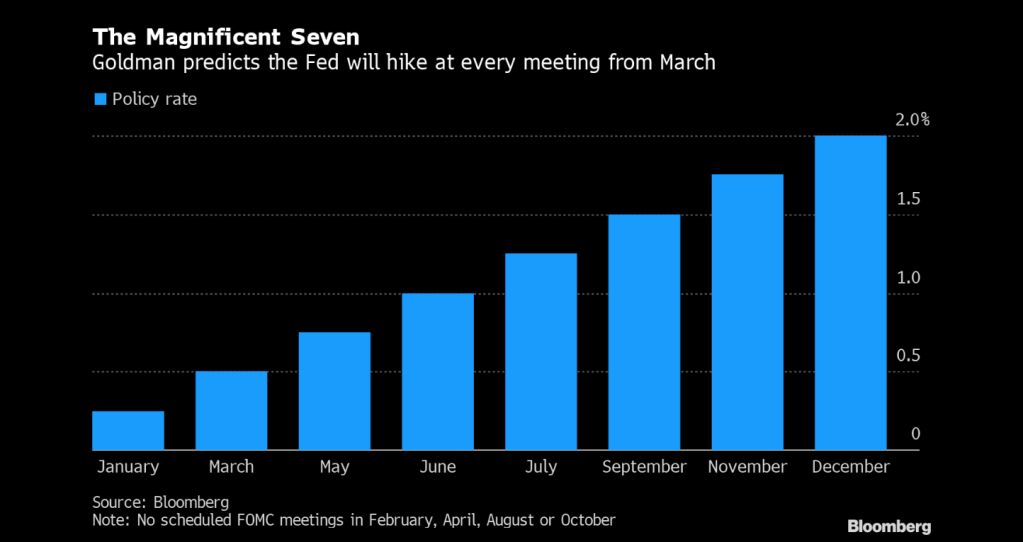

The bank is joining others on Wall Street in ramping up bets for faster policy tightening, after U.S. consumer prices posted the biggest jump since 1982 in January. Goldman Sachs Group Inc. is forecasting seven hikes this year, up from its earlier prediction of five.

“We now look for the Fed to hike 25bp at each of the next nine meetings, with the policy rate approaching a neutral stance by early next year,” the JPMorgan team, led by chief economist Bruce Kasman, said in a research note.

January U.S. inflation readings “surprised materially to the upside,” the economists wrote. “We now no longer see deceleration from last quarter’s near-record pace.”

On inflation, the economists said a “feedback loop” may be taking hold between strong growth, cost pressures, and private sector behavior that will continue even as the intensity of current price pressures in the energy sector eventually fade.

Strong growth? 1.3% is strong growth??

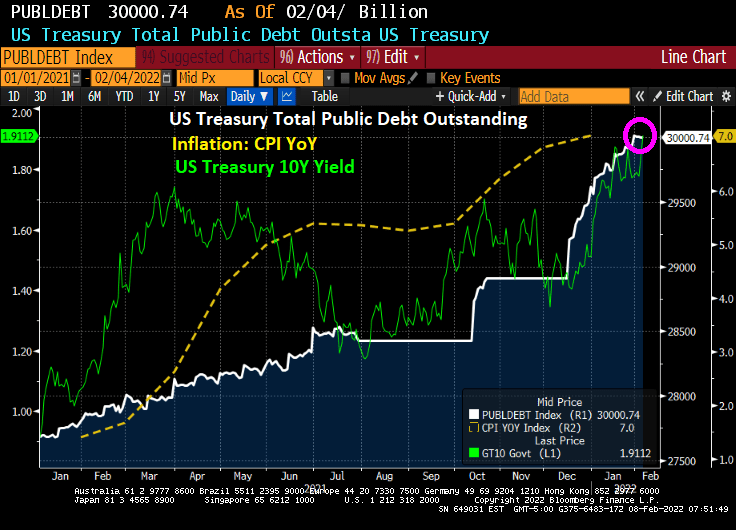

Be that as it may, the US economy is at a different place today than under President Jimmy Carter. When Volcker started raising The Fed Funds Target rate, US public debt was still under $1 trillion. It has ballooned to over $30 trillion today.

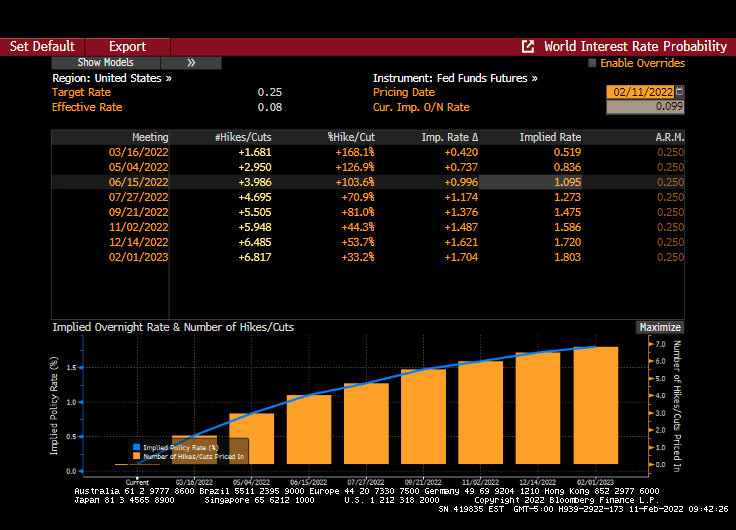

9 rate increases is above what is being priced in The Fed Funds FUTURES market which is 6 rate increases over the coming year.

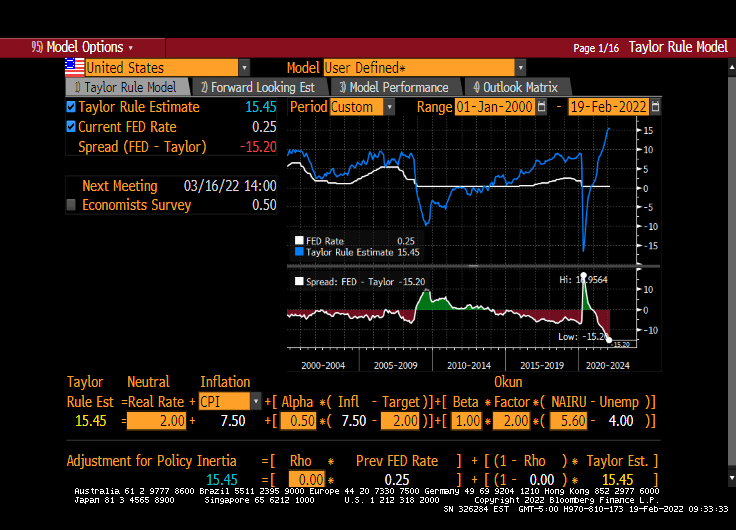

With 7.5% inflation, the Taylor Rule suggests a target rate of 15.45%. Talk about “Shock and Awful!”

We are starting to see GOLD (gold) surging and Bitcoin (yellow) falling as The Fed prepares “shock and awful” rate hikes and Biden continues to beat the war drums over Russia invading Ukraine.

If The Fed actually raises rates 9 times and dramatically pares back its massive monetary stimulus, it will be “shock and awful.”

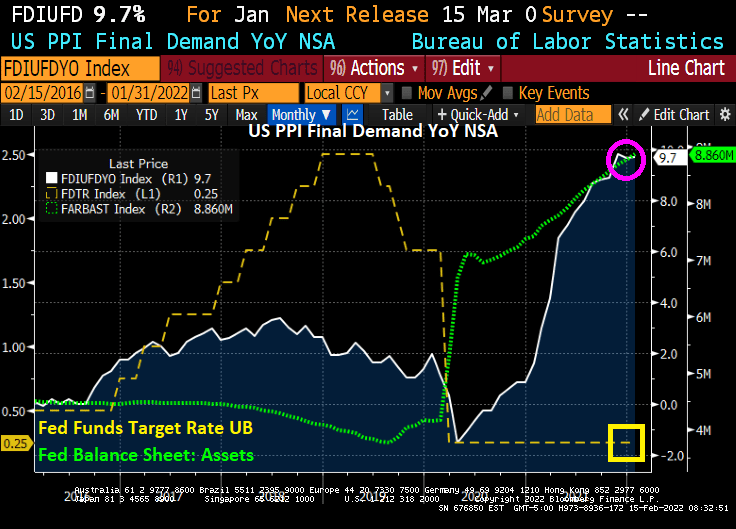

Today, the Final Demand Producer Price Index (PPI) printed at 9.7% YoY.

Biden claimed inflation was caused by COVID. How about 1) Biden’s anti-fossil fuel policies combined with 2) excessive fiscal (Biden and Congress) and excessive monetary stimulus (Fed)?

The Fed held its behind-closed-doors meeting on Monday, but nothing has been released about what they discussed. Suffice it to say, they have left the staggering monetary stimulus in play.

I wonder if The Fed is concerned about a soft landing with proposed rate increases.

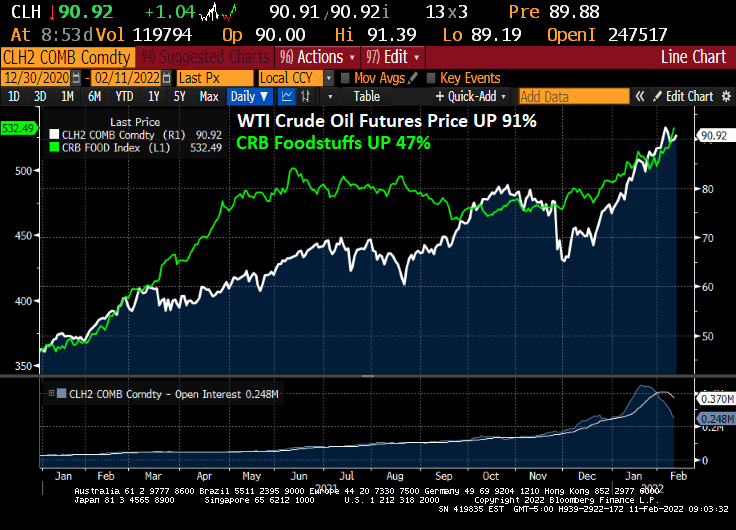

Well, it has been a cringe-worthy year+ under President Biden. West Texas Intermediate Crude futures price is up 91% and the Commodity Research Bureau Foodstuffs index is up 47%. Talk about Biden’s energy folicies being passed through to American households in the form of higher food costs and energy prices!

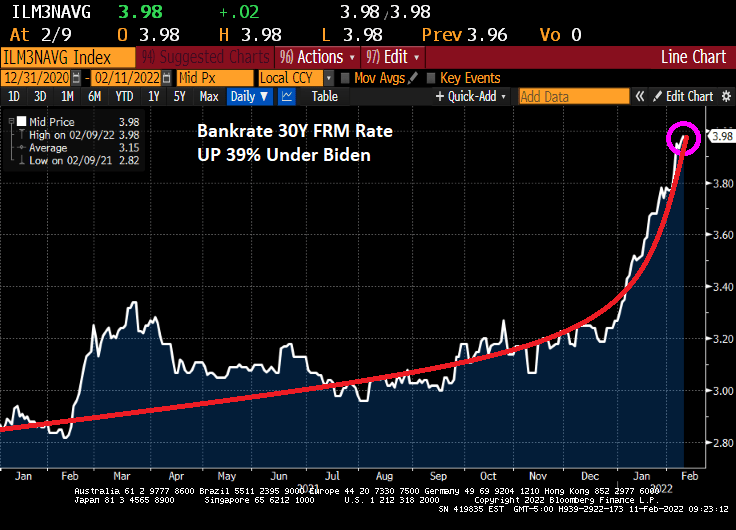

And then we have mortgage rates. Bankrate’s 30Y mortgage rate is up to almost 4%, up 39% since the beginning of 2021.

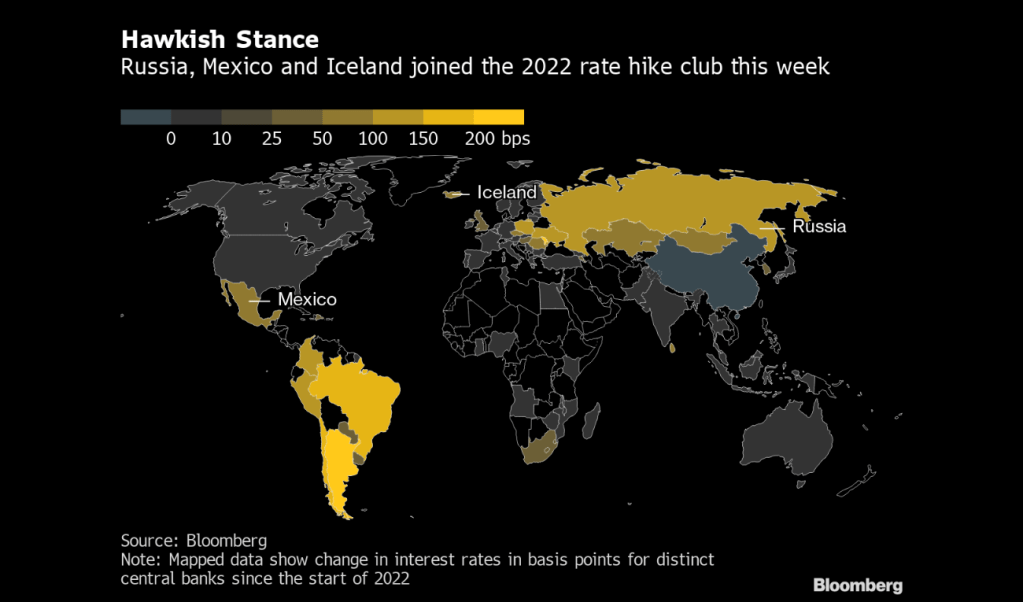

Other central banks are raising rates like banshees on the moor, while The Federal Reserve continues to send conflicting signals about possible March rate hikes.

Goldman Sachs sees 7 rate hikes in 2022, culminating in an eventual 2% rate in December.

Fed Funds Futures are signalling 7 rates increases by the February 1, 2023 meeting.

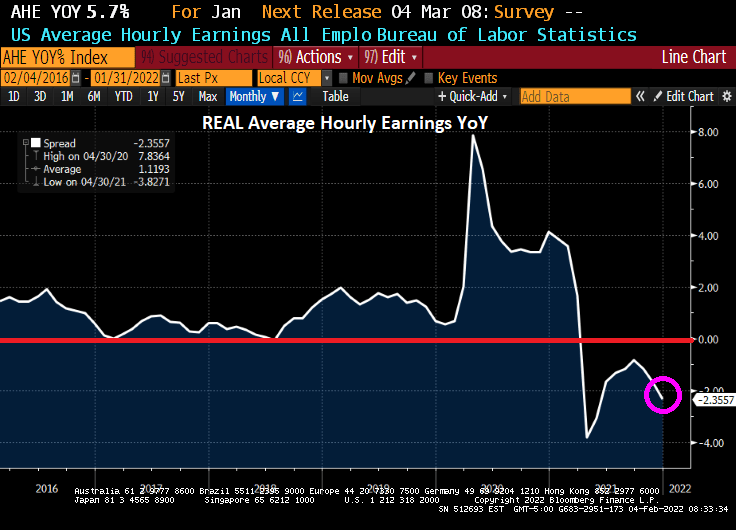

Well, the COVID hysteria from the Biden Administration and the media preparing us for a horrible jobs report was … incorrect. In fact, the January jobs report was “exceptional”. 467,000 jobs were added and average hourly earnings growth ROSE to 5.7% YoY.

The bad news? Thanks to surging inflation, REAL average hourly earnings growth YoY FELL to -2.36%.

Unemployment ROSE to 4.0% from 3.9% as more people dropped out of the labor force in January. On the bright side, labor force participation rate rose to 62.2% from 61.9%.

Leisure and hospitality employment (one of the most vulnerable to inflation) expanded by 151,000 in January, reflecting job gains in food services and drinking places (+108,000) and in the accommodation industry (+23,000).

The reaction in the bond market? US 10-year yields are up 6.9 basis points as Eurozone is up across the board.

Energy prices are up (except natural gas futures).

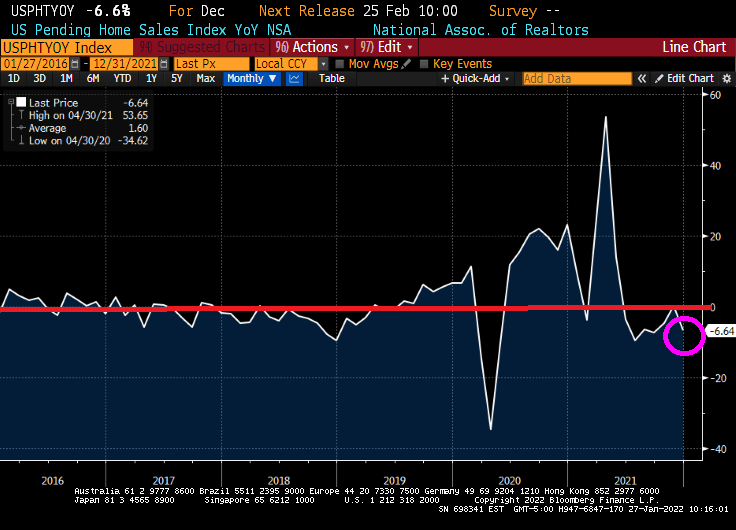

Pending home sales in the USA tanked 6.64% YoY. Yes, it was for December, but down 6.64% YoY means that pending home sales are lower than last December.

And the stock market was up across the board as Powell refused to take his foot off the monetary gas pedal.

Gold is down along with Bitcoin for you ALT investment types.

It has been a tough 7 days for Bitcoin, Ethereum and the NASDAQ composite index as The Fed is anticipated to raise their target rate AND engage in quantitative tightening.

While the NASDAQ composite index has been deflating over past 7 days, Bitcoin and Ethereum plunged in recent days. What is going on??

The Russell 2000 value (white) and growth (green) indices are both deflating.

With regards to anticipated Fed rate increases, Fed Funds Futures are signaling almost 4 rate hikes in 2022 and 4 by the February 2023 meeting.

Then we have the massive increase in The Fed’s balance sheet after COVID struck in early 2020. Now, with the S&P 500 skyrocketing (until 7 days ago), why is The Fed buying sooooo much Agency MBS??

You must be logged in to post a comment.