Global uncertainty hits an ALL-TIME HIGH.

Higher than Covid, the 2008 financial crisis, and the dot-com crash COMBINED.

You know what that means!

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

Global uncertainty hits an ALL-TIME HIGH.

Higher than Covid, the 2008 financial crisis, and the dot-com crash COMBINED.

You know what that means!

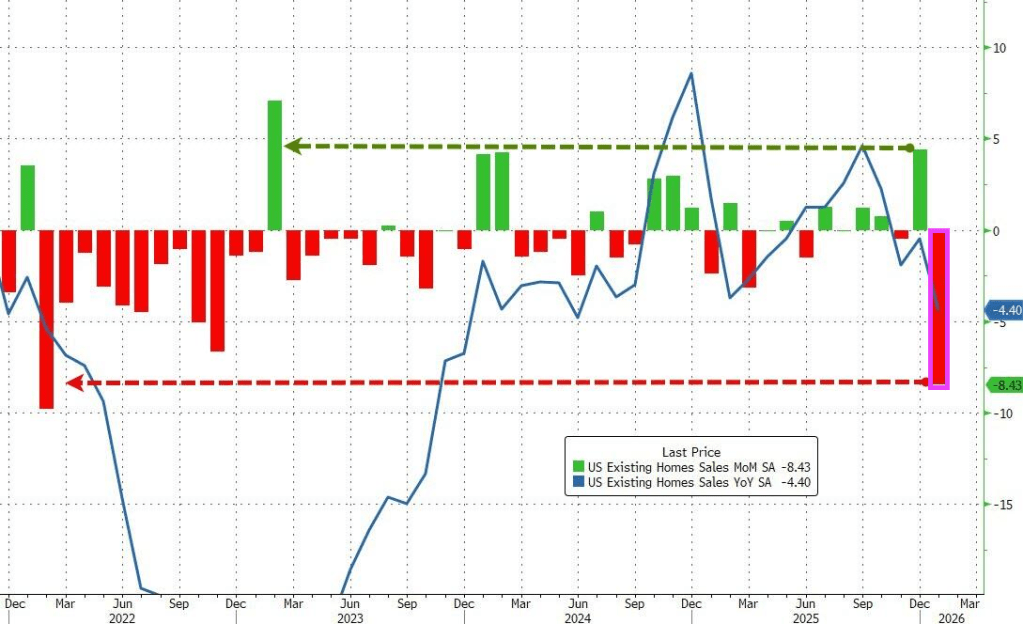

After managing a 1.4% YoY rise in 2025 (dramatically down from the 9.7% YoY rise in 2024, and 33% YoY collapse in 2023), US existing home sales were expected to drop 4.6% MoM in January (following December’s outsized 5.1% MoM surge), despite a tumble in mortgage rates.

The analysts were correct on the direction but wrong on the scale as existing home sales plunged 8.4% MoM in January from a downwardly revised +4.4% MoM in December. That is the biggest MoM drop since February 2022.

While some suggested this could be impacted by the Winter Storms, this is based on contracts signed in November/December… and the biggest decline was in The West (which had zero weather impact)

Nevertheless, realtors gonna realtor:

“The below-normal temperatures and above-normal precipitation this January make it harder than usual to assess the underlying driver of the decrease and determine if this month’s numbers are an aberration,” NAR Chief Economist Lawrence Yun said in a statement.

That MoM plunge pulled the total SAAR down near 15 year lows…

Without an extended period of improved affordability, the recovery in the housing market is likely to be prolonged.

The NAR report showed the median selling price rose 0.9% from a year earlier to $396,800 last month.

First-time buyers represented 31% of buyers of existing homes in January, up slightly from 29% in the prior month and higher than a year ago.

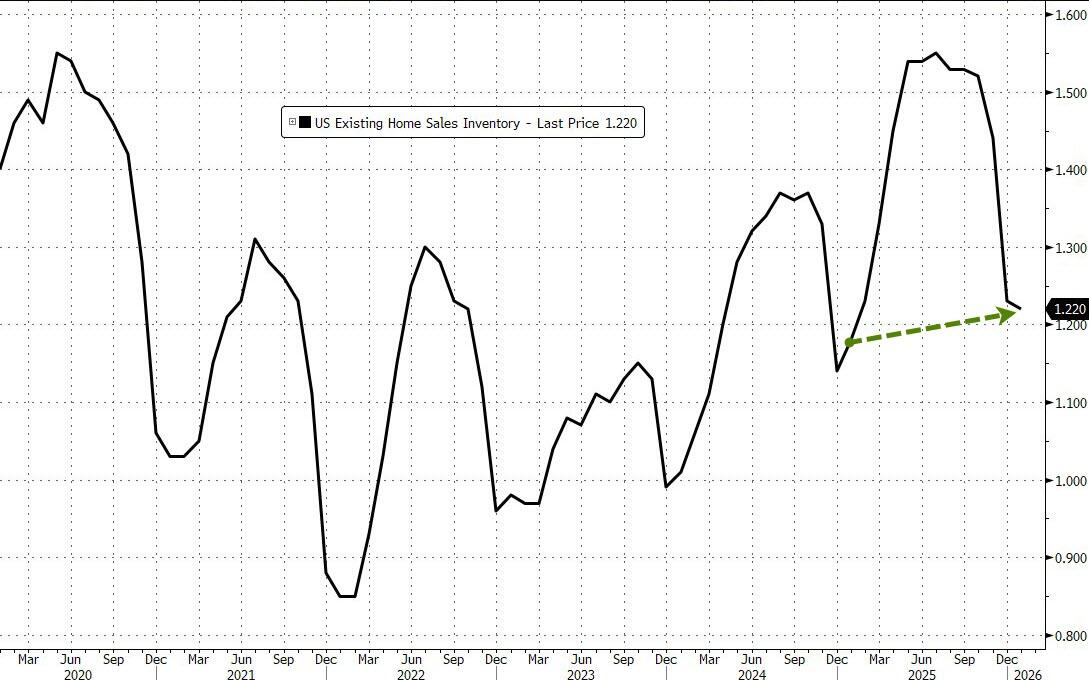

The inventory of previously owned homes increased 3.4% in January from a year ago to 1.22 million.

A pickup in supply through 2025 has helped to tame price growth, though Yun said on a call with reporters that listings need to increase much more to help improve sales.

On the bright side, it appears mortgage applications are rebounding as the year started with lower rates…

Arguably, existing home sales have much further to go to the upside as the lagged mortgage rate has continued to decline… so what triggered this collapse?

Finally, circling back to where we started, NAR expects home sales to rise a stunning 14% this year, higher than most other forecasts but a figure that NAR Chief Economist Lawrence Yun said he feels “confident” in. That assumes more inventory will come on the market, mortgage rates will hover around 6% and the Fed will cut interest rates another two times, compared to policymakers’ median projection for one.

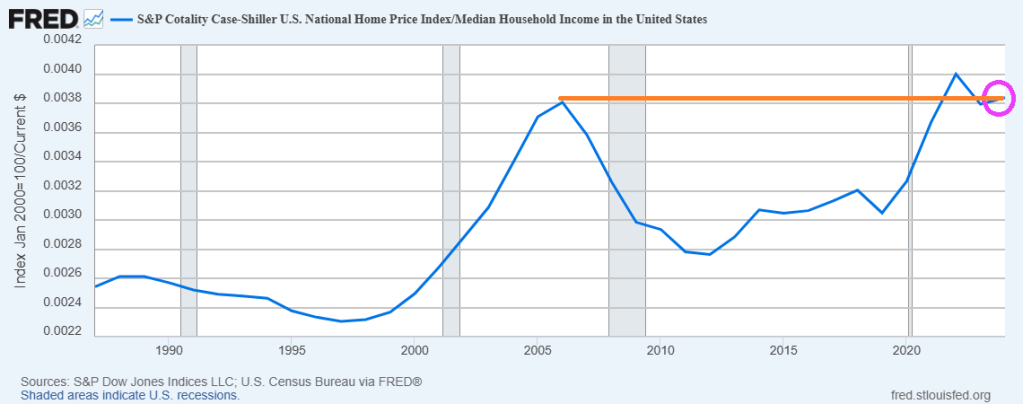

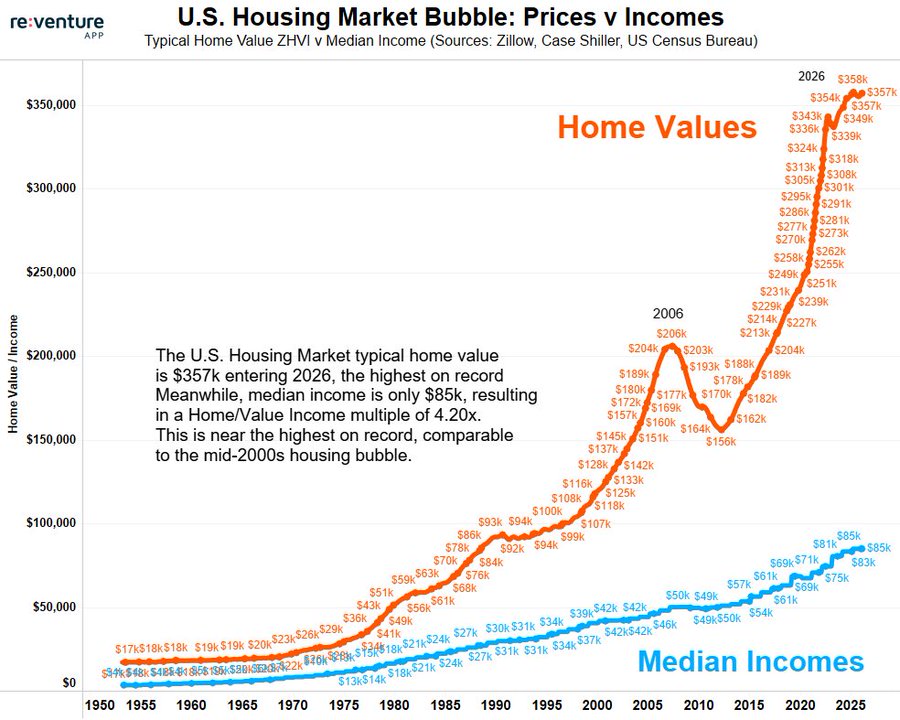

Yikes! The ratio of US Home Prices to US Median Household Income is now higher than the ratio during the catestrophic housing bubble during the latter half of the 2000s.

Here is a chart of home prices and median household incone,

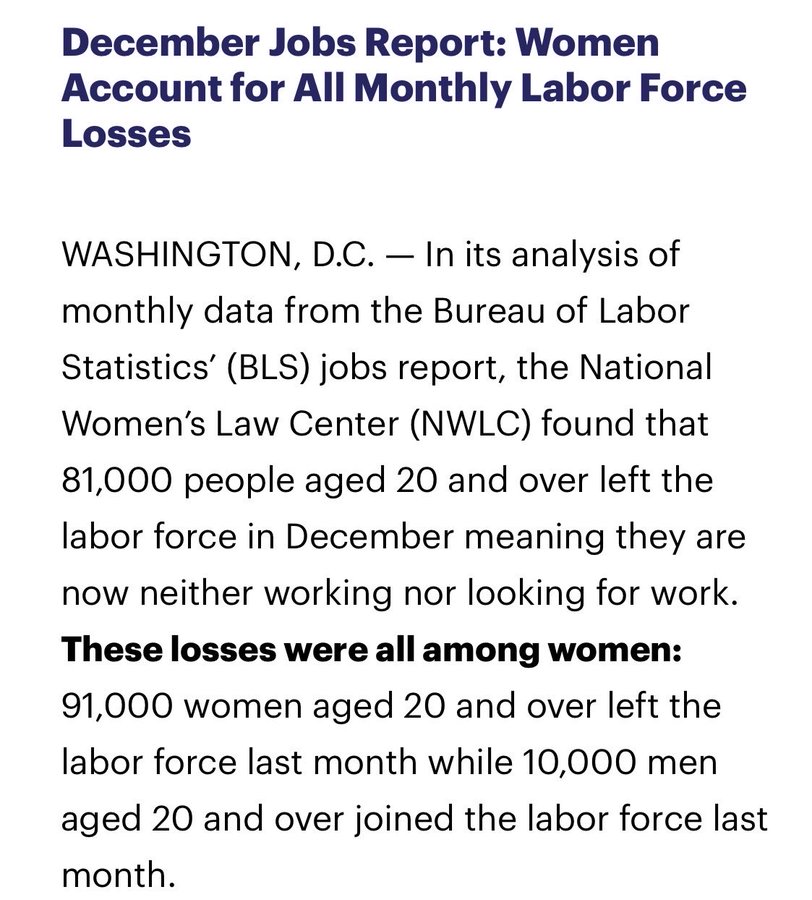

The labor market is truly screwed-up. The December jobs report reveals that women account for nearly all labor force losses.

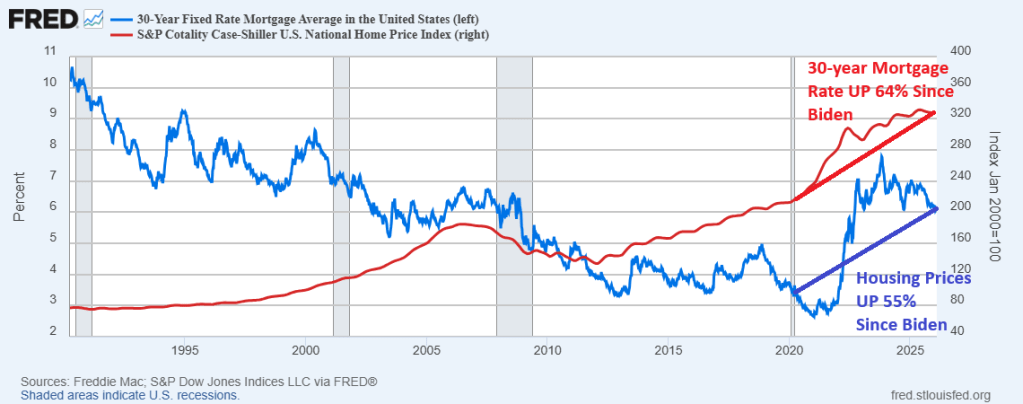

I ain’t drunk! But it would help in this housing market where housing prices and mortgage rates are much higher than when Joe Biden became President in January 2020. In fact, the Case-Shiller national home price index is 55% higher than when Sleepy Joe took the reins of Presidency and the 30-year mortgage rate is 64% higher.

Because of higher housing prices and mortgage rates,

The Case-Shiller national home price index is 55% higher than when Sleepy Joe took the reins of Presidency and the 30-year mortgage rate is 64% higher.

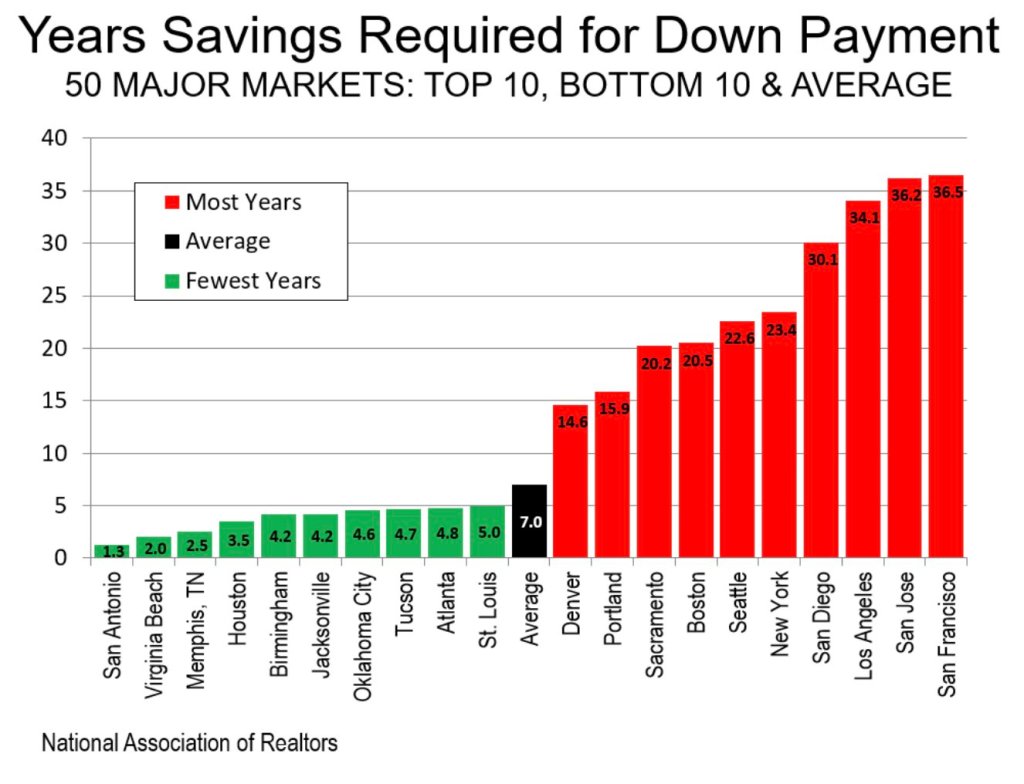

As a result of higher housing prices and mortgage rate (and Gavin Newsom’s ludicrous policies), it will take over 30 years to accumulate enough savings to buy a home in San Diego, Los Angeles, San Jose and San Francisco.

I ain’t drunk, but first-time homebuyers will need to be drunk in this housing market.

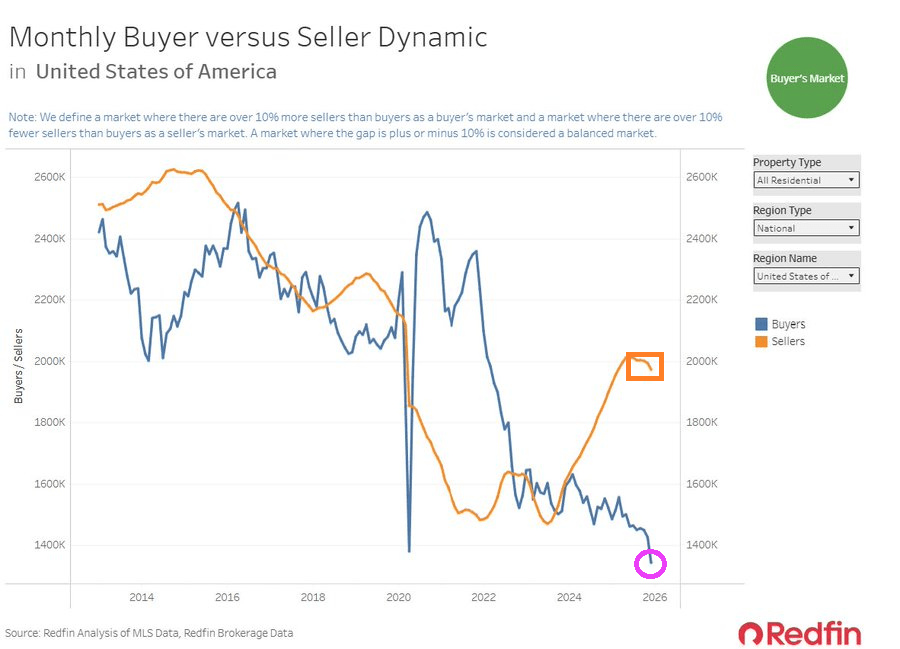

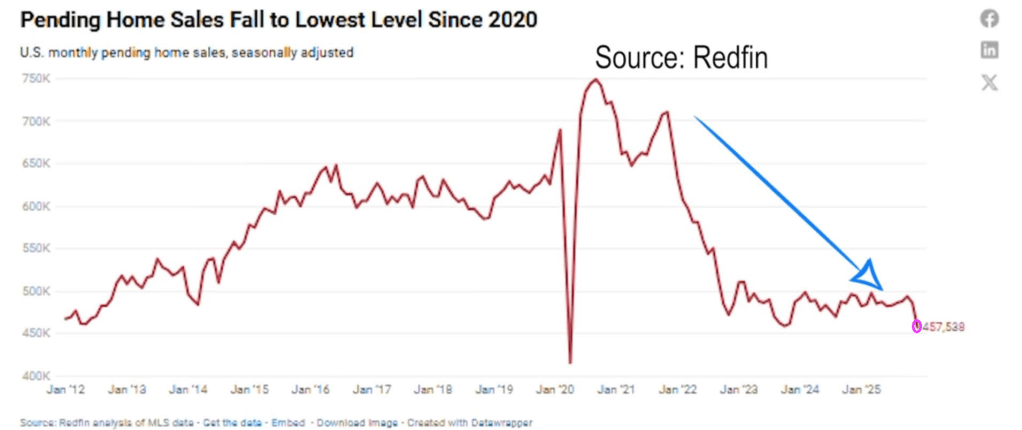

According to Redfin, US pending home sales fell to the lowest since the Covid epidemic of 2020.

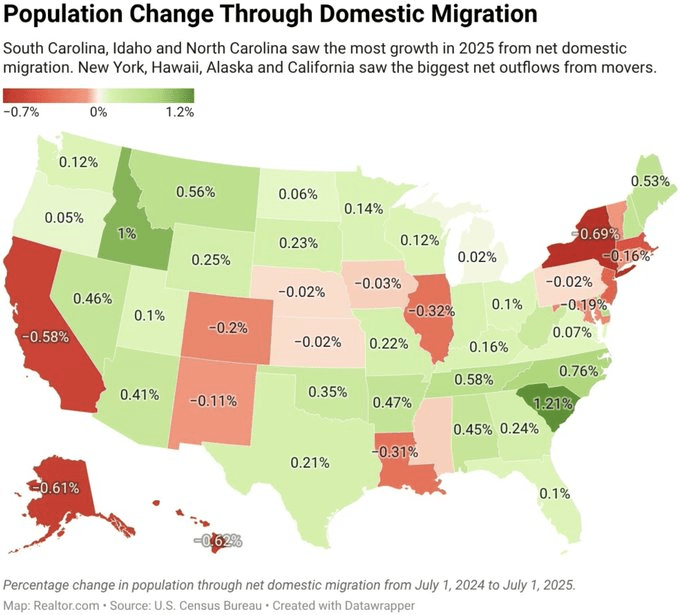

With the population change from state to state, like New York, California and Illinous to South Carolina and Idaho (home of Napolean Dynamite), it is no wonder that the housing market is in a state of turmoil.

Why leave New York? A scene from Mandami’s NYC.

Wipeout! $6 TRILLION ERASED IN 60 MINUTES

Gold wiped out nearly $3 trillion

Silver erased nearly $790 billion

S&P 500 lost nearly $780 billion

Nasdaq wiped out $750 billion

Crypto market erased $100 billion

Insane crash at US market open.

Gold suffered too.

Along with Bitcoin.

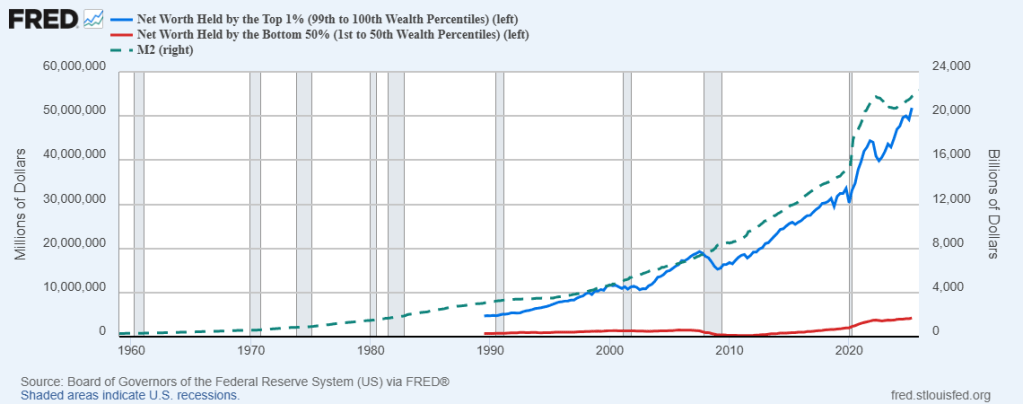

A good Federal Reserve don’t. Print money, that is.

The Federal Reserve prints a lot of money (M2). Unfortunately, it largely benefits elites (the top 1%). The bottom 50% get some benefits, but the gains in net worth largely benefits the elite class.

This sounds like a legal Somali daycare scheme. Perhaps The Fed should be renamed “The Federal Quality Learing Center.”

Yes, Somalis have daycare centers in Columbus Ohio. Thanks Governor Dewine for doing absolutely nothing to reign in their fraud. /sarc

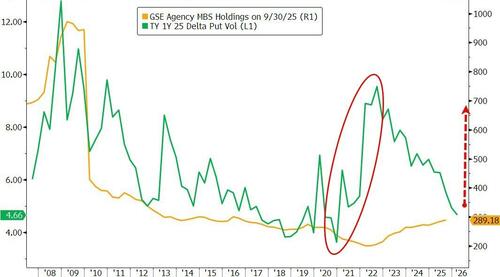

President Trump ordered Fannie Mae and Freddie Mac to operate like The Federal Reserve. Buying assets to manipulate interest rates. In this case, F&F have been ordered to buy $200 billion of agency MBS.

Thursday’s Truth Social post triggered an immediate snap tighter in mortgages, led by the belly and lower coupons. By pulling MBS spreads tighter and crowding out real-money buyers, Fannie and Freddie’s purchases would push incremental demand into Treasuries as the next-best duration substitute, putting a modest bid under the belly of the curve.

However, execution and the ultimate size of purchases is still unclear, as my colleague Alyce Andres noted. If the government-sponsored enterprises GSEs stagger purchases, and signal an ultimate increase above the announces $200 billion, further tightening should occur. They can fund a lot of the buys from existing liquidity portfolios, though there’s a path where they could issue short-term debt to preserve operating buffers and could nudge repo wider at the margin.

The bigger transmission channel is hedging, as highlighted by colleagues Ira Jersey and Will Hoffman. Unlike the Fed, the GSEs actively hedge MBS holdings, shedding duration by paying fixed rates in swaps and using swaptions to manage the negative convexity and vega risks embedded in mortgages. That matters for swap spreads and for volatility, especially in the belly.

That’s why GSE MBS purchases don’t have to be huge to change the feel in rate markets. The post-Global Financial Crisis regime dulled the classic convexity feedback loop because the Fed held such a large amount of agency MBS and didn’t hedge it, while the GSEs shrank their portfolios. Trump’s directive risks bringing more of that regime back.

A recent note out of Goldman Sachs frames it cleanly: A $200 billion build could lift the active convexity-hedger footprint by about 25%. The street then starts front-running the mechanical flows — paying in selloffs, receiving in rallies — which makes breakouts more likely even if day-to-day ranges look calm, Goldman added.

Positioning makes the setup more precarious. JPMorgan already saw mortgage valuations as a “bit snug” before the announcement, while BofA flagged that rates market had recently added fresh belly shorts sitting against a backdrop of benchmark funds still overweight MBS versus IG.

That mix can keep the initial tightening sticky, but it also raises the odds of sharp reversals if the market decides the purchasing flows are slower, smaller, or more heavily hedged than hoped.

Fannie and Freddie’s retained portfolio are soaring along with the duration gap.

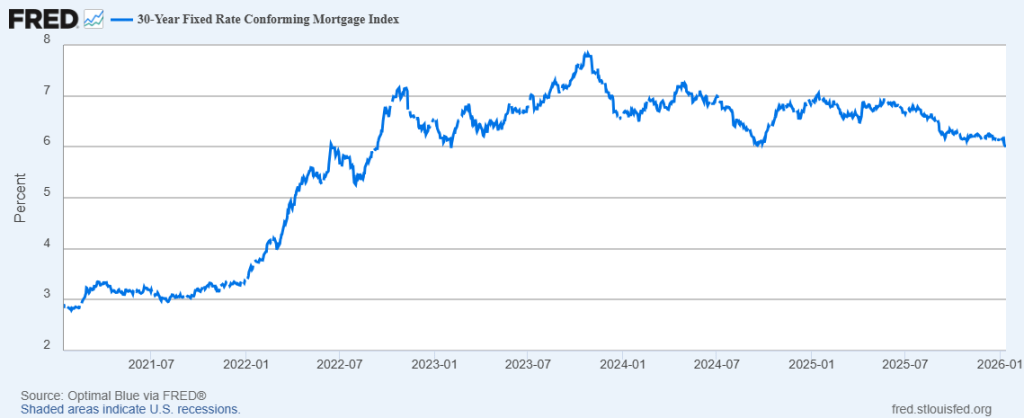

The effect on mortgage rates has so far has been negligible. The 30-year conforming mortgage just fell below 6% at 5.99%.

It looks like President Trump wants ANOTHER Federal Reserve. He has ordered the GSEs (Fannie Mae and Freddie Mac) to purchase $200 BILLION in mortgage bonds in an attempt to lower mortgage rates. Puzzling since real GDP growth is soaring.

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2025 is 5.4 percent on January 8, up from 2.7 percent on January 5. After recent releases from the US Bureau of Economic Analysis, the US Census Bureau, and the Institute for Supply Management, the nowcast of fourth-quarter real personal consumption expenditures growth increased from 2.4 percent to 3.0 percent, while the nowcast of the contribution of net exports to fourth-quarter real GDP growth increased from -0.30 percentage points to 1.97 percentage points.

The 5.4% real GDP forecast is largely due to exports rising at 6.1% and imports falling -9.4%.

Looks like Trump’s tariffs are working.

Politicians love to scream about housing being simply unaffordable. Like mayor-elected Mandami in New York City. But the reality is that housing prices vary by city and there are more affordable cities than New York City to choose from. Federal policies should not be focused on letting people staying a particular city.

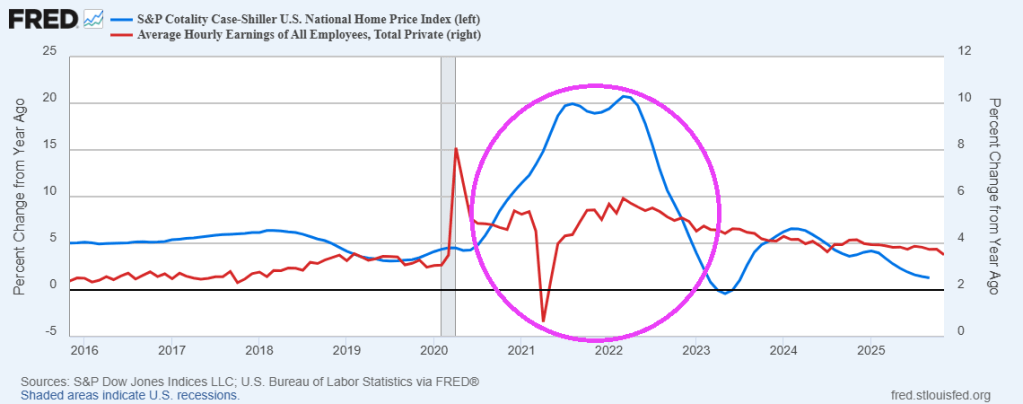

When we look at housing prices compared to average hourly earnings, we see housing prices rising with average hourly earnings … as expected.

If we look at year-over-year changes, we see the Covid bump in housing prices corresponding with the surge in Federal spending. But things have simmered down since the bump in 2020-2023.

My suggestion is for the Federal government to stop interfering in the housing market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.