Joe Biden has a new name: the crypt keeper. As in the person through his economic screw-ups is causing a massive inflow to cryptos.

Anticipation of an eventual US spot Bitcoin ETF – which Bloomberg’s analysts assign a 90% probability of being approved by the SEC in January.

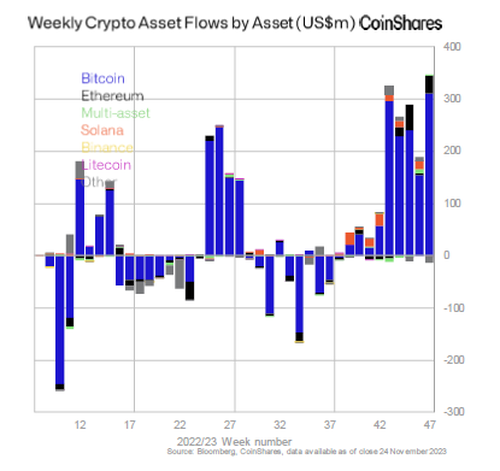

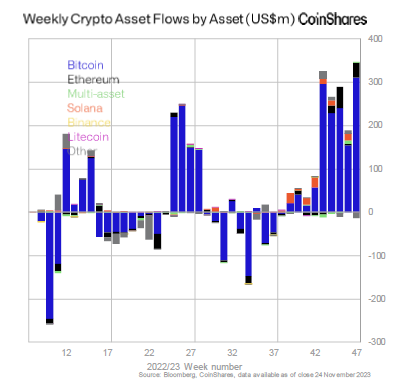

as well as surging prices, have helped to spur inflows into digital-asset investment products for a ninth consecutive week, the largest run since the crypto bull market in late 2021.

According to a recent report from CoinShares, these products which include trusts and exchange-traded products, saw inflows of $346 million last week, with Canada and Germany contributing to 87% of the total. Only $30 million came from the US, a sign of continued low participation from the country, the asset-management firm said. Of course, that will change as soon as investors start seeing double digit percentage weekly gains, and reallocating their money into crypto in droves, just like they did in 2020 and 2021.

Since early October, the crypto market has surged as traditional asset managers like BlackRock prepared for spot Bitcoin ETFs, potentially bringing in many more investors into the asset and resulting in inflows of tens of billions in fresh capital.

“The combination of price rises and inflows have now pushed up total assets under management to $45.3 billion, the highest in over one and half years,” the report said.

Bitcoin products raked in $312 million last week, pushing inflows to over $1.5 billion since the start of the year. Ether products saw $34 million in inflows last week, almost negating outflows all of 2023.

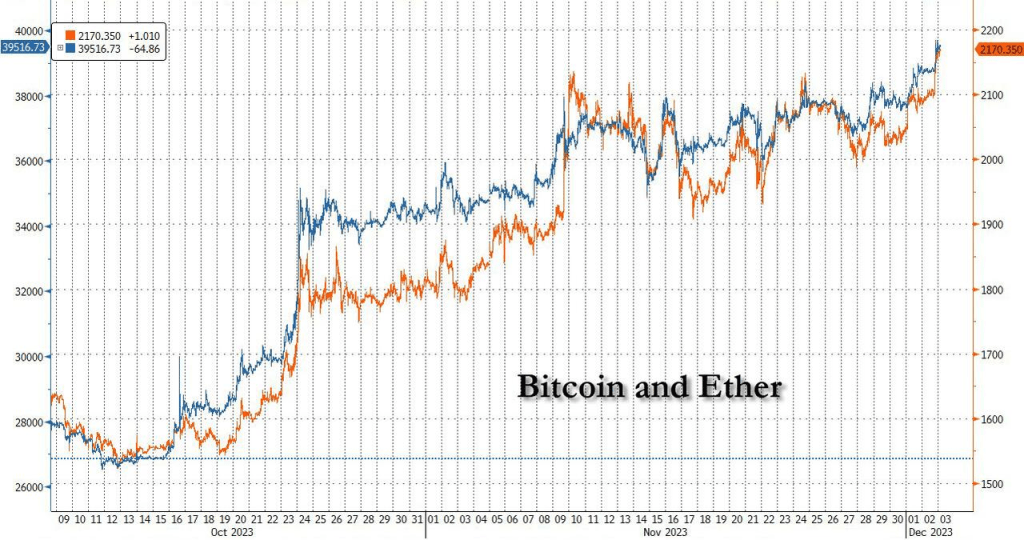

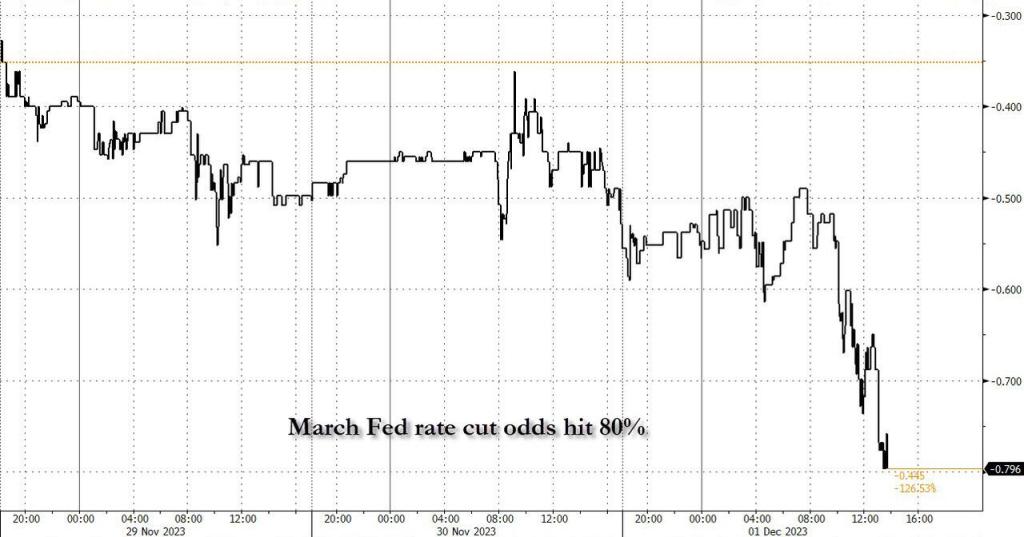

Amid the surging inflows, and amid expectations for imminent ETF approval by the SEC and a surge in March rate cuts odds, bitcoin and ethereum have continued their furious ascent, with the former now trading just shy of $40.

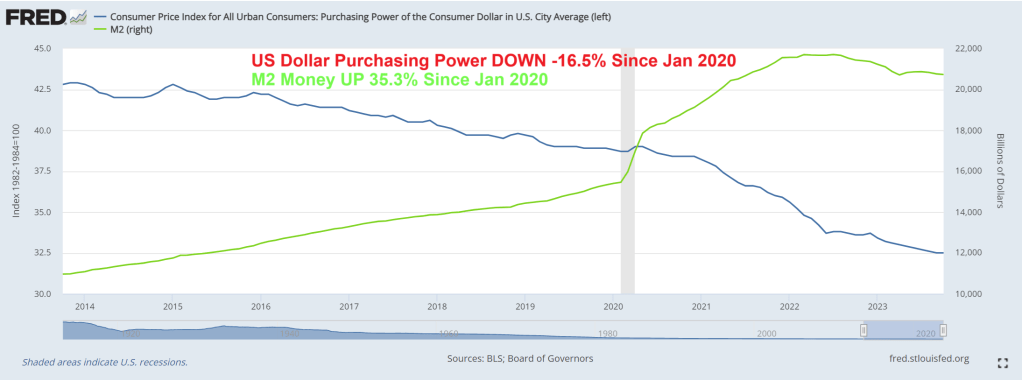

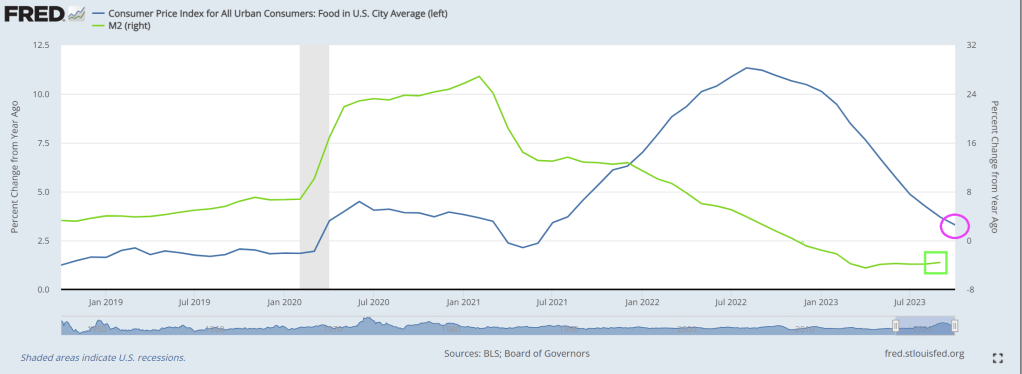

Since Covid and the idiotic government and school shutdowns of 2020, the purchasing power of the US Dollar has fallen -16.5% as M2 Money grew 35.3%. Keep on printing?

I suppose Biden’s biography can be called “Tales From The Crypt(o)”.

While members of the Biden Administration party at DC nightclubs, the rest of America are drinking Carlo Rossi wine (a favorite of mine in high school!) and eating Spam.

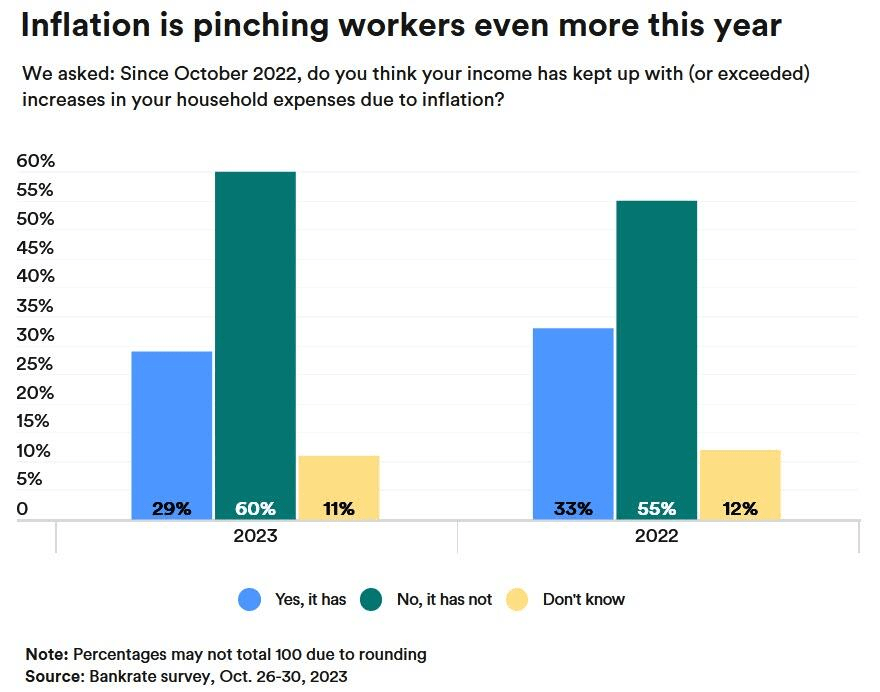

While hourly pay has increased, inflation has outpaced it.

Spending on basic survival needs like food, transportation, housing, and energy has increased, with households in the Mountain West facing the highest rates of inflation.

“We choose January 2021 as the base month because it was the last time inflation was within recent historical norms,” the report reads.

“Due to a combination of higher inflation rates and higher average household spending, inflation is imposing the highest monthly costs on families in the states of Colorado, Utah, and Arizona,” the report adds.

Families in Colorado and Washington, DC, are experiencing inflation costs higher than the national average.

Things are even worse in 2023 regarding inflation ravaging worker’s income. Over 60% of Americans reported that their wages were lagging well behind inflation.

Since January 2021, US purchasing power of the US Dollar is down a whopping -15.4% under Biden.

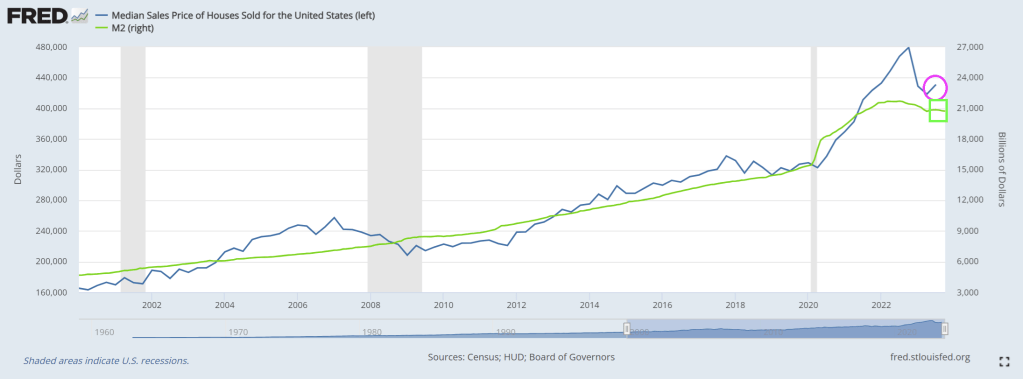

And home prices are up 33.2% under Biden, much of it due to The Feral Reserve money printing to fund Biden’s folicy initiatives. (I saw Biden claim he wrote the Inflation Reduction Act … the one thing we know is House legislation is written by an army of Congressional staffers, not El Presidente).

Home prices up 33.2% and purchasing power of US Dollar down -15.4% under Biden.

And like magic, Biden made $11,400 disappear from household income to pay for Bidenomics.

Median home prices are up a whopping 20% under Biden and his signature Bidenomics, growing the economy from the inside-out (?) instead of top-down. Excuse me Joe, Bidenomics is pure top-down Soviet-style economic planning. Markets be damned! The end result? Housing is far more expensive under Biden as are down payments.

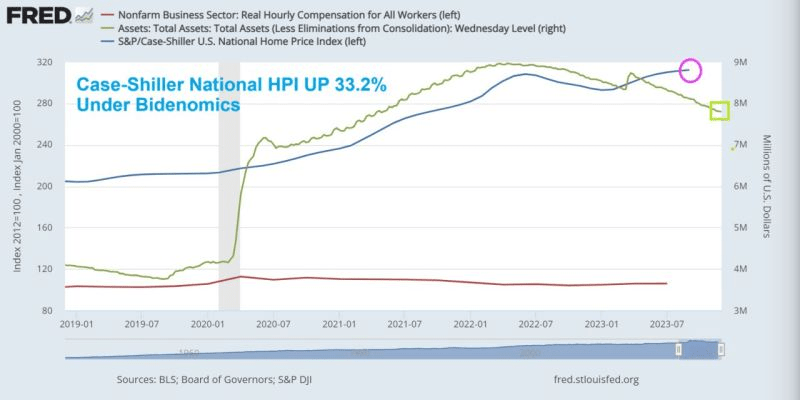

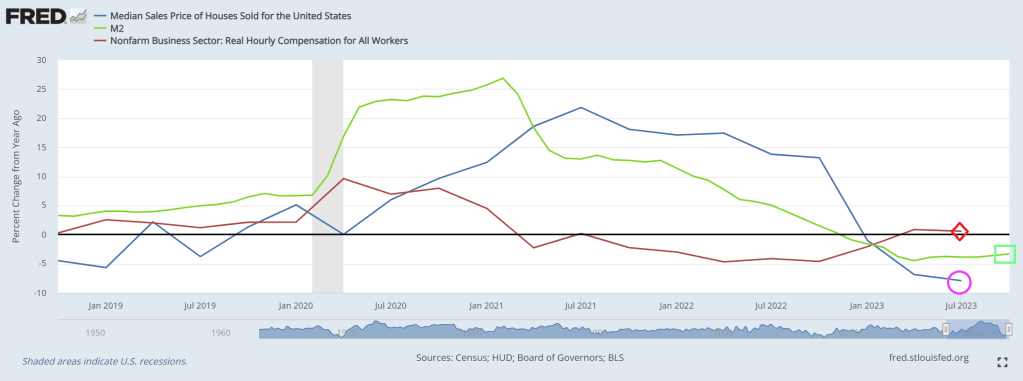

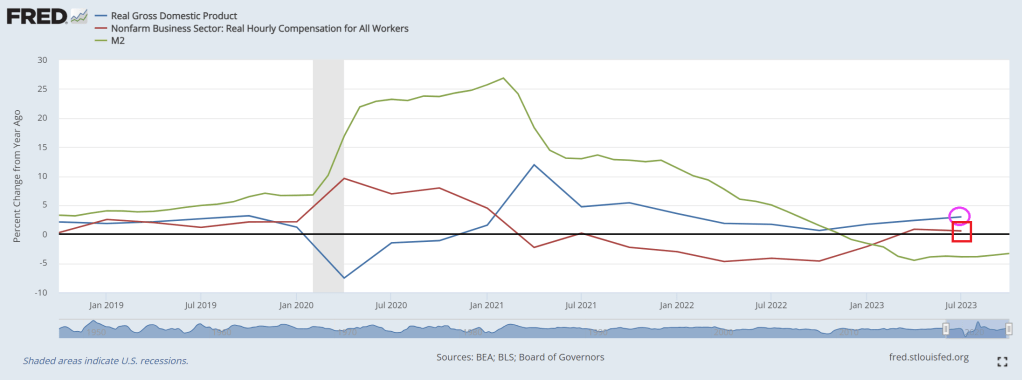

If we look at year-over-year (YoY), we can see the burst of Covid-related spending and M2 Money growth (green line) that surged in 2020/2021. And rising home prices followed shortly thereafter. But as M2 Money growth slows, median home price growth declined into negative growth. The only factor that is positive is real hourly compensation (red line). But that is barely above 0%.

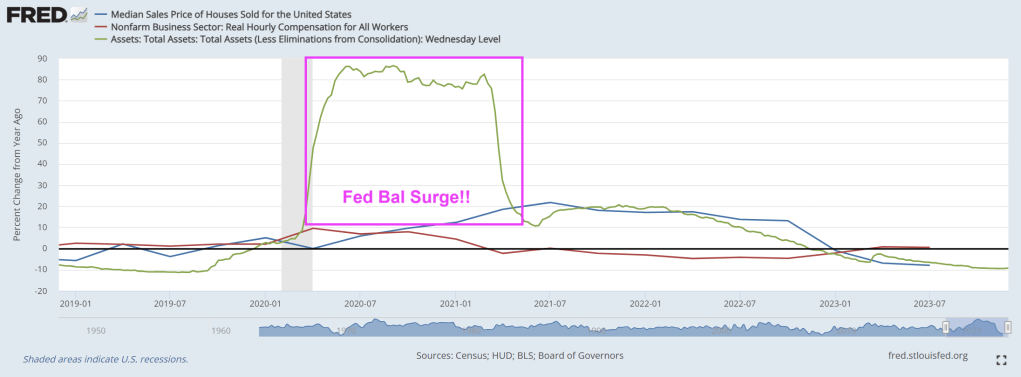

If we look at The Fed’s balance sheet surge (much like a storm surge), you can see the 2020/2021 overreaction to Covid and the various government shutdowns (along with school shutdowns).

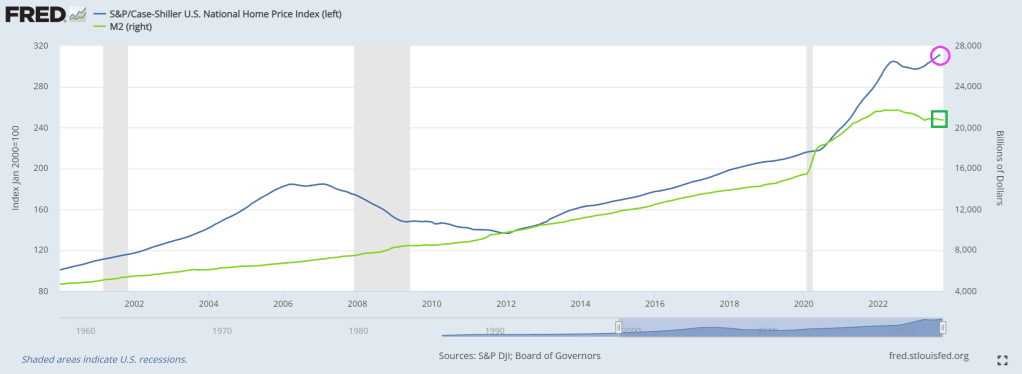

The problem is that The Fed is shrinking their balance sheet like Biden shuffles. Maybe The Fed is following Biden’s lead: slow walking, incoherent messaging. And with the Fed storm surge of 2020/2021, Case-Shiller national home price index is up 33.2% under Bidenomics. Good luck with that down payment if you are renting and want to become a homeowner.

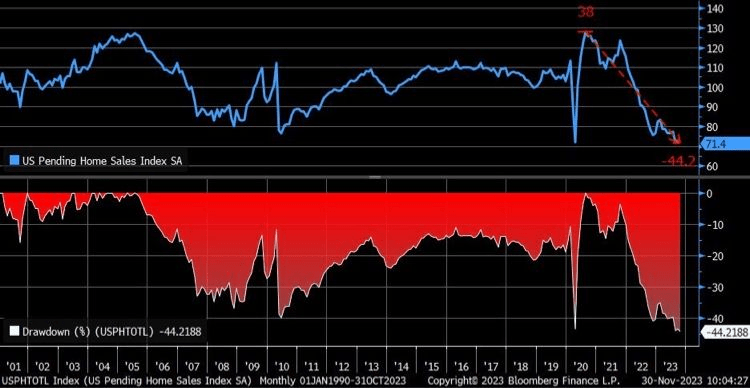

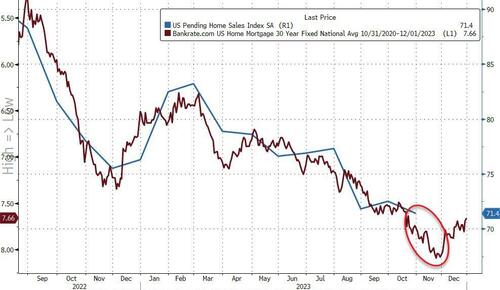

Pending home sales crash is showing why government usually fails to deliver sensible outcomes.

After all, Biden (and his overlord Obama) are truly addicted to gov solutions. Which means they are doomed to fail, as most government policies do.

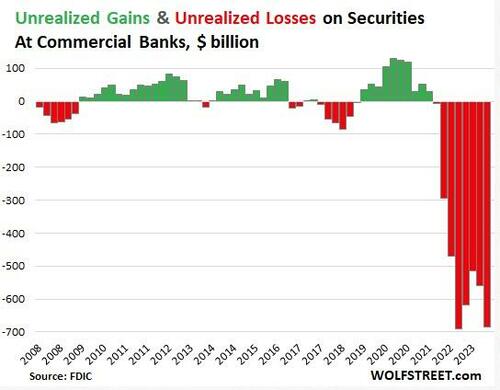

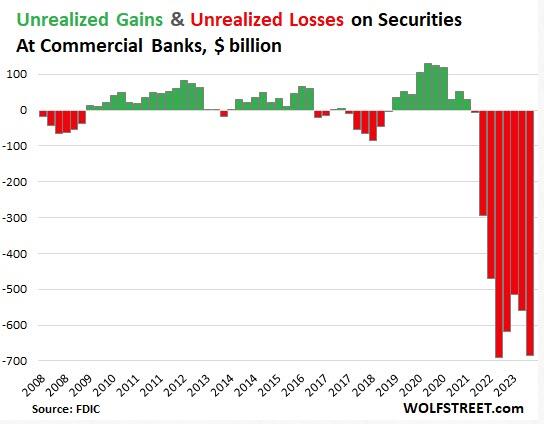

Unrealized losses on securities held by US banks exploded by 22% in the third quarter.

Of course, unrealized losses don’t really matter — until they do.

This is yet more evidence that the financial crisis that kicked off last March continues to bubble under the surface.

Unrealized losses, primarily on US Treasuries and mortgage-backed securities rose by $126 billion in Q3 and now total $684 billion, according to the FDIC’s quarterly bank data release.

Current unrealized losses are only slightly below the record set in the third quarter of 2022. This reflects the fact that the FDIC took over three failed banks earlier his year and ate their unrealized losses when it sold the banks’ assets, thus wiping them from the books.

Unrealized looses on securities are divided between two accounting methods.

Unrealized losses on held-to-maturity (HTM) securities jumped by $81 billion to $391 billion.

Unrealized losses on available-for-sale (AFS) securities jumped by $45 billion to $293 billion.

It’s important to understand these are only paper losses. Ostensibly, the banks will hold these bonds until maturity and then will be paid their face value. If it plays out this way, there won’t be any real losses.

The problem is that these unrealized losses drastically decrease a bank’s liquidity. If it has to sell bonds in order to raise capital, the bank will experience significant losses. This is exactly what took down Silicon Valley Bank last March.

Here’s what happened.

SVB sold a large portion of its bond portfolio at a $1.8 billion loss. At the time, SVB CEO Greg Becke said the bank made the sale “because we expect continued higher interest rates, pressured public and private markets, and elevated cash burn levels from our clients.”

The bank bought the bonds when interest rates were low. As a result, the $21 billion available for sale (AVS) bond portfolio was not yielding above cash burn. Meanwhile, rising interest rates caused the value of the portfolio to fall significantly. The plan was to sell the longer-term, lower-interest-rate bonds and reinvest the money into shorter-duration bonds with a higher yield. Instead, the sale dented the bank’s balance sheet and caused worried depositors to pull funds out of the bank.

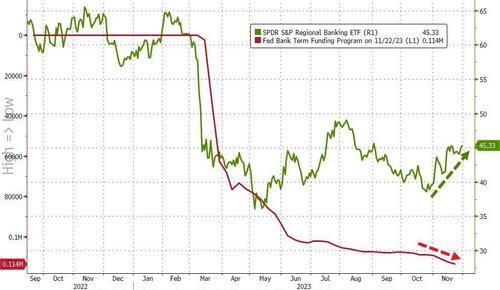

WolfStreet explained more generally how these “irrelevant” unrealized losses can suddenly become relevant.

Banks, via a quirk in bank regulations, don’t have to mark these securities to market value, but can carry them at purchase price. The difference between market value and purchase price is the ‘unrealized gain or loss’ that the bank must disclose in its quarterly financial filings, so that we the depositors can see them and get spooked by them and yank our money out, us billionaires and centimillionaires first, on the two fundamental principles of investing: 1, he who panics first, panics best; and 2, after us the deluge.”

The Federal Reserve set up a bailout program to allow banks to deal with this problem. Instead of selling bonds at a loss, cash-strapped banks can go to the Fed’s Bank Term Funding Program (BTFP) and borrow against them “at par” (face value). This allows banks to use these undervalued assets to raise cash (at least temporarily) without realizing big losses on their balance sheets.

As unrealized losses rise, banks continue to tap into this bailout program more than nine months after the crisis kicked off.

In effect, the Fed managed to paper over the financial crisis with this bailout program.

It basically slapped a bandaid on it. But it has not addressed the underlying issue – the impact of rising interest rates on an economy and financial system addicted to easy money.

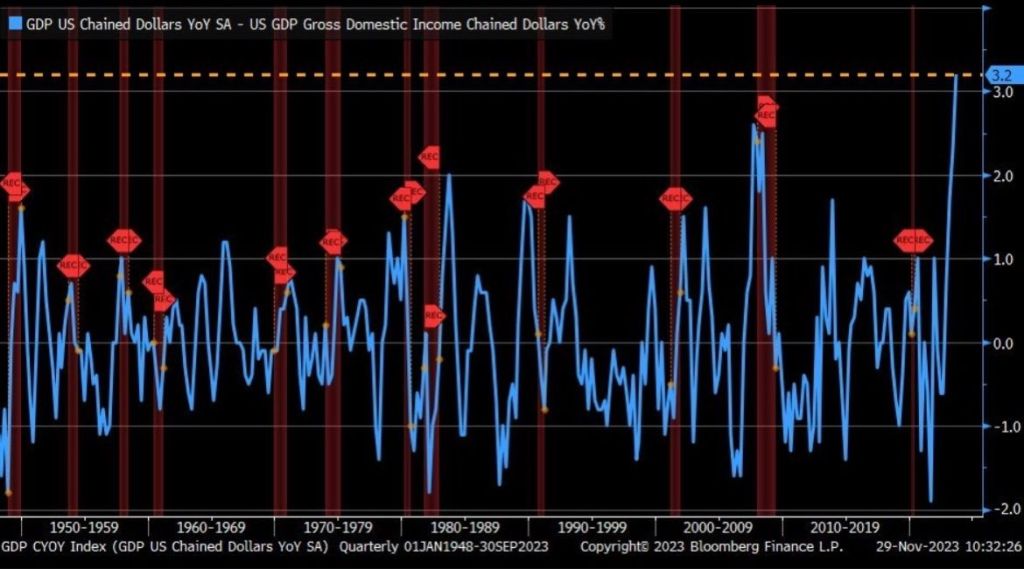

Remember, the US is on the cusp of a REAL recession, thank to Bidenomics.

The spread between real GDP and real Gross Domestic Income (GDI) just hit an all-time high. Even higher than The Great Recession of 2009.

Might as well have AC/DC’s Angus Young as US Treasury Secretary instead of tone-deaf Janet Yellen.

Despite The Fed’s attempts at cooling inflation down to 2%, we are seeing a re-animation of price increases. this time with home prices.

On a year-over-year basis, the Freddie Mac National FMHPI was up 6.0% in October, from up 5.1% YoY in September. The YoY increase peaked at 19.1% in July 2021, and for this cycle, bottomed at up 0.9% in April 2023. …

vv

Austin TX is the big loser, down -11.2% from peak. Followed by Idaho (largely people escaping from Newsomland (California) and speculators. The sixth leading area is Lake Havasu AZ.

As of October, 7 states and D.C. were below their previous peaks, Seasonally Adjusted. The largest seasonally adjusted declines from the recent peak were in Idaho (-4.5%), Utah (-2.7%), D.C. (-2.0%), and Nevada (-1.6%). Nevada, Idaho and Utah are now known as the Mild, Mild, West due to sagging home prices.

For cities (Core-based Statistical Areas, CBSA), here are the 30 cities with the largest declines from the peak, seasonally adjusted. Austin continues to be the worst performing city.

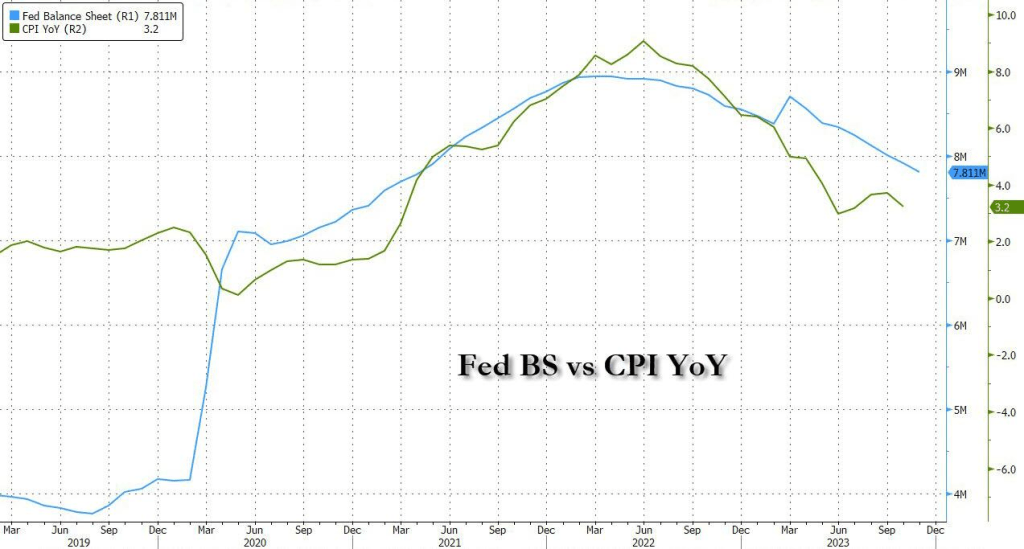

Speaking of inflation and The Fed, Biden claiming he lowered inflation is laughable if it wasn’t so sad. It is all The Fed. And their timidness is shrinking their balance sheet is contributing to persistent inflation.

So, yes, inflation is growing again. This time it is persisent and growing.

The US housing and mortgage markets are thunderstruck by The Fed’s attempts at cooling inflation down to 2%.

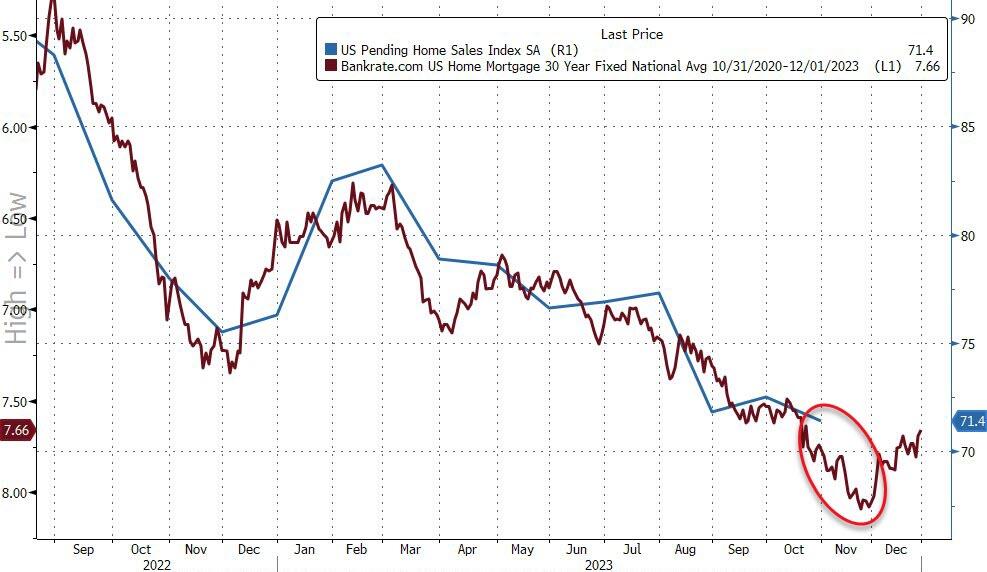

After a small bounce last month – following the puke in August – pending home sales dropped 1.5% MoM in October (better than the 2.0% MoM decline expected). This left YoY sales down 6.6% (negative for the 23rd straight month)…

Source: Bloomberg

The Pending Home Sales Index dropped back to a new record low…

Source: Bloomberg

By region, only the Northeast saw an increase in pending sales last month.

Sales fell the most in the West, down 6%, while contract signings in the South and Midwest slipped 1.9% and 0.4%, respectively.

Home sales are rising in places with more inventory, Lawrence Yun, NAR’s chief economist said, noting that purchases of new houses are up so far this year because of builders’ ability to create inventory.

“During October, mortgage rates were at their highest, and contract signings for existing homes were at their lowest in more than 20 years,” Yun said in a statement.

“Recent weeks’ successive declines in mortgage rates will help qualify more home buyers, but limited housing inventory is significantly preventing housing demand from fully being satisfied.”

The trend in pending home sales is following the mortgage rate (with a one month lag) and is set to fall further still…

Source: Bloomberg

The pending-home sales report is a leading indicator of existing-home sales given houses typically go under contract a month or two before they’re sold.

How long with Powell and his pals be able to keep this ‘higher for longer’ stress up as Americans’ largest source of wealth evaporates?

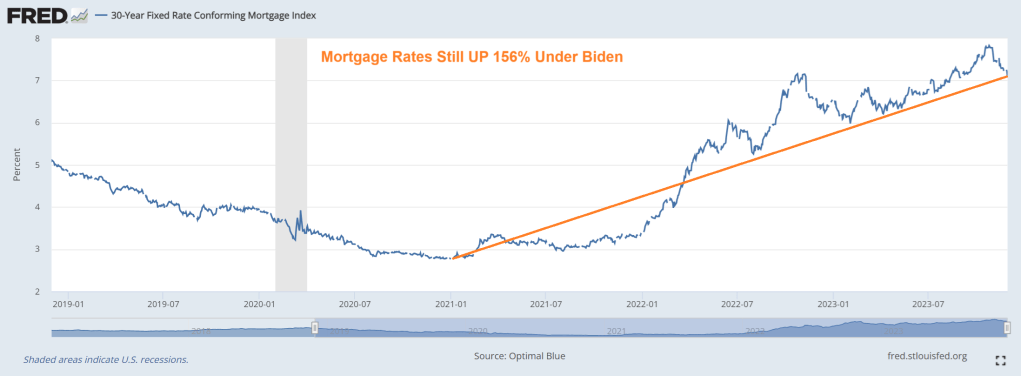

Mortgage rates have fallen recently, but are still up a staggering 156% under Biden.

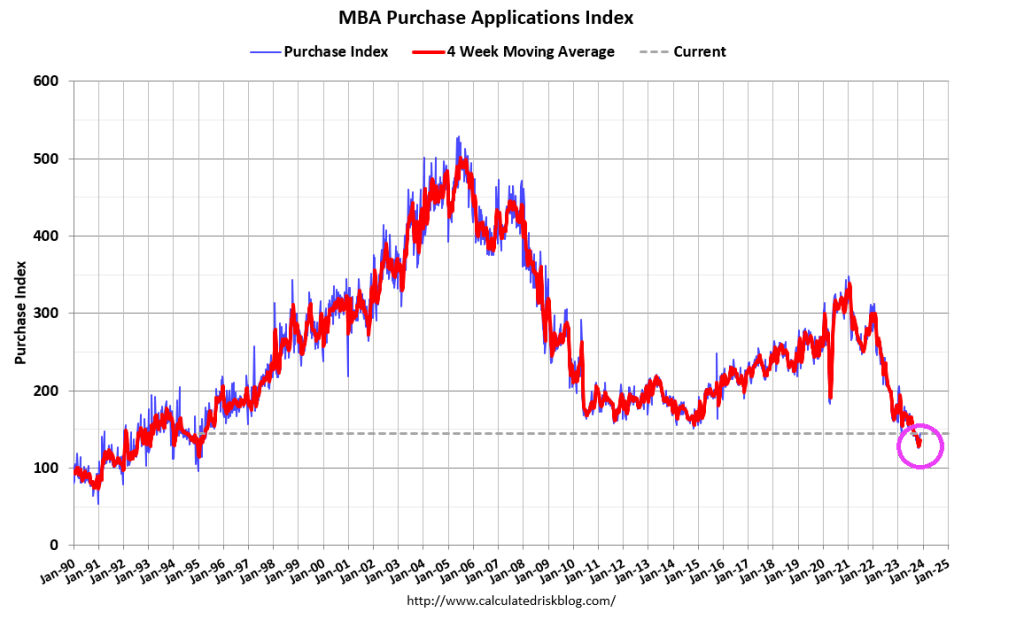

And mortgage purchase applications keep falling.

Here is The Fed keeping a close eye on the housing and mortgage market.

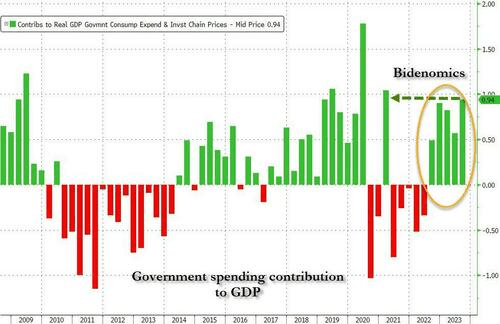

But was it organic growth or simply The Federal Government funding the defense and green energy industies with trillions in spending?

One factor has been government spending which grew an unsustainably 4.7% in real terms over the last year. Outside the pandemic, this is one of the fastest rates in decades and works at a cross purpose with monetary policy objectives.

Bidenomics is code for massive Federal spending (and debt) to fund Federal priorities: wars in Ukraine, Israel and likely involvement around Taiwan. And the costly switch to green energy (but not nuclear, for some reason).

If the US economy growing simply to function as a war machine and wealth transfer mechanism from the middle class to the 1%, we are on the Highway To Hell. Personal consumption contributed 2.44% to the bottom line GDP print in Q3, down from the pre-revision number of 2.69% but well above Q2’s 0.55%.

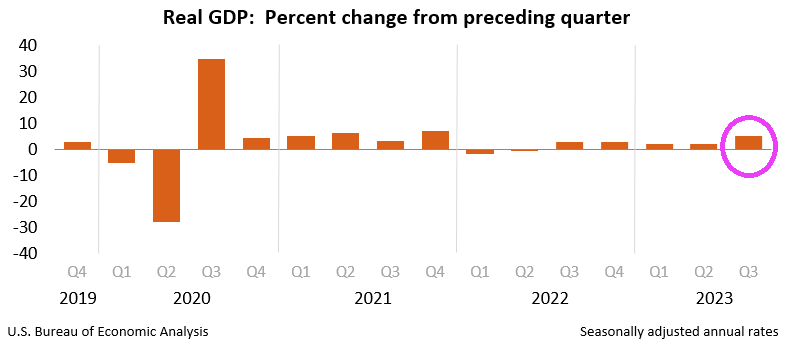

As expected, Q3 Real GDP was revised upwards to 5.2% annualized. Of course, this shatters JKP’s talking points that Biden inherited a train wreck of an economy from Trump. Q3 2020 Real GDP grew at over 30%.

And on a year-over-year (YoY) basis, US real GDP grew at 3.0% in Q3. Unfortunately, real hourly compensation grew at a measly 0.6% YoY.

Meanwhile, home prices have hit an all-time high. Too bad real wages are so low.

Why is growth so strong? One factor has been government spending which grew an unsustainably 4.7% in real terms over the last year. Outside the pandemic, this is one of the fastest rates in decades and works at a cross purpose with monetary policy objectives.

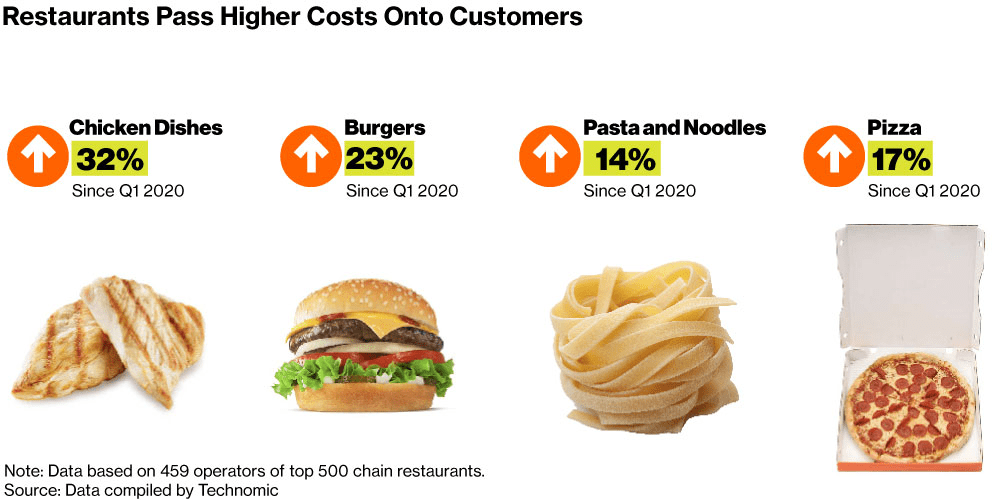

Despite Biden/KJP’s ridiculous lies about about this Thanksgiving being the 4th “cheapest” in history, inflation while cooling is still way up under Biden. In fact, food prices are up 25% since 2020.

Since 2020, US groceries are up 25%, used cars climbed 35% and rents roughly 20%. In 2020, a survey showed a 4-person household spent an average of $238.32 in a week on food at home. A similar survey in 2023 showed that figure had jumped 32% to $315.22.

Notice that food CPI peaked at 11.33% in August 2022 and has been declining since as M2 Money growth dies.

Of course, Biden blames high prices on … anyone but himself and big spending Congress. “Biden admits prices ‘too high’ but blames sellers for 18% inflation.” Sure Joe, the big spending bills you championed as part of Bidenomics that helped surge M2 Money supply (green line) has nothing to do with price increases, just the evil private sector.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.