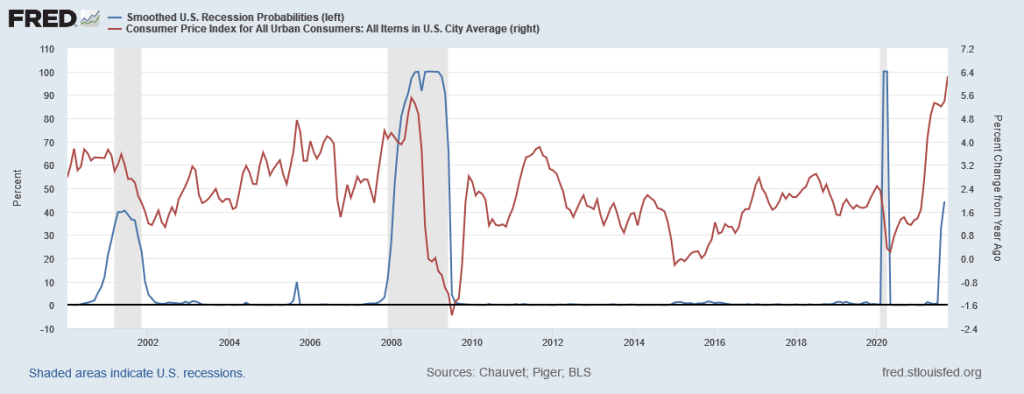

The Misery Index, inflation plus unemployment, is over 10% at 10.80%.

Unemployment has been steadily declining since the COVID shutdowns of 2020. The real culprit has been rapidly rising since COVID as well. At this point, inflation improvements (that The Fed is chasing) have been overwhelmed by inflation (which is being caused by The Fed’s monetary policy and Federal policies).

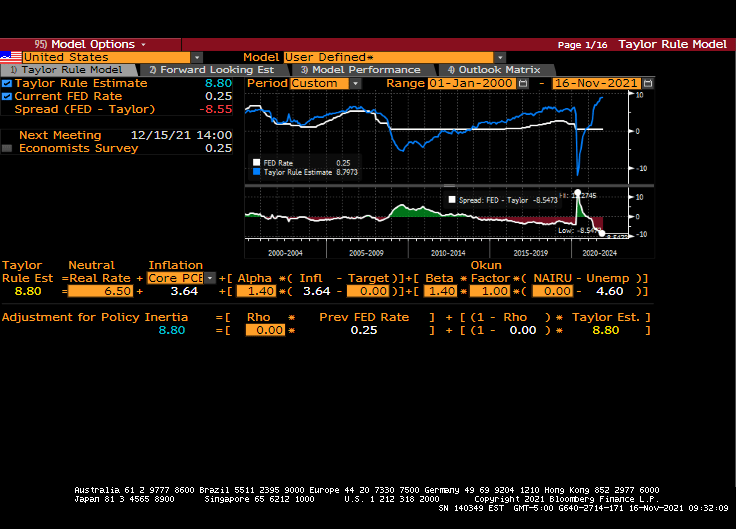

Powell has said that he is not going to raise rates until unemployment has improved, but risk more explosive inflation in striving to improve unemployment.

How I feel about Biden announcing Powell’s reappointment and uber-dove Brainard appointment as Deputy Fed Chair.

President Biden has decided to nominate Fed Chair Jerome Powell for a second term in an effort not to rock the boat. Lael Brainard is nominated for Deputy Chair.

To quote Gomer Pyle USMC, “Surprise, surprise, surprise!”

The humongous spending bill awaiting Joe Manchin to sign off on it will cost almost double what the CBO said it would. Why? Because spending programs in Washington DC never get cancelled, they only grow.

“We estimate the House Build Back Better Act includes roughly $2.4 trillion of spending and tax cuts along with roughly $2.2 trillion of offsets.However, the bill relies on a number of sunsets and expirations to keep the official cost down. If the plan’s temporary policies were made permanent, we find the cost would increase by as much as $2.5 trillion.As a result, the gross cost of the bill would more than double from $2.4 trillion to $4.9 trillion.

The Build Back Better Act relies on a number of arbitrary sunsets and expirations to lower the official cost of the bill. These include extending the American Rescue Plan’s Child Tax Credit (CTC) increase and Earned Income Tax Credit (EITC) expansion for a year, setting universal pre-K and child care subsidies to expire after six years, making the Affordable Care Act (ACA) expansions available through 2025, delaying the requirement that businesses amortize research and experimentation (R&E) costs until 2026, and setting several other provisions – from targeted tax credits to school lunch programs – to expire prematurely.

Excluding changes to the state and local tax (SALT) deduction, we estimate the Build Back Better Act would cost $2.1 trillion as written. We estimate making all of these temporary policies permanent would cost roughly $2.2 trillion, more than doubling the gross cost of the bill to $4.3 trillion through 2031.”

When asked about the Center for a Responsible Budget saying the bill could be twice as expensive, Manchin replies “it’s concerning. Sure. It’s concerning.”

Surprise, surprise, surprise! And it is certainly more expensive than the estimate Biden gave: $0.

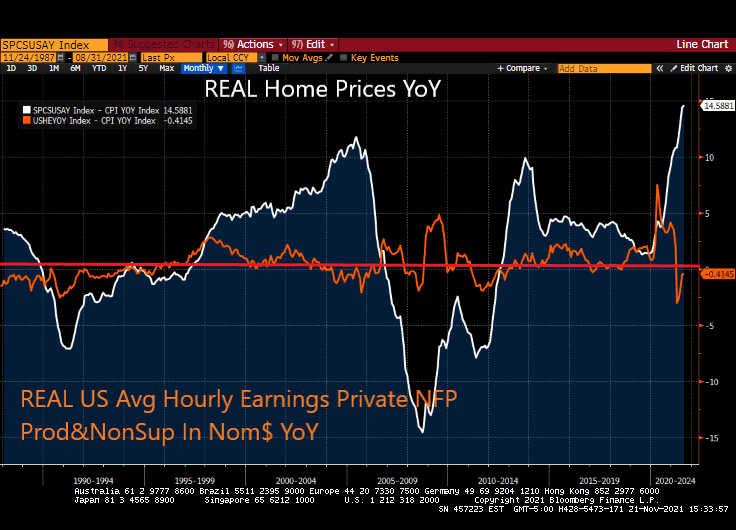

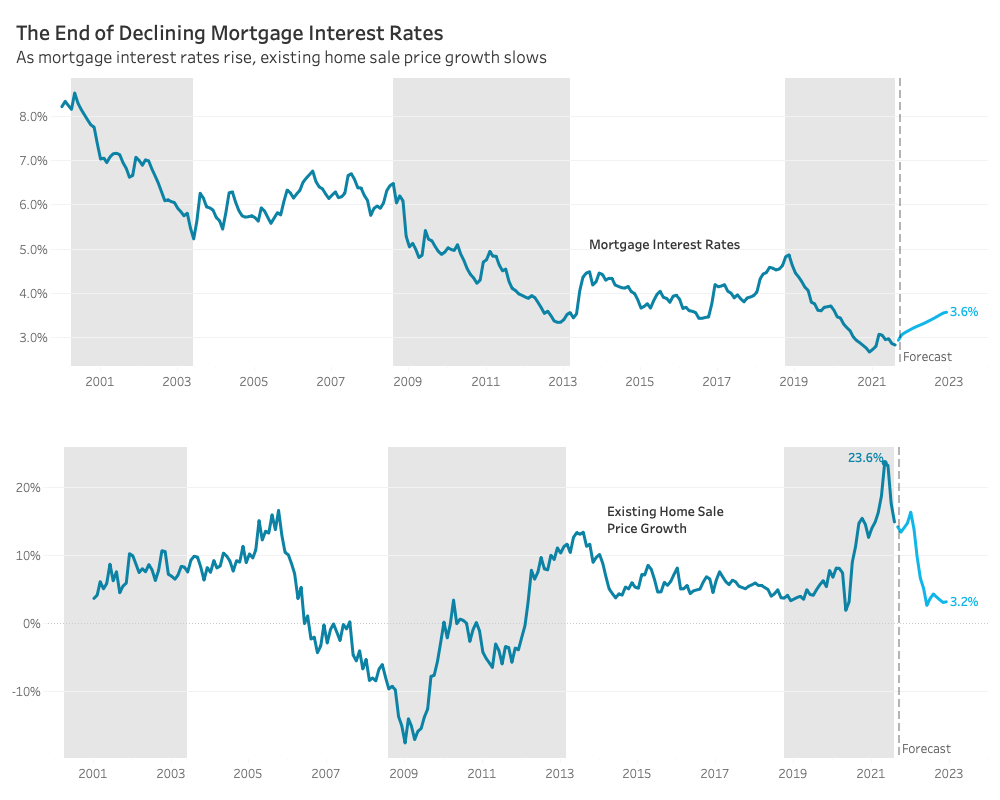

Welcome to The Fed’s Gilded Age … for housing! The gilded age refers to the thin-veneer of gold covering up problems in the late 1800s.

Today’s gilded age is largely fueled by The Federal Reserve’s uber-easy monetary policies combined with absurd Federal government policies. The result? Thanks to inflation, REAL home prices are growing at 14.6% YoY while REAL hourly earnings are declining (-0.41% YoY).

Redfin predicts a more balanced housing market in 2022. Part of their rationale is that they predict mortgage rates will rise to 3.6%. This growth in the mortgage rate is predicted to slow home price growth to 3.2% from double digit growth currently.

While this scenario is plausible, it will require a change in direction of the 10-year Treasury yield which has been declining since 1981. 5.39% YoY inflation may encourage The Fed to raise rates.

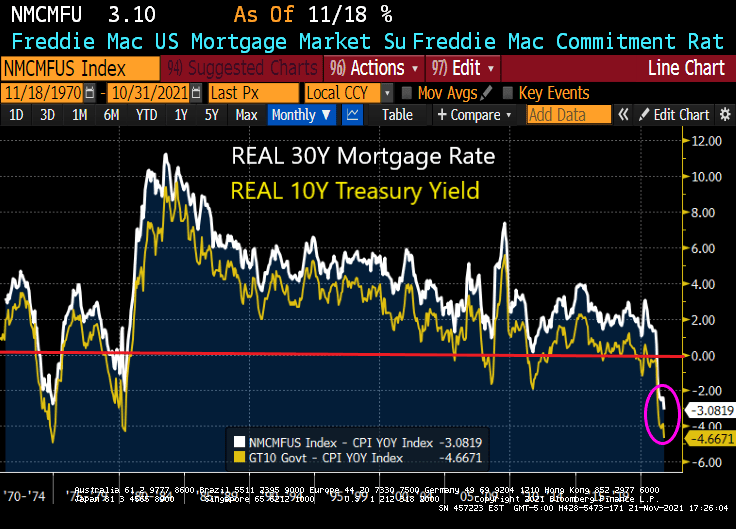

Today’s REAL 30-year mortgage rate is -3.08% while the REAL 10-year Treasury yield is -4.67%. It will require a reduction in inflation AND an increase in the nominal rate to get to 3.6%.

With the Freddie Mac 30-year survey rate at 3.10, will a 50 basis point increase in mortgage rates send the market crashing? Not likely.

After all, the US economy is under the thumb of The Federal Reserve.

The Marty Stuart/Travis Tritt song “This One’s Gonna Hurt You (For A Long, Long Time)” seems appropriate for the plight of the middle and lower income classes in the face of high inflation. How do you spell the combination of President Biden’s policies and The Fed’s inaction on inflation? T-R-O-U-B-L-E … for the middle and lower income classes.

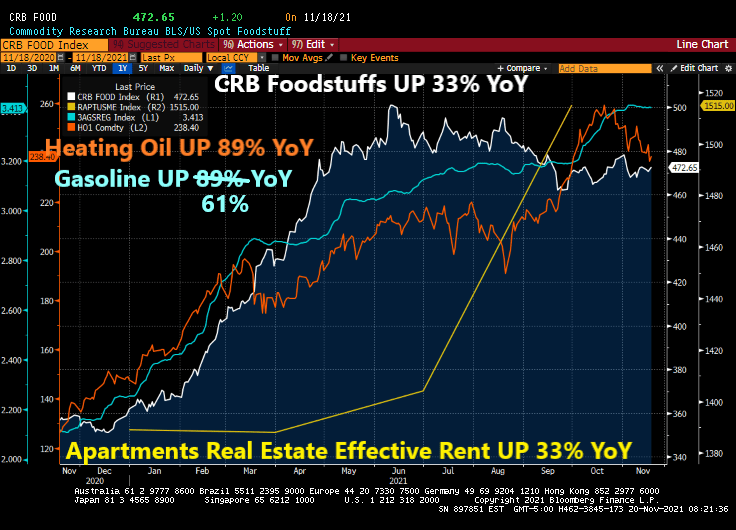

Over the past year, since the election of Joe Biden, the household consumption bundle (food, rent, heating, gasoline) have all risen dramatically in terms of prices. Food is up 33%, heating oil is up 89%, regular gasoline is up 61%, and effective apartment rents are up 33%.

Meanwhile, the 1% are sitting high on a mountain top obvious to the pain caused by The Federal Reserve and Biden Administration. Here is the growth in wealth by the 1% since the housing bubble burst and financial crisis compared with the bottom 50%.

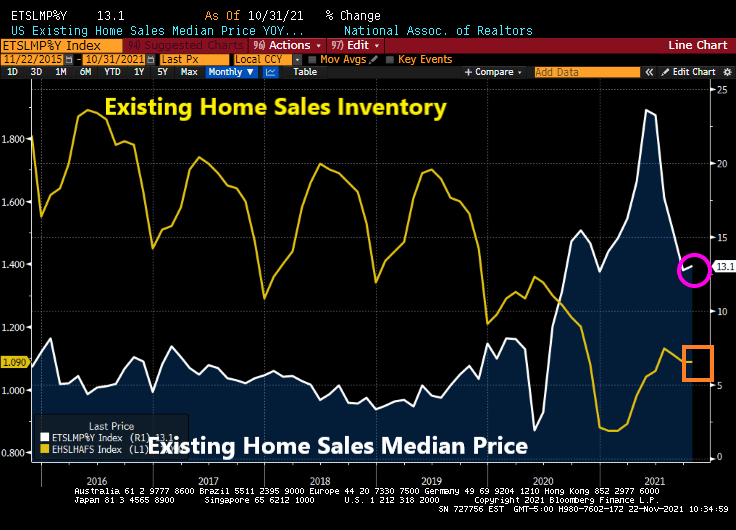

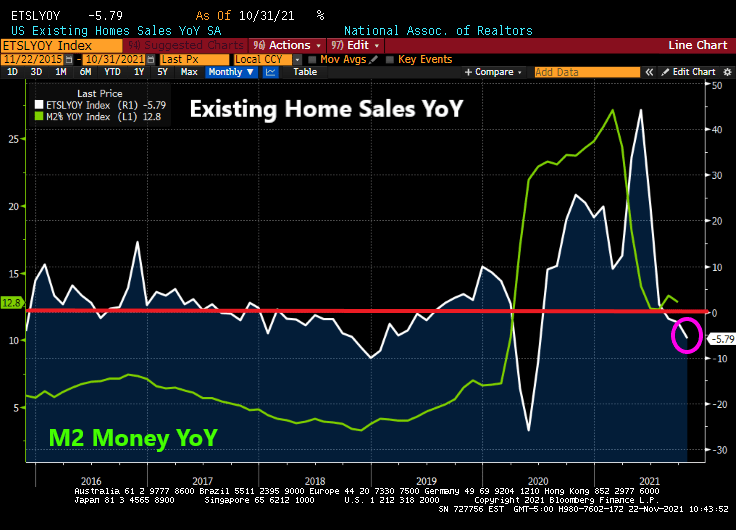

A problem facing renters is the rapid growth of home prices particularly since the COVID epidemic. At least M2 Money has “slowed” to 12.80% YoY while home prices are raging at almost 20% YoY. But hopefully home price growth will slow with declining M2 growth.

Compendium of Fed Chair Jerome Powell and President Biden on vacation.

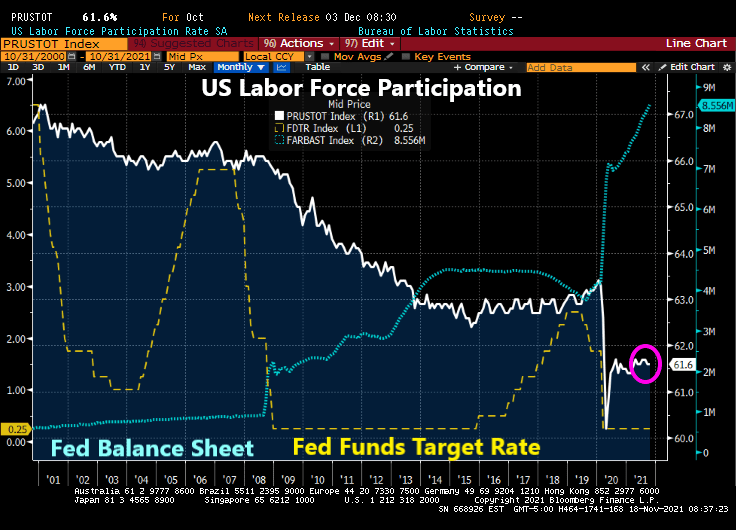

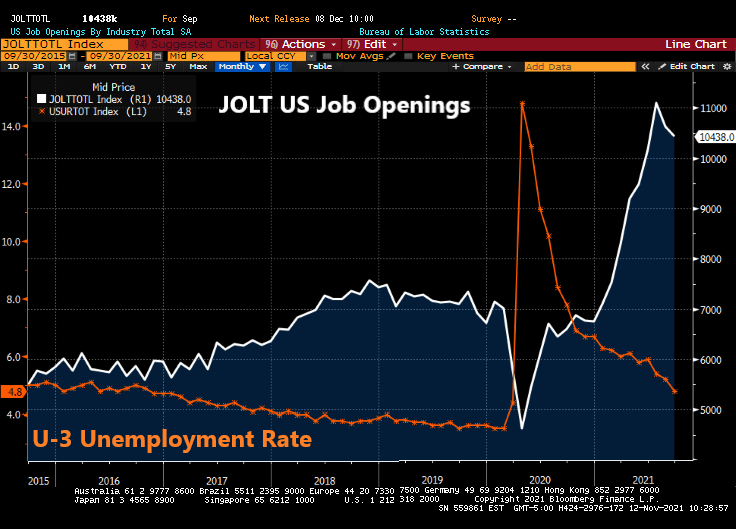

Is the US at full employment? That is, is the US at REALISTIC full employment? And if the US is at realistic full employment, why is The Federal Reserve keeping rates at 25 basis points??

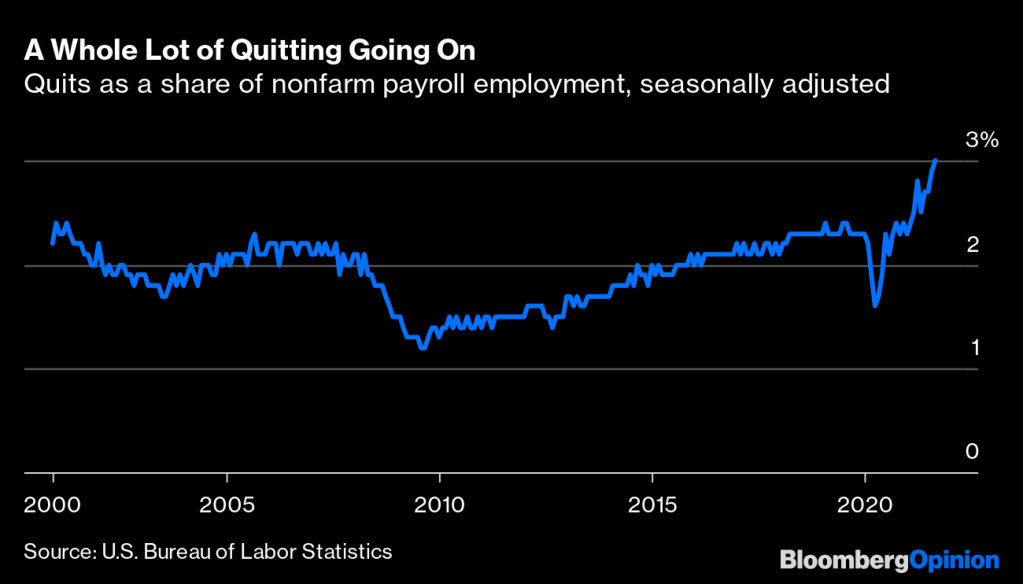

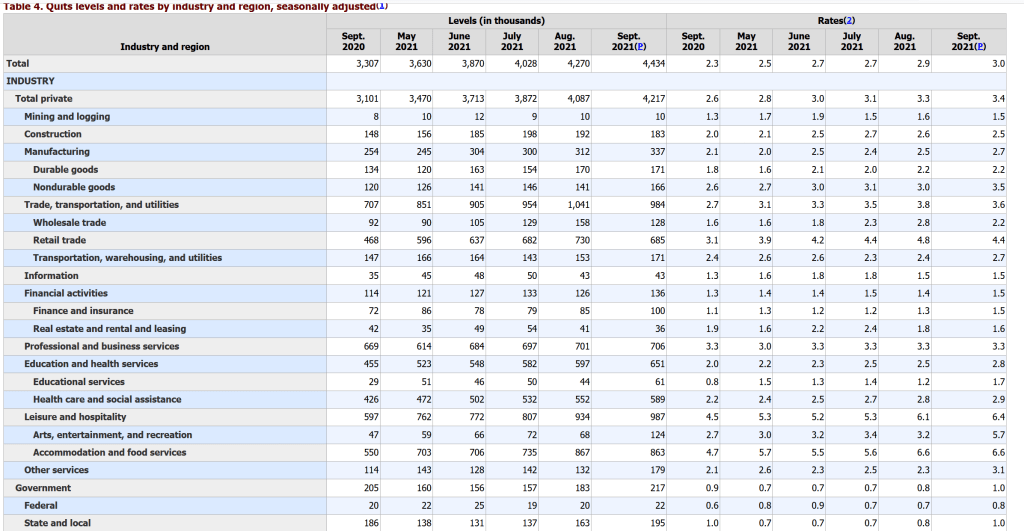

Let’s start with the “quits” data. An estimated 3% of American workers quit their jobs in September, the Bureau of Labor Statistics reported last week.1That’s the highest percentage since the BLS started keeping track two decades ago.

Front-line and low-wage workers are leaving at rates higher than historical norms while higher-paid office workers aren’t. College-educated workers haven’t been quitting or dropping out of the workforce at higher rates than before the pandemic, but less-educated workers have.

The quits rate in professional and business services was just 0.4 percentage points higher in September than before the pandemic in February 2020. In financial activities it was unchanged. In the information sector, made up of telecommunications, publishing, broadcasting, motion pictures, software and most internet companies, the quits rate was down 0.3 percentage points.

The biggest increases in quit rates were in sectors such as leisure and hospitality where office workers are few, working remotely seldom an option and wages low. Within manufacturing, the quits-rate increase has been much bigger in lower-paying nondurable goods (of which food manufacturing is the biggest part) than in higher-paying durable goods.

In particular, fast food restaurants are offering above minimum wage salaries to attract workers. Burger King was even offering college tuition (not to University of Chicago, but to the local community college).

Labor force participation crashed with COVID and has struggled to recover, despite the staggering monetary stimulus. If this a sign that the US is at full employment (or very difficult to entice workers to enter and stay in the labor force)?

US housing starts for October were less than expected. A 1.5% increase MoM was expected, but housing starts actually fell -0.7% MoM.

5+ unit (multifamily) starts were up 6.82% MoM. 1-unit single family detached units were down -3.89% MoM. Permits to build were up 4% MoM.

On a YoY basis, 1-unit start declined -10.6% as M2 Money growth continues to fall.

And 1-unit housing starts have fallen with the rapid decline in home buying sentiment.

1-unit starts have slowed to pre-COVID levels, thanks in part to The Federal Reserve’s money printing bonanza which may never end.

As housing sentiment crashes (due to rapid home price growth), we are seeing the demand for multi-family housing rise. 5+ unit (multifamily) starts were up 6.82% MoM in October.

I wonder if Biden’s Press Secretary Jen Psaki will argue that inflation is transitory … again?

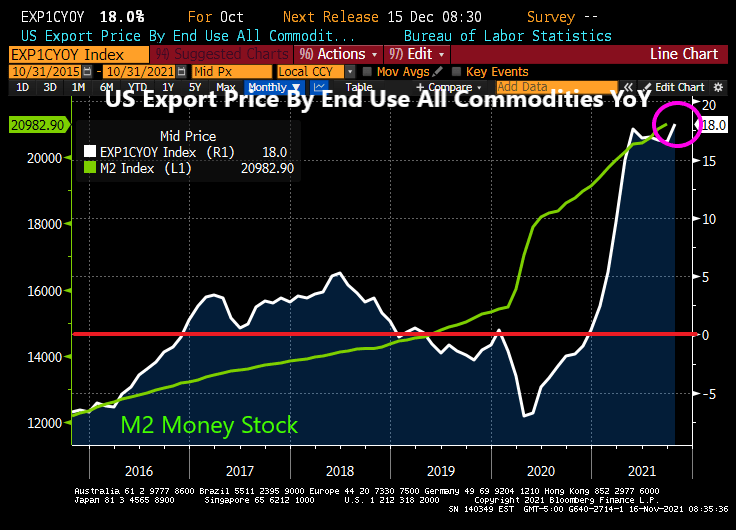

Well, the US is exporting inflation to our trading partners. US Export Prices by end use rose 18% YoY.

Of course, with the Biden Administration shutting down energy pipeline and drilling, it is not surprising.

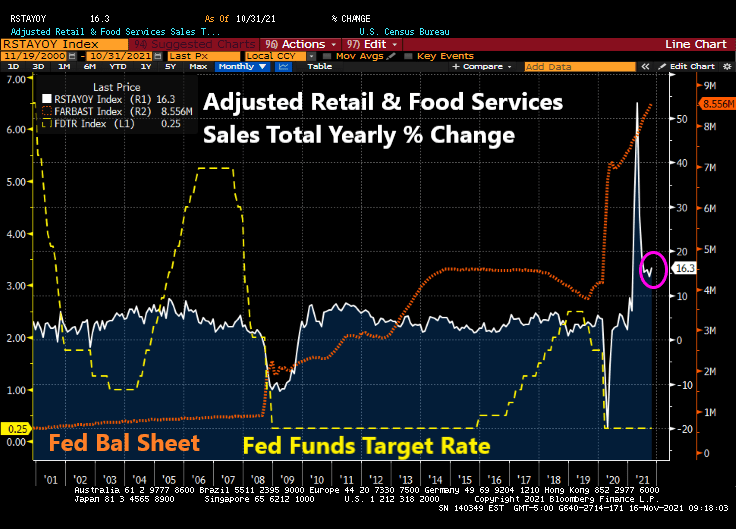

Then we have the advance retail sales numbers for October. Growing at 16.3% YoY with massive monetary stimulus still in play.

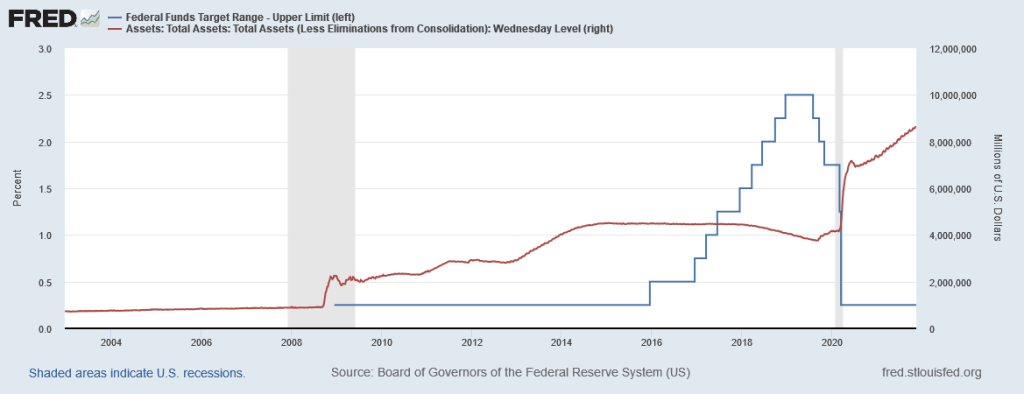

Then we have Federal Reserve Bank of St. Louis President James Bullard saying that the central bank should speed up its reduction of monetary stimulus in response to a surge in U.S. inflation.

You mean like what Mankiw’s specification of the Taylor Rule model suggests??

How did healthcare insurance companies get a seat at the table for the massive infrastructure bill is beyond me.

President Biden and Congressional Democrats are celebrating the signing of the $1.2 trillion Infrastructure Bill at the White House. Remember, of the $1.2 trillion estimated price tag, less than 10 percent –$110 billion – will fund true infrastructure: bridges, roads, tunnels, and waterways.

And what the hell is healthcare doing in the infrastructure bill?

H.R. 3864 will restore a 2 percent cut in reimbursements to Medicare providers, on top of all the other federal payments reductions.

A second health care provision buried in the $1.2 trillion infrastructure bill delays implementation of the Medicare Part D Rebate Rule, a Trump-era rule that would inject competitive forces into the market for prescription drugs. Just like payment cuts, by delaying this rule, desperately needed drugs will remain unaffordable and therefore unavailable.

And they wonder why there is a going concierge medicine movement that won’t accept Medicare and healthcare insurance. It is The Red Hour for free markets.

“I am Landrieu.” Former mayor of the most corrupt city in the United States. Makes sense that Biden would choose Landrieu to coordinate the infrastructure plan.

You must be logged in to post a comment.