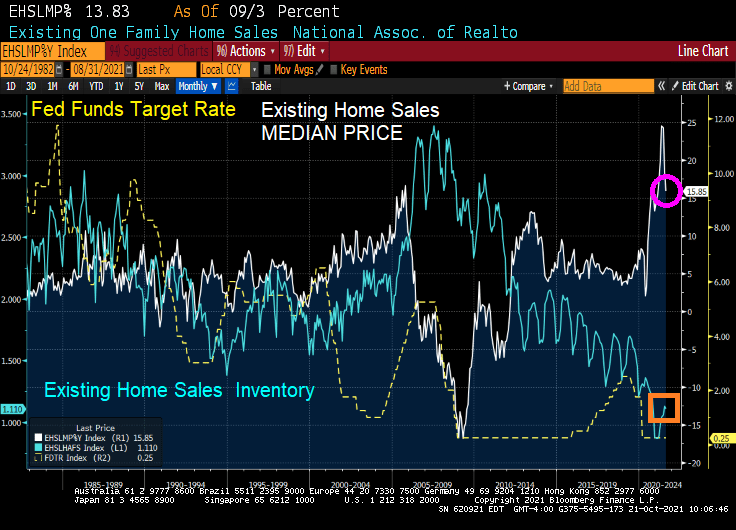

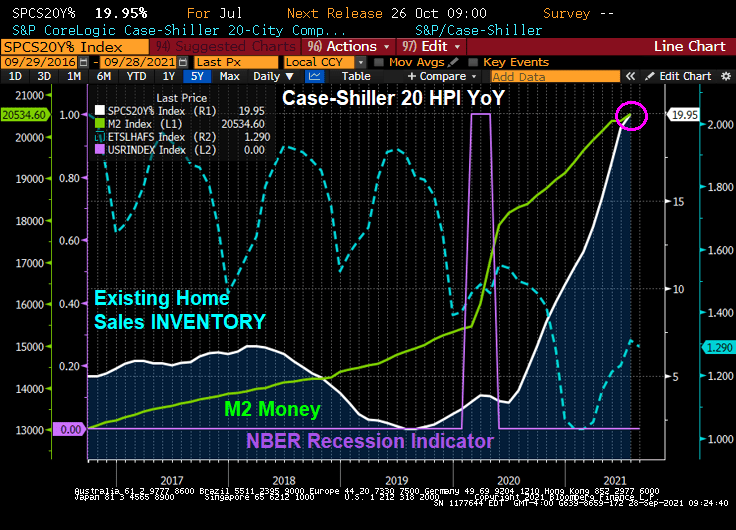

It was a surprise to see 6.29 million home sold SAAR in September. That is a 7% MoM growth rate.

The median price of existing home sales GROWTH slowed to 15.85% YoY (it was over 24% for the last two months).

And INVENTORY of existing homes for sale remains MIA.

Perhaps President Biden can issue an executive order forcing households to place their homes up for sale if they refuse to get vaccinated for Covid. /sarc

Yes, the super-heated housing market is showing signs of slowing down.

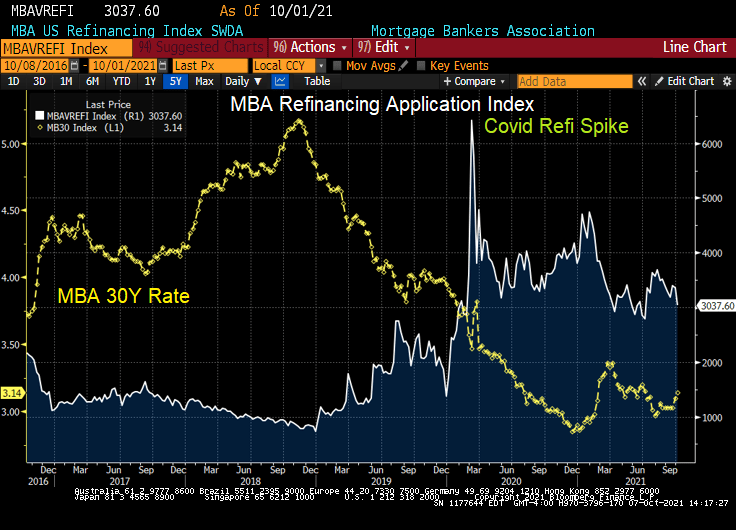

According to the Mortgage Bankers Association (MBA), mortgage purchase applications rose 1.87% from the previous week. However, purchase applications are down 10% from the same week last year.

Refinancing applications dropped -.48% from the previous week as the 30-year mortgage contract rate rose from 3.14% to 3.18%. Refi apps are up 6% from the same week last year.

As rates begin to rise, mortgage refi applications will decline.

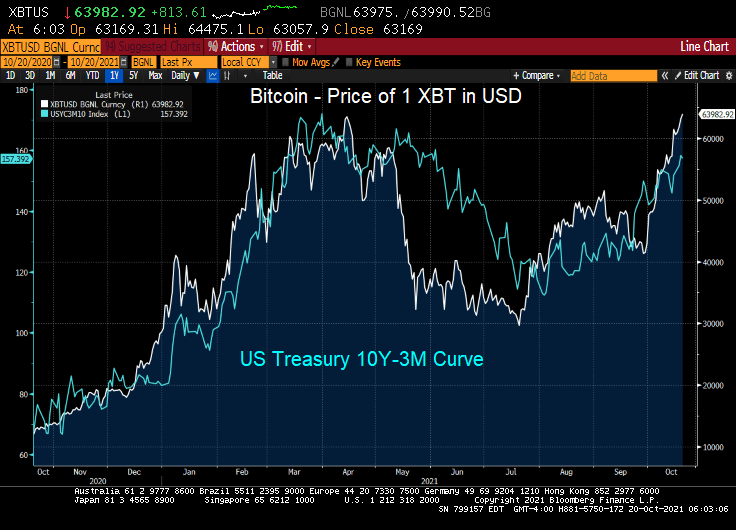

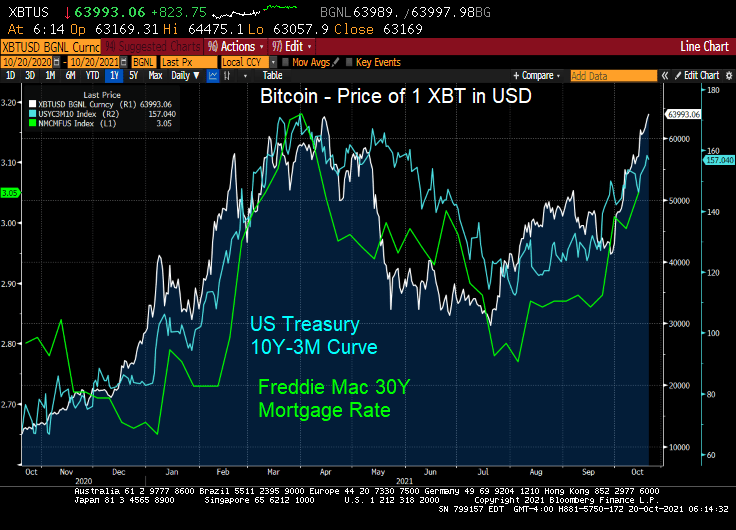

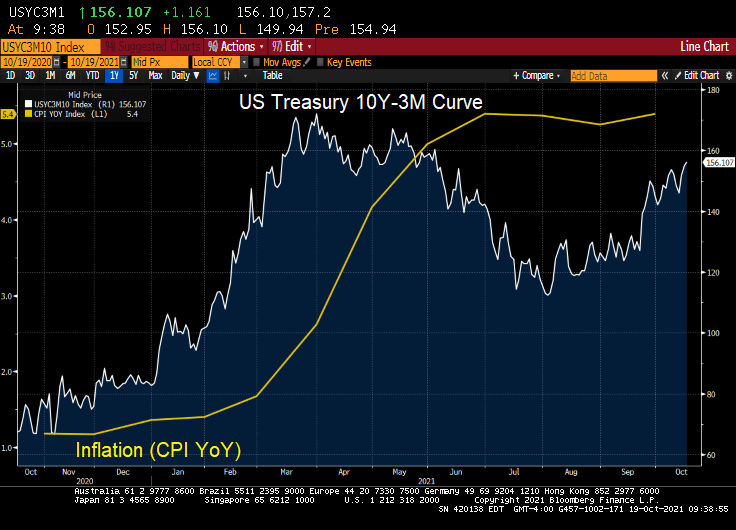

I have no idea why Jack Dorsey tweeted “705742.” But I do know that Bitcoin hit 63,982.92 this morning as the US 10Y-3M curve has been steepening.

Since the 3-month Treasury yield has been repressed to near zero, the 10Y-3M curve is pointing to rising 10-year yields. Which likely means that 30-year mortgage rates will be rising too.

UPDATE! Bitcoin hits 66,615 as Proshares Bitcoin Strategy E rises as well.

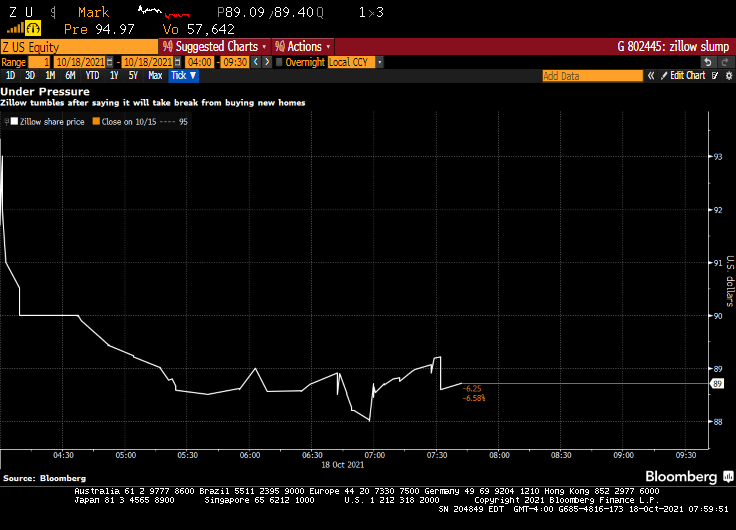

Zillow Group Inc. shares fell as much as 6.8% in premarket trading Monday after the online real estate firm said it would stop buying new homes and work to clear a backlog of properties it already has.

The Seattle-based company, which acquired more than 3,800 homes during the second quarter, has seen its stock price tumble about 27% this year after it nearly tripled in 2020 amid the pandemic-fueled housing market boom.

The shares have come under additional pressure in recent weeks after a viral TikTok video from a real estate agent in Las Vegas said an unnamed company was pulling off a convoluted scheme to manipulate housing prices in his home market. Zillow is also facing increased competition from firms like Opendoor Technologies Inc., which announced in August that it bought about 8,500 homes during the second quarter.

Zillow, which acquired more than 3,800 homes in the second quarter, will stop pursuing new home purchases as it works through a backlog of properties already in its pipeline.

“We are beyond operational capacity in our Zillow Offers business and are not taking on additional contracts to purchase homes at this time,” a spokesperson for Zillow said in an email. “We continue to process the purchase of homes from sellers who are already under contract, as quickly as possible.”

Zillow is best known for publishing real estate listings online and calculating estimated home values – called Zestimates – that let users keep track of how much their home is worth. The popularity of the company’s apps and websites fuels profits in Zillow’s online marketing business.

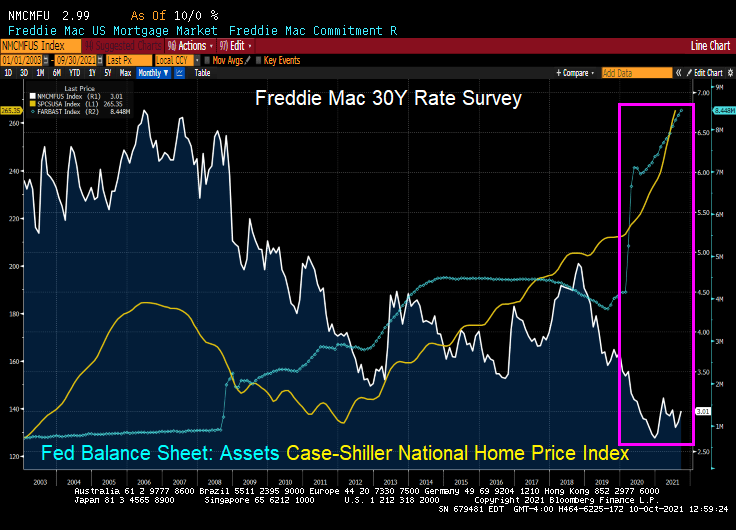

Of course, The Fed dumping in trillions into a bottlenecked housing market is helping to fuel the flipper fire.

Is this a secret warning about a possible slowdown in the housing market?

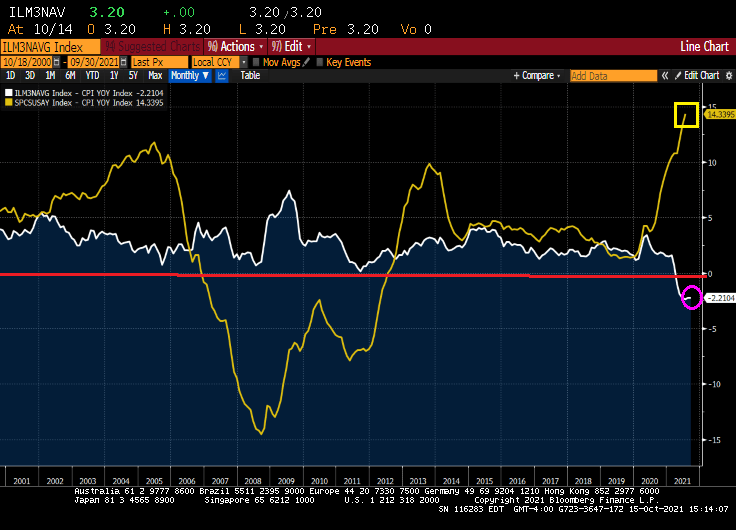

This is a time even unlike the disastrous housing bubble of the 2000s that led to the financial crisis and Great Recession. Even during the housing bubble years, we still had positive REAL mortgage rates: Bankrate 30Y Fixed rate – CPI YoY. But today we have even FASTER REAL home price growth and NEGATIVE mortgage rates!

And yes, REAL home price growth is 14.34% YoY while REAL hourly earnings growth is -0.79%.

The University of Michigan consumer survey came out today and buying conditions for housing improved to 75. Which means that more people were negative than positive due to skyrocketing home prices.

With negative 30Y mortgage rates and rising apartment rents, is it time to buy? Just remember what happened to Leon in Blade Runner.

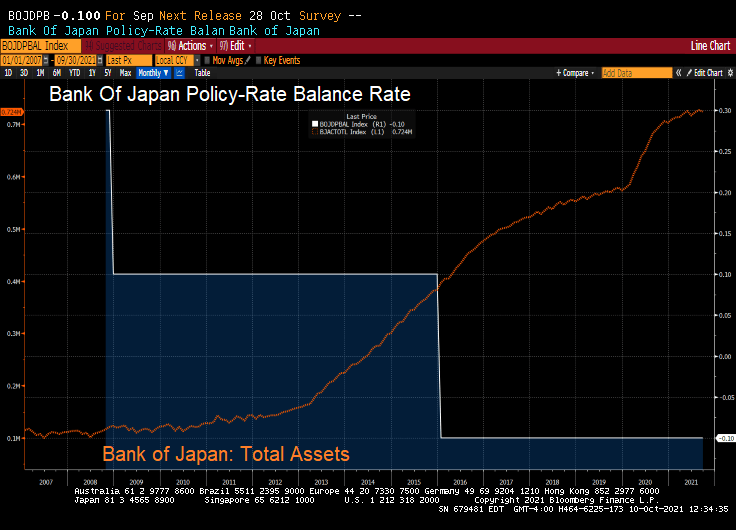

What’s left of it is that the BoJ (and Bank of Japan Governor Haruhiko Kuroda) now holds about half of the huge pile of the central government’s debt. With their target rate at -0.10% and a gargantuan balance sheet, what could go wrong?

But BOJ’s QE has ended. The BoJ’s overall assets stopped growing, and its holdings of government bonds have started to decline.

As of the BoJ’s balance sheet dated September 30, released on Thursday, total assets declined to a still monstrous ¥724 trillion ($6.4 trillion), below where it had been in May 2021.

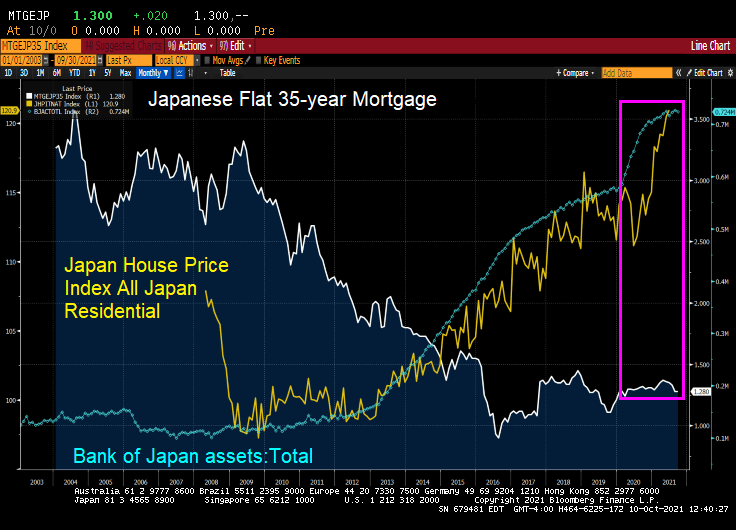

But look at Japanese home prices with the growth of the BOJ’s balance sheet and general decline in mortgage rates. Like the USA, there was a balance sheet spike associated with Covid and a resulting spike in home prices.

The USA? We also saw a surge in home prices following The Fed’s monetary “stimulypto.”

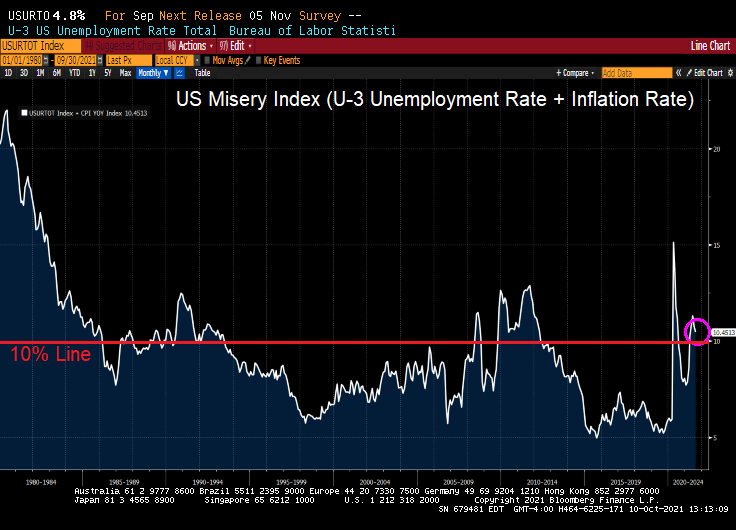

Bear in my that the US Misery Index is above 10% (U-3 unemployment + inflation).

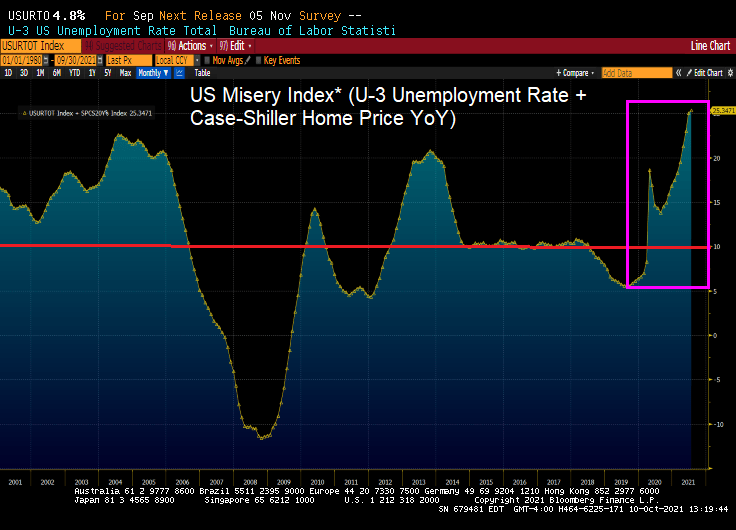

And if I define the US Misery Index as U-3 unemployment + home price growth, we can see we are at record misery rates. Miserable for households that don’t own a home or are trying to move to a higher housing price area).

It was great to be a “Master of the Universe” (Treasury and MBS trader) since October 1981 when the US 10Y Treasury yield peaked at 15.84% and mortgage rates peaked at 18.63%. Treasury and mortgage rates have generally fallen ever since. But what happens if Treasury and mortgage rates rise?

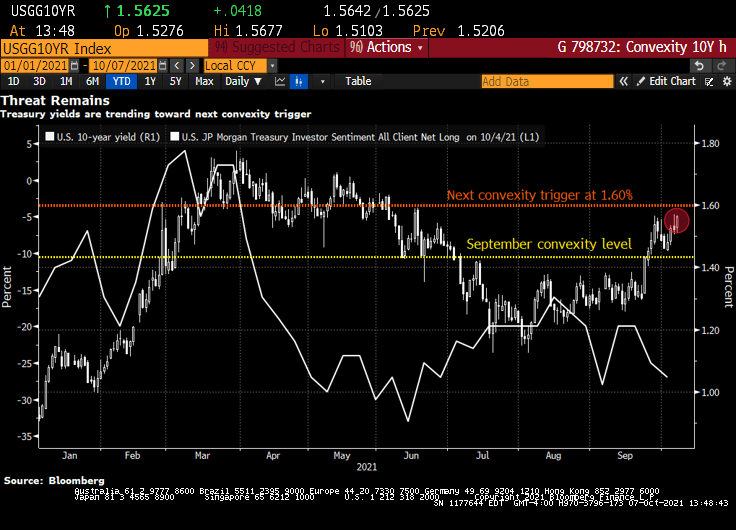

Bond investors are piling back into short positions, motivated not only by the specter of inflation but also by the risk that yields are approaching levels that will unleash a wave of new selling by convexity hedgers.

That level is around 1.60% in the U.S. 10-year Treasury yield, less than 10 basis points from its current mark, according to Brean Capital’s head of fixed income strategy, Scott Buchta. It’s the mid-point of “a key threshold” between 1.40% to 1.80%, an area “most critical from a convexity hedging point of view.”

Convexity hedging involves shedding U.S. interest-rate risk to protect the value of mortgage-backed securities as yields rise, slowing expected prepayment rates.

It’s already begun to pick up as yields stretched past the 1.40% level. Another wave is expected at around 1.6% — a point of “maximum negative convexity” in agency MBS, “where 25bp rallies and sell-offs should have an equal effect on convexity-related buying and selling,” Buchta says.

Signs that short positions are accumulating include Societe Generale’s “Trend Indicator.” Among its 10 newest trades are short positions in Japanese 10-year debt, German 5-year debt futures, U.K. 10-year gilts, U.K. short sterling and U.S. 2- and 5-year notes. Meanwhile, CFTC positioning data for U.S. Treasury futures show asset managers flipped to net short in 10-year note contracts in the process of dumping the equivalent of $23 million per basis point of cash Treasuries over the past week. Hedge-fund shorts also remain elevated in the long-end of the curve, as measured by net positions in Bond and Ultra Bond futures.

“Bond-bearish impulses remain in place,” says Citigroup Inc. strategist Bill O’Donnell in a note, citing tactical and medium-term set-ups. Traders should be aware of short-covering rallies in the meantime, however, he says.

“Potentially extreme short-term positioning and sentiment set-ups could easily allow for a counter-trend correction under the right conditions,” he said.

U.S. 10-year yields topped at 1.57% this week, the cheapest level since June, spurring the breakeven inflation rate for 10-year TIPS to 2.51%, the highest since May. Friday’s September jobs report could add fuel to this inflationary fire, rewarding bond shorts.

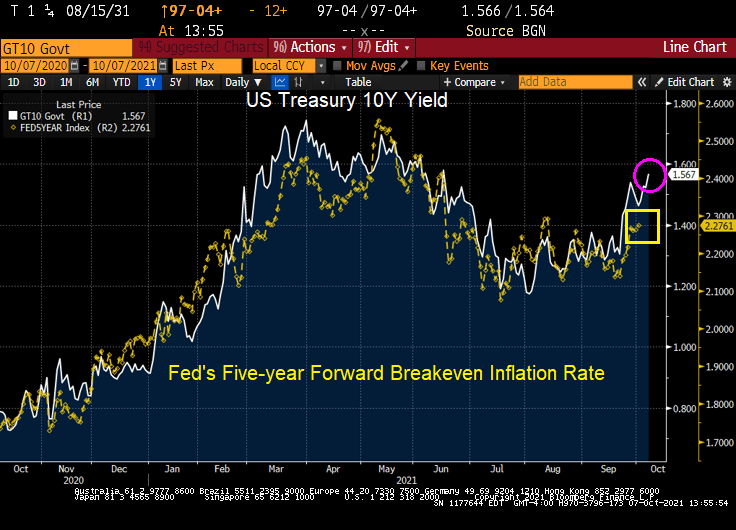

Here is a chart of the rising 10Y Treasury yield against The Fed’s 5Y forward breakeven rate.

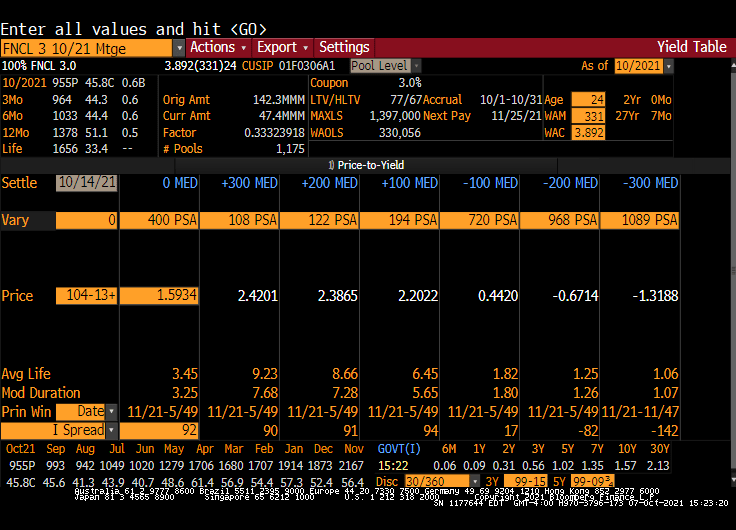

Here is a Fannie Mae 3% coupon MBS. Note the rise in Modified Duration with an increase in interest rates.

Can you say “All the king’s horses and all the king’s men ..” Or “All The Fed’s stimulus and all of Biden’s jobs bills ..”

Yes, the Atlanta Fed’s GDPNow Q3 tracker slumped to 2.3% despite the massive stimulus coming from The Federal Reserve and the Biden Administration. Down from 13.7% GDP growth as of 5/5/2021.

So much for the transitory inflation that The Federal Reserve keeps spouting on about.

(Bloomberg) — The pace of rent increases is heating up in the U.S.

Rent data for the past two months show no sign yet of the usual seasonal dip at this time of year, following peaks early in the summer, when many lease renewals come due.

A Zillow Group Inc. index based on the mean of listed rents rose 11.5% in August from a year earlier, with some cities in Florida, Georgia and Washington state seeing increases of more than 25%.

Since the start of the pandemic, the median rent for a two-bedroom apartment has soared 13.1% to $1,663, Zumper data show.

But rent on newly-signed leases rose 17% from the previous tenant’s lease.

For the New York market, landlords are raising rent prices as much as 70% now that people are flooding back into the city as offices and entertainment venues open up. In July, the median asking rent in New York City surged to $3,000, compared with the pandemic low of $2,750 in January 2021, data from StreetEasy showed.

Of course, rent surge is not surprising given that home prices have surged since Covid given limited inventory and massive Fed stimulus.

Perhaps if The Fed and Federales (Federal government) start reducing their apocalyptic-level stimulus, THEN we will see inflation as transitory.

You must be logged in to post a comment.