Its Thanksgiving in the USA! Confession: I don’t like turkey. Prime rib with horseradish sauce? You bet!!

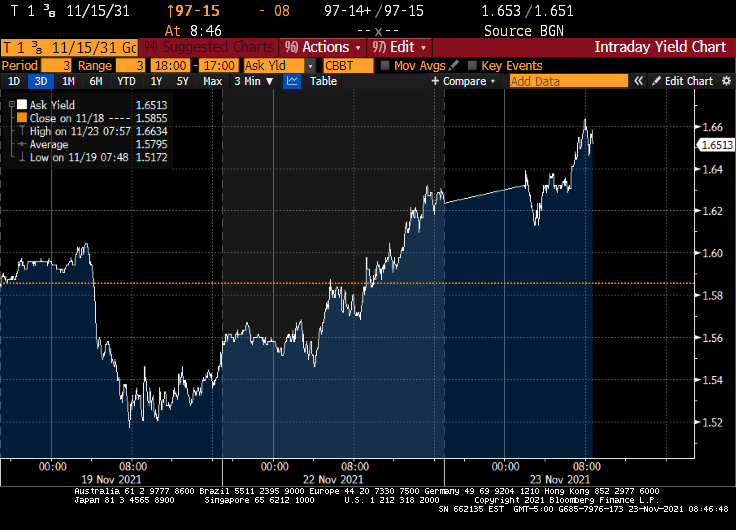

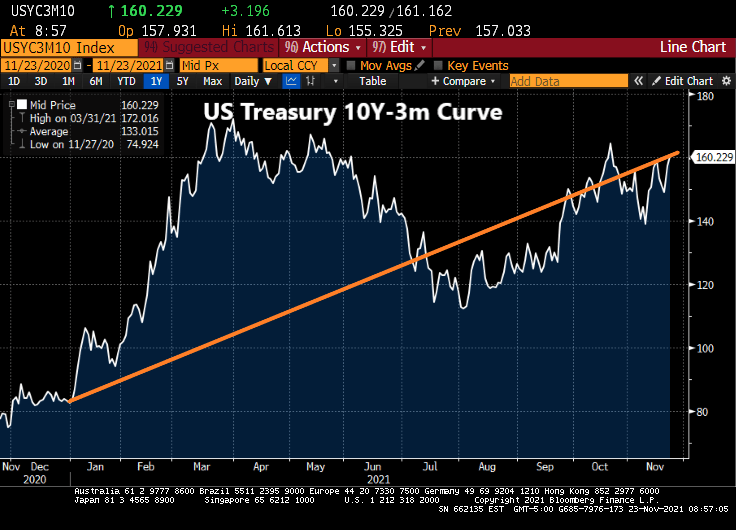

Anyway, Treasuries ended mixed Wednesday with the yield curve sharply flatter after a raft of U.S. economic data and minutes of the November FOMC meeting bolstered expectations for an earlier start to Fed rate increases. Two- and 5-year yields reached YTD highs, and 5s30s spread reached narrowest since March 2020.

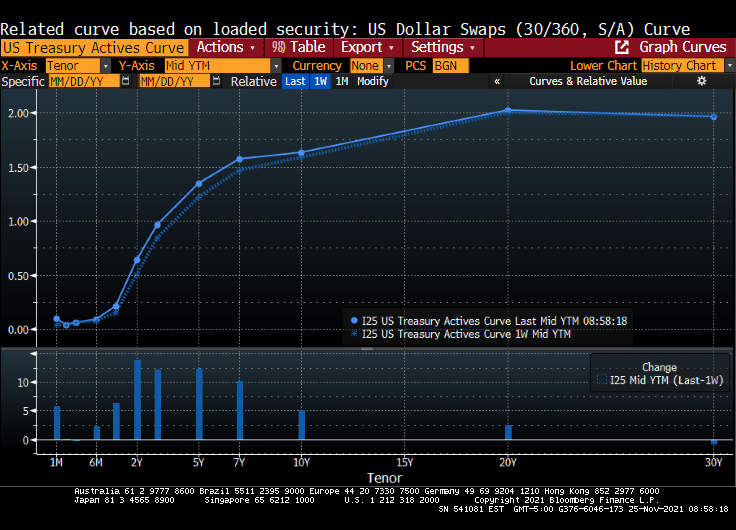

Over the past week, the Treasury actives curve rose 13.85 basis points at the 2 year tenor.

Yields ended richer by ~6bp across long-end of the curve, while front-end cheapened almost 3bp; 2s10s flattened more than 5bp, 5s30s more than 6bp; 10-year yields shed ~3bp to ~1.635%

Release of Nov. 2-3 FOMC meeting minutes drew minimal market reaction, as flatter curve held its shape.

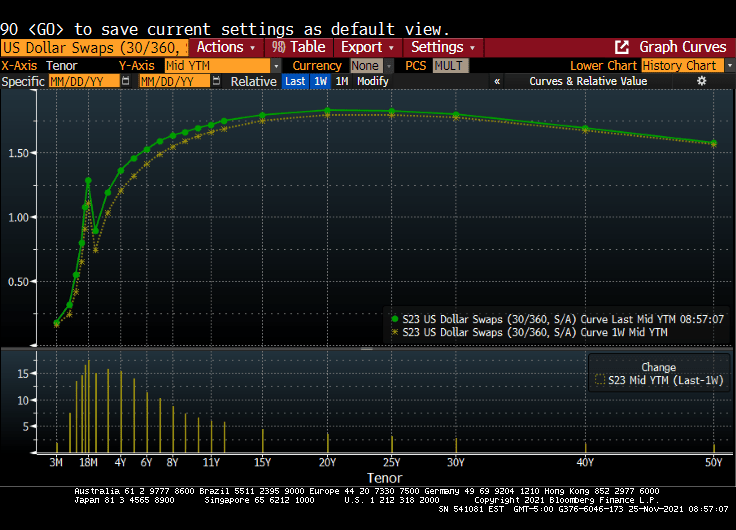

The US Dollar Swaps curve rose from the previous week as well.

Minutes said participants considered elevated inflation as likely transitory, “but judged that inflation pressures could take longer to subside than they had previously assessed”

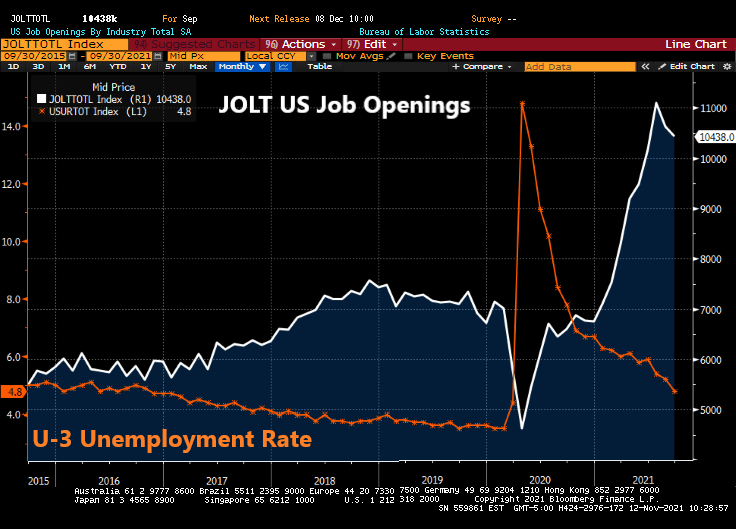

Earlier, front-end and belly sold off after a heavy slate of U.S. economic data including the lowest initial jobless claims tally since 1969

Also during U.S. morning, Fed’s Daly said she would support accelerated tapering of asset purchases, which added to pressure across front-end Treasuries

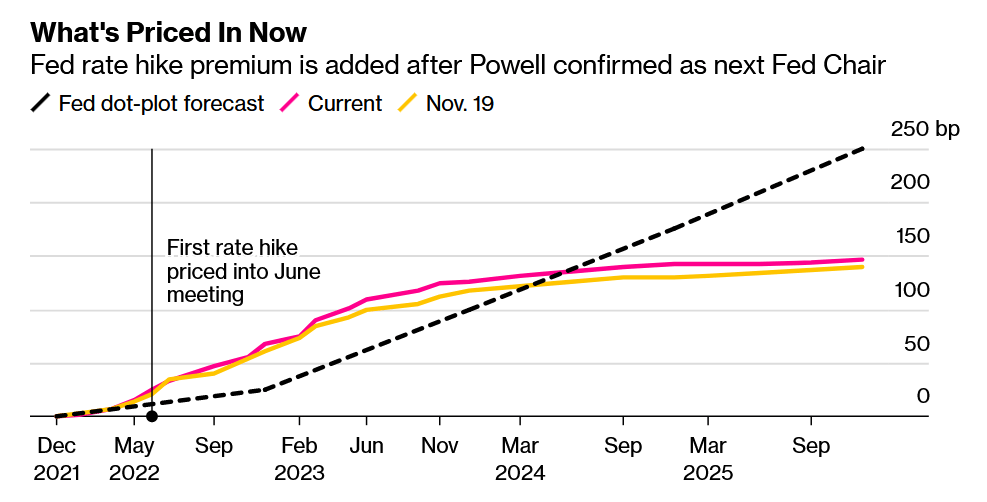

Subsequently, eurodollars traded heavy over the session as rate-hike premium continued to ramp up in 2022 and 2023; overnight index swaps showed 30% chance of a March hike, while around three hikes — or 75bp — were priced in by the end of next year

Wishing you a happy Thanksgiving! In my dreams!

You must be logged in to post a comment.