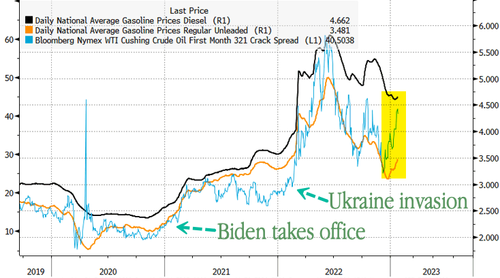

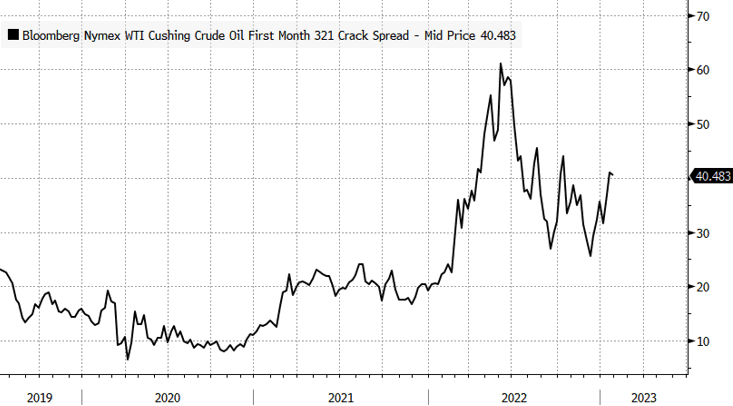

The 3-2-1 crack spread is a great indicator to gauge fuel product tightness. High spreads indicate gasoline, diesel, jet fuel, and other petroleum products are in short supply, while low spreads mean an abundance of supply. Spread direction is also important — if rising, it would mean fuel inventories are declining.

The simple calculation of refining margins is for every three barrels of crude oil the refinery processes — it makes two barrels of gasoline and one barrel of distillates like diesel and jet fuel.

On Tuesday, the crack spread hit a three-month high of $42 a barrel. For some context, the five-year January average is $15.56.

Reuters pointed out that refinery outages exacerbate fuel supply tightness.

A diesel producing unit at PBF Energy’s (PBF.N) Chalmette, Louisiana, refinery was shut following a fire on Saturday. It could be out for at least a month. Exxon Mobil (XOM.N) said Monday it will perform planned maintenance on several units at its Baytown, Texas, petrochemical complex.

The ongoing refinery maintenance season could be much lengthier than usual, with many U.S. Gulf Coast refineries still running below capacity after Winter Storm Elliott knocked out some 1.5 million barrels per day of refining capacity in December. A Suncor refinery in Commerce City, Colorado, has remained offline since the storm.

Also, the number of refinery overhauls is double the amount this spring. Many of these overhauls were postponed due to the pandemic. Some are due to record-high margins driving increased profitability for oil companies.

There are at least 15 oil refineries plan maintenance ranging from two to 11 weeks through May, tallies by Reuters and refining intelligence firm IIR Energy show. By mid-February, U.S. refiners will drop some 1.4 million barrels per day of processing capacity, double the five-year average.

“A lot of plants didn’t want to shut down last year when margins were strong, but they have to get this work done,” said John Auers, refining analyst with Refined Fuels Analytics.

Nine U.S. refineries operated by Marathon Petroleum, Valero Energy, Exxon Mobil, Phillips 66, and BP will shutter some of their fuel-producing units this spring, according to IIR and Reuters sources.

All of the outages and planned overhauls are going to make it difficult for refiners to catch up with demand as inventories are relative to historical levels.

“If we aren’t hearing the alarm bells, it’s because we’re deaf after refining margins reached eye-watering levels in 2022, when the 3-2-1 crack spread briefly surged above $60. But from a historical perspective, current margins are sky-high, as well,” Bloomberg Opinion’s Javier Blas said.

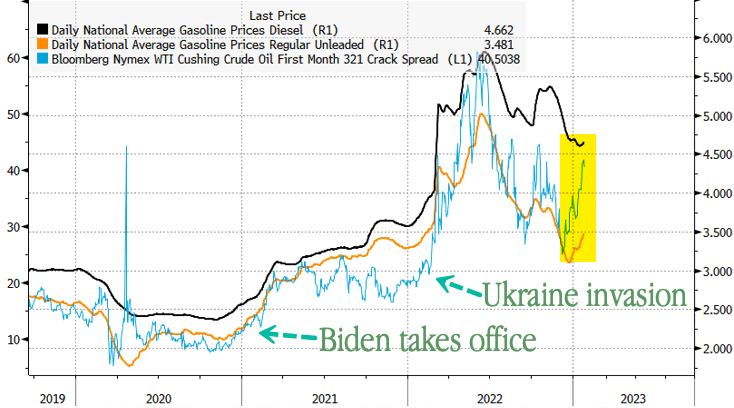

According to AAA data, gasoline and diesel prices at the pump are starting to move higher after months of declines following the rise in the 3:2:1 crack spread.

And the ‘raw materials’ for the refining process are rising rapidly…

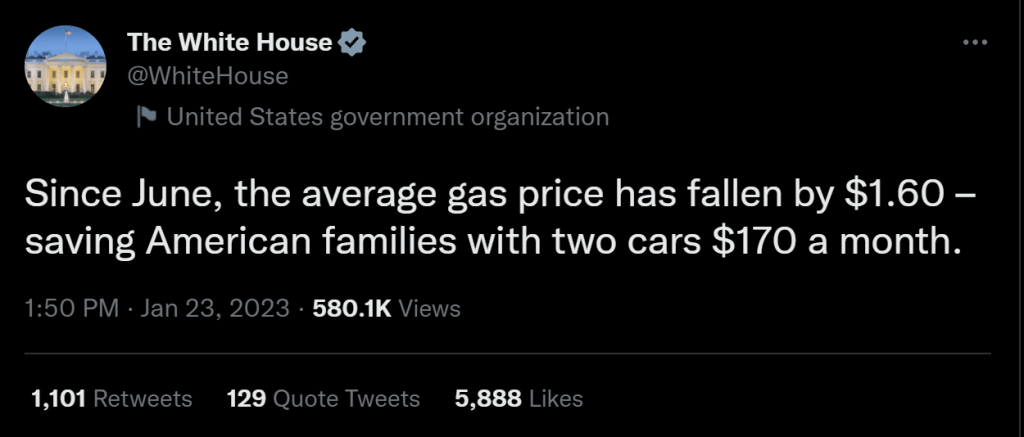

Perhaps the victory lap was a little premature?

Mission Accomplished 2.0?

Not really. US gasoline prices are UP 45% under Biden, diesel prices (the lifeblood of the shipping industry) are UP 77 under Clueless Joe and the Strategic Petroleum Reserve is DOWN -47% under China Joe.

Falling mortgage rates are having a predictible effect on mortgage refinancing applications, but not so much for mortgage purchase applications.

Mortgage applications increased 7.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 20, 2023. This week’s results include an adjustment for the observance of Martin Luther King, Jr. Day.

The Refinance Index increased 3.15 percent from the previous week and was 77 percent lower than the same week one year ago.The unadjusted Purchase Index decreased 1 percent compared with the previous week and was 39 percent lower than the same week one year ago.

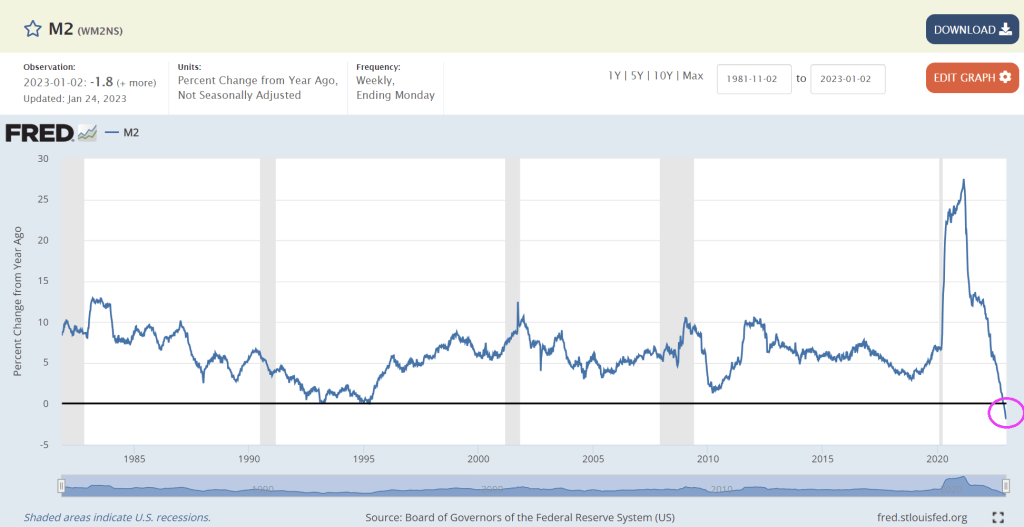

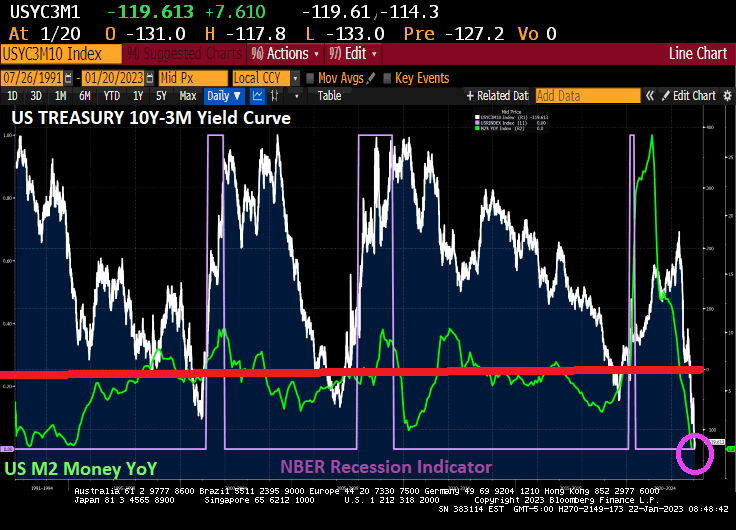

Generally speaking, declining mortgage rates are due to declining 10-year Treasury yields. And 10-year Treasury yields decline as the economy weakens. Of course, M2 Money growth YoY is now 0% as The Fed tightens.

Three regional Fed reports I like to watch are New York’s Empire State Outlook, Philly Fed’s Outlook and Richmond Fed’s outlook. Today, The Richmond Fed released their manufacturing outlook and … it declined to -11.

So the big three are all down (Philly down to -8.9 while NY’s Empire State outlook is down to -32.9.

On the Treasury front, the US 10Y-3M yield curve inverted further (a signal of impending recession) just tanked to -126.462 basis points.

The Conference Board’s Leading Indicator should be called The Bleeding Indicator given that the leading index has declined to 10 straight months. This is happening as The Fed tightens monetary policy to combat inflation.

Leading indicators include economic variables that tend to move before changes in the overall economy. These indicators give a sense of the future state of an economy.

The first headline I saw when I turned on Bloomberg.com was “DOJ Officials Find More Classified Documents at President Biden’s Home.” This is an improvement! So far, the task has been handled by Biden’s private attorneys who don’t have proper security clearance; at least the Justice Department is finally getting involved!

But back to the US yield curve. It is now the most inverted in 30+ years as M2 Money growth stalls. Inverted yield curves have preceded recessions in the past.

But as China reopens and Europe is experiencing a warmer winter than expected (meaning that Europe has sufficient natural gas reserves) and US inflation cooling,

we are seeing market-implied odds of a recession falling in January.

I am still betting on a recession in the second half of 2023.

First, US default risk as measured by credit default swaps remains elevated (primarily because Biden and Democrats refused to cut wasteful spending or reign in non-retirees on Social Security). And NY Fed’s Reverse Repos remain elevated.

And then we have Citi’s economic surprise index for the US at -17 as The Fed slows money growth to 0%.

I wish I knew a place where inflation and insane Federal government spending and policies doesn’t exist.

The Thrill Is Gone from the US housing market as M2 Money growth fells to 0%.

US Existing Home Sales fell -1.5% from November to December (MoM) to 4.02 SAAR units sold. That translates to a depressing -34% decline since December 2021 (YoY).

On the positive side, these numbers are better than expected (-3.4% MoM expected). Still, these numbers are pretty dismal.

Existing home sales MEDIAN PRICE fell to $366.9k as M2 Money growth vanishes. And inventory of existing homes for sale remains lower than pre-Covid levels.

Let’s see what Powell and the Gang (aka, The Federal Reserve Board of Governors) does with interest rates going forward.

Today, the 10-year Treasury yield is up 7.1 basis points, but the real action is in Europe where sovereign yields are up 11.5 bps in France, 9.8 bps in Germany and 18.6 bps in Italy.

Notice that the debt ceiling keeps on climbing once the Kabuki Theater of Democrats and Republicans is over.

The Volatility Cube for the US CDS 1 year signals that it will all be over soon.

So, Yellen and Treasury are threatening us with taking away Social Security and Medicare if we don’t agree with their lavish Pelosi-like spending sprees and debt.

And why exactly is Janet Yellen flying to China? I admit Washington DC has lousy Chinese food, but at least I hope Yellen takes Hunter Biden with her to negotiate the impending US default and debt workout.

December’s housing construction numbers are a mixed bag. On the one hand, US housing starts are down -1.36% from November to December, but down -21,8% since December 2021 (YoY).

The good news? 1-unit (single family detatched) rose 11.26% from November to December (MoM). But 5+ (multifamily) starts are down -18.91% MoM.

But 5+ unit PERMITS are up 7.14%. Perhaps Hunter Biden can now rent an apartment rather than pay his father $50,000 a month in rent for Joe’s Wilmington Delaware house.

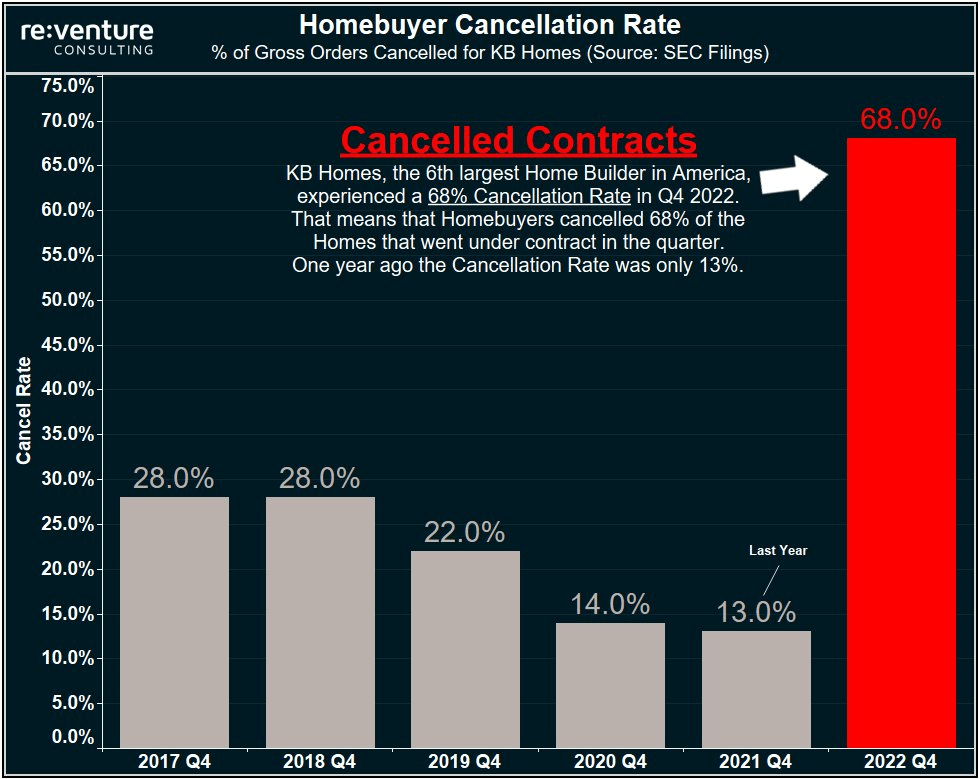

KB Homes experienced a 68% cancellation rate in Q4 2022.

This version of The Scream is one of four made by Edvard Munch, and the only one outside Norway. It is coming up for auction at Sotheby’s in New York.

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.