As US/Russian tensions grow over Ukraine, The Federal Reserve may be forced to postpone or reduce planned rate increases and balance sheet trimming.

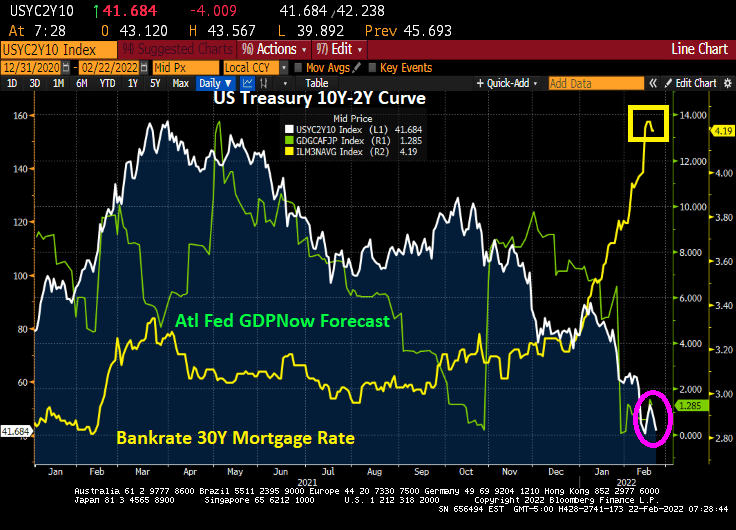

But in addition, we see US GDP slowing to near zero (1.285%) as the US Treasury 10Y-2Y yield curve has flattened to 41.684 BPS. The good news? Bankrate’s 30Y mortgage rate increases have slowed to 4.19%.

On a different note, I noticed the Chicago Bulls logo when turned upside-down looks like a space alien violating a crab.

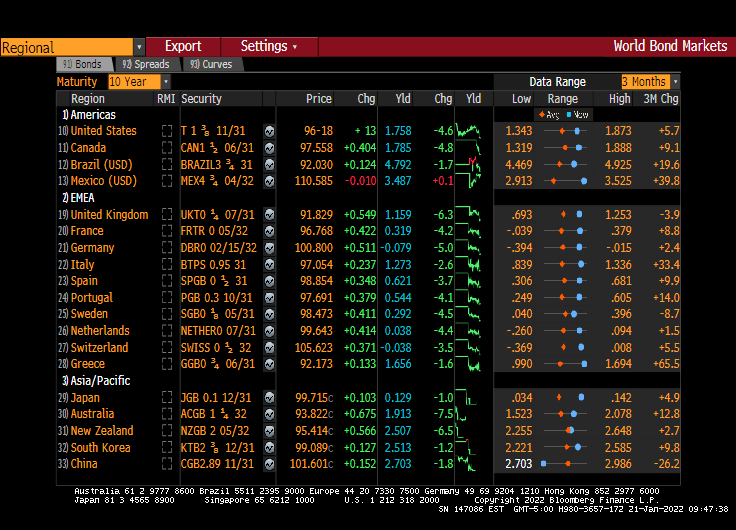

Once upon a time, European PIGS (Portugal, Italy, Greece and Spain) saw incredible spikes in their sovereign yields related to Greek credit default contagion. But the European Central Bank (ECB), World Bank (WB), International Money Fund (IMF) rose to the rescue.

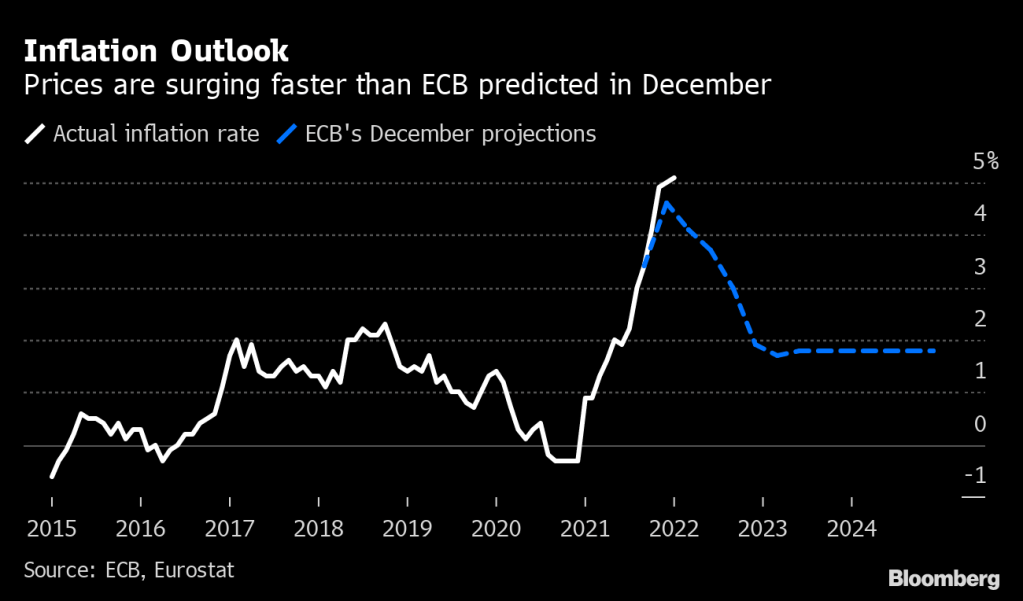

But here we go again! Thanks to rising inflation, the ECB is threatening to remove the massive monetary stimulus. Sound familiar??

Here are the Eurozone 10-year sovereign yields as of this morning. Greece is up a whopping 27.4 basis points, Italy is up 11.7 BPS, Portugal is up 9.3 BPS and Spain is up 9.2 BPS. The core of the Eurozone, France and Germany, are up 4.3 and 3.0 BPS, respectively.

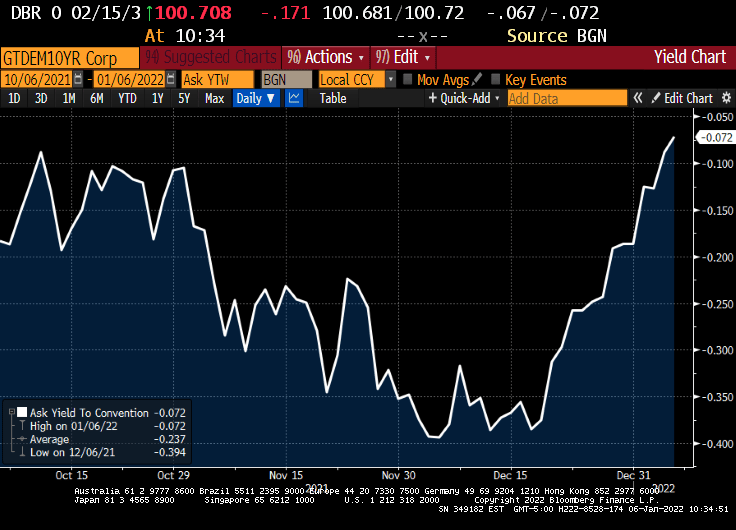

Germany has REAL 10Y Bunds yields of -4.7%.

Like the USA, the Eurozone Taylor Rule is much higher than the ECB’s Main Refinancing rate of 0%..

Here is ECB’s Christine Lagarde saying “What, me worry??”

(Bloomberg) — European Central Bank President Christine Lagarde is no longer ruling out an interest-rate hike this year, a pivot toward the tightening stance of global peers that officials privately see materializing with a shift in policy guidance as soon as next month.

Investors brought forward bets on ECB action as the monetary chief delivered surprisingly hawkish comments citing unexpected record inflation data, contrasting with an earlier statement on Thursday that kept intact its formal view that price increases will ease.

She spoke after policy makers agreed that it’s sensible no longer to exclude a rate move in 2022, and that bond buying could end in the third quarter, according to officials familiar with their thinking who asked not to be identified because such discussions are confidential. An ECB spokesman declined to comment.

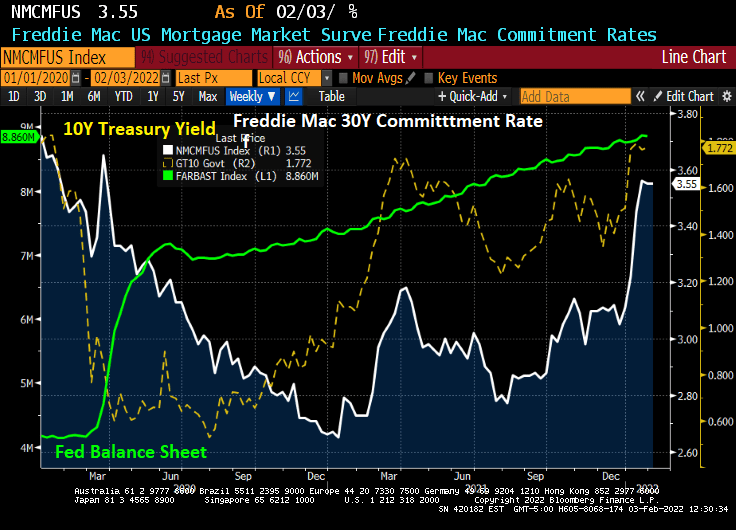

The result of Lagarde’s jaw boning?

US mortgage rates are rising in anticipation of the US following Largarde’s lead. Powell and the Gang continue to lag.

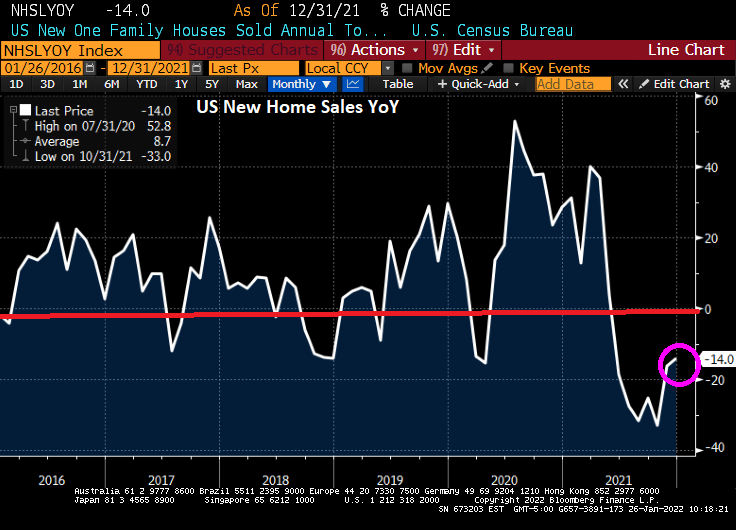

US new home sales spiked in December by 11.9% from November, but were down 14% year-over-year.

But the median price of new home sales (YoY) declined to 3.4%.

The Midwest saw a surge in new home sales (+56%).

The MBA’s mortgage applications index shows declining purchase applications (-1.83%) and declining refinancing applications (-12.60%) as mortgage rates increased from 3.64% to 3.72% for the week of 01/21.

Now, mortgage purchase applications rose for the week of 01/21 if we used non-seasonally adjusted data.

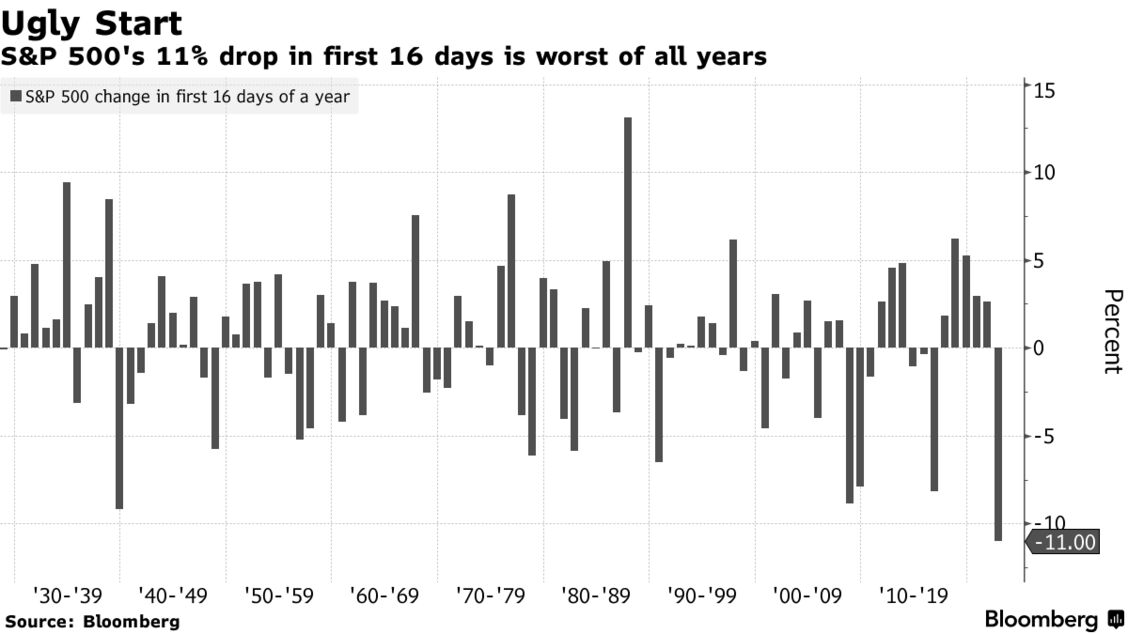

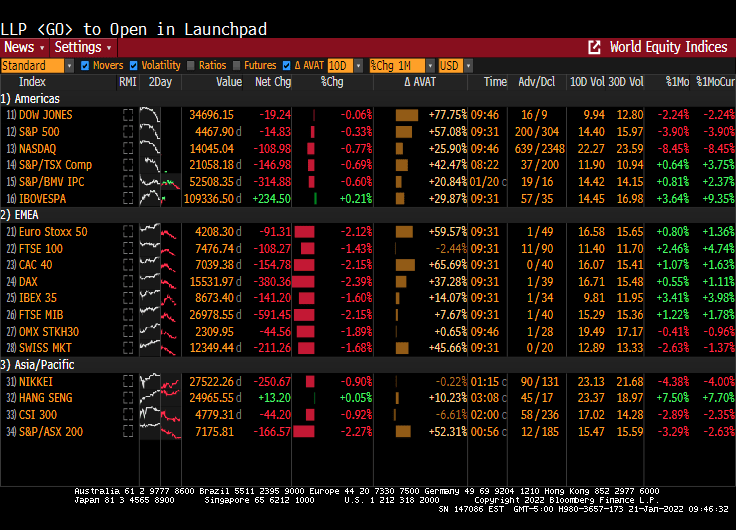

The stock market has never started a year falling as quickly as it is now.

The S&P 500 has dropped 11% — heading into correction territory — in the first 16 trading days of 2022 in its worst-ever start to a year, according to Bloomberg data that goes back over nine decades.

The downturn comes as traders brace for the Federal Reserve to tighten monetary policy and a surge in U.S. Treasury yields weighs on the outlook for stocks. A host of technical signals also suggest that more volatility may be coming up ahead.

“The Fed pulled the punchbowl, liquidity has evaporated, and the S&P and NDX broke below their 200dma for the first time since the Covid outbreak,” said Rich Ross, technical strategist at Evercore ISI.

A bear market down to the 3,800 level is likely for the S&P 500, Ross said, given “the dramatic erosion of the technical backdrop, in conjunction with the highest inflation, tightest policy, and most uncertain political and geopolitical condition in years” — not to mention its historic rally since 2020.

The Shiller CAPE ratio is extremely high …. not surprising how much air The Fed pumped into the market tires.

Is this the bubble burst many were expecting once The Federal Reserve starting raising rates?

Well, if today’s market opening is an indication, the answer is yes. The NASDAQ Composite Index is down 1.36% and West Texas Intermediate Crude Oil futures prices are down 2%.

The S&P 500 index is down over 10% since January 3rd.

Drawdown is taking place.

But if you think the US equities are deflating, look at European equities. The Euro Stoxx 50 index is down 4.04%.

Let’s see how The Federal Reserve is going to compete with other central banks when 19 European nations have negative 2-year sovereign yields. Call them the “Nervous 19.” Note that France has the lowest 2Y yield of the big 3 (France -0.664%, Germany -0.593% and Italy -0.092%).

True, The Fed’s reaction to COVID shutdowns was more extreme than the ECB’s reaction.

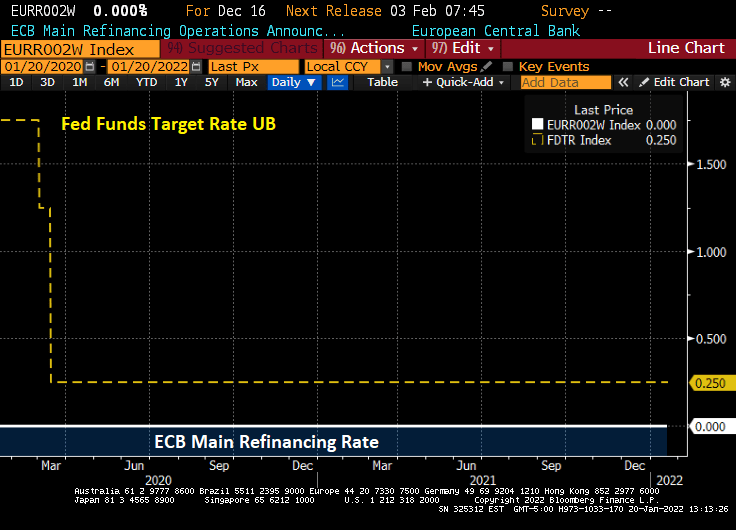

The ECB’s main refinancing rate is 0% and The Fed’s target rate is 0.25%.

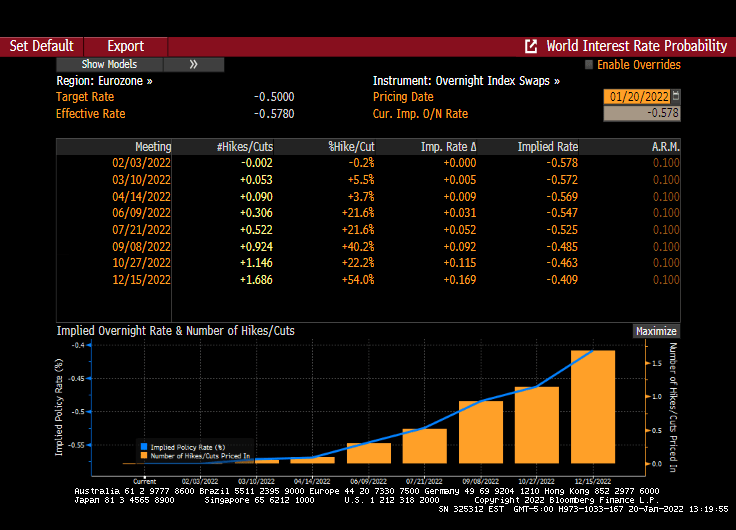

Unlike the US with its 4 expected rate increases, the Eurozone is pricing in only 1 rate increase for 2022 … in October.

The ECB’s monetary policy is as stiff as French President Emmanuel Macron.

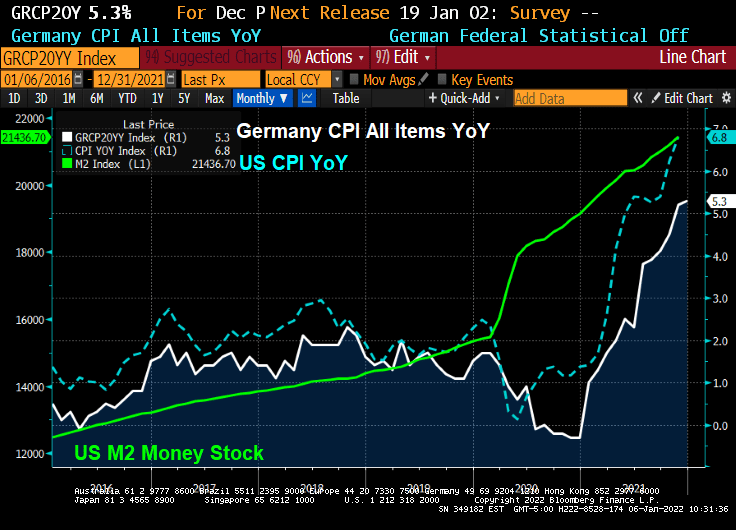

The world has become a wild and wacky place since COVID was unleashed on an unsuspecting population. Since the massive spending spree by The Federal government in the USA coupled with extraordinary monetary stimulus from The Federal Reserve, US inflation has shot up to 6.8% YoY.

German is also having an inflation moment. With their CPI YoY running at 5.3%, faster than the anticipated 5.1%.

At least the German 10-year sovereign yield is ALMOST back to 0%.

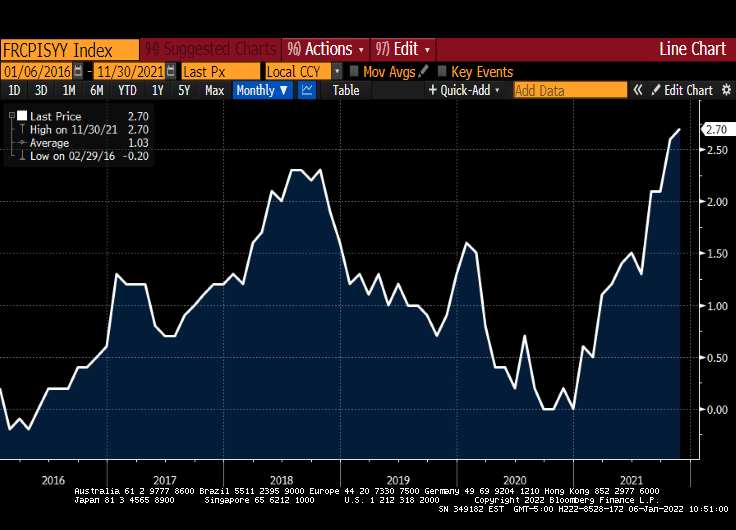

France, on the other hand, is seeing inflation rising to 2.70% YoY.

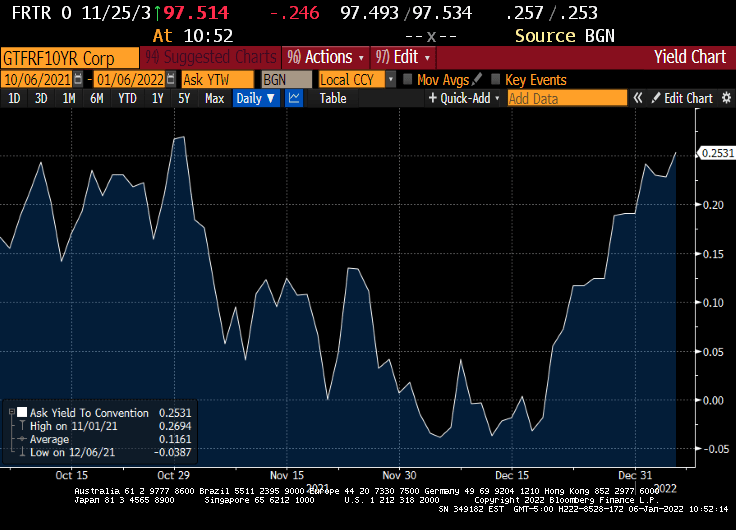

While the French 10Y sovereign yield rose to 0.2531%.

France’s Macron certainly likes to have his photo taken as if he wants to go 10 rounds with UK’s Tyson Fury.

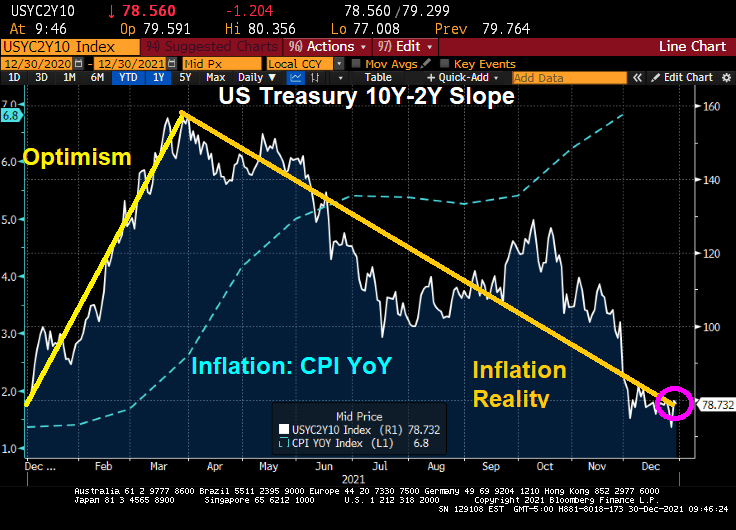

It has been almost a year since Joe Biden has been President of the United States and a Democrat majority took control of The House and Senate. And what has happened to the US Treasury yield curve slope over the past year?

The yield curve is back where it started. There was the “honeymoon effect” where the curve slope rose. After all, Biden was Obama’s Vice President for 8 years and The Democrats has promised so much in the 2020 election. But by early April, the reality of the massive Federal spending (combined with Fed Stimulypto) began showing what was feared: inflation (blue line) started to grow at a rapid rate of speed. With inflation now at 6.8% YoY,

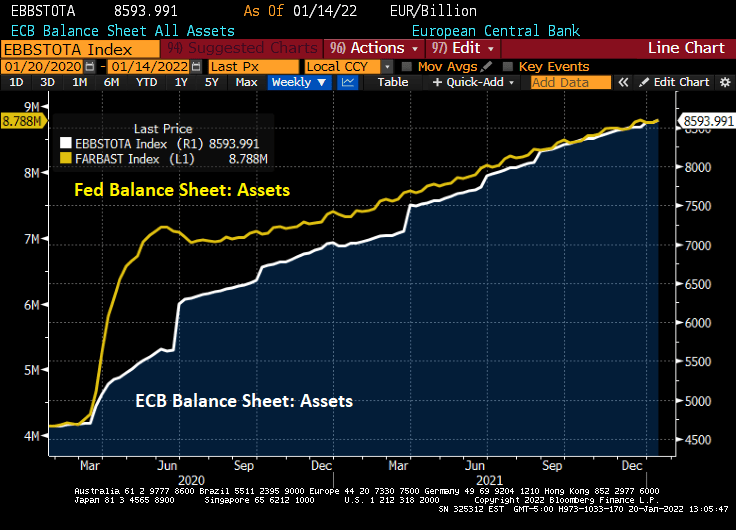

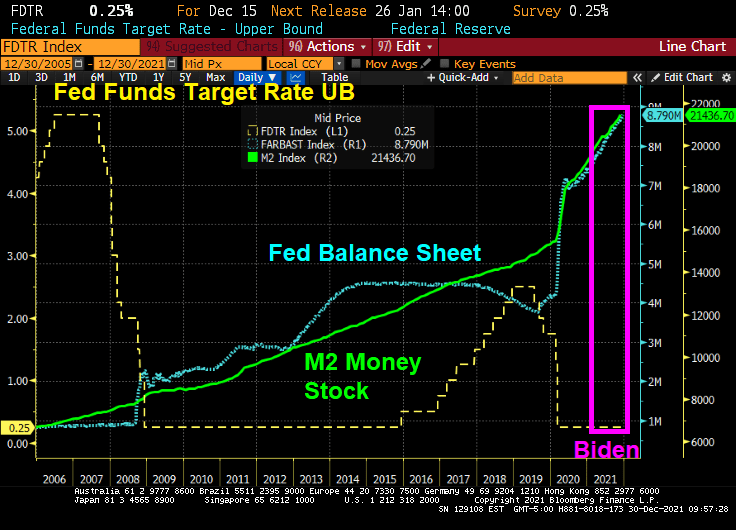

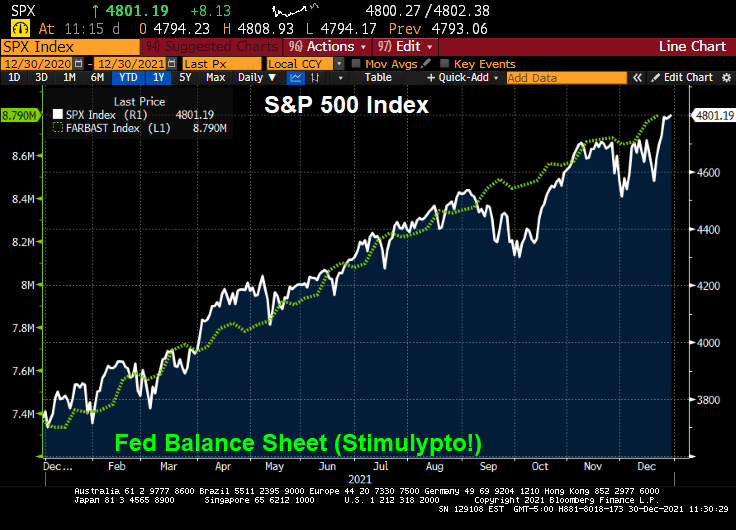

In fairness to Biden, The Federal Reserve has been overstimulating the economy since The Federal Reserve since Ben Bernanke and the Fed Open Market Committee (FOMC) dropped the hammer on The Fed Funds Target Rate once the rate hit 5.25% in September 2007. They kept cutting it reached 25 basis points (or 0.25%) in December 2008. In August 2008, Bernanke and Company began their “Quantitative Easing” or asset purchasing programs. Between The Fed’s Target Rate and QE, The Fed has continued to overstimulate markets ever since. Under Biden, The Fed Funds Target Rate remains at 0.25% and The Fed’s Balance sheet has grown to $8.79 Trillion (bigger than the entire economies of Japan and Germany put together!).

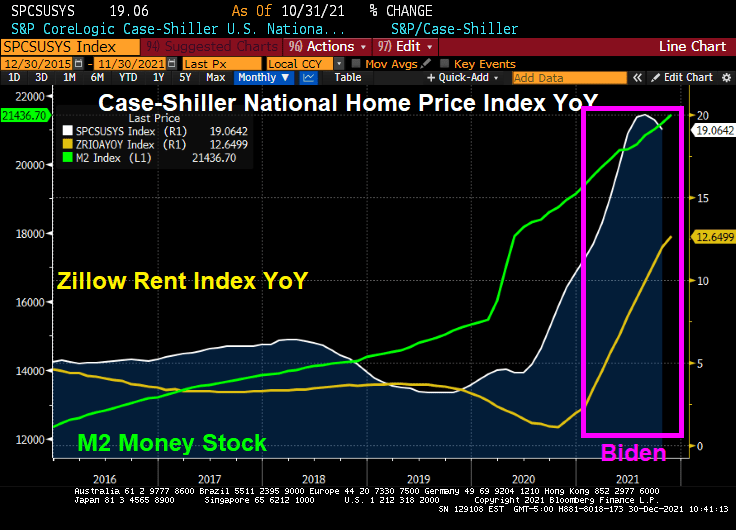

How about housing? Home prices are growing at 19% YoY while rents are growing at 12.65% YoY.

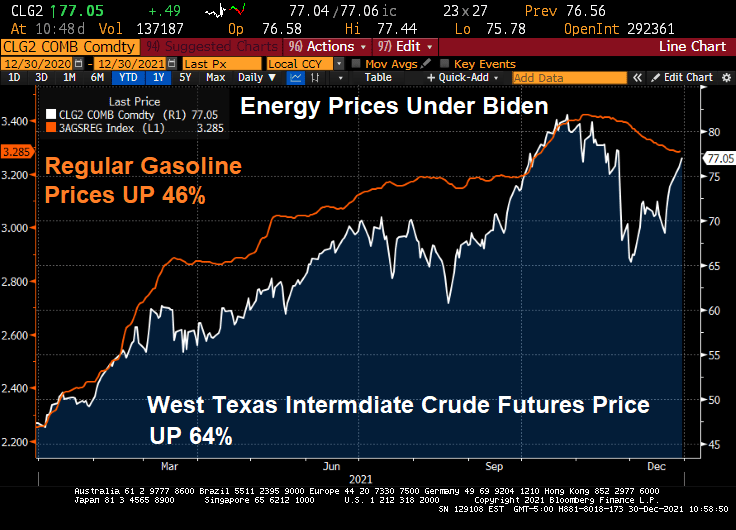

Energy prices have risen dramatically under Biden. Gasoline is up 46% despite a slight reprieve recently. WTI crude prices are up 64%.

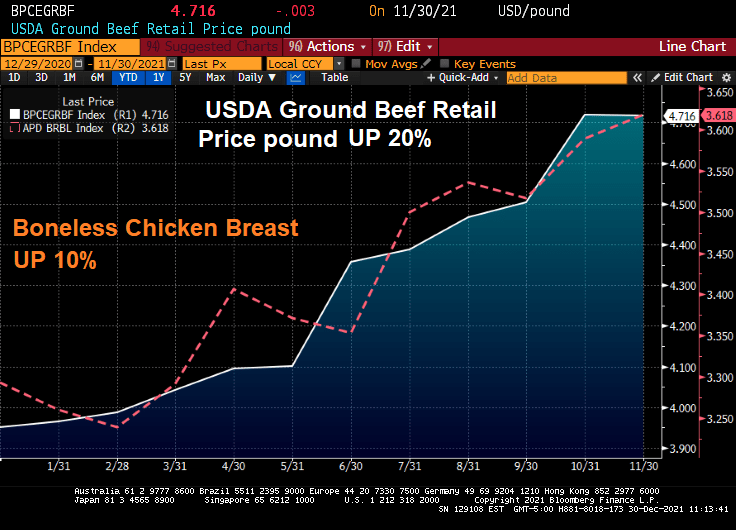

How about food? Beef prices are up 20% and chicken prices are up 10%.

On a positive note, the S&P 500 index has soared … thanks has soared during Biden’s term thanks to Fed stimulus and Federal spending on COVID.

The Build Back Better Act if passed (in its entirety or on a piecemeal basis) will lead to even MORE inflation.

Perhaps Biden’s spokesperson Jen Psaki can recreate the Biden Administration as a lovable, hilarious family like the comic strip Gasoline Alley with old Joe Biden as Skeezix. And insider-trading star, House Speaker Nancy Pelosi as the family matriarch.

You must be logged in to post a comment.