President Biden nominated Jerome Powell for a second term as Fed Chair and nominated Lael Brainard as Deputy Chair to replace Richard Clarida. The US House of Overlords (aka, the US Senate) will hold hearings on the nominees (with Elizabeth Warren opposing Powell and supporting Brainard’s nomination).

Treasury yields jumped and U.S. index futures signaled a continued selloff in technology shares as traders pruned bets for a dovish-for-longer Federal Reserve after the renomination of Jerome Powell as its chair.

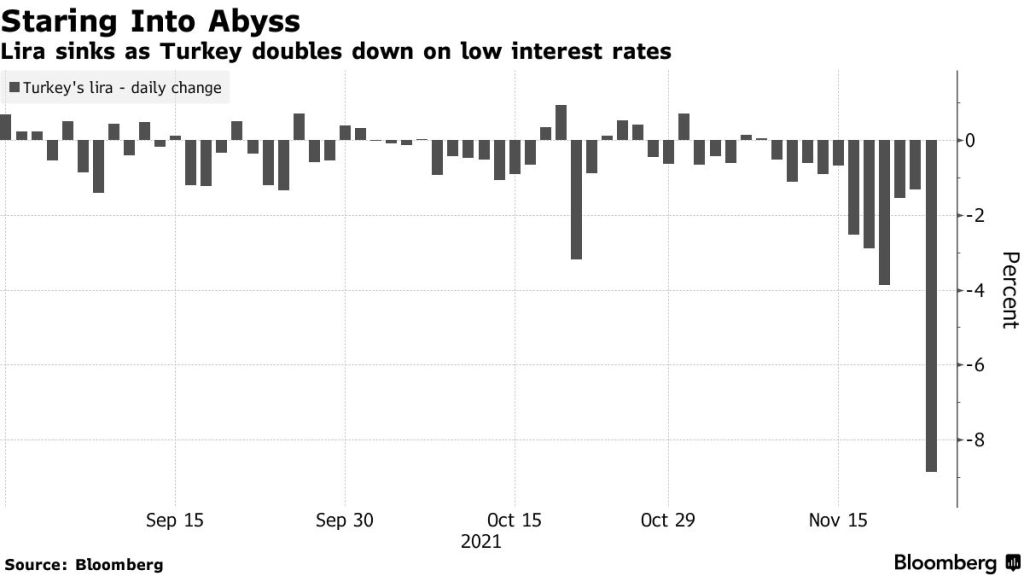

Contracts on the Nasdaq 100 Index fell 0.3% after Monday’s last-hour selloff in technology stocks. The subgroup was the worst performer in Europe Tuesday, sending the region’s benchmark to a three-week low. A currency crisis deepened in Turkey, with the lira weakening past 13 per U.S. dollar. Zoom Video Communications Inc. lost 9% in premarket trading on slowing growth.

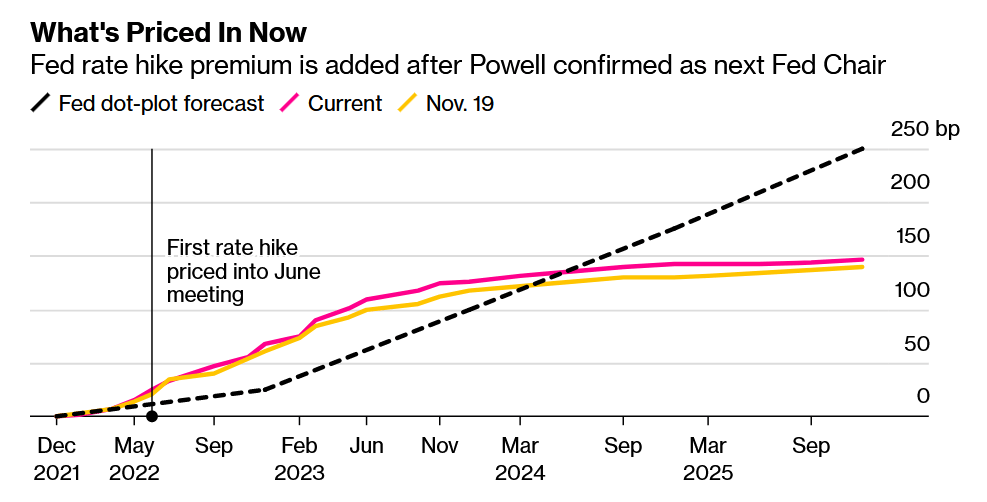

Investors are reducing expectations for a deeper dovish stance by the Fed after Powell was selected for a second term. The chair himself sought to strike a balance in his policy approach saying the central bank would use tools at its disposal to support the economy as well as to prevent inflation from becoming entrenched.

Fed rate hike premium is added after Powell confirmed as next Fed Chair:

Change in Fed’s interest-rate target implied by overnight index swaps and eurodollar futures.

Fed Bank of Atlanta President Raphael Bostic said Monday the U.S. central bank may need to speed up the removal of monetary stimulus and allow for an earlier-than-planned increase in interest rates.

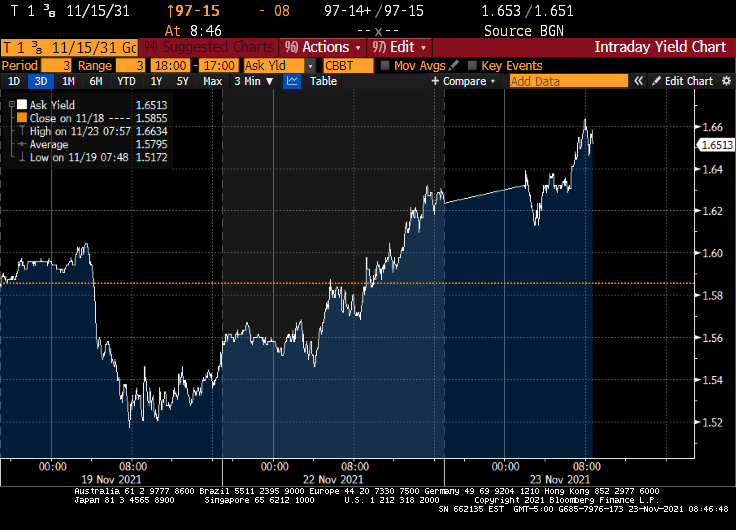

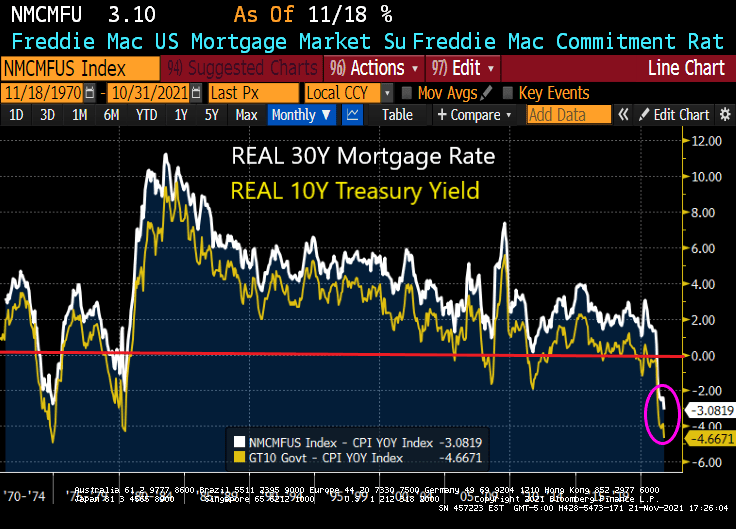

Translation: Markets are pricing in MORE hawkish Powell over uber-dove Brainard. The 10-year Treasury yield has risen from 1.52% to 1.65%

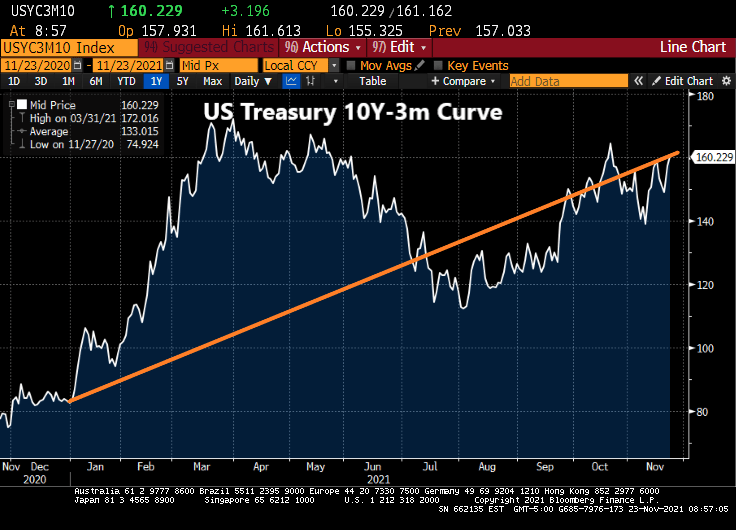

And the 10Y-3M Treasury curve has risen from 83 basis points at the beginning of 2021 to 160 basis points today. I will this the Biden Inflation Effect (BIE).

Let’s see if Powell & Company deliver on removing the excessive stimulus from the market, particularly with midterm elections approaching.

You must be logged in to post a comment.