The first headline I saw when I turned on Bloomberg.com was “DOJ Officials Find More Classified Documents at President Biden’s Home.” This is an improvement! So far, the task has been handled by Biden’s private attorneys who don’t have proper security clearance; at least the Justice Department is finally getting involved!

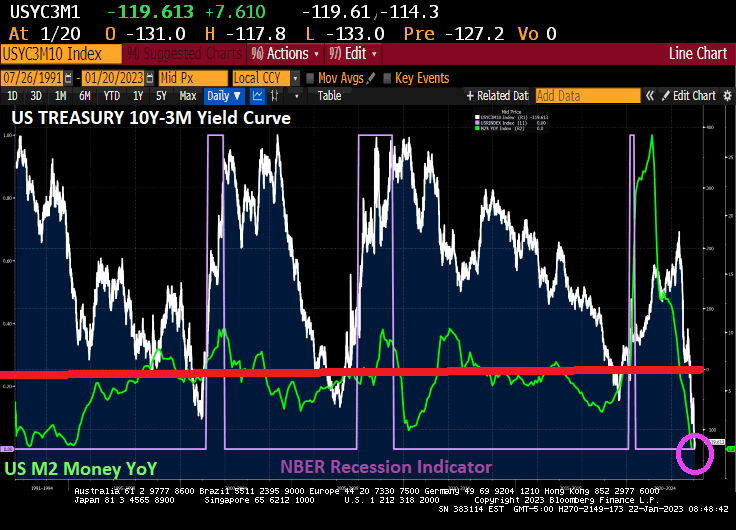

But back to the US yield curve. It is now the most inverted in 30+ years as M2 Money growth stalls. Inverted yield curves have preceded recessions in the past.

But as China reopens and Europe is experiencing a warmer winter than expected (meaning that Europe has sufficient natural gas reserves) and US inflation cooling,

we are seeing market-implied odds of a recession falling in January.

I am still betting on a recession in the second half of 2023.

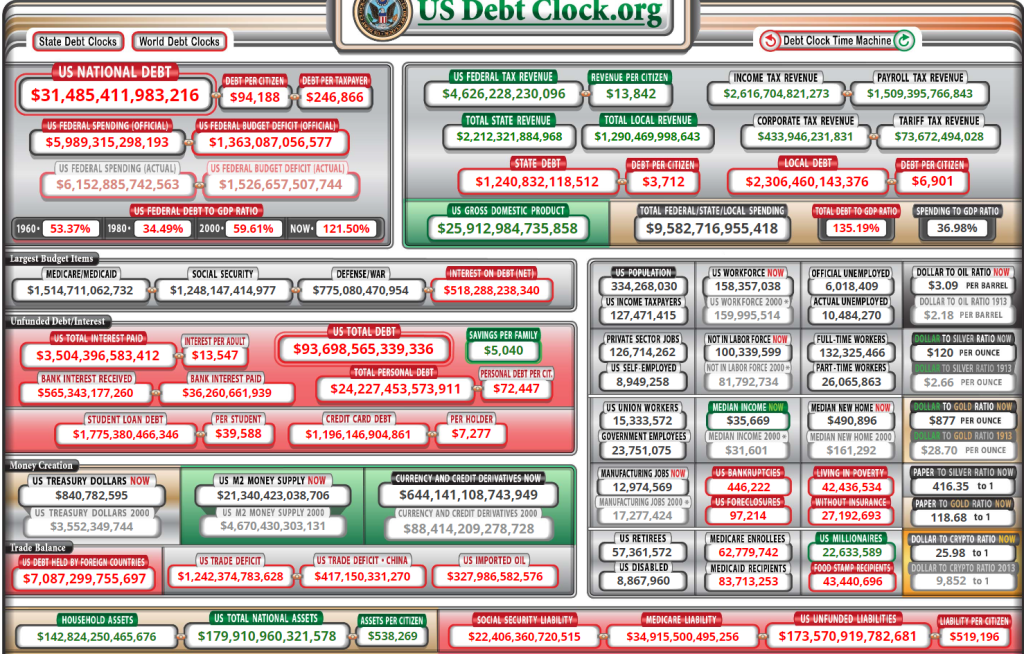

Newly-minted US House Speaker Kevin McCarthy faces a daunting task: trying to avoid a US debt default. As I have discussed many times before, nothing has been the same since the US housing bubble and near-collapse of the banking system that produced an expensive bailout of seemingly all financial institutions. After 2008, Federal spending has gone out of control. The budgetary hawks (or pigeons) in the US House of Representatives (with Pelosi, Boehner, Ryan then Pelosi again) went on Federal spending sprees of epic proportions.

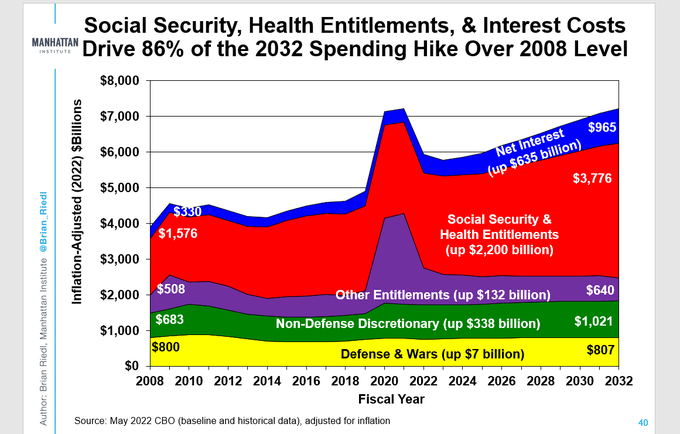

The Manhattan Institute has a nice chart showing the explosion in the Federal budget since 2008. Of particular note, interest payments on the Federal debt has increased by a staggering 192%. On the non-interest spending front, Social Security and Health Entitlements have increased by 140% while Nondefense Discretionary Spending has increased 76%.

The massive increase in Federal debt interest is due to both increased Federal spending and rising interest rates thanks to The Federal Reserve raising rates to fight inflation.

But what will McCarthy and House Republicans recommend cuts in? Tighter restrictions on who qualifies for Social Security and particularly Social Security Disability payments?

The odd factoid is that Defense and Wars budget is up less than 1% from 2008 to 2032. So, Ukraine military aid is coming from somewhere, but not from the Defense budget. Is Ukraine another entitlement program?

Rest assured that after debate, the House will pass a budget and, provided that virtually nothing was cut, the Senate will gleefully agree to more spending and “Top Secret Documents” Biden will sign it.

After he parks his gorgeous Corvette Sting Ray, that is.

Its that time again when Congress does its Kabuki Theater drama about raising the US debt limit. Of course, everyone in Congress and the Biden Administration want to spend trillions of dollars so they will hike the debt limit.

With the US government facing the danger of a payments default later this year, Congress has a variety of paths to avert economic disaster and boost the debt ceiling.

All of them would likely involve going right up to the market-rattling brink, according to current and former lawmakers and aides.

The timeline kicks off within weeks, when Treasury Secretary Janet Yellen is expected to advise that the government will deploy extraordinary accounting measures to avoid running out of cash. Those steps are forecast to be exhausted after July.

Republicans now in control of the House are demanding deep spending cuts as the price for an increase in the ceiling, while President Joe Biden and congressional Democrats reject such an outcome.

Nothing has been the same since the financial crisis of 2008 and the ascension of all-time big spender Nancy Pelosi as House Speaker. Budget deficits have never been the same. The last budget surplus was under House Speaker Newt Gingrich. But since the financial crisis of 2008, Federal spending seems to have increased its trajectory.

Note that mandatory spending (Medicare, Social Security, etc) is growing like a wild fire while discretionary spending is seemingly flat. So, it mandatory spending that Congress will pretend to cut.

Yes, it is Medicare for our aging population that has blown out of control.

Then we have defense spending. The Ukraine spending should come from this pot, but forces decisions to make between Ukraine and taking care of our Navy (to compete with the growing Chinese navy).

Of course, as The Fed fights inflation, we are seeing the COST of Federal debt soaring since Covid.

Yes, Congress NEEDS to cut back the spending, particularly on Social Security and Medicare (not to mention Ukraine spending), but it is all Kabuki theater. Queue the screams of “Republicans will take away …”.

I wish everyone in Congress were like Kentucky U.S. Senator Rand Paul, not the other spendaholic Kentucky Senator.

As we are painfully aware, inflation is still high at 7.1% Year-over-year (YoY). To cope with inflation, consumers have been gutting their savings and increasing their use of credit. In November, consumer credit increased 7.9% YoY while personal savings fell -64.8% YoY.

The good news? Inflation month-over-month is expected to be 0% tomorrow.

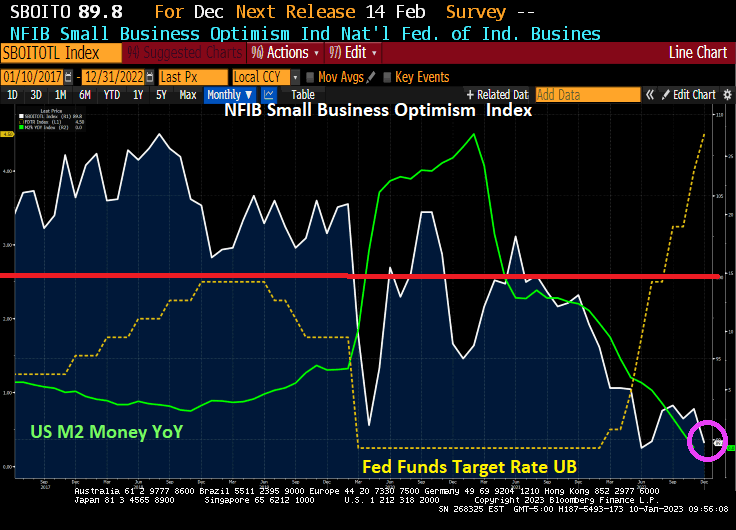

The NFIB Small Business Optimism Index is plunging and just fell below 90. The index was above 100 before the Wuhan virus outbreak in 2020, but has only been at 100 or above for only two months under Biden. And the trend is definitely looking bleak as The Federal Reserve fights inflation with M2 Money growth having collapsed to 0% YoY growth.

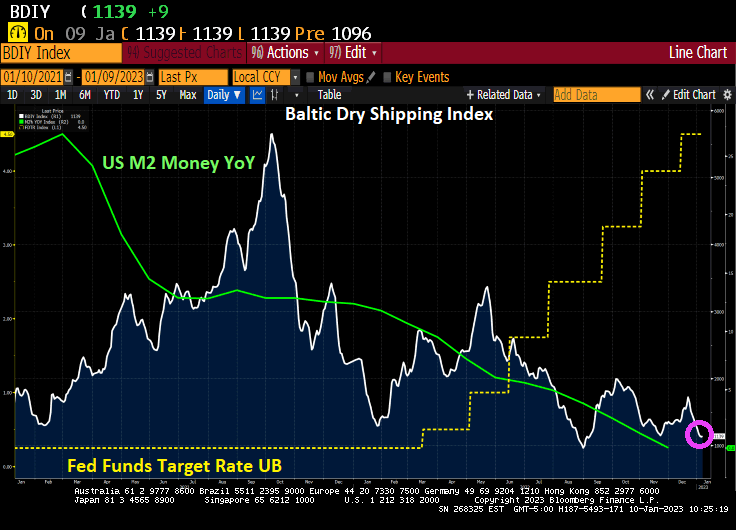

And the Baltic Dry shipping index is falling with M2 Money growth YoY.

I wonder what Fed Chair Jerome Powell is thinking?

And with it, ISM Manufacturing Report for December is showing weakness. New orders (orange line) is down to 45.2 (below 50 is contraction) and the prices paid is down to 39.4 (white line). All this is happening as The Fed raises its target rate (yellow line) and removes monetary stimulus (green line).

This gives us “The Devil’s Tower” looking economic spike after massive Covid-related monetary stimulus and Federal government repeated stimulus.

Speaking of Already Gone, look at the US Treasury 10Y-2Y yield curve with slowing M2 Money growth. Yield curve inversion is more about vanishing M2 Money growth than it is a forecast of recession.

Mortgage applications generally nosedive in the last two weeks of the year (seasonality effect), but Federal Reserce monetary tightening to fight inflation is making the last two weeks worse than usual.

Mortgage applications decreased 13.2 percent from two weeks earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 30, 2022. The results include adjustments to account for the holidays. It marked the lowest mortgage applications since 1996.

The Market Composite Index, a measure of mortgage loan application volume, decreased 13.2 percent on a seasonally adjusted basis from two weeks earlier. On an unadjusted basis, the Index decreased 39.4 percent compared with the two weeks ago. The holiday adjusted Refinance Index decreased 16.3 percent from the two weeks ago (2WoW) and was 87 percent lower than the same week one year ago (YoY). The seasonally adjusted Purchase Index decreased 12.2 percent from two weeks earlier. The unadjusted Purchase Index decreased 38.5 percent compared with the two weeks ago and was 42 percent lower than the same week one year ago.

Notice that purchase applications are declining with slowing M2 Money growth showing the impact of The Fed trying to remove the punchbowl.

The week-over-week (or WoW) numbers are pretty bad.

2022 is one of the record books and not in a Tiger Woods way. Call it a year of pain.

First, the US enacted policies that drove up energy prices (goin’ green) that reverberated through the entire economy in the form of higher prices. Second, The Federal Reserve, in attempt to combat runaway inflation, started removing the excessive monetary stimulus that had been around since Fed Chair Bernanke initiated QE, the seemingly unlimited purchase of Treasury and Agency MBS securities. Janet Yellen continued the massive asset purchases and zero interest rate policies or ZIRP. Now that inflation has struck the American middle class hard, we are seeing Fed Chair Powell doing what Bernanke and Yellen wouldn’t do — remove the monetary punchbowl.

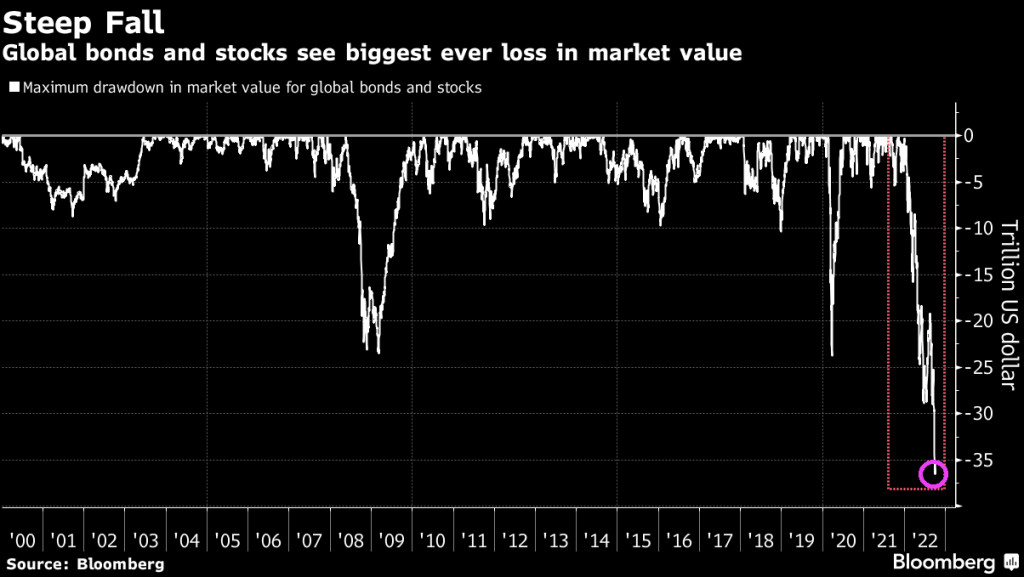

Using Robert Shiller’s on line data, US stocks and bonds have had an awful year, the worst combined year since 1871.

US equity returns have been demolished under the NEW dual mandate (goin’ green = rising prices = Fed tightening).

Let’s see how two of the most famous investment gurus did in 2022, Warren Buffet and Cathie Wood. Buffet’s Bershire Hathaway Class A equity was UP 4% in 2022, while Cathie Wood’s ARK Innovation ETF collapsed by -67% in 2022.

Here is the clinker. The US economy (as well as the global economy) seem dependent on “cheap money” from Central Banks like The Federal Reserve. So the question is … will The Fed pivot? Fed talking heads are saying no, but Fed Funds investors are saying yes to a pivot after June 2023.

Ulysses S Grant was the President the last time the combined stock and bond market was this bad.

More tech tantrums. China’s Covid surge. And above all, no central banks riding to the rescue if things go wrong. Reeling from a record $18 trillion wipeout, global stocks must surmount all these hurdles and more if they are to escape a second straight year in the red.

With a drop of more than 20% in 2022, the MSCI All-Country World Index is on track for its worst performance since the 2008 crisis, as jumbo interest rate hikes by the Federal Reserve more than doubled 10-year Treasury yields — the rate underpinning global capital costs.

And in the US, we have the S&P 500 index being pulverized by Fed rate hikes to in their attempt to slow inflation.

And in the US, mortgage-backed securities and Treasury securities are also getting pulverized by inflation and Fed rate tightening.

We are now left with the leftovers like high inflation.

As a diabetic, eggs are a perfect food. Unfortunately for me and other diabetics, the price of eggs has soared by a whopping 79% since February 28, 2022.

Of course, this year’s deadly Avian flu has been reducing poultry flocks. Also, fertilizer prices have soared as well. Also, soaring inflation has resulted in an aggressive Federal Reserve hiking their target rates.

You must be logged in to post a comment.