Yes, it is the much anticipated Fed Week! The Fed Open Market Committee (FOMC) will announce it decision (probably the first rate hike under Biden of 25 basis points).

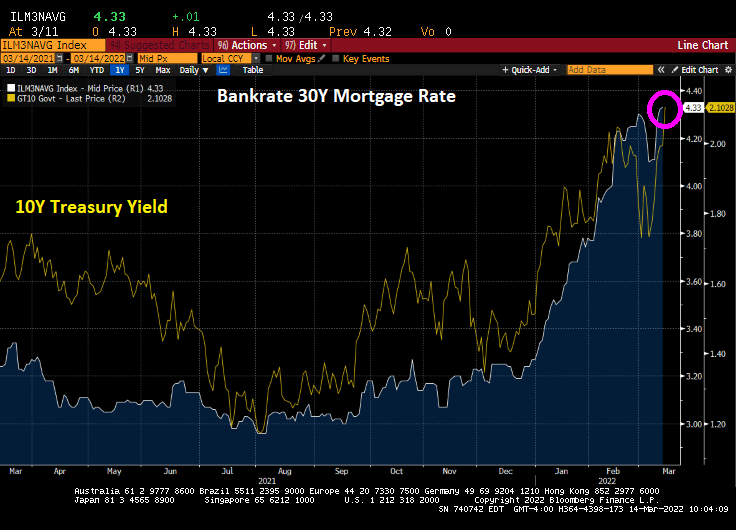

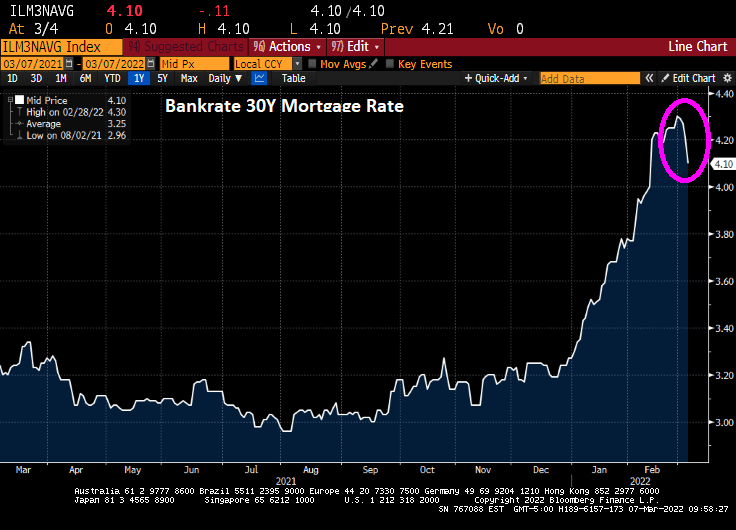

This morning, the 10-year Treasury yield rose by 11.1 basis points and the Bankrate 30Y mortgage rate rose to 4.33%.

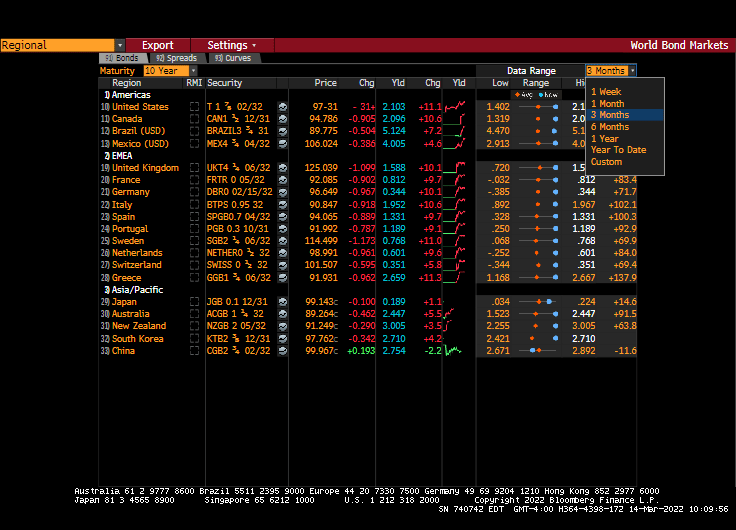

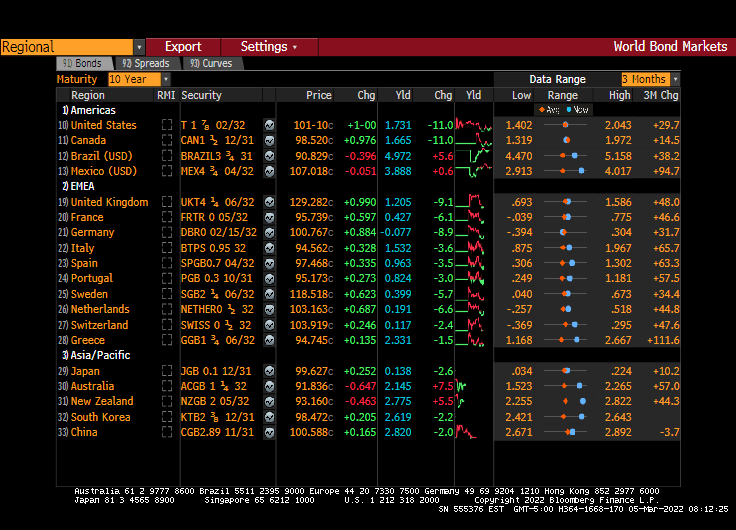

Actually, sovereign yields are up around 10 basis points in the US, Canada, and across the pond.

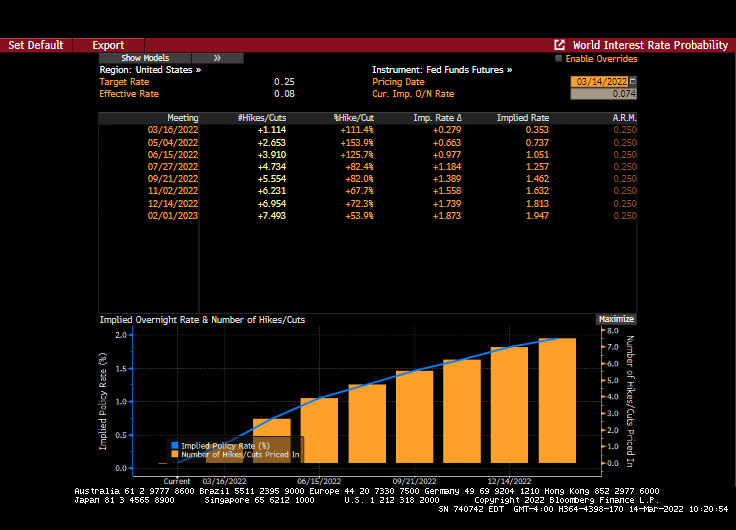

Fed Funds Futures are pointing to 7 rate hikes over the next year with 1.114 rate hikes on Wednesday. That means The FOMC may raise rates MORE than the 25 basis points expected my many (including me).

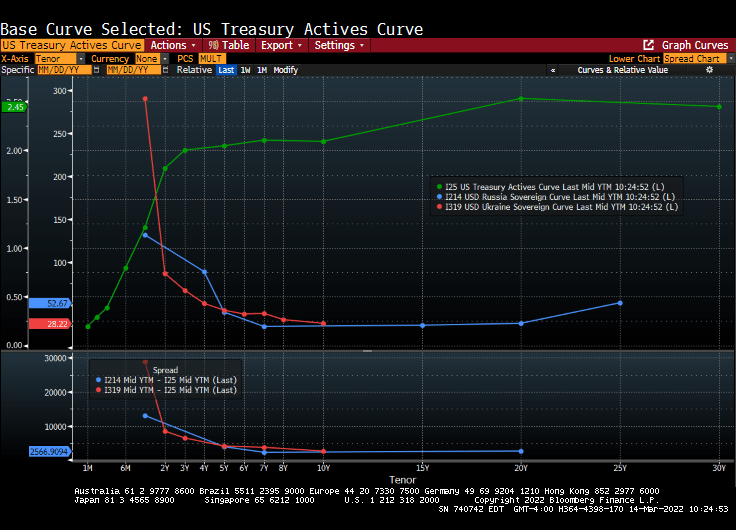

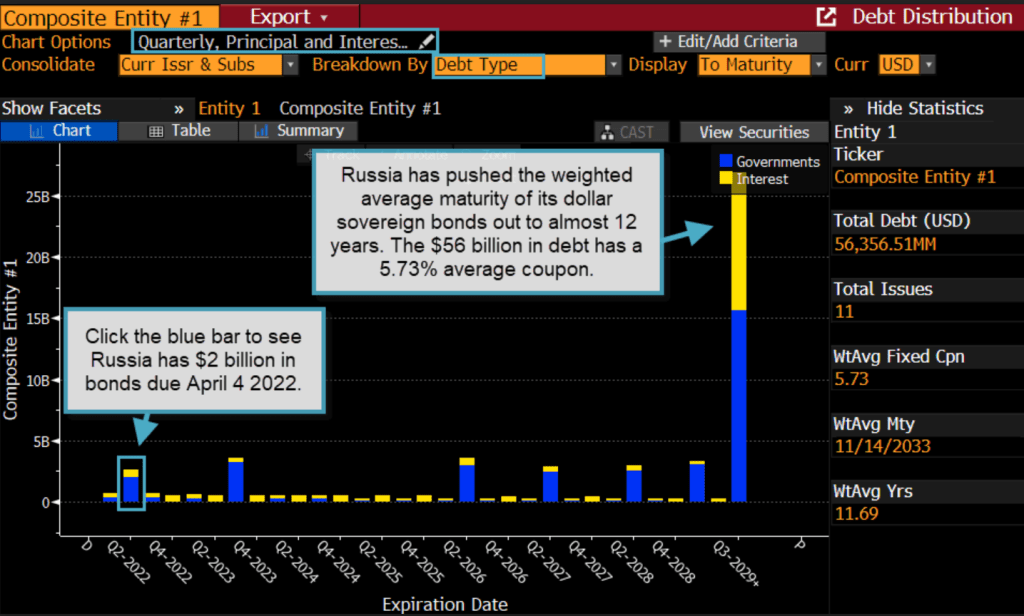

The US Treasury actives curve remains steeply upward sloping while both the Russian and Ukraine sovereign curves are steeply inverted and crashing.

Russia has pushed the weighted average maturity of its dollar sovereign bonds out to almost 12 years.

The most hilarious headline of the day is a Bloomberg opinion piece: “Fighting Inflation May Require the Fed to Be Brutal: Clive Crook” How about the Biden Administration relaxing oil drilling and pipeline restraints? Otherwise, brutal translates into causing a recession. Great suggestion, Clive! … NOT!

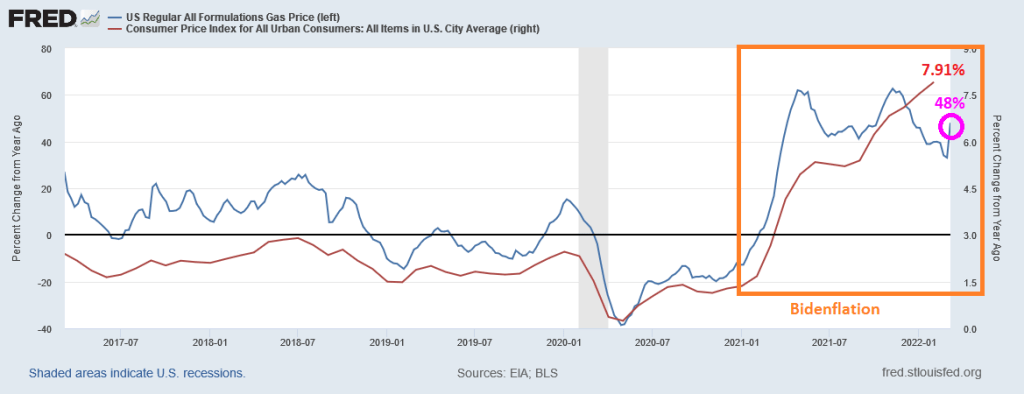

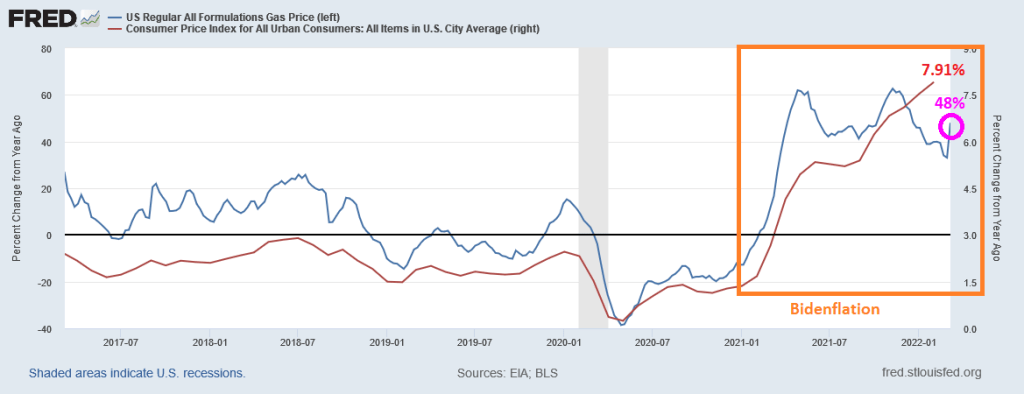

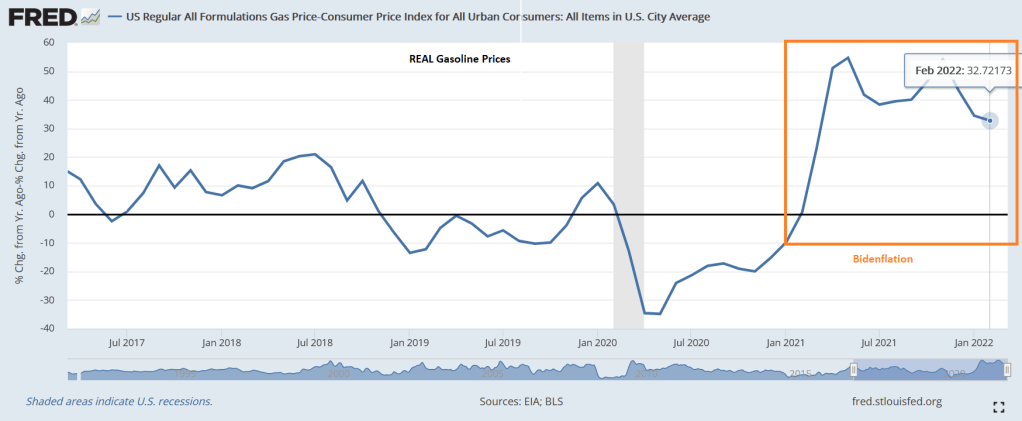

Well, so much for rising gasoline prices being the fault of Vlad “The Ukrainian Impaler” Putin and Russia invading Ukraine. In fact, gasoline prices were rising at a 62% YoY pace in April 2021, well before Russia’s invasion of Ukraine.

REAL gasoline prices (nominal gasoline prices less inflation) are up 32.72% YoY in February.

Press secretary Jen Psaki can take the opportunity to proclaim that REAL gasoline prices have actually declined in February.

I keep waiting for the Biden Administration and Congress to launch price controls and supply rationing rather than simply allow the Keystone Pipeline to be built and allow drilling on Federal lands.

US Speaker of the House and American Oligarch Nancy Pelosi together with Senate Majority Oligarch Charles Schumer passed yet another massive spending bill that seemingly benefited them and not the American middle class.

This legislation would provide $774.4 million for the Members Representational Allowance, known as the MRA, which funds the House office budgets for lawmakers, including staffer salaries. This $134.4 million, or 21 percent, boost over the previous fiscal year marks the largest increase in the MRA appropriation since it was authorized in 1996, according to a bill summary by the House Appropriations Committee. For paid interns in member and leadership offices, the House would get $18.2 million.

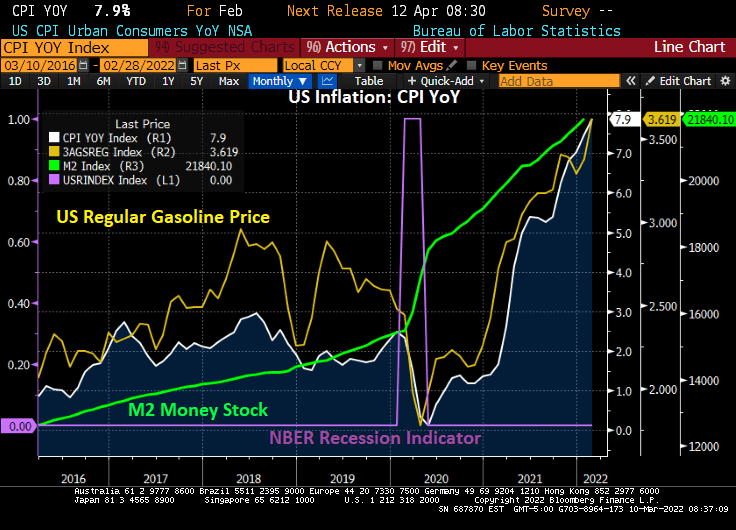

This is especially unfortunate given at inflation is growing at 7.9%. If we remove food and energy (two important categories for consumers and retirees), core inflation is growing at 6.4% YoY. As such, Social Security COLA doesn’t even keep pace with CORE inflation, let alone food and energy costs.

In August, Speaker Nancy Pelosi announced staffers’ salaries could exceed those of lawmakers. Members in both the House and Senate, with the exception of leadership, make an annual salary of $174,000. Staffers can make up to $199,300.

After an 11-year drought, congressional earmarks are back with vengeance.

The $1.5 trillion, 2,741-page omnibus spending package is loaded with funding for lawmaker pet projects, some of which could help incumbents in this fall’s elections.

The legislation includes more than 4,000 earmarks, according to a list of projects provided to The Hill by a Senate Republican aide that spanned 367 pages.

One of the biggest winners was New York — thanks to Senate Majority Leader Charles Schumer (D-N.Y.), who is up for reelection this year.

Schumer’s name is attached to 59 earmarks totaling nearly $80 million in the omnibus’s transportation and housing and urban development (HUD) section alone, according to a review by The Hill. He successfully requested funding for the projects either individually or with other lawmakers from his home state.

Is wild-spending Pelosi actually “The Bride of Chucky (Schumer)”?

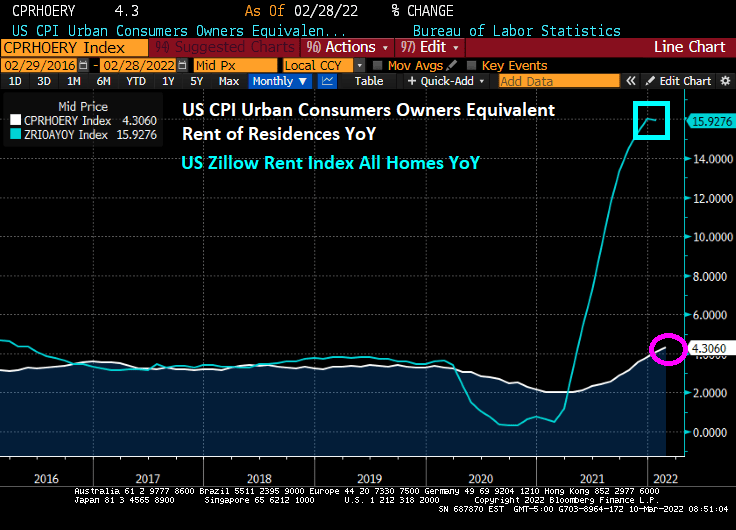

US rent inflation (owner’s equivalent rent of residence YoY) surged to 4.30%. However, Zillow’s rent index last month was 15.93% YoY.

But if we look at US Monthly Rent YoY, we see that rents are climbing at a 17.6% rate.

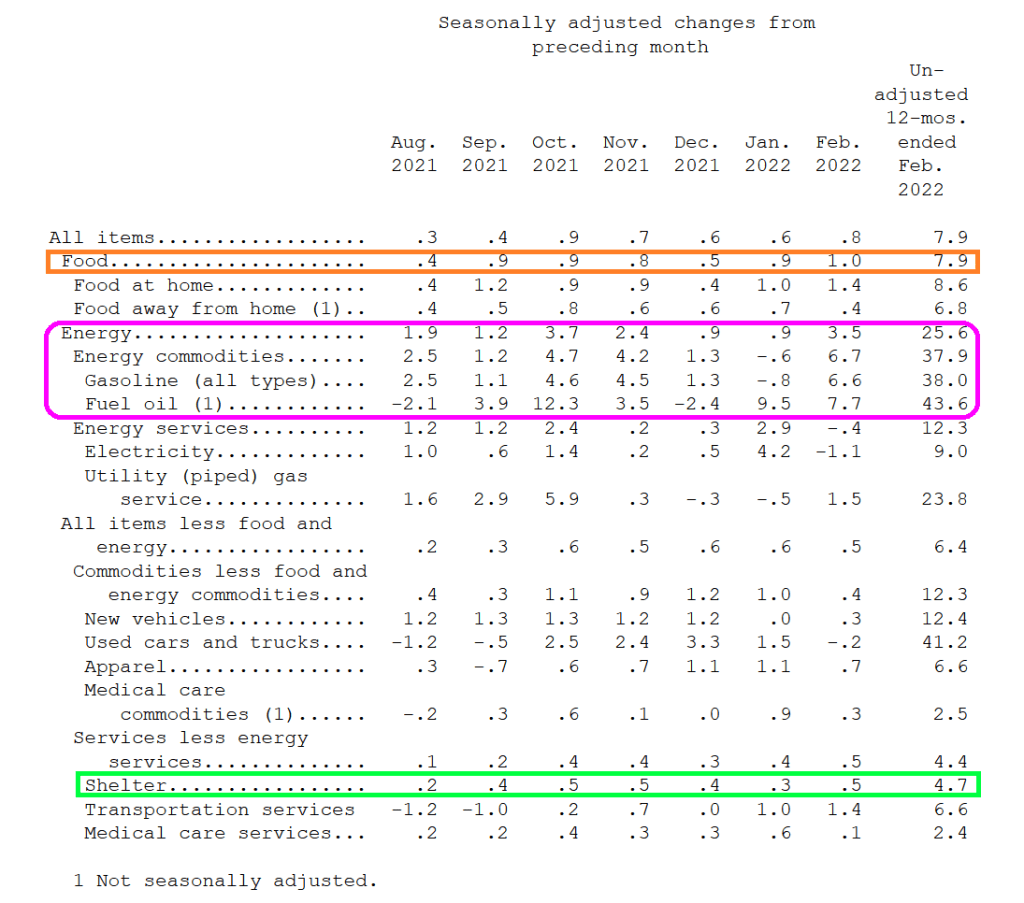

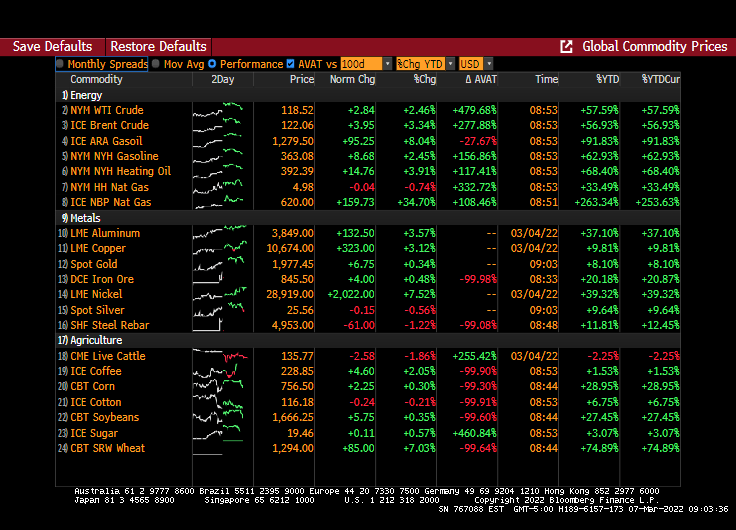

Energy costs soared in February YoY. Gasoline was up 38%. Fuel Oil was up 43.6%. Food was up 7.9%.

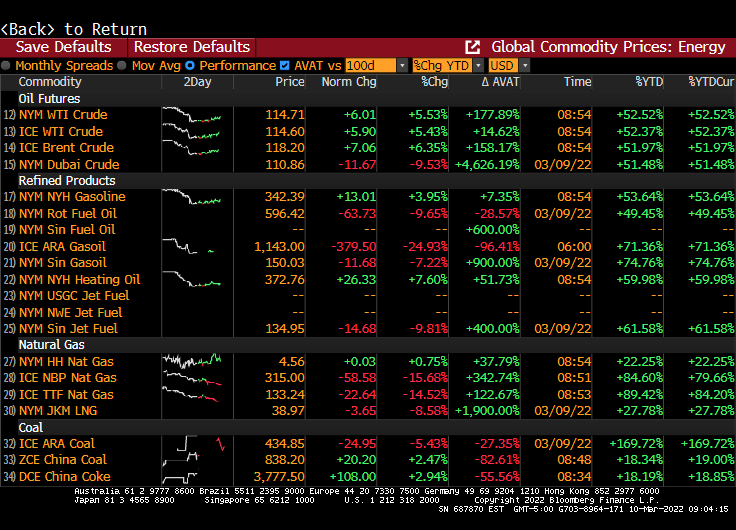

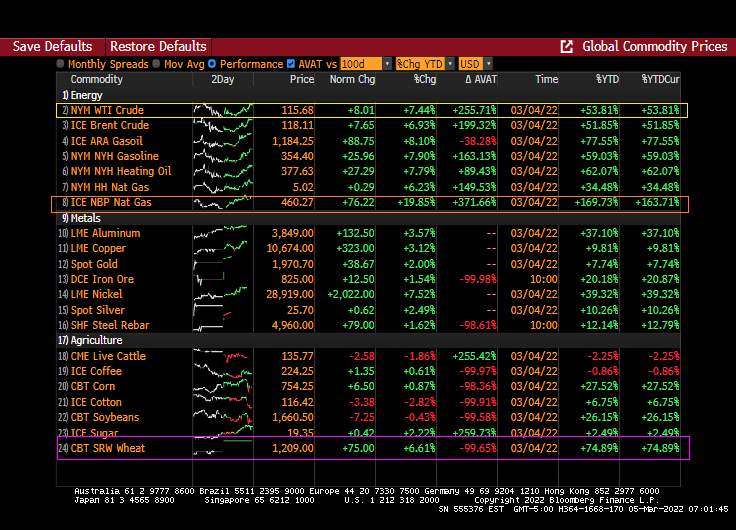

Volatility (AVAT) rages in the energy sector.

There are still 7 rate hikes in the cards from The Federal Reserve.

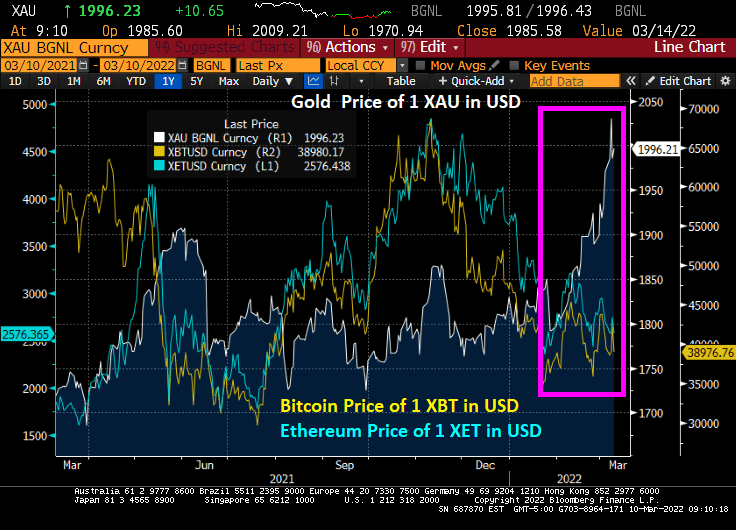

Gold has been climbing as Russia invades Ukraine. Cryptos Bitcoin and Ethereum are steady, even as the Biden Administration issues an executive order to “study” cryptocurrencies.

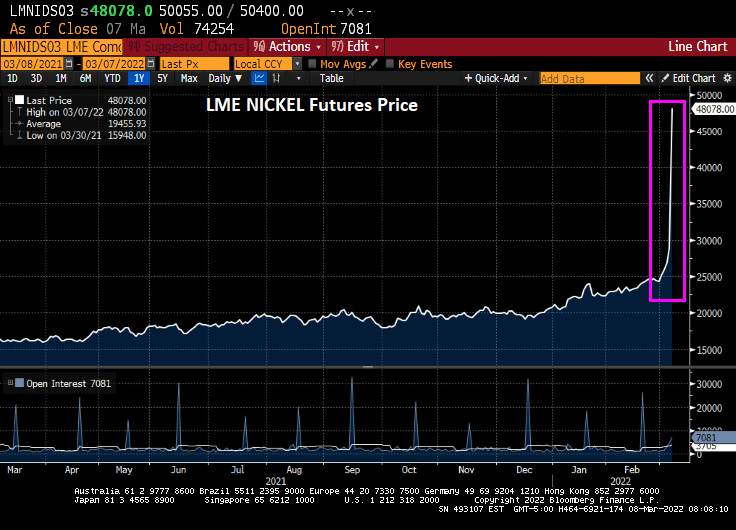

America is suffering a “nickel pickle.” As the US Federal government pushes their green energy agenda, Mayor Pete Buttigieg (aka, Transportation Secretary) on Monday said “the American people stand to benefit from having more electric vehicles on the road.” Unfortunately, electric vehicles use nickle in their production and guess who produces the most nickel? Russia.

Nickel futures were up +66.25%.

Unfortunately, Russia is the largest miner of nickel. But Brazil is second.

We are also seeing rising volatility of US stocks (VIX) and bonds (MOVE) as Russia’s invasion of Ukraine continues and crude oil prices soar.

While NYM WTI Crude volatility is up +296%, NYM DUBAI Crude is up +4,626.19%, and NYM JKM (Japan/Korea) natural gas volatilty is up 1,900%.

Now, US oil and gas exploration and drilling rig count has almost doubled under Biden as oil price surge.

We are in an American pickle since Russia is a major supplier of oil and natural gas as well as nickel.

WTI Crude Oil spot price was up 91% from the beginning of 2021 to the Russian invasion of Ukraine. Now it is up 142% thanks to the invasion of Ukraine.

Energy prices are still soaring with UK Natural Gas prices up another 34.70% today with Brent Crude futures up 3.34%. Wheat futures are up 7.03%.

The US Treasury 10Y yield rose 6.8 bps this morning (UK takes the lead with a 10.3 bps increase).

The US Treasury 10Y-2Y yield curve slope continues to swoon to where it is now flatter than when President Biden entered office.

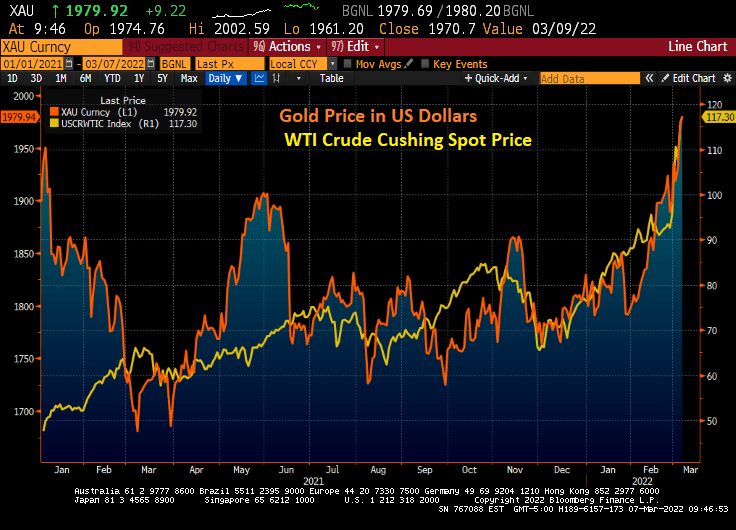

Gold is now at it highest level since before Biden was sworn-in as President as WTI Crude Oil soars.

Gold hit $2,000 before retreating back down.

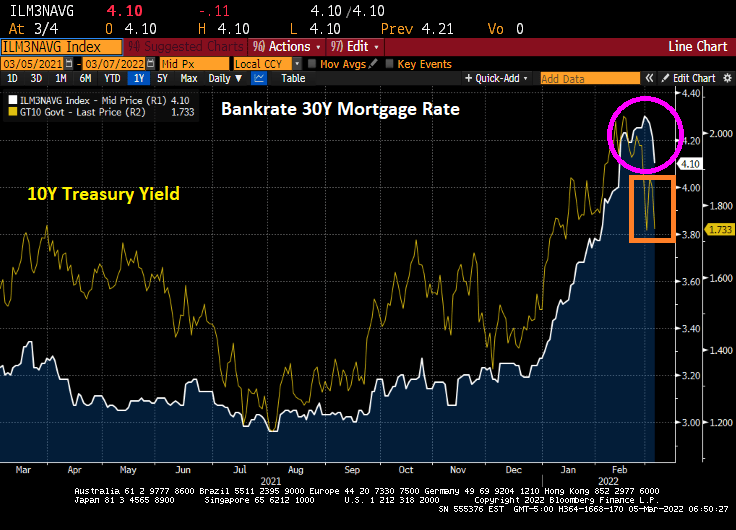

And Bankrate’s 30Y mortgage rate declined to 4.10%.

Russia is the world’s largest exporters of wheat and Ukraine is the 5th largest exporter.

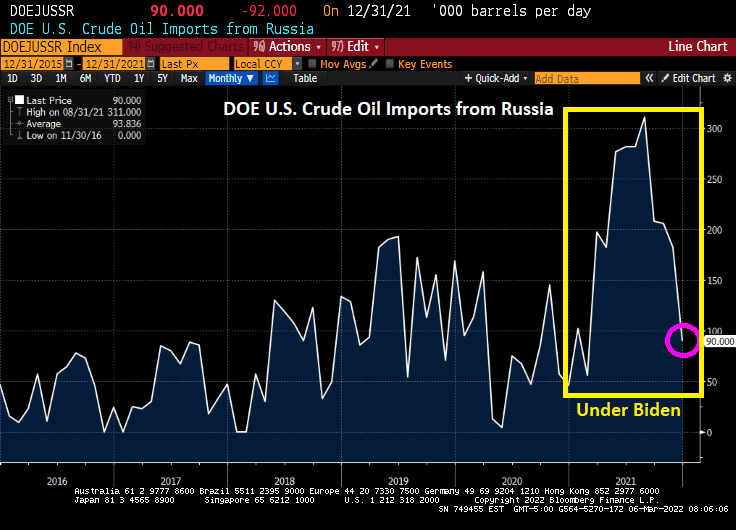

Russia is still engaged in its invasion of Ukraine. And the US continues to import crude oil from Russia. In fact, US crude oil imports from Russia soared under Biden only to decline again in December 2021.

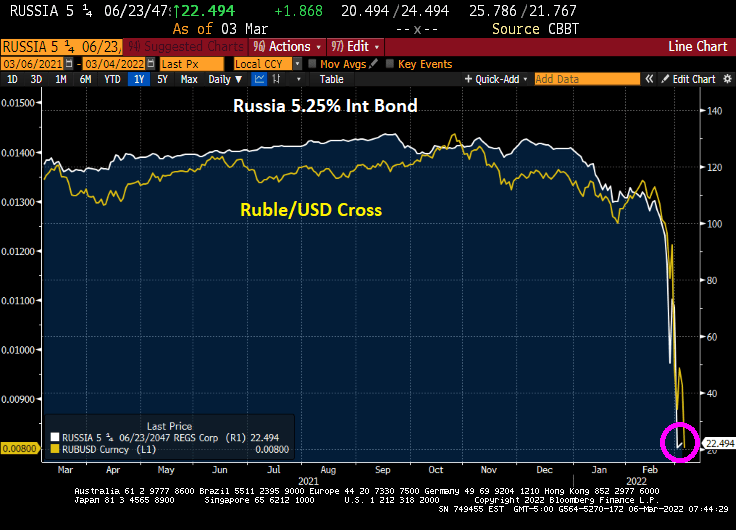

On the sovereign bond and currency front, the 5.25% coupon Russian international sovereign bond has crashed to 22.494. And the Ruble/USD cross has crashed as well.

Sberbank Bank 5 1/8% corporate bond has crashed to 25.

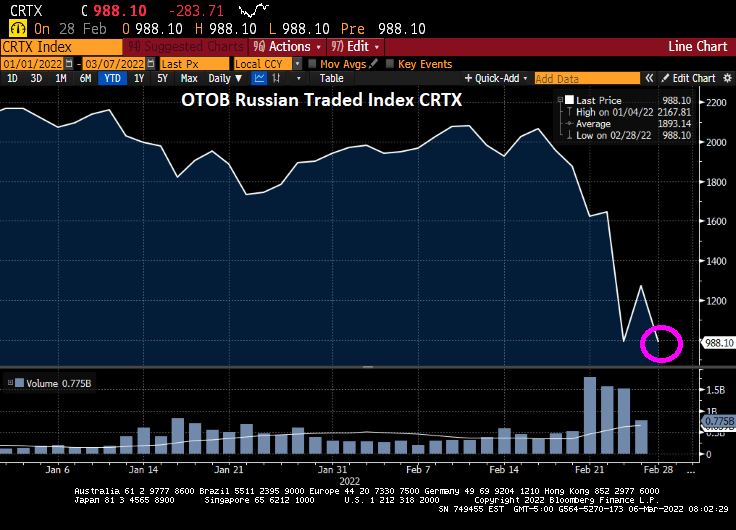

The Russian blue-chip stock market (OTOB Russian Traded Index CRTX) has crashed by over 50% since the invasion of Ukraine.

Fortunately, I like Cheerios for breakfast made from oats, since wheat futures are soaring.

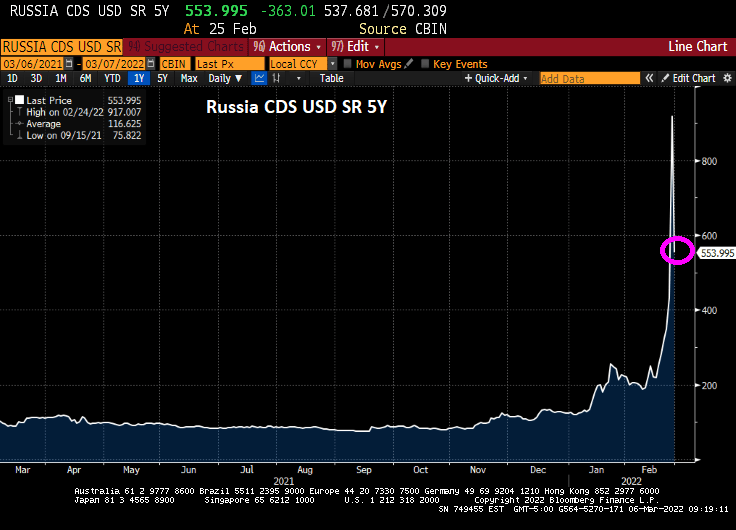

Russia’s Credit Default Swap (CDS) 5Y has dropped to a still-elevated 554.

The US really needs to ban Russian crude oil imports, since Biden’s failed in game theory by cutting US energy exploration on Federal lands and offshore drilling.

War is hell, as Vlad “The Ukrainian Impaler” Putin has demonstrated.

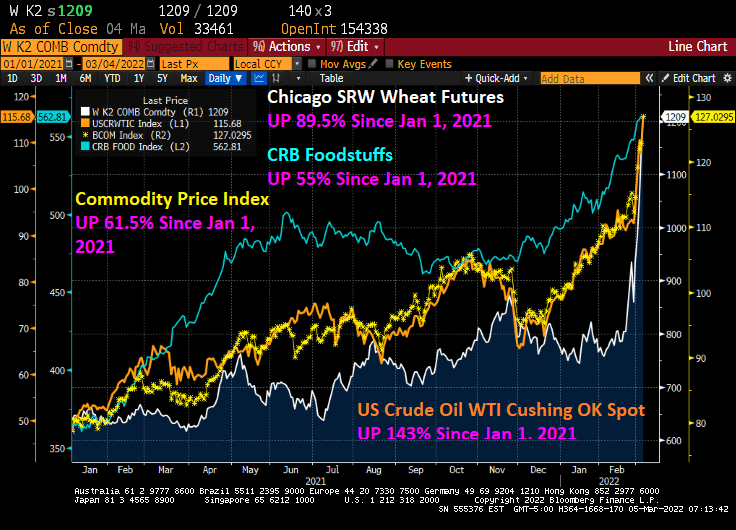

This has been a brutal week for consumers. With the Russia/Ukraine conflict raging and Congress seems determined to not allow for additional oil and gas production, and Biden’s anti-fossil fuel edicts still in place, we are seeing dramatic price increases in wheat (UP 89.5% since January 1, 2021), WTI Crude (UP 143% since January 1, 2021), and food stuffs (UP 55% since January 1, 2021).

Bankrate’s 30-year mortgage rate has actually been falling the last several days, which is good for prospective home buyers as the 10-year US Treasury Note yield has been declining.

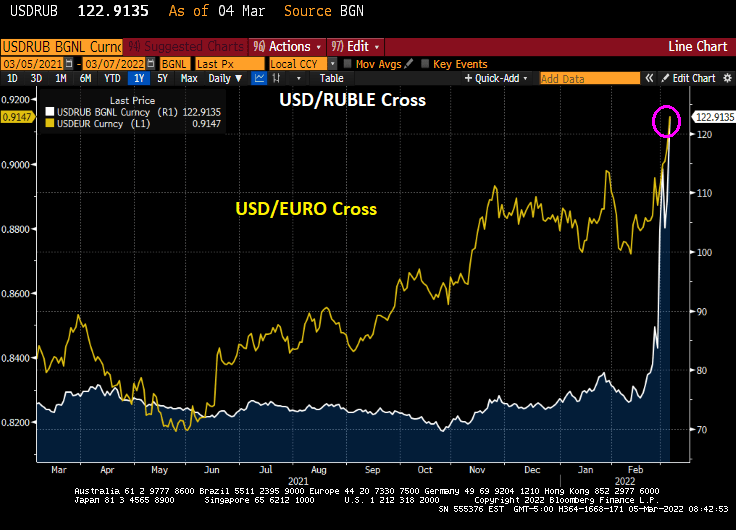

The USD/Russian Ruble cross is skyrocketing and the USD/Euro is doing likewise. Russians visiting the US will find that their trip is suddenly unaffordable (as do many American citizens will its rampant inflation). As Bruce Willis said in “Die Hard,” “Welcome to the party, pal.”

On Friday, the US Treasury 10-year yield declined 11 bps.

And energy prices continue to soar, particularly UK Natural Gas Futures that rose 19.85% overnight.

The US inflation data will be released on March 10th and the consensus is that February CPI inflation will rise to 7.9% YoY.

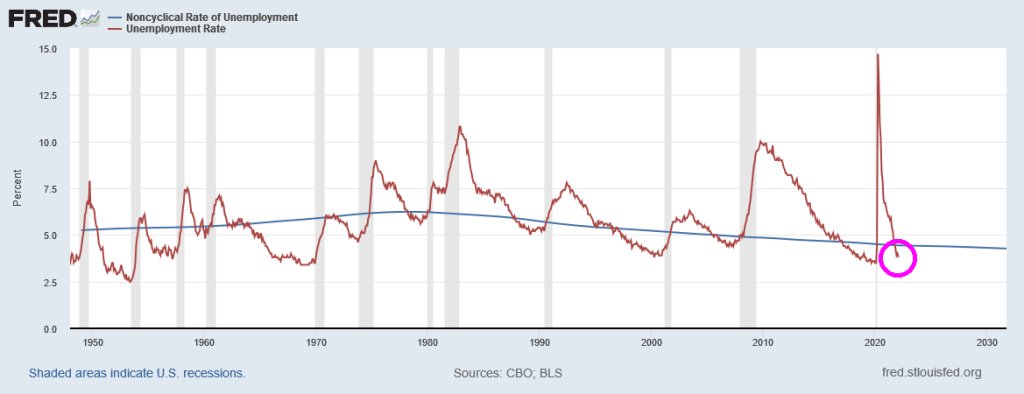

But even the latest unemployment rate report (3.8%) is signalling that The Fed should be raising interest rates since it is lower than the Natural Rate of Unemployment or NAIRU (4.44%).

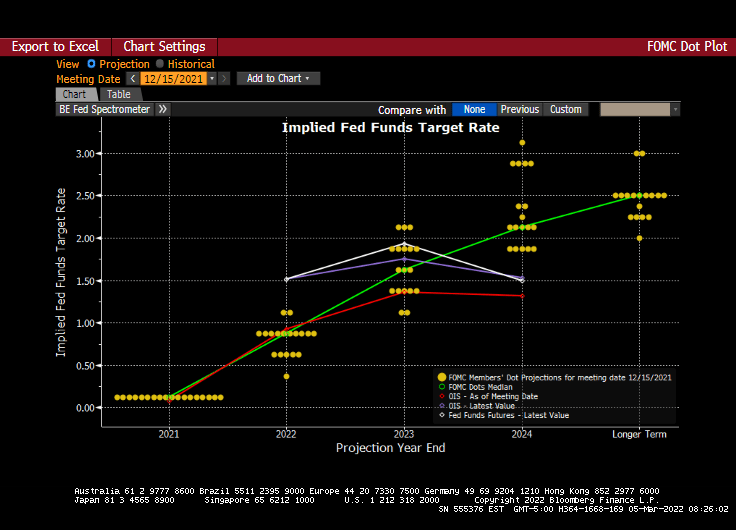

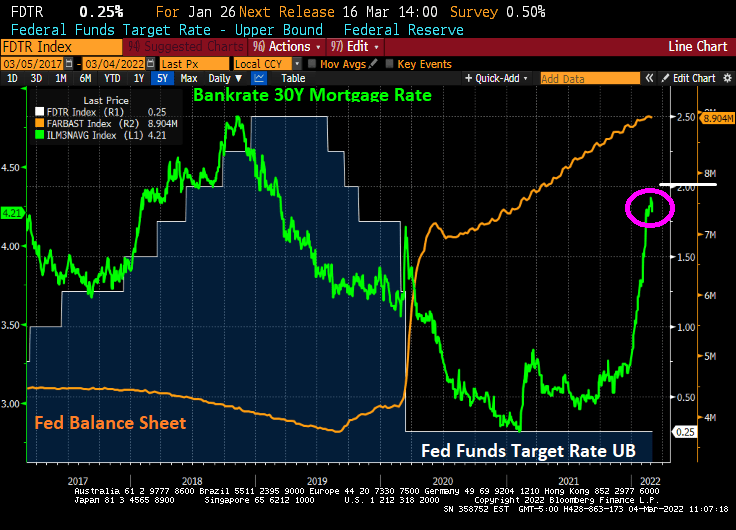

And we have the next Fed policy error on March 16th. The Fed dots plot looks like the glide slope for an aircraft, but the message is that rates will be going up at future meetings.

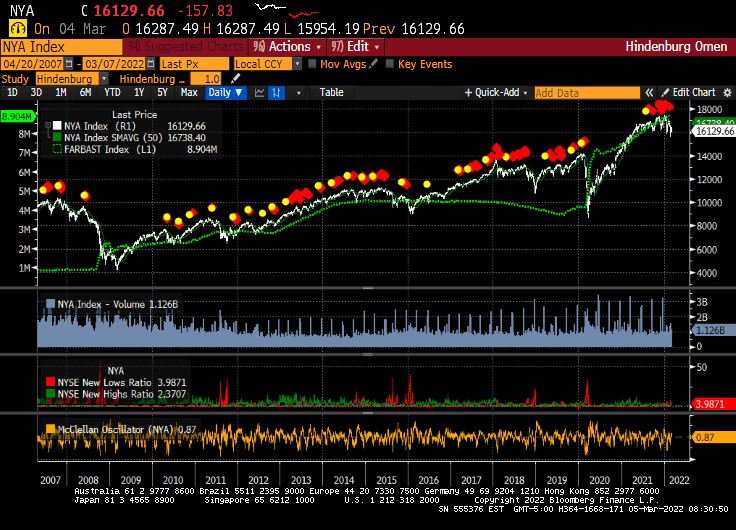

And just for amusement, I present to you the infamous Hindenburg Omen chart that forecast the 2008/2009 stock market correction. Since that correction, the Hindenburg Omen has been flashing “danger” but the only correction was the COVID-linked correction of early 2020. While the Hindenburg Omen is flashing red right now, The Federal Reserve’s balance sheet (green line) has protected against market corrections. Let’s see what happens if and when The Fed decides to remove the epic monetary stimulus.

Its anyone’s guess as to whether The Fed will actually tighten monetary policy.

Despite crude oil, natural gas and gasoline price skyrocketing, House Speaker Nancy Pelosi proclaimed that

“The president has already talked about releasing oil from the — the st– as he already has done from the (slurred, inarticulate). And (slurred, inarticulate) I’m not for drilling on public lands.”

Well, if President Biden rescinded his executive order on drilling, pipelines, etc., we would see a reduction in energy prices AND inflation. But between Biden’s anti-fossil fuel orders and the Russia-Ukraine conflict, we can see that the WTI Cushing crude oil spot price has risen from $47 per barrel in early January 2021 to $112.05 today. That is over a doubling of crude oil prices.

Energy prices are up across the board, particularly gasoil, heating oil and coal.

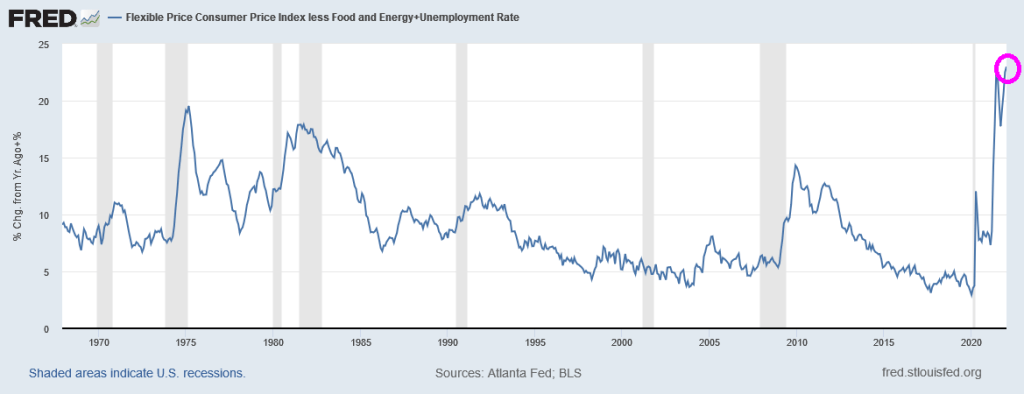

If we use the core Flexible Price Index as a measure of inflation, we can see that Americans are the most miserable in modern history (Core Flexibe CPI + U-3 Employment rate).

UPDATE! House Republicans introduced the “American Independence from Russian Energy Act” on Feb. 28, a measure meant to authorize the Keystone XL pipeline, boost domestic oil and gas production, and prevent President Joe Biden’s executive branch agencies from halting energy leasing on federal land and water, among other provisions. Yet on March 1, the legislation was shot down by Democrats in a 221–202 vote, almost entirely along partisan lines.

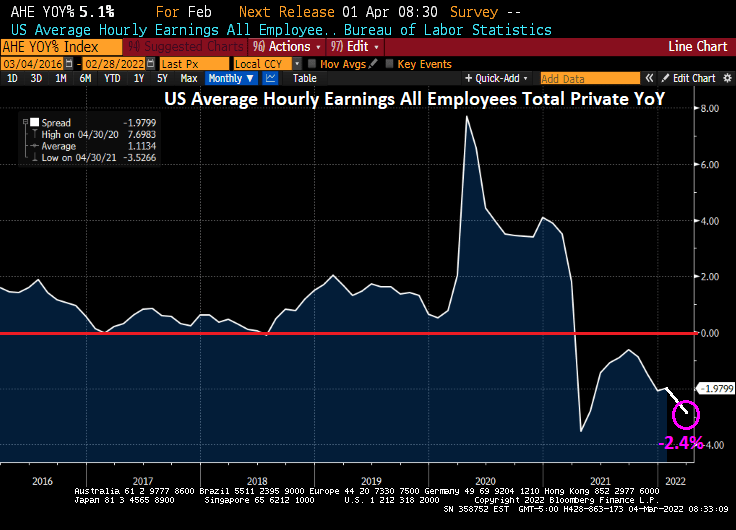

The bad: Month-over-month wage earning experienced 0% growth (although YoY growth declined to 5.1%).

The ugly: inflation is still at 40 years highs of 7.5%. Meaning that REAL wage growth is -2.4%.

Here is the jobs report summary.

Of course, the leading sector for job creation was … leisure and hospitality with 179k added. Food services and drinking places (aka, bars) added 124k jobs.

Energy prices are way up … again … which will fuel more price increases. WTI Crude is up over 4% overnight, NYH gasoline futures are up 4.33%, coal is up 22.48%.

You must be logged in to post a comment.