Michael Lea and I wrote a paper several years ago arguing that most borrowers would be better-off with an adjustable-rate mortgage than a fixed-rate mortgage. The US is one of the few countries in the world where the 30-year fixed-rate mortgage is dominant. Why is this the case? FEAR of rising mortgage payments with adjustable-rate mortgages (ARMs) while the fixed-rate mortgage (FRMs) have constant payments over the 30-year term.

The reason why the fear of ARMs is unwarranted is that ARMs generally have CAPS on rate increases, either in a given period or over the life of the loan. Of course, READ the loan terms to ensure that the ARMs has restrictive caps on rate increases.

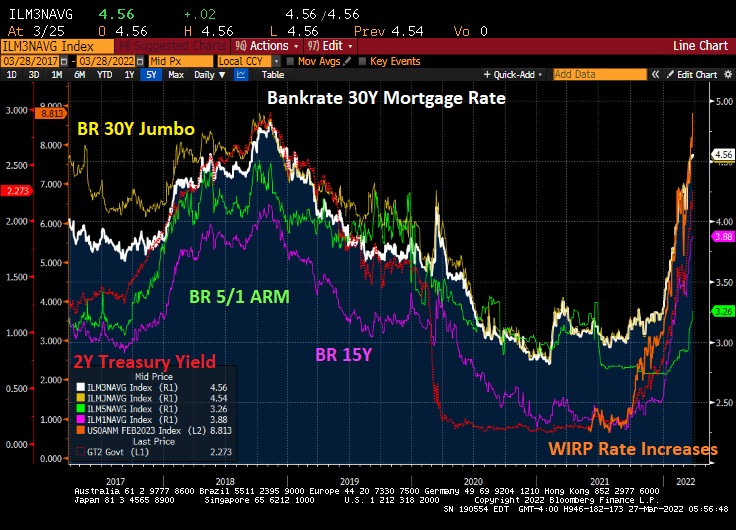

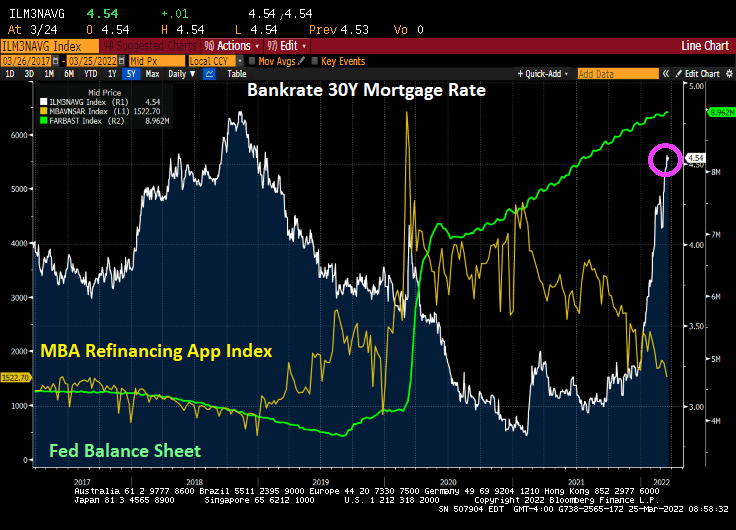

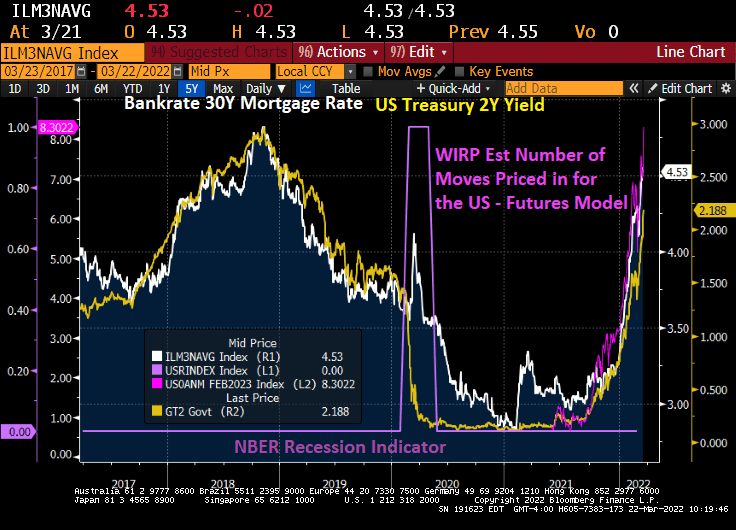

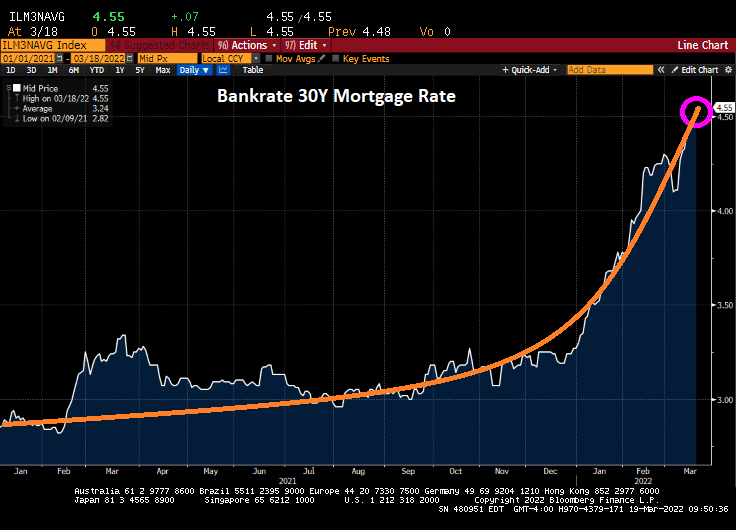

Currently, the 5/1 ARM is at 3.26% while the 30-year FRM is at 4.56%, a spread of 130 basis points.

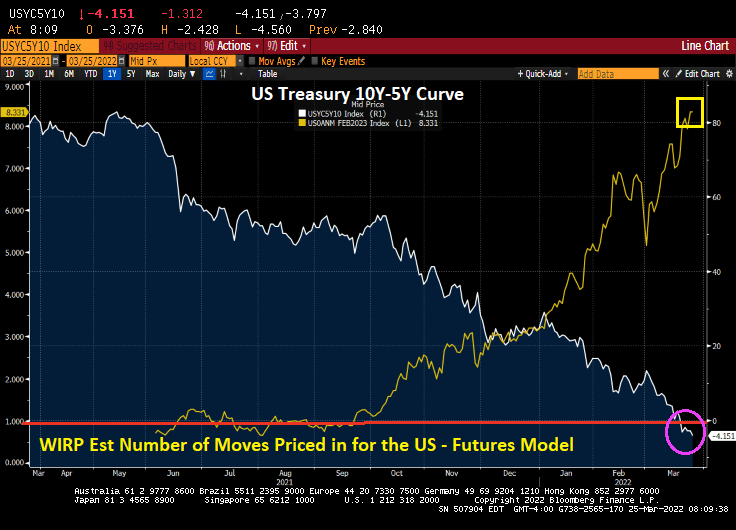

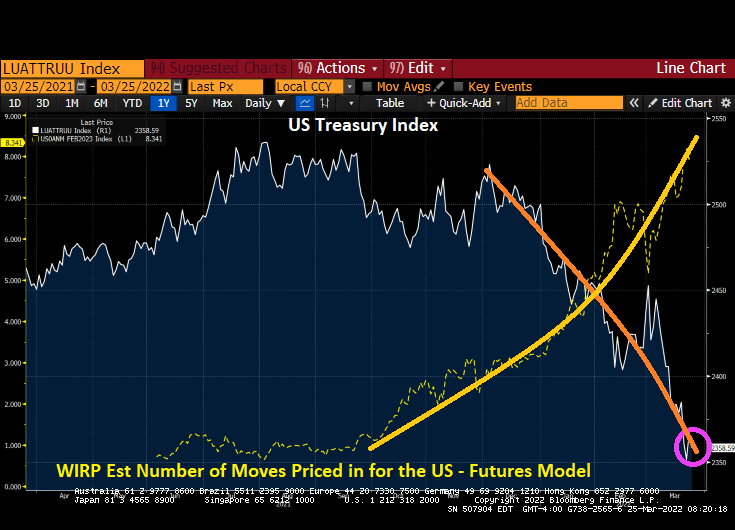

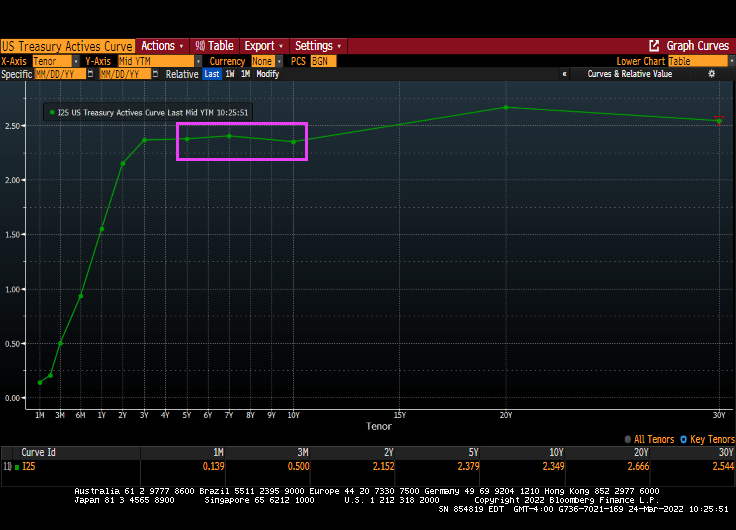

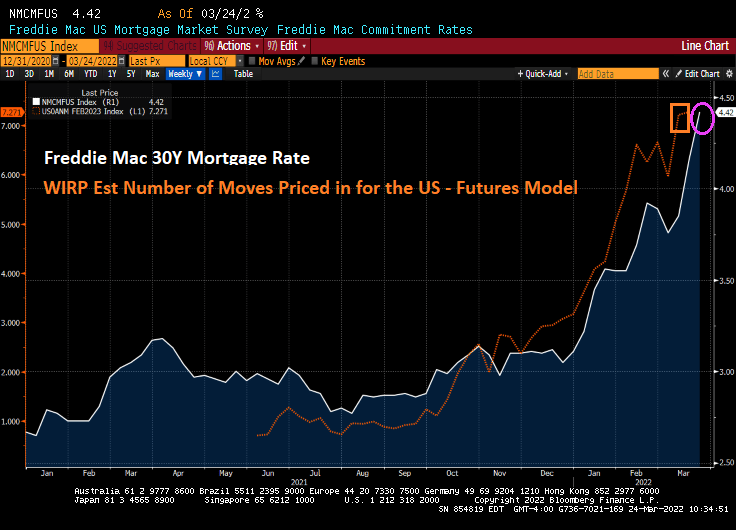

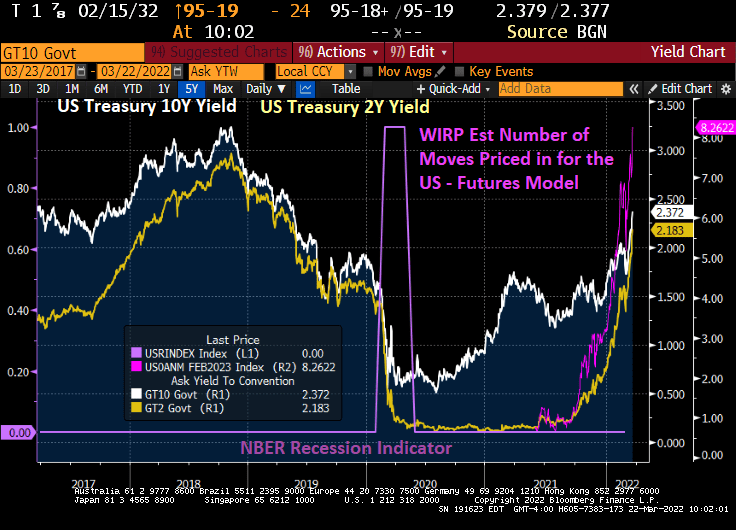

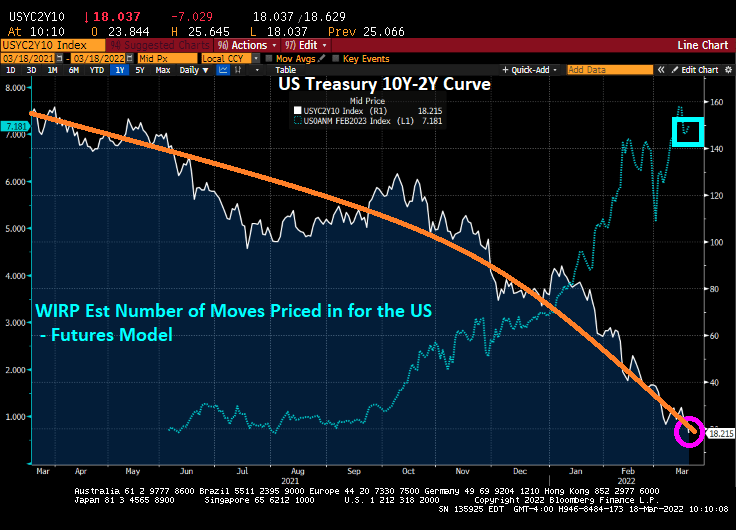

Mortgage rates of all flavors are rising rapidly with the expectation of Federal Reserve Quantitative Tightening (QT). There are several headwinds that could counter The Fed’s QT efforts such as low GDP growth (Atlanta Fed’s GDPNow real-time GDP tracker is at 0.9% for Q1), the Russia-Ukraine invasion, approaching midterm elections, etc. But as of today, The Fed seems on a collision course with rising mortgage rates.

With the increasing likelihood of Fed rate hikes over the next year, we are seeing an increase in US ARM loan share from 4% to 7.9%, almost a doubling of ARM share. But FRMs are still over 90% of all mortgage originations.

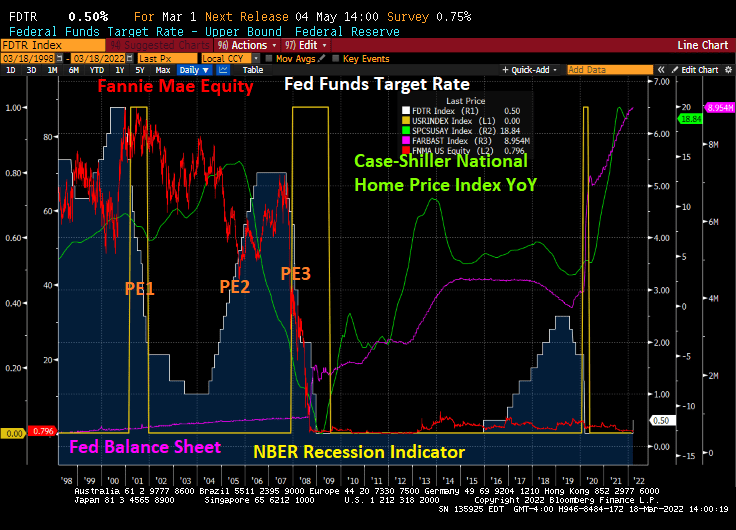

Lending institutions would prefer consumers to use ARMs rather than FRMs since ARMs allow for the transfer on long-term interest rate risk to the borrower, while the FRM sticks the lender with long-term interest rate risk. Hence, we have Fannie Mae and Freddie Mac, the Government Sponsored Enterprises (GSEs) that allow lenders to originate FRMs and sell them to F&F. We are the only country with twin GSEs.

So, while most consumers would be better-off with an adjustable-rate mortgage, the structure of the mortgage market (particularly after the financial crisis) encourages lenders to originate FRMs and sell them to Fannie Mae and Freddie Mac.

But FEAR drives many US mortgage borrowers into the FRM space rather than getting an ARM with a lower interest rate, even if ARM caps would prevent the mortgage rate from rising more than 100 basis points over the life of the loan.

You must be logged in to post a comment.