Mortgage applications are going down as expectations of monetary tightening send mortgage rates soaring.

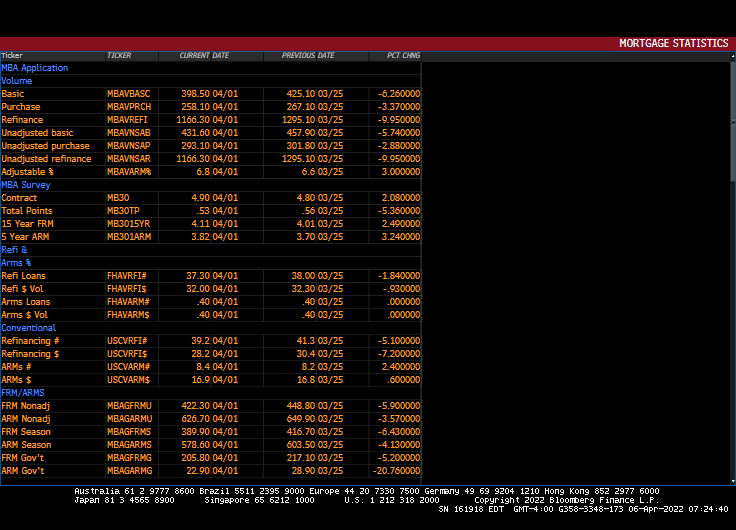

Mortgage applications decreased 6.3 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 1, 2022.

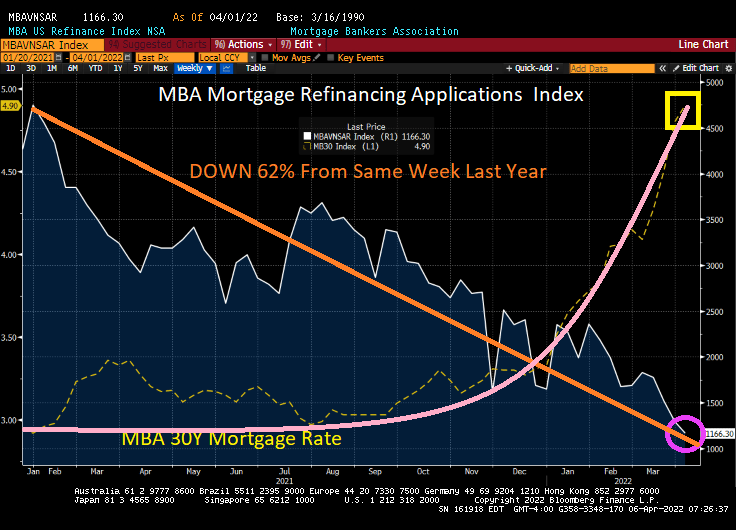

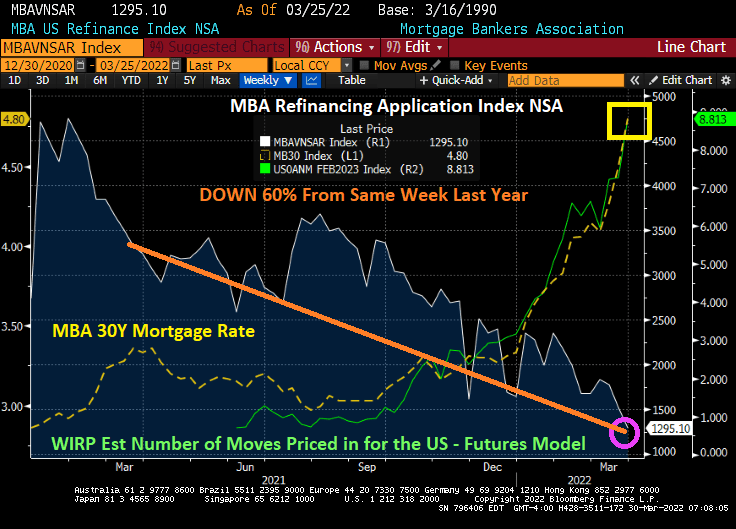

The Refinance Index decreased 10 percent from the previous week and was 62 percent lower than the same week one year ago.

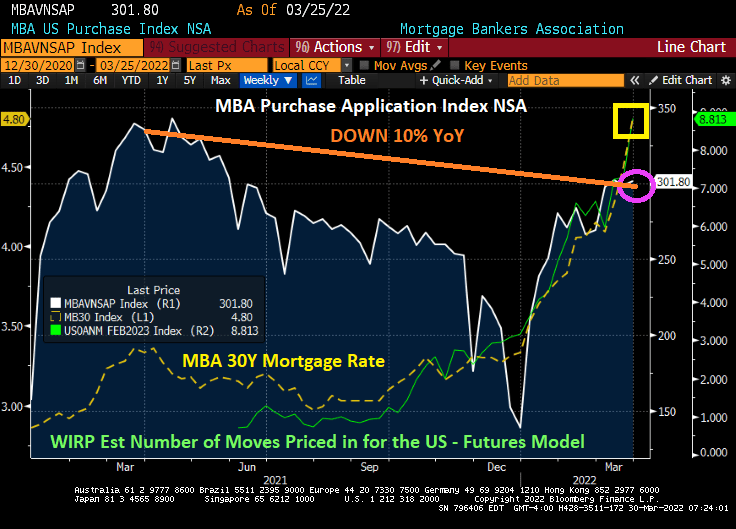

The seasonally adjusted Purchase Index decreased 3 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 9 percent lower than the same week one year ago.

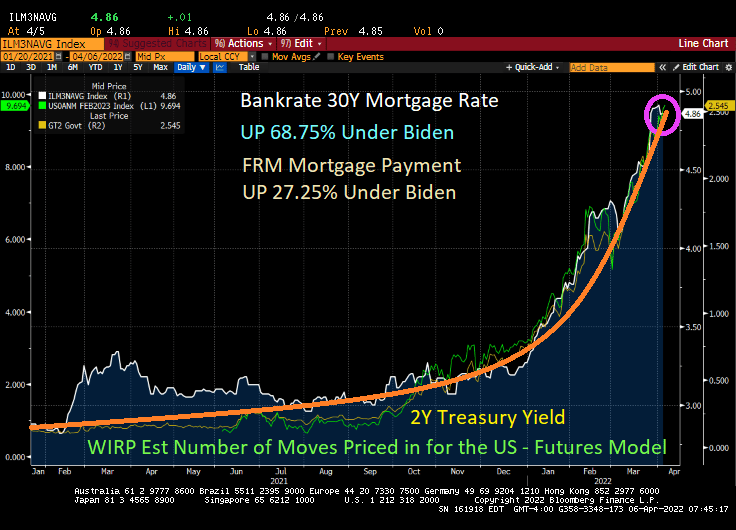

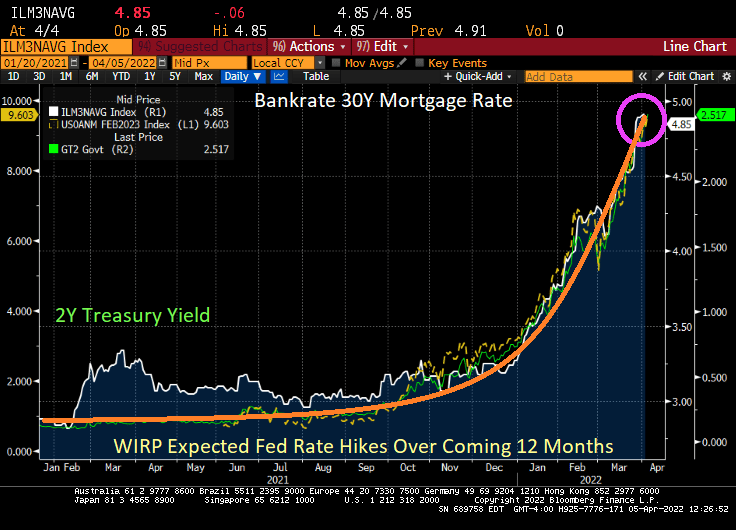

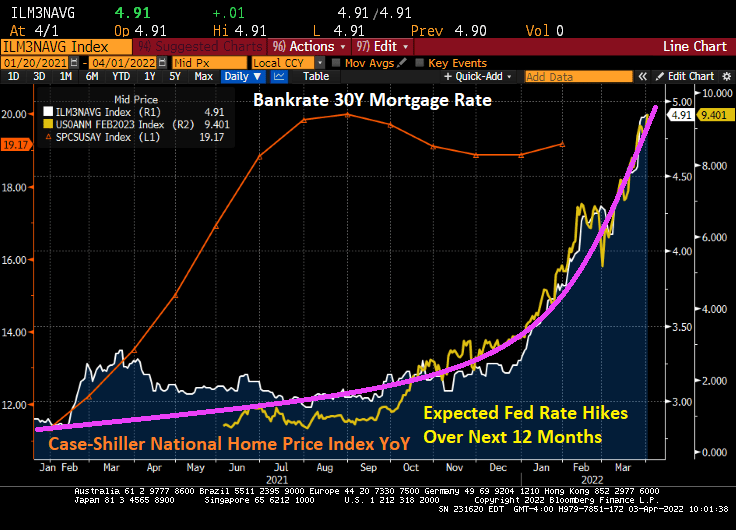

Bankrate’s 30-year mortgage rate rose only slightly today to 4.86%, but the 30-year mortgage rate has risen 68.75% and a fixed-rate mortgage payment has risen 27.25% under Biden.

The rest of the story? The adjustable rate mortgages (ARMs) remain at only 6.8% of loan origination volume despite being almost 150 basis points lower in rate (4.90 FRM versus 3.38% 5/1 ARM).

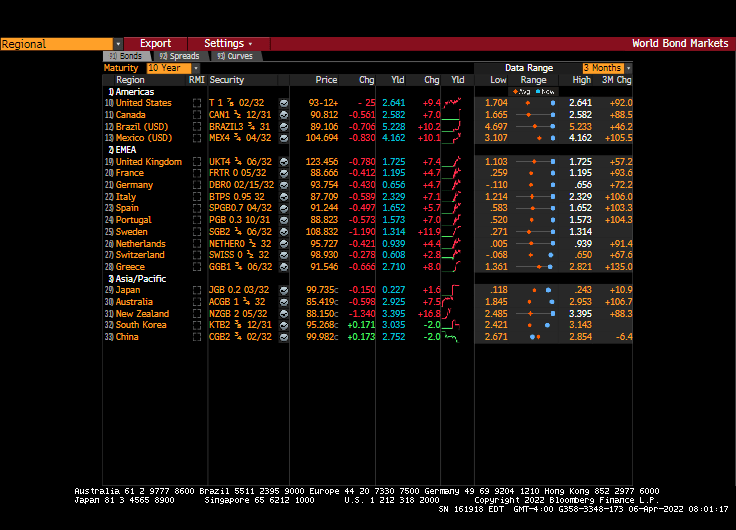

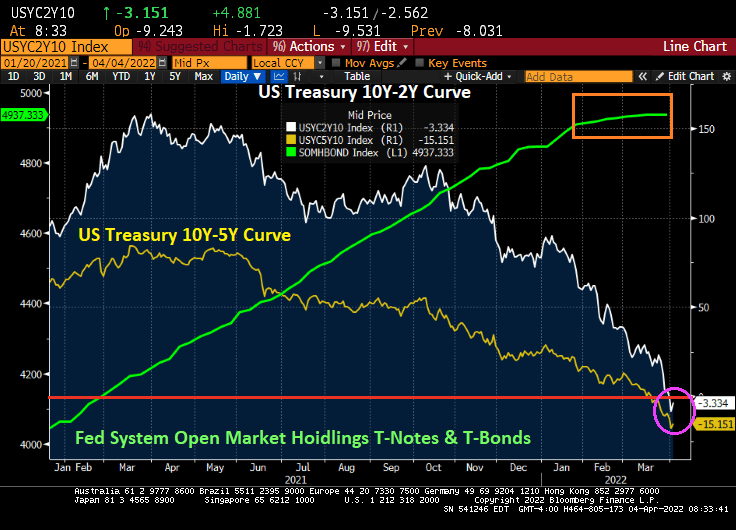

Meanwhile, US Treasury yields rose again with the 10-year yield rising almost 10 basis points … again.

And President Obama spoke at The White House defending his healthcare initiative, The Affordable Care Act. It seems that Nancy Pelosi, Amy Klobuchar, Jame Clyburn and the others were thrilled to see Obama back in The White House. So much so that Biden was abandoned on stage and left to wander aimlessly around.

You must be logged in to post a comment.