Warning! Evidence of a US recession is appearing. And with a recession, prices will likely fall due to lack of demand.

Why might inflation be falling? Take a gander at ISM Prices Paid. They just fell to the lowest level since the infamous Covid economic shutdowns of 2020.

M2 Money growth YoY is the lowest in years, but The Fed’s balance sheet remains elevated. But apparently the Covid-related sugar rush has ended.

As soon as Bidenflation started soaring with his war on fossil fuels and manic Federal spending, we saw The Federal Reserve starting to remove the excessive monetary stimulus, but Congress didn’t cancel its spending spree.

We ADP jobs report yesterday was ugly (+127k jobs added after +239k jobs added in October). Now we have the Challenger, Gray and Christmas jobs report for Novemeber … and it is terrible. An increase of 416.5% in job cuts.

Today, the US Personal Consumption Expenditures data was released. It shows that the CORE PCE YoY fell to a still high 5%.

If The Fed actually followed any rules other than CNTRL PRINT, we can see that with Core PCE YoY of 5% (or 4.98% to be exact), the Taylor Rule estimate for where The Fed Funds Target rate should be is … 9.78%

Yes, The US Treasury 10Y-2Y yield curve remains inverted, for the 104th straight day. And Bankrate’s 30-year mortgage rate has dropped -57 basis points since November 3, 2022.

This comes after a gruesome Pending Home Sales and mortgage applications reports today.

The Federal Reserve continues to remove the monetary punch bowl despite the global yield curve inverting and The Fed fighting Bidenflation.

On the mortgage front, mortgage applications decreased 0.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 25, 2022. This week’s results include an adjustment for the observance of the Thanksgiving holiday.

The Refinance Index decreased 13 percent from the previous week and was 86 percent lower than the same week one year ago. The unadjusted Purchase Index decreased 31 percent compared with the previous week and was 41 percent lower than the same week one year ago.

On the housing front, US pending home sales fell for a fifth month in October as demand continued to sag under the weight of high mortgage rates.

The National Association of Realtors index of contract signings to purchase previously owned homes decreased 4.6% last month, according to data released Wednesday. And fell -36.7% YoY.

All together now. Look at pending home sales YoY and mortgage purchase applications SA compared with M2 Money YoY.

The hawkish drumbeat from central bankers is raising fears of a downturn, with global bonds joining US peers in signaling a recession, as a gauge measuring the worldwide yield curve inverted for the first time in at least two decades.

The US Treasury 10Y-2Y yield curve, on the other hand, has been inverted for 107 straight months.

And in Europe, 10-year sovereign yields are dropping like a paralyzed falcon.

The world and US yield curves are pointing to trouble. And drums along the Potomac (DC) and East River (NYC).

During the Covid crisis of 2020 (red box). consumer credit declined and households were saving. But following the end of US Covid economic shutdowns, we saw inflation soaring to 40-year highs as Biden declared war on fossil fuels and a Pelsoi-led Congress went on an epic spending spree. But with soaring inflation, came a decline in personal savings and soaring consumer credit outstanding in an attempt to cope with Bidenflation.

Meanwhile, in the crypto universe, CNBC’s Jim Cramer and ARK’s Cathie Wood are going big for cryptos. With Wood buying Bitcoin and Cramer touting Coinbase.

Hmmm.

But at least Litecoin and the others are up today. Likely because Cramer and Wood are touting cryptos with “buy the dip!” strategy.

And on the Sam Bankman-Fried fiasco front, I am watching the deflection of wrongdoing from SBF to his girlfriend and now the co-CEO of Alameda Research, Sam Trabucco.

Bloomberg: He has a degree from MIT and cut his teeth as a trader at Susquehanna International Group. Yet the former co-head of Alameda Research made it clear that poker and black-jack tables were where he honed the gambler’s instincts he applied to cryptocurrency trading.

“I may or may not be banned from 3 casinos for this,” Sam Trabucco once tweeted about counting cards at black jack tables.

Today, the PPI Final Demand YoY index printed for October was it was still agonizingly high at 8% YoY (The Fed likes to see 2% for inflation).

True, PPI Final Demand YoY is down from its recent peak of 11.7% YoY in March. But notice that M2 Money YoY (liquidity) has collapsed following the Covid surge (green line).

Then I have this update on Sam Bankman-Fried of FTX and Alameda Research notoriety.

As Sam Bankman-Fried’s crypto empire imploded last week, costing him effectively all of his $15.6 billion fortune, other digital-asset billionaires sought to make clear that their steep losses in 2022 wouldn’t be similarly fatal.

Cameron Winklevoss, 41, who along with his twin brother Tyler founded cryptocurrency exchange Gemini, posted an 11-part series of tweets emphasizing that Gemini “has no exposure to FTT tokens or Alameda and no material exposure to FTX,” referring to Bankman-Fried’s trading house and crypto exchange.

And despite Spam Bankman-Fried’s disaster for his investors like Tom Brady, Steph Curry and the Democrat party, the crytpo market has done some recovery with most cryptos this morning.

The evidence from the last thirty years is clear. Keynesian policies leave a massive trail of debt, weaker growth and falling real wages. Furthermore, once we look at each so-called stimulus plan, reality shows that the so-called multiplier effect of government spending is virtually inexistent and has long-term negative implications for the health of the economy. Stimulus plans have bloated government size, which in turn requires more dollars from the real economy to finance its activity.

As Daniel J. Mitchell points out, there is evidence of a displacement cost, as rising government spending displaces private-sector activity and means higher taxes or rising inflation in the future, or both. Higher government spending simply cannot be financed with much larger economic growth because the nature of current spending is precisely to deliver no real economic return. Government is not investing; it is financing mandatory spending with resources of the productive sector. Every dollar that the government spends means one less dollar in the productive sector of the economy and creates a negative multiplier cost.

When society decides to use a certain part of the resources generated by the productive sector for non-economic return activities, be it social spending or mitigation of threats, it can only do it by understanding how much of the productive capacity of the economy is able to sustain a larger cost. When costs are not considered as a burden, but considered as entitlements that can only grow, the productive capacity is not strengthened, but weakened.

The main problem of the past decades, but particularly since 2008, is that government spending and monetary policy have become solutions of first resort to any slump in economic activity, even if that decline was created by government decisions, such as shutting down the economy due to a health crisis. Furthermore, government spending increases and loose monetary policy continued even in growth periods. This, in turn, creates an unsustainable public deficit that needs to be monetized or refinanced. Both mean a larger harm for the productive sector as the debt increase leads to higher taxes for everyone but also a soaring cost of living coming from the destruction of purchasing power of the currency.

Government spending does not boost private sector activity, even less so when the entire budget is spent on non-investment outlays. It is even worse when citizens believe that infrastructure or real economic return investments should be conducted with taxpayers’ money. If an investment is productive and economically viable there is no need to involve the government. At best, the government should only participate as a co-investor, as the example of technology and defence shows, but never as a resource allocator for a simple reason. Public intervention is always aimed at perpetuating the existing inefficiencies and maximizing the budget. Efficient resource allocation cannot come from entities that have a core interest in expanding the budget and always perceive any inefficiency or poor result as the consequence of not having spent enough.

Yes, US public debt has exploded, particularly since the 2008 financial crisis and then again the Covid outbreak of 2020.

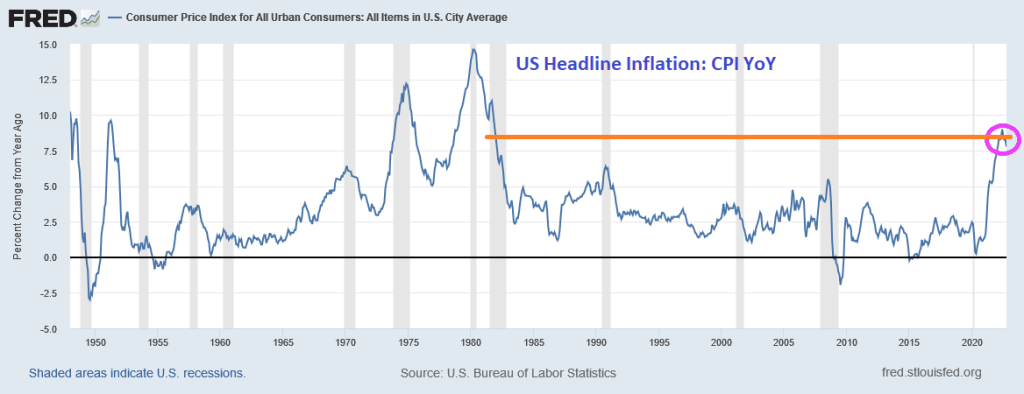

And inflation is near a 40-year high.

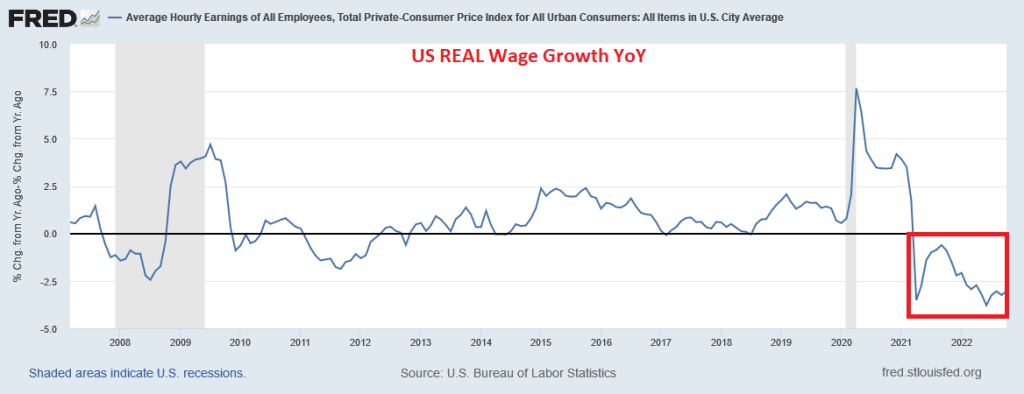

Then we have 19 consecutive months of negative wage growth in the US.

Biden is apparently doubling down on “Green Schemes” now that the US House of Lords (aka, Senate) remain under Keynesian control (aka, Democrat). So watch for inflation to start increasing again.

You must be logged in to post a comment.