The evidence from the last thirty years is clear. Keynesian policies leave a massive trail of debt, weaker growth and falling real wages. Furthermore, once we look at each so-called stimulus plan, reality shows that the so-called multiplier effect of government spending is virtually inexistent and has long-term negative implications for the health of the economy. Stimulus plans have bloated government size, which in turn requires more dollars from the real economy to finance its activity.

As Daniel J. Mitchell points out, there is evidence of a displacement cost, as rising government spending displaces private-sector activity and means higher taxes or rising inflation in the future, or both. Higher government spending simply cannot be financed with much larger economic growth because the nature of current spending is precisely to deliver no real economic return. Government is not investing; it is financing mandatory spending with resources of the productive sector. Every dollar that the government spends means one less dollar in the productive sector of the economy and creates a negative multiplier cost.

When society decides to use a certain part of the resources generated by the productive sector for non-economic return activities, be it social spending or mitigation of threats, it can only do it by understanding how much of the productive capacity of the economy is able to sustain a larger cost. When costs are not considered as a burden, but considered as entitlements that can only grow, the productive capacity is not strengthened, but weakened.

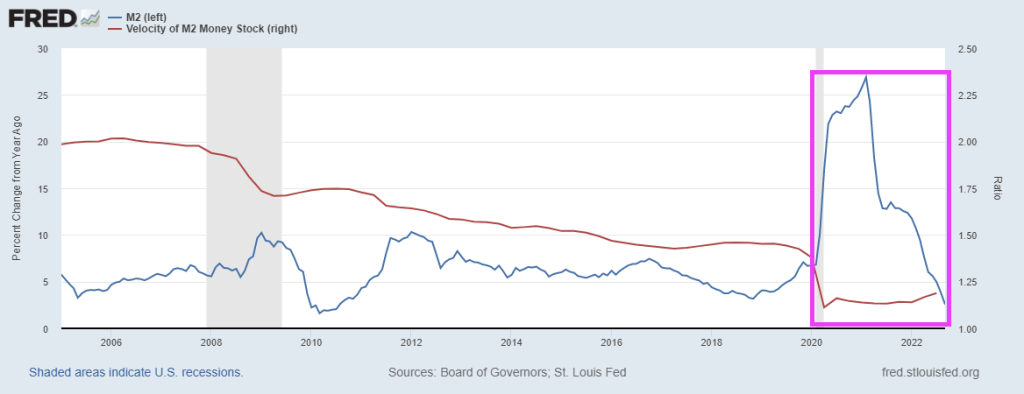

The main problem of the past decades, but particularly since 2008, is that government spending and monetary policy have become solutions of first resort to any slump in economic activity, even if that decline was created by government decisions, such as shutting down the economy due to a health crisis. Furthermore, government spending increases and loose monetary policy continued even in growth periods. This, in turn, creates an unsustainable public deficit that needs to be monetized or refinanced. Both mean a larger harm for the productive sector as the debt increase leads to higher taxes for everyone but also a soaring cost of living coming from the destruction of purchasing power of the currency.

Government spending does not boost private sector activity, even less so when the entire budget is spent on non-investment outlays. It is even worse when citizens believe that infrastructure or real economic return investments should be conducted with taxpayers’ money. If an investment is productive and economically viable there is no need to involve the government. At best, the government should only participate as a co-investor, as the example of technology and defence shows, but never as a resource allocator for a simple reason. Public intervention is always aimed at perpetuating the existing inefficiencies and maximizing the budget. Efficient resource allocation cannot come from entities that have a core interest in expanding the budget and always perceive any inefficiency or poor result as the consequence of not having spent enough.

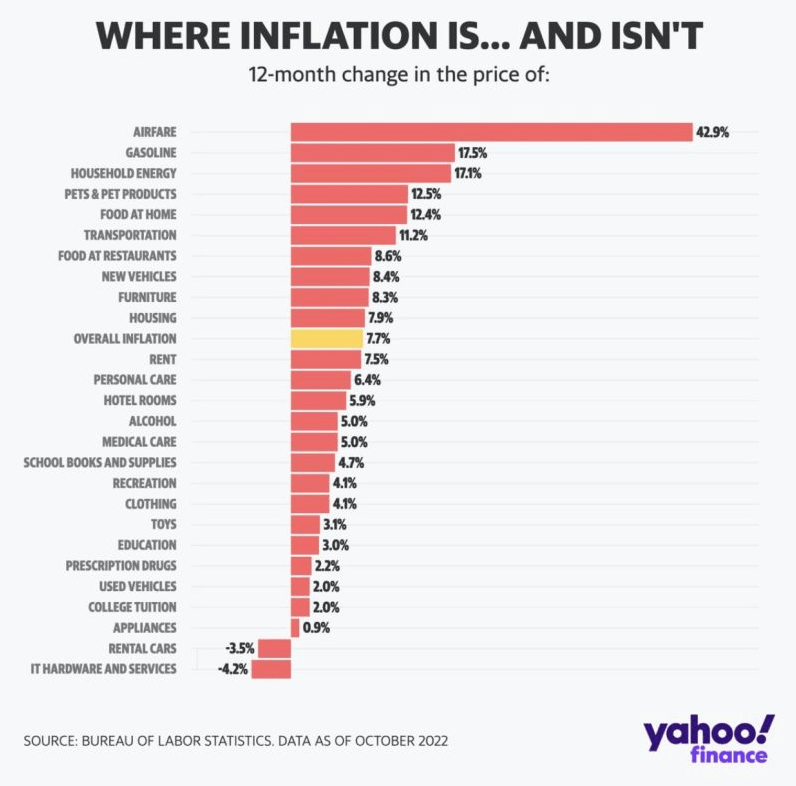

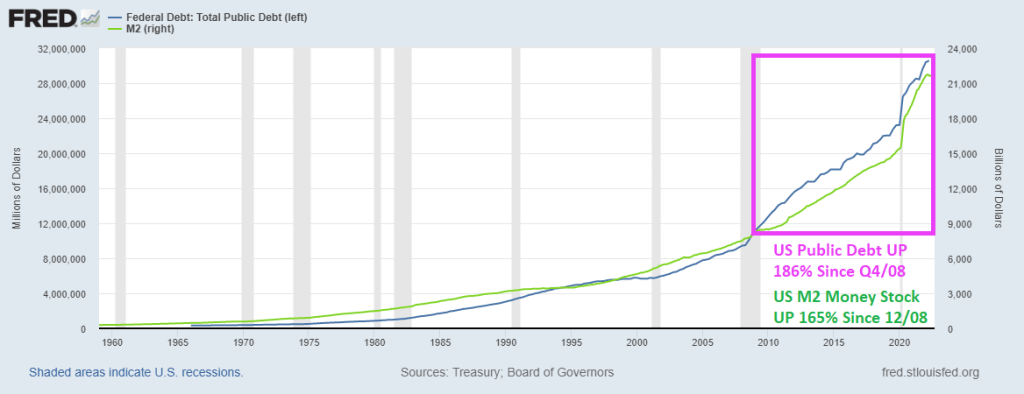

Yes, US public debt has exploded, particularly since the 2008 financial crisis and then again the Covid outbreak of 2020.

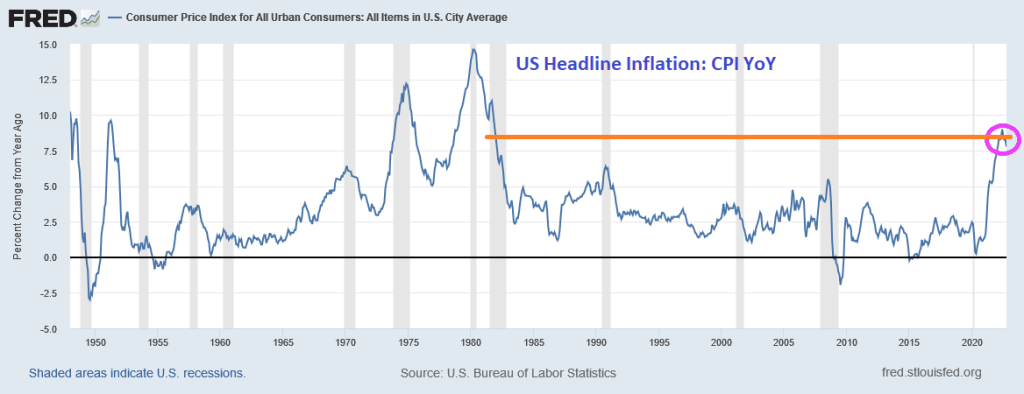

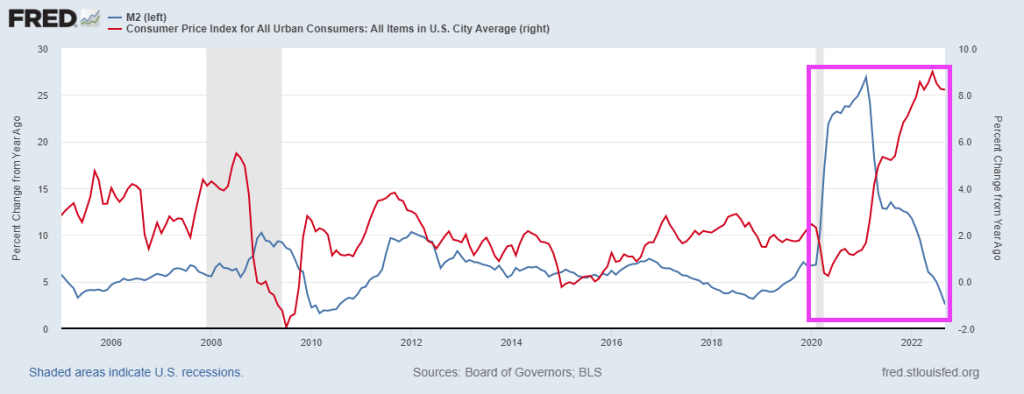

And inflation is near a 40-year high.

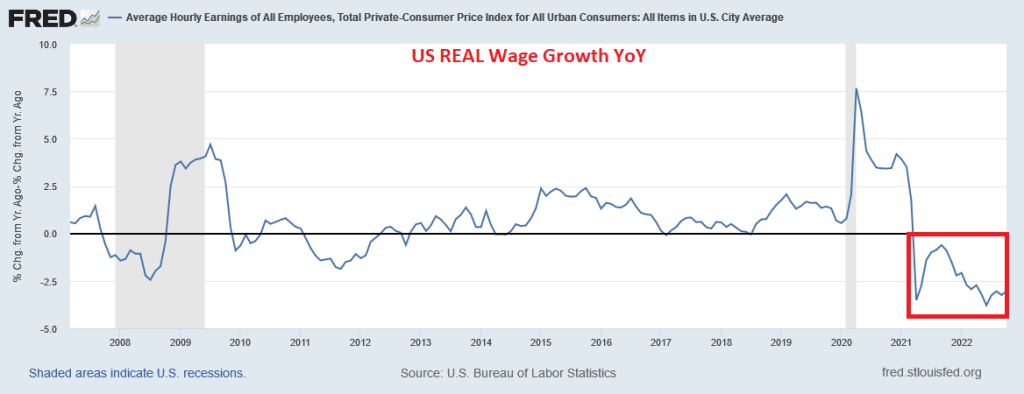

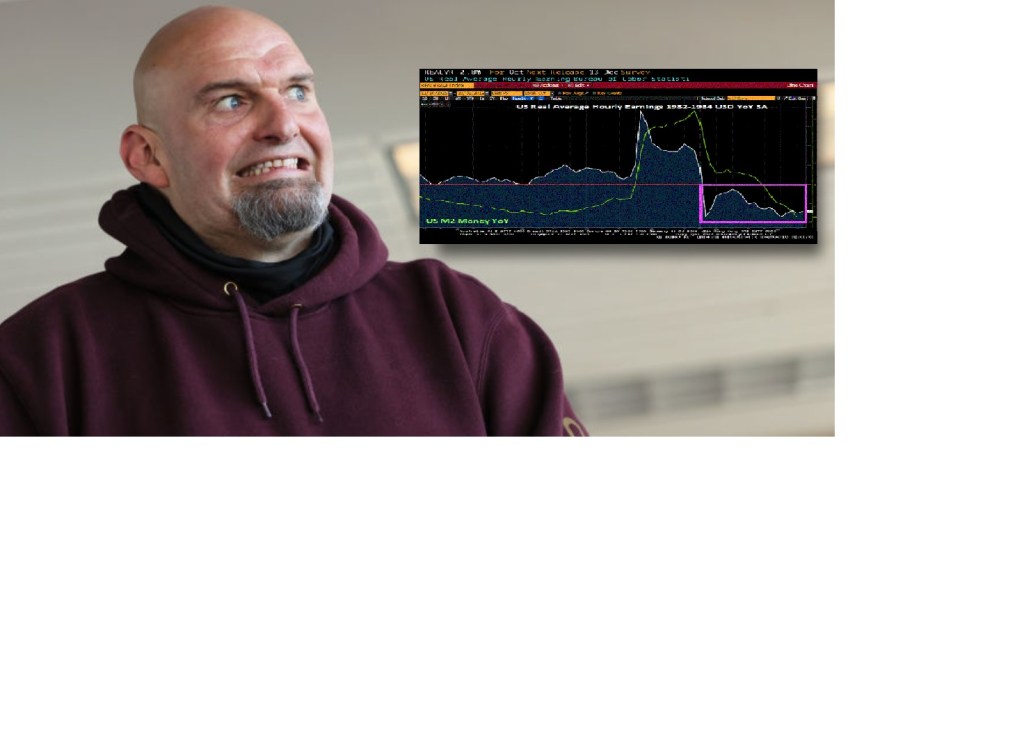

Then we have 19 consecutive months of negative wage growth in the US.

Biden is apparently doubling down on “Green Schemes” now that the US House of Lords (aka, Senate) remain under Keynesian control (aka, Democrat). So watch for inflation to start increasing again.

You must be logged in to post a comment.