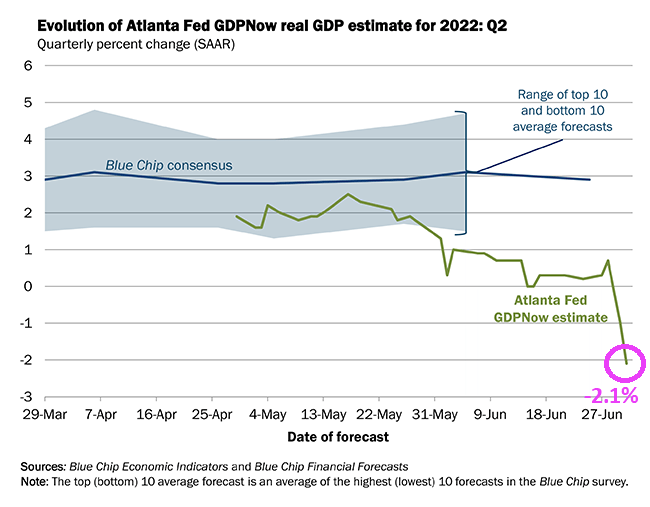

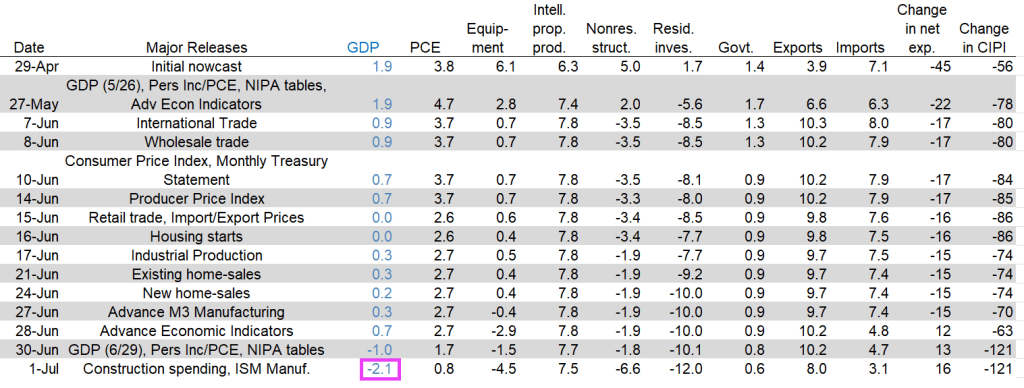

Which is bad news for Biden and Democrats after Q1’s bad GDP report of -1.6% “growth”, we now see the Atlanta Fed’s real-time GDP report for Q2 at -2.1%.

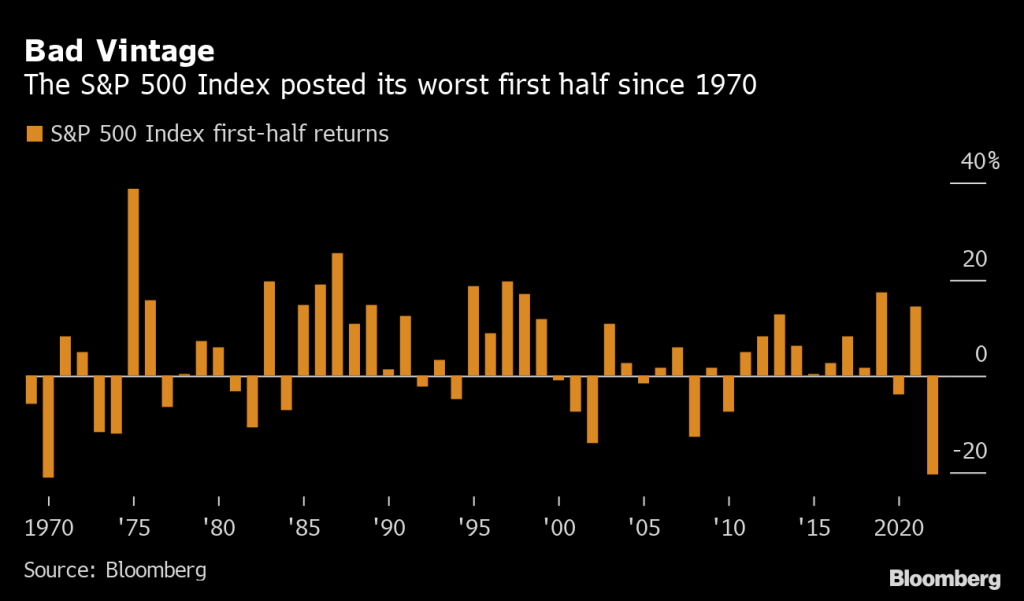

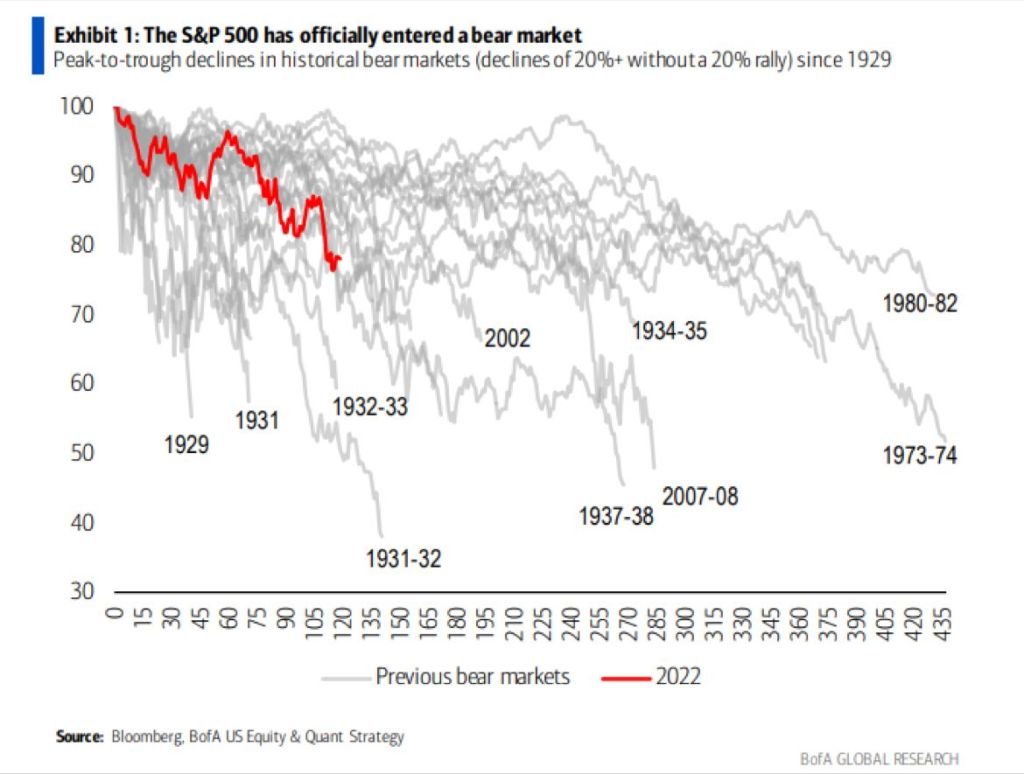

A “recession shock” begins for markets following the worst first-half for the S&P 500 in more than 50 years.

And investors are running to Treasuries for safety as US Treasury 10-year yields tank 14 basis points.

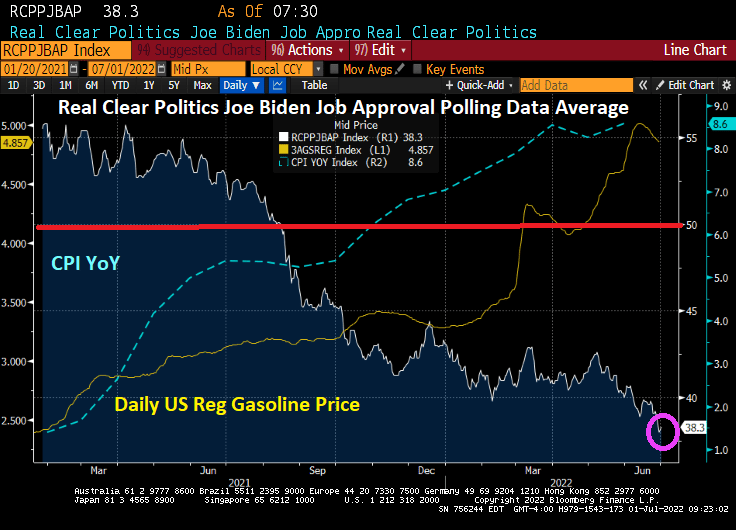

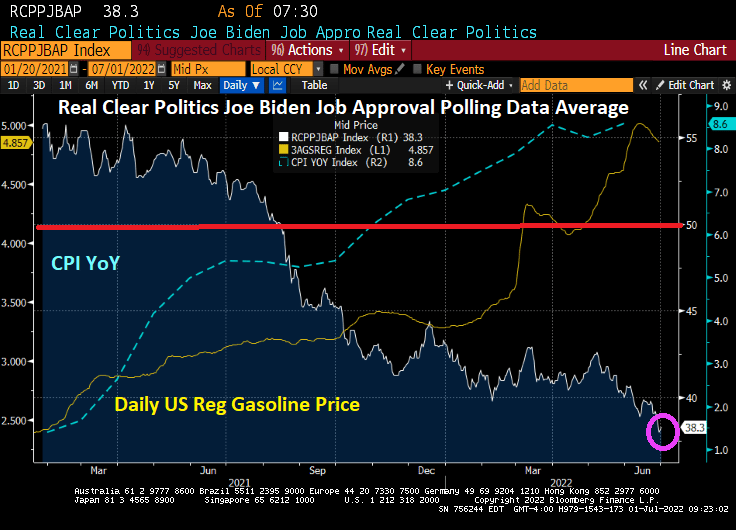

Biden’s approval rating has collapse with inflation and rising gasoline prices. Note that Biden’s approval rating dropped below 50 in mid-August 2021, long before the Russian invasion of Ukraine in late February 2022. Gasoline prices had risen 49% since Biden’s inauguration as President, but before the Russian invasion of Ukraine.

The US economy is slowing as inflation ravages consumers. US Regular Gasoline prices, for example, are up 104% under President Biden which helps to slow the economy.

US personal consumption expenditures fell to +0.2% MoM in May as “inflation” or real personal consumption expenditures PRICES rose +6.3% YoY as The Fed’s balance sheet (aka, Master Blaster!) remains.

As I mentioned above, US regular gasoline prices are UP 103% under President Biden, diesel prices (the cost of shipping goods to markets like … food is up 119% under Biden while CRB foodstuffs is up 55% under China Joe.

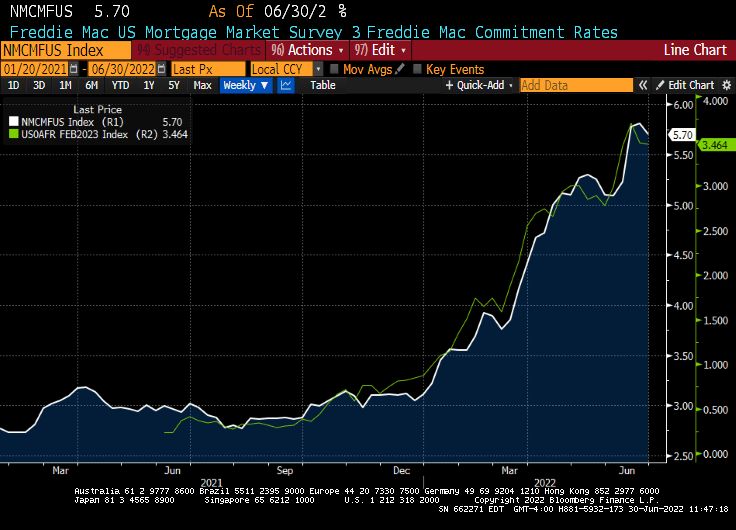

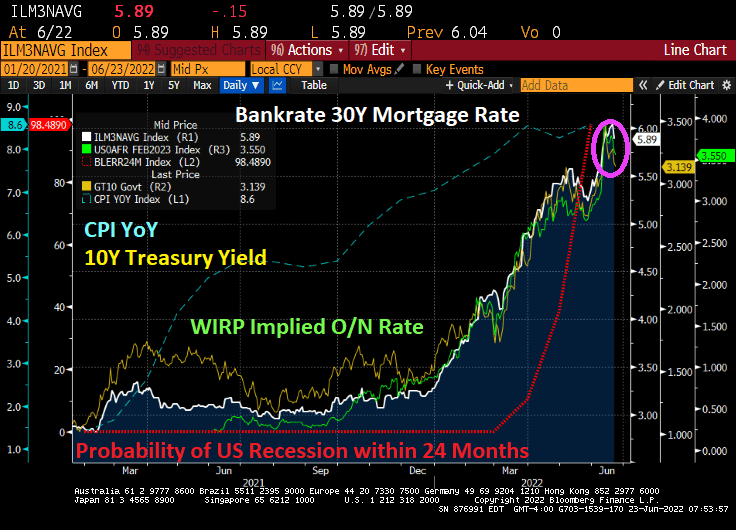

Now we have mortgage rates in the US falling for the first time in four weeks. The average for a 30-year loan was 5.7%, down from 5.81% last week, Freddie Mac said in a statement Thursday.

This year’s Fourth of July celebration is going to cost 18% more than last year’s celebration.

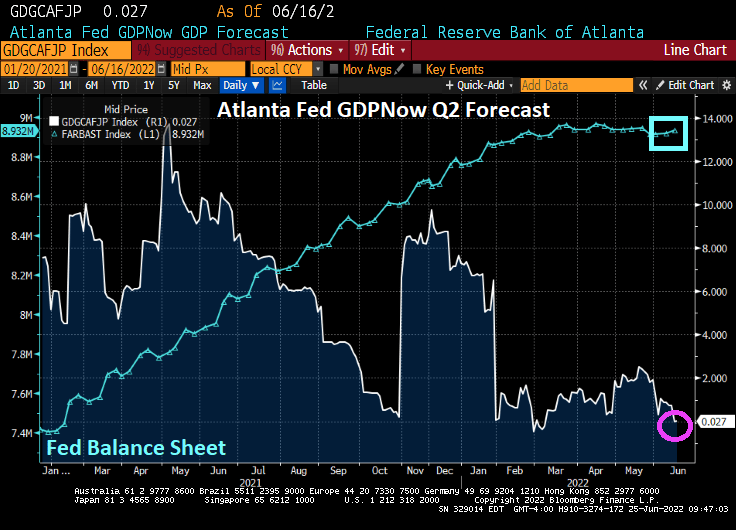

Lastly, the Atlanta Fed GDPNow real time tracker for Q2 is showing … -1% GDP “growth.”

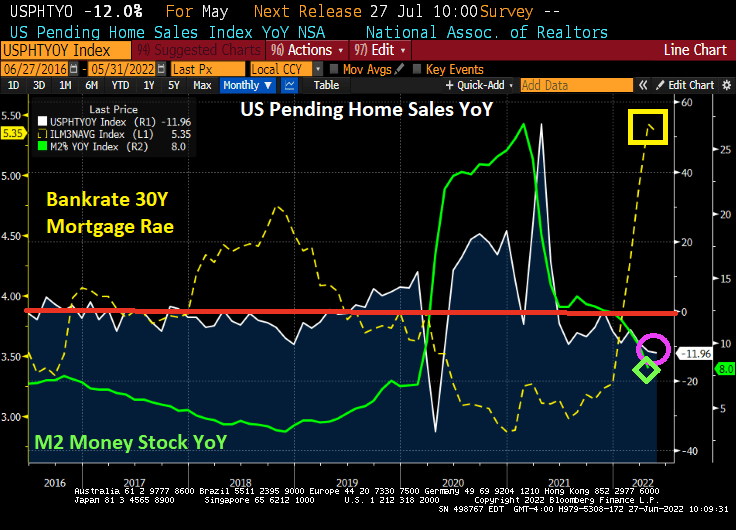

US pending home sales declined -12% YoY in May as The Fed cranked up mortgage rates. That was 11 out of the last 12 months had declining pending home sales.

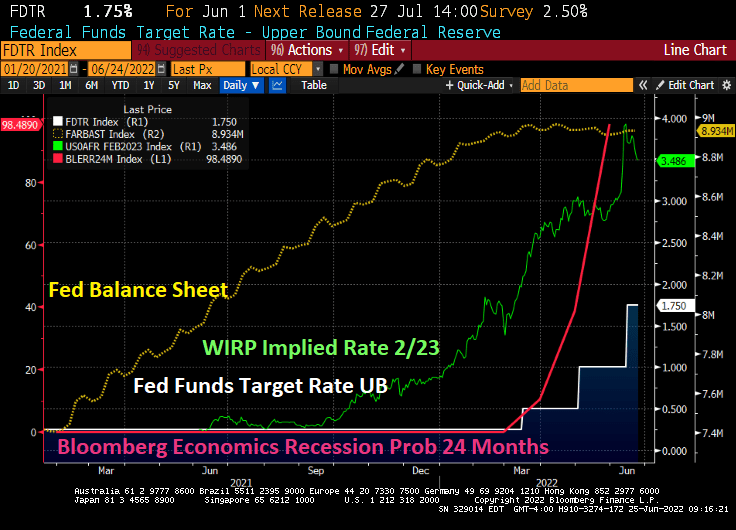

As a recession approaches, we are seeing the WIRP implied Fed o/n rate (green line) declining. And with The Fed chickening-out, we saw a surge in equities (NASDAQ composite index in blue).

Gasoline prices are falling too (orange line), but due to rising global economic slowdown. But notice that The Fed’s balance sheet (yellow line) is still growing despite repeated signals that Covid stimulus would be removed (I call this Quantitative Frightening).

As I mentioned above, The Fed has stopped trimming their balance sheet despite signals to the market of getting rid of the Covid stimulus. As Billy Preston sang, “Nothing From Nothing.”

The Atlanta Fed GDPNow Q2 forecast is for … 0% GDP growth despite the massive monetary stimulus and fiscal stimulus from Biden/Pelosi/Schumer.

And yes, the S&P 500 has officially entered a bear market under the leadership of Joe “The Bear” Biden.

So, Biden’s economic agenda (read, just spend more money and inflation declines?) is failing. Hence, The Fed is backing off a bit helping to drive up stock prices.

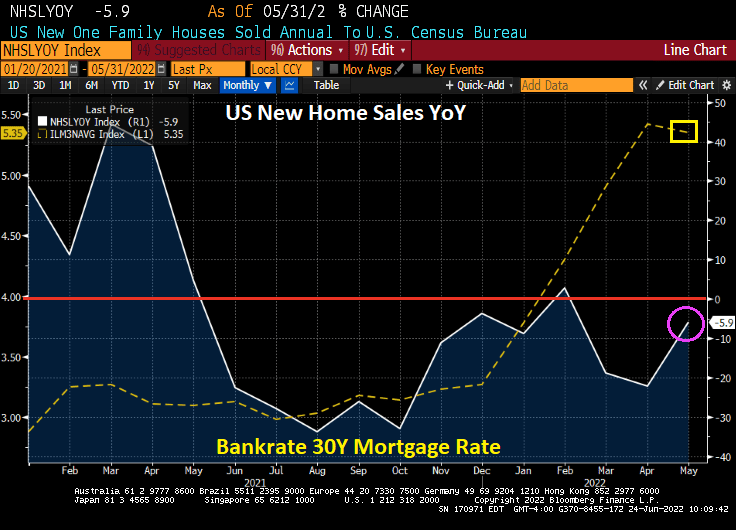

Thanks to massive Fed monetary stimulus still stalking the housing market, US new home sales rose +10.7% MoM (from April to May), but were down -5.9% YoY (from May 2021 to May 2022) as mortgage rates rose.

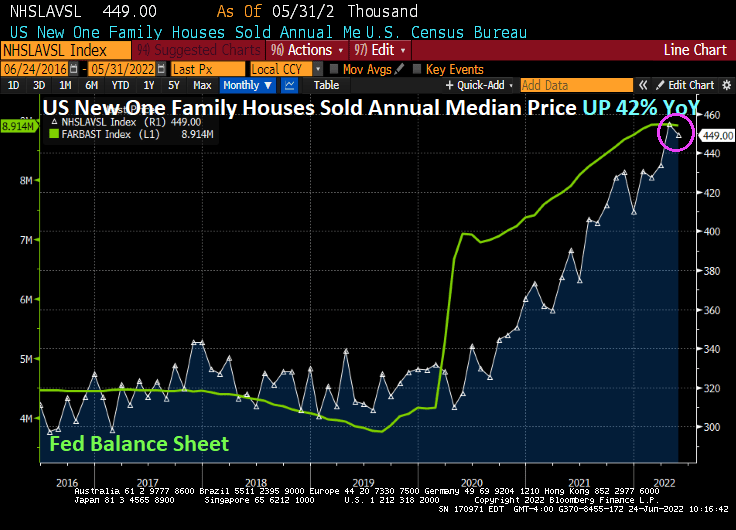

Median price of new home sales rose 42% since May 2021, thanks to Fed stimulypto. And Federal government stimulus spending.

Yes, like the predators from the movies, The Fed’s balance sheet is still stalking markets.

Despite what Biden and his muppets say, there is a good chance that the US will slip into recession over the next 24 months. And with that, we are seeing a slight drop in US mortgage rates.

Inflation is surging, and The Fed seems intent on “inflation fighting” but may have to pause that fight the impending recession. This is called a “U-turn” although Powell didn’t mention that is his testimony yesterday.

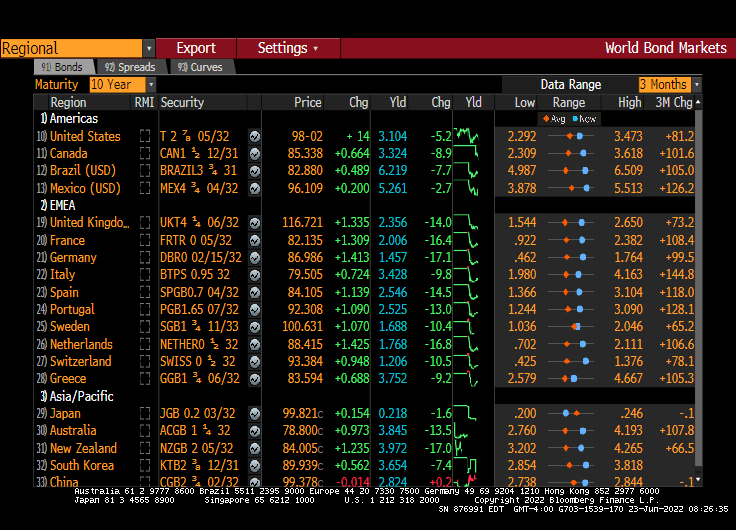

Europe is signaling their u-turn to recession fighting as 10-year sovereign yield have dropped over 10 basis points this morning. Australia and New Zealand are dropping hard as well.

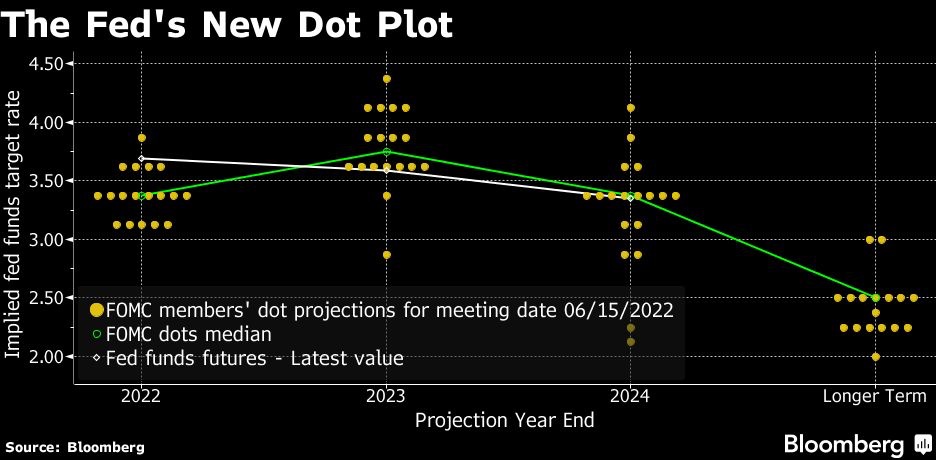

Here is the Federal Reserve’s open market committee deciding on the direction of interest rates … inflation fighting or recession fighting?

Even since the housing bubble burst and ensuing financial crisis on 2007-2008, The Federal Reserve under Ben “The Savior!” Bernanke, Janet Yellen and Jerome Powell let their zero/low interest rate policies be too low for too long that anyone with common sense knew would lead to serious problems when The Fed was forced (this time by inflation) to end the massive OVER monetary stimulus. We are now living through The Great Reset of the US economy.

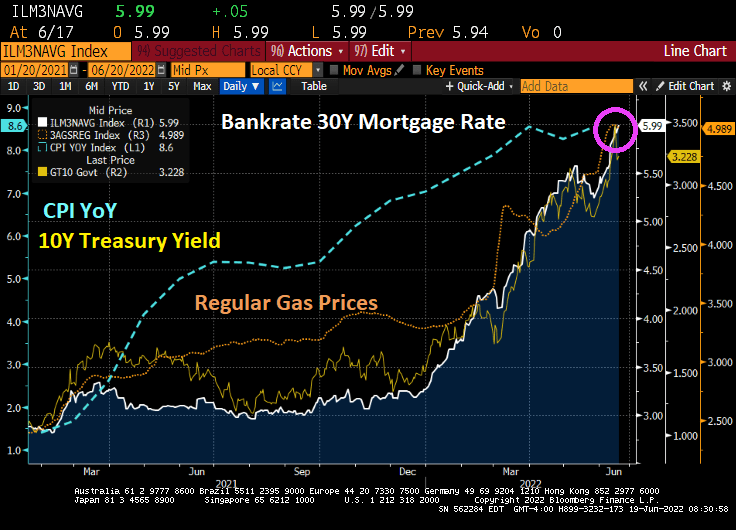

Since Biden was sworn-in as President (or El Presidente) in January 2021, 30-year mortgage rates are up 108% to 6%, regular gasoline prices are up 108% to $5 a gallon nationally. Inflation is up to 8.6% YoY.

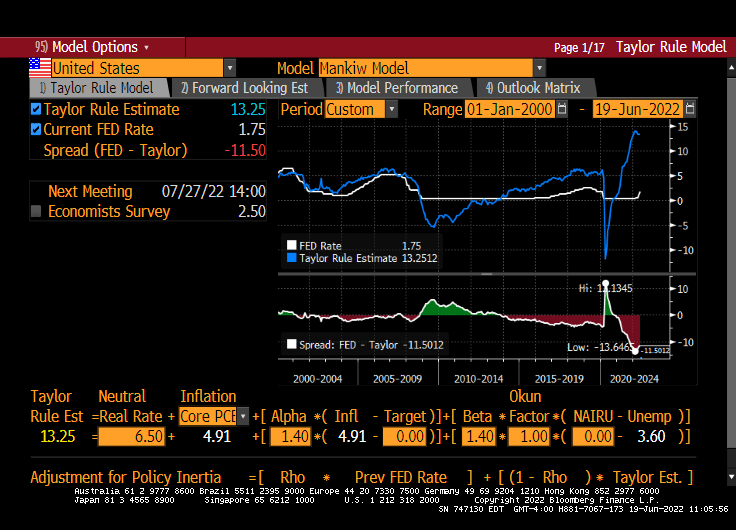

Bernanke, Yellen and Powell did not follow any rule per se, just a “seat of the pants” panic button approach. Using the Mankiw specification of the Taylor Rule model, the Fed Funds target rate should be 13.25% based on CORE PCE. Notice starting in 2014, The TR suggested target rate started to be higher than the actual Fed target rate. And since the Covid monetary blast of 2020, the gap between the Taylor Rule and Fed target rate (red area) has grown to near the highest level in history. Even now Mohamed A. El-Erian, Chief Economic Advisor at Allianz, is starting to admit that The Fed’s ZIRP policies are beginning to hurt.

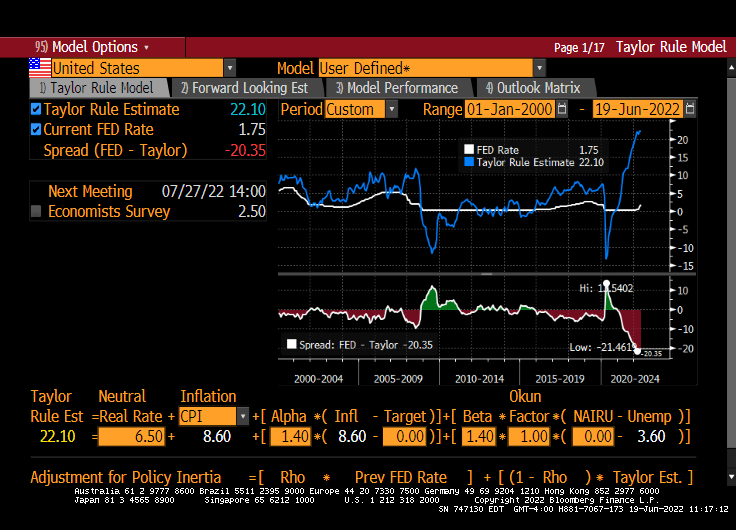

But if we use total inflation rather than core inflation, the measure that picks up the actual pain that Americans are feeling from rising gasoline prices and mortgage rate, we get a Fed Target rate of 22.10%. Since The Fed’s current target rate is only 1.75%, The Fed has “Room To Move.”

And in a painful. bad way.

Bernanke, Yellen and Powell must think that The Taylor Rule is the New Jersey ham pork roll.

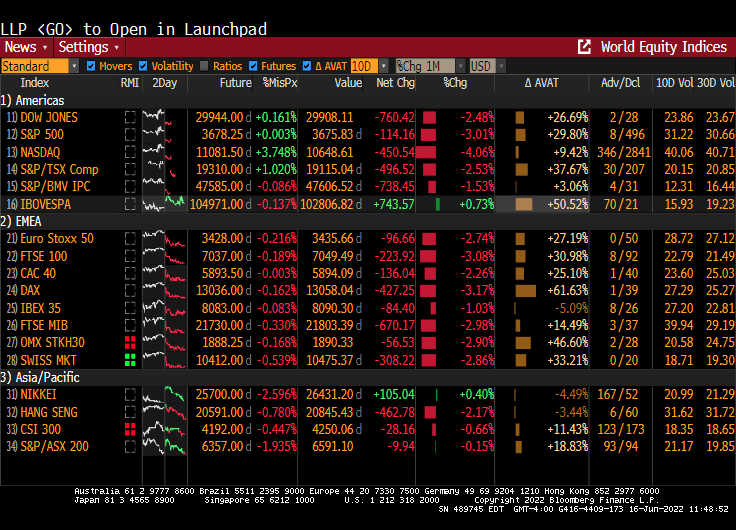

On the heels of The Fed’s 75 basis point surge in the target rate, the US Treasury yield jumped +11.5 BPS as of 8:30 AM EST. The S&P 500 E-mini futures contract is down -1.8%.

As investors brace for a recession, mortgage rates dropped to 6.03%.

Gasoline prices remain near $5 per gallon, diesel prices are near $6 per gallon and The Fed’s massive balance sheet is still in force.

On the housing front, US housing starts plunged -14.4% MoM in May, the biggest decline under Biden.

While housing starts were down -14.4% MoM in May, single-family detached home were down only -9.16%. It was 5+ unit (multifamily) starts that were down -26.83% MoM.

Good morning peeps! Reality is dawning after the market surge yesterday after investors celebrated that The Fed could have raised rates even more.

You must be logged in to post a comment.