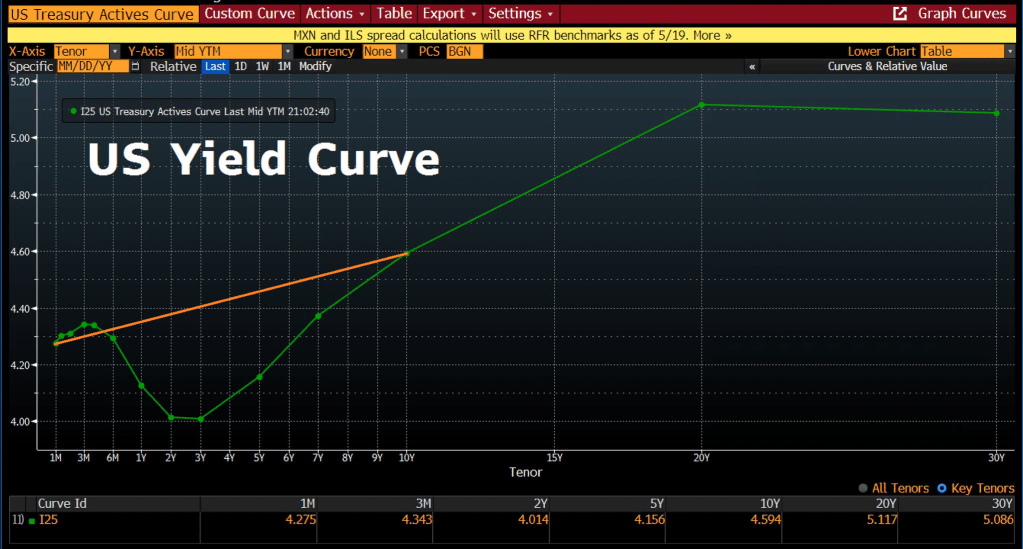

US 30y bond yields are heading toward their highest level since 2007.

The yield curve has finally normalized!

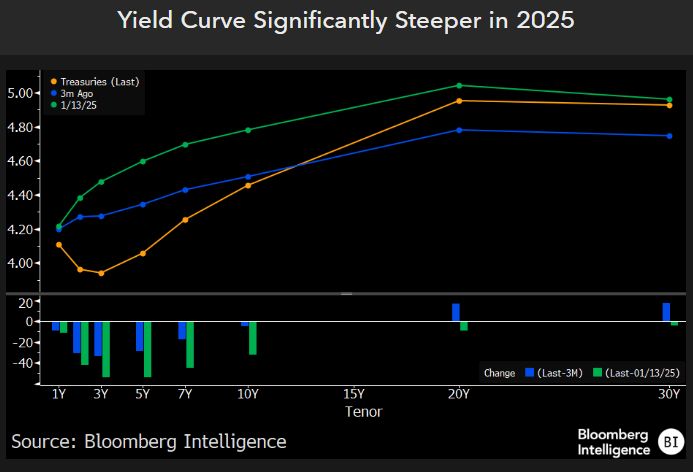

And significantly steeper in 2025.

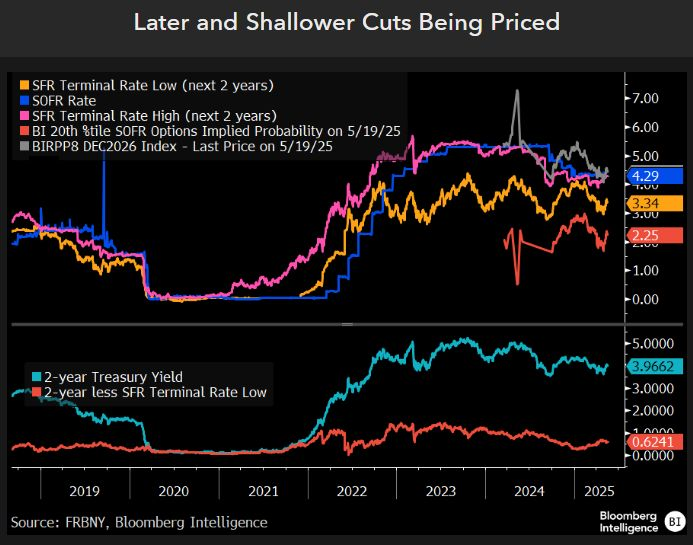

Later and shallower rate cuts are being priced.

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

US 30y bond yields are heading toward their highest level since 2007.

The yield curve has finally normalized!

And significantly steeper in 2025.

Later and shallower rate cuts are being priced.

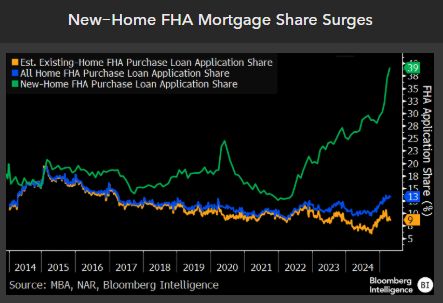

The not shocking news out of DC: The ‘Big, Beautiful Bill’ Will “Massively” Increase Near-Term Deficits, Add $5 Trillion In Debt. The surprising news? New home FHA Mortgage Share has surged!

On the not surprising news front: FHA debt-to-income ratios have surged (the surge started under Biden).

New-home loan sizes have fallen to 2021 levels.

Now you know why Trump is so eager to cut wasteful spending! The real mystery is why Democrats and RINOs are so determined to continue wasteful spending and not cut taxes.

Trump inherited a fiscal disaster from Biden and Congress. Not to mention The Federal Reserve. Credit default swaps (CDS) for the USA are near Greece (and China) levels.

Since Covid struck in 2020, US debt is up a staggering 56%!

And M2 Money is up 40% since Covid.

Opa! Our country is on fire!

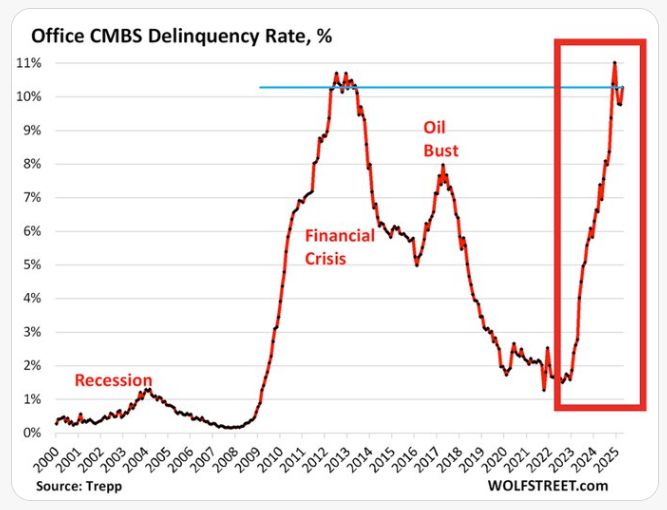

The delinquency rate on US commercial mortgage-backed securities (CMBS) for offices SURGED to 10.3% in April, near the highest EVER.

Moreover, the multifamily delinquency rate spiked 113bps in April, to 6.57%, the highest since 2015.

The Fed can help, but won’t. We are still struggling to recover from Biden’s cockeyed management of the economy,

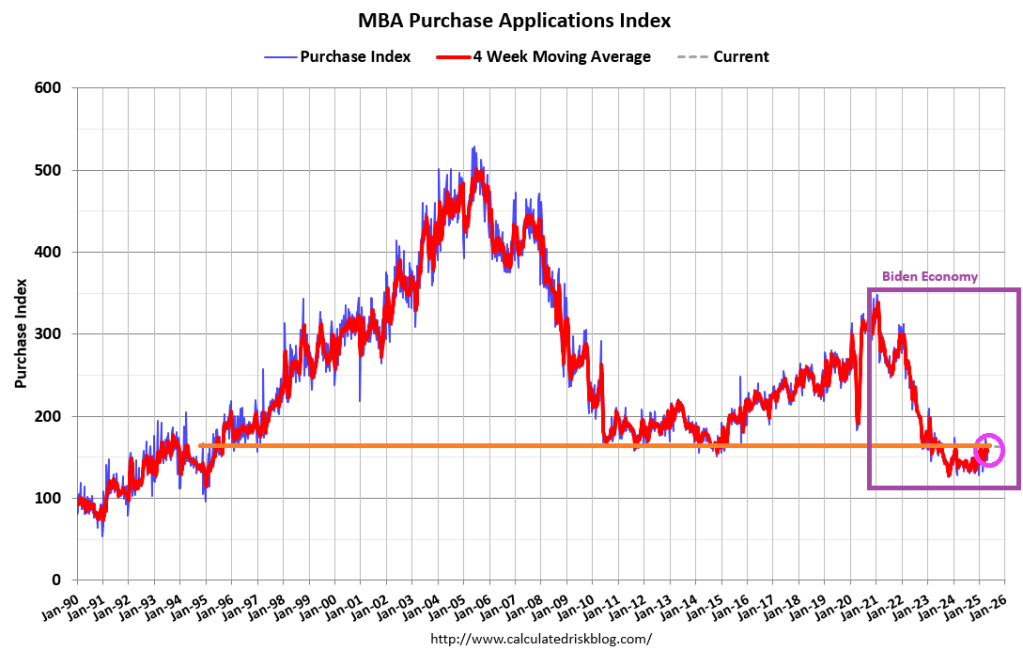

Mortgage applications increased 11.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending May 2, 2025.

The Market Composite Index, a measure of mortgage loan application volume, increased 11.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 12 percent compared with the previous week. The seasonally adjusted Purchase Index increased 11 percent from one week earlier. The unadjusted Purchase Index increased 12 percent compared with the previous week and was 13 percent higher than the same week one year ago.

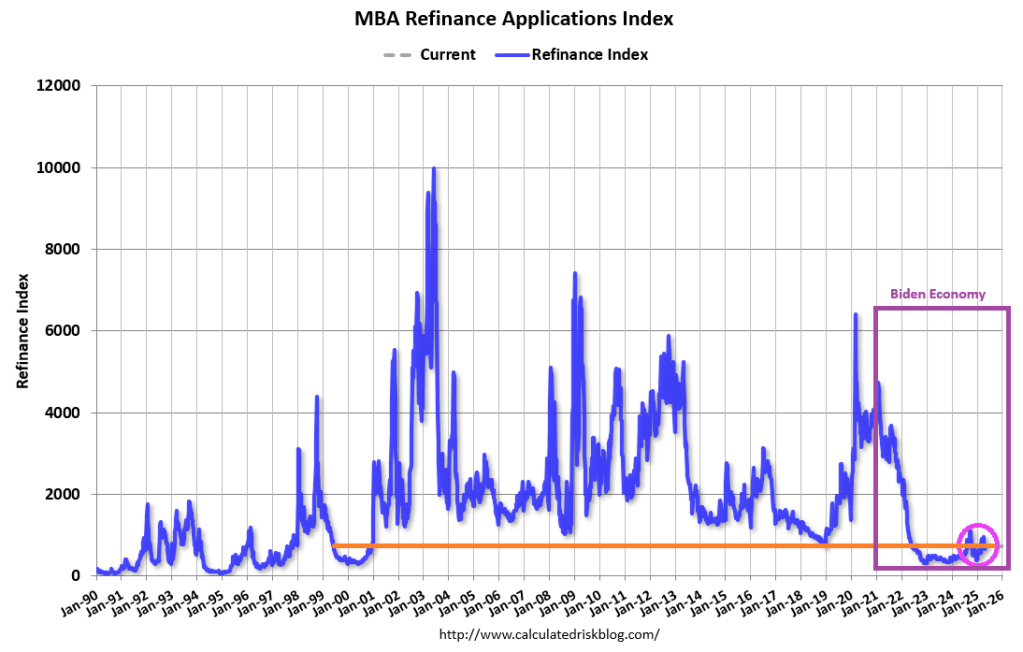

The Refinance Index increased 11 percent from the previous week and was 51 percent higher than the same week one year ago.

The economic news last week included a negative reading for first-quarter GDP growth and further signs of contraction in the manufacturing sector, mixed with a solid employment report for April. The net impact on mortgage rates was mostly downward but just back to levels from early April. The 30-year fixed rate declined to 6.84 percent.

But there will be no rate cuts today from The Fed.

The April Jobs report blew away the tariff crash hysteria. 177k jobs were added, far better than the doomsayers predicted. Even better, more jobs went to native-born workers than foreign-born workers. Even better still, Federal jobs decreased (thanks to Doge).

The US labor market under the Biden administration “grew” almost entirely on the back of “foreign-born” workers, who – as we also first revealed and eventually was widely accepted – were primarily illegal aliens. But in April, we saw a reversal with native-born workers growing and foreign-born workers declining.

And Federal workers continue to decline.

The good news? The Fed will likely not change rates at the next meeting.

I hope the good news on employment continues!

Republicans are trying to lock in Trump’s tax cuts and Democrats are resisting. We now know that DOGE is trying to end the wasteful spending in DC. But I would really like to see tax rates on the middle class fall.

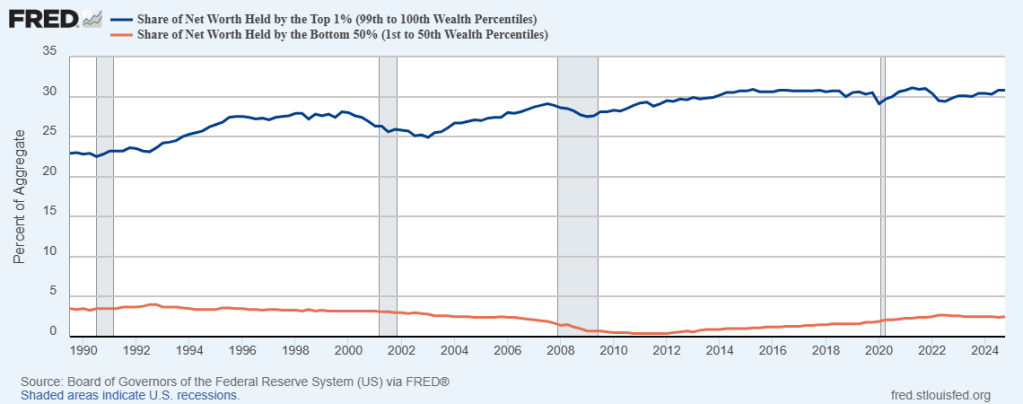

The wealth gap between the top 1% of taxpayers and the bottom 50% of taxpayers is enormous. And has gotten worse since 1990.

Meanwhile. to fight off the temporary effects of the tariff war, Trump is urging Fed Chair Powell to cut rates.

Powell will likely NOT cut rates. But what does “Lunatic Liz” Warren say about rate cuts??

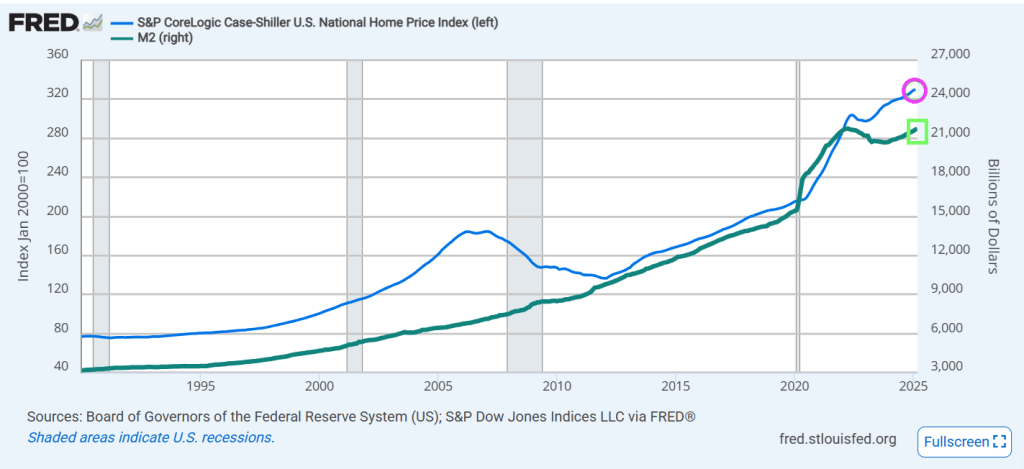

US home prices hit a new record high in February, according to the latest data from S&P CoreLogic Case-Shiller, rising 0.4% MoM (as expected). However, the pace of price rises did slow modestly (after accelerating for the past three months) to +4.50% YoY. And home prices track Fed money printing.

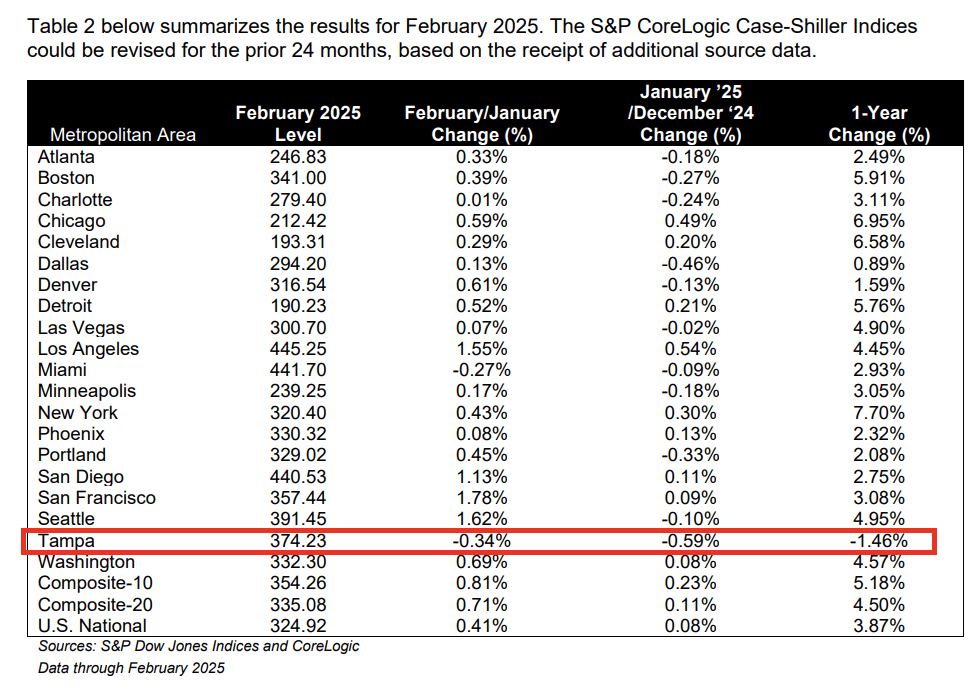

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 3.9% annual return for February, down from a 4.1% annual gain in the previous month. The 10-City Composite saw an annual increase of 5.2%, down from a 5.4% annual increase in the previous month. The 20-City Composite posted a year-over-year increase of 4.5%, down from a 4.7% increase in the previous month. New York again reported the highest annual gain among the 20 cities with a 7.7% increase in February, followed by Chicago and Cleveland with annual increases of 7.0% and 6.6%, respectively. Tampa posted the lowest return, falling 1.5%.

The pre-seasonally adjusted U.S. National, 10-City Composite, and 20-City Composite Indices presented slight upward trends in February, posting 0.4%, 0.8%, and 0.7% respectively.

After seasonal adjustment, the 10-City and 20-City Composite Indices posted month-over-month increases of 0.5% and 0.4%. The U.S. National Composite Index posted a month-over-month increase of 0.3%.

“Even with mortgage rates remaining in the mid-6% range and affordability challenges lingering, home prices have shown notable resilience,” said Nicholas Godec, CFA, CAIA, CIPM, Head of Fixed Income Tradables & Commodities at S&P Dow Jones Indices. “Buyer demand has certainly cooled compared to the frenzied pace of prior years, but limited housing supply continues to underpin prices in most markets. Rather than broad declines, we are seeing a slower, more sustainable pace of price growth.”

Washington DC is loaded with good ol’ boys. Willing to cut deals with anyone for a slice of financial pie. Like “10% For The Big Guy” Joe Biden.

Money flowing into Treasury funds hit its highest since 2017, by far.

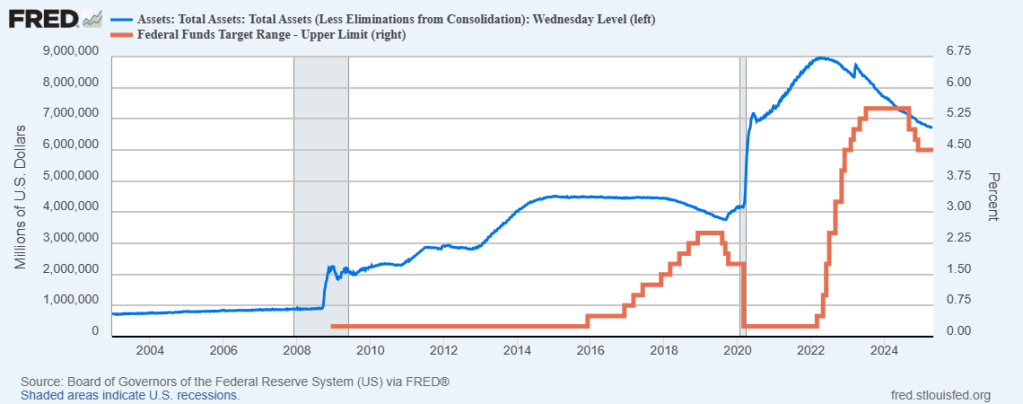

And with the massive expansion of The Fed’s balance sheet with a) the financial crisis and b) Covid crisis, The Fed still has a staggering amount of bonds on its balance sheet, making it vulnerable to interest rate increases.

Like what has happened in 2023 and 2024 under Biden. A fine mess!

Sail away. We are all prisoners of the theft by DC politicians.

Fed Chair Jerome Powell is apparently waiting for the tariff “war” to settle down before he pushes for interest rate cuts. Meanwhile, rising mortgage rates are hurting consumers and the mortgage industry.

Mortgage applications decreased 12.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending April 18, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 12.7 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 11 percent compared with the previous week. The seasonally adjusted Purchase Index decreased 7 percent from one week earlier. The unadjusted Purchase Index decreased 6 percent compared with the previous week and was 6 percent higher than the same week one year ago.

The Refinance Index decreased 20 percent from the previous week and was 43 percent higher than the same week one year ago.

Overall mortgage application activity declined last week, as rates increased to their highest level in two months. The 30-year fixed rate rose for the second straight week to 6.9 percent, an almost 30-basis-point increase over two weeks.

The 10Y-2Y Treasury yield curve is steepening.

Fed Chair Jerome Powell. Nyuk, Nyuk, Nyuk!

You must be logged in to post a comment.