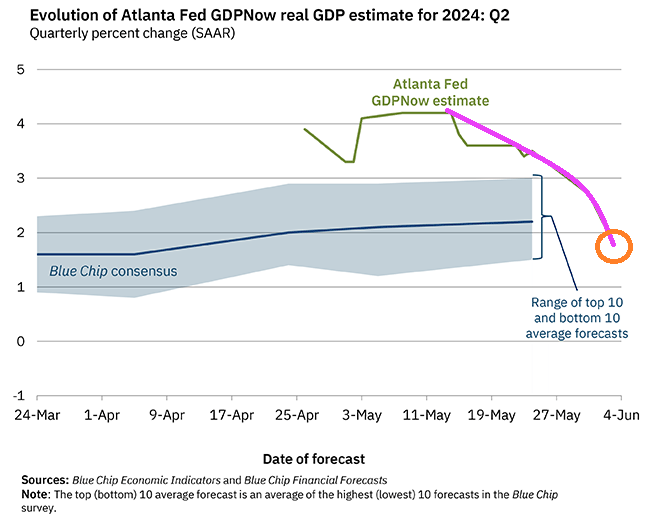

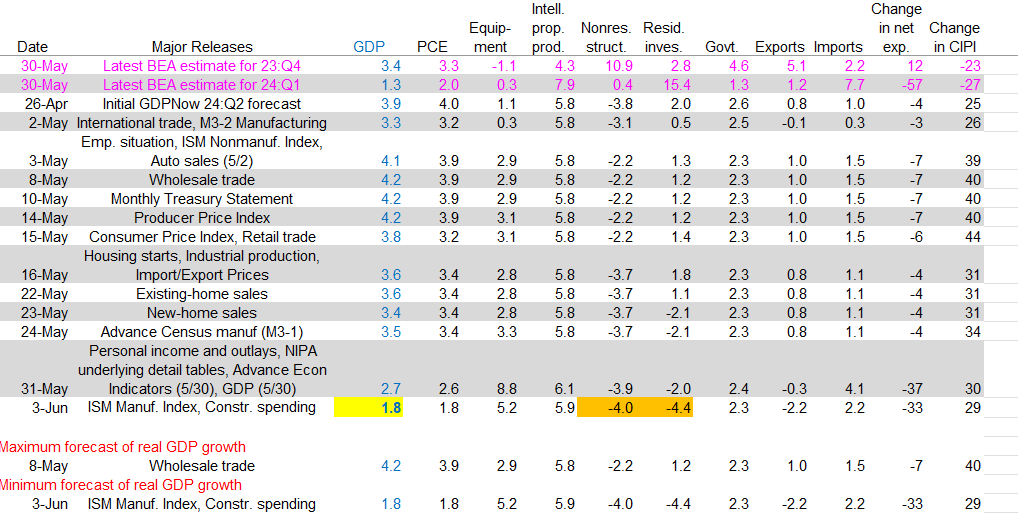

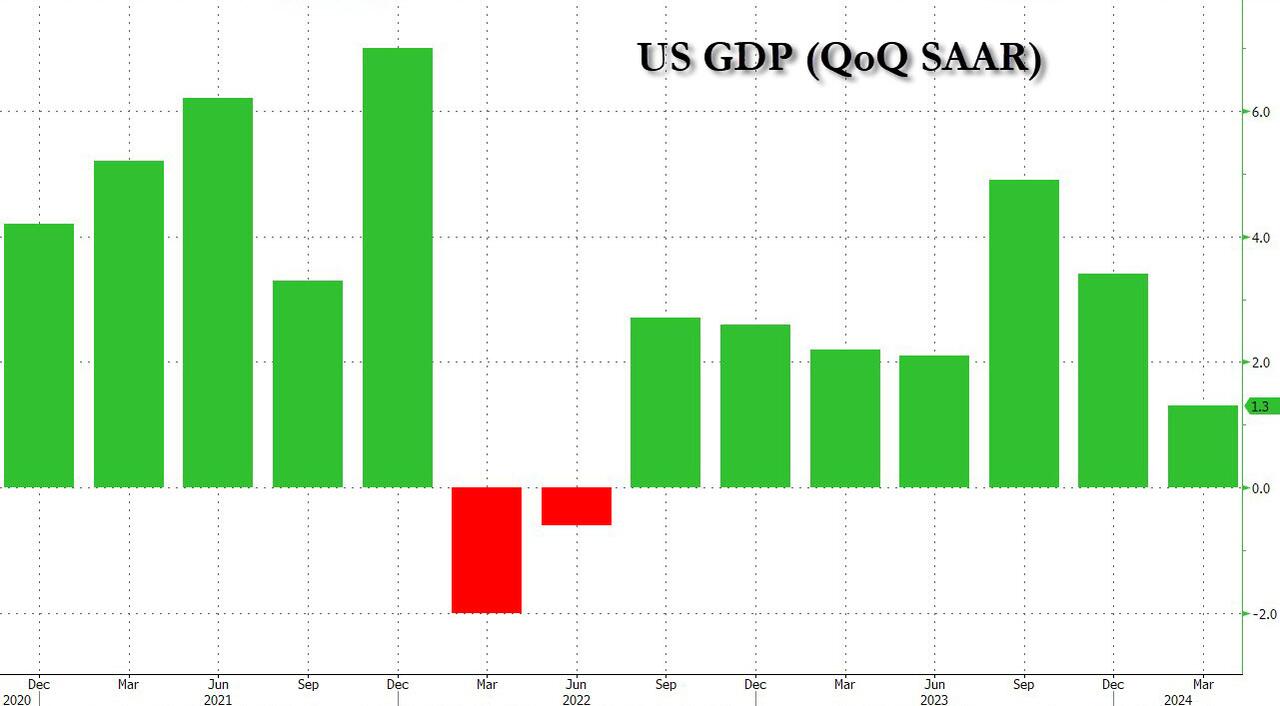

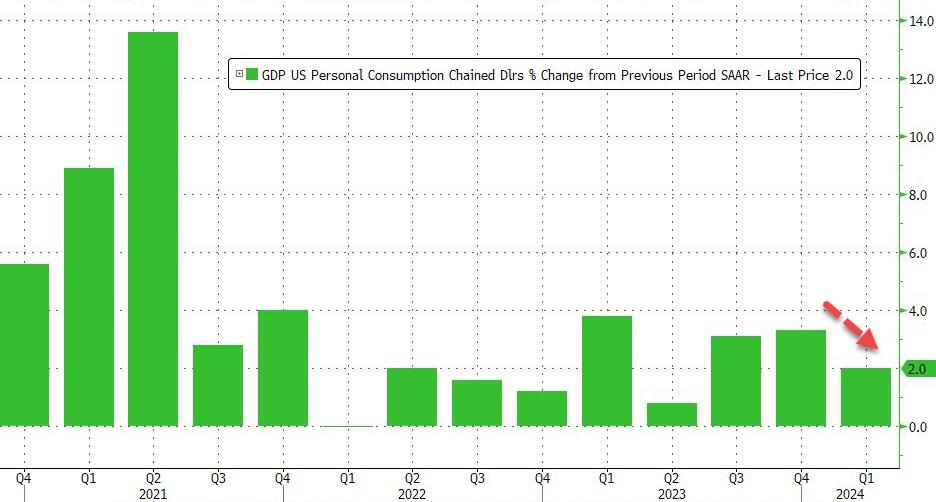

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2024 is 1.8 percent on June 3, down from 2.7 percent on May 31. After recent releases from the US Census Bureau and the Institute for Supply Management, the nowcasts for annualized second-quarter real personal consumption expenditures growth and real private fixed investment growth declined from 2.6 percent and 3.1 percent, respectively, to 1.8 percent and 1.5 percent.

fff

Since I used The Animal’s version of the John Lee Hooker great tune “Boom Boom,” I will use another Animals tune for Joe Biden’s penchant for sniffing little girls. “Baby Let Me Take You Home.”

The Animals band. Not to be confused with the animals in the Biden Administration and Congress.

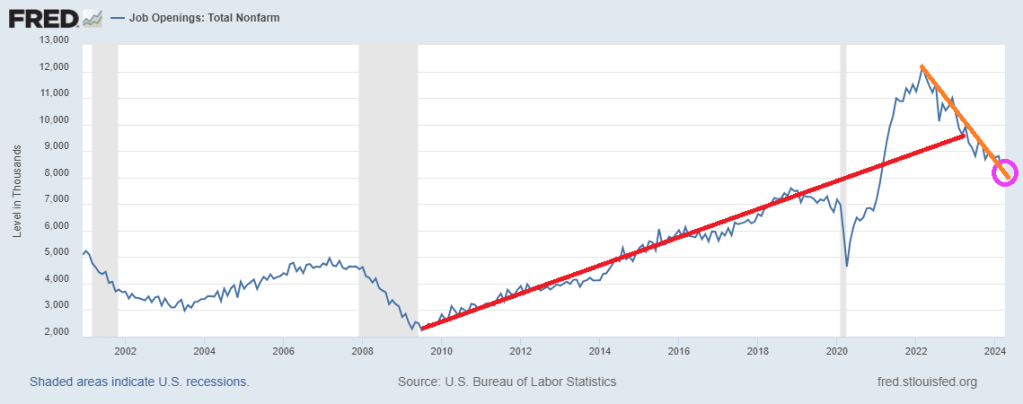

Job openings in April 2024 dipped to 8,059. Notice the trend (orange line) is below the trend set prior to Covid (red line).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.