The last US debt crisis occured in 2013 when Congress finally raised the debt ceiling … and kept on borrowing and spending, But if you thought that a debt crisis would scare Congress (and the Administration) into balancing the Federal budget, you would be wrong. In fact, since the 2013 debt crisis, Federal debt is up 88% (+$14.7 TRILLION over the last 10 years).

And with the massive growth in Federal debt under Obama, Trump and Biden has resulted in an explosion in interest payments on the Federal debt.

And with $182 TRILLION in UNFUNDED liabilities, the debt issuance won’t stop.

Let’s see what is in Treasury Secretary Janet Yellen’s bag of tricks.

LIBOR cracked 5% for first time since 2007.

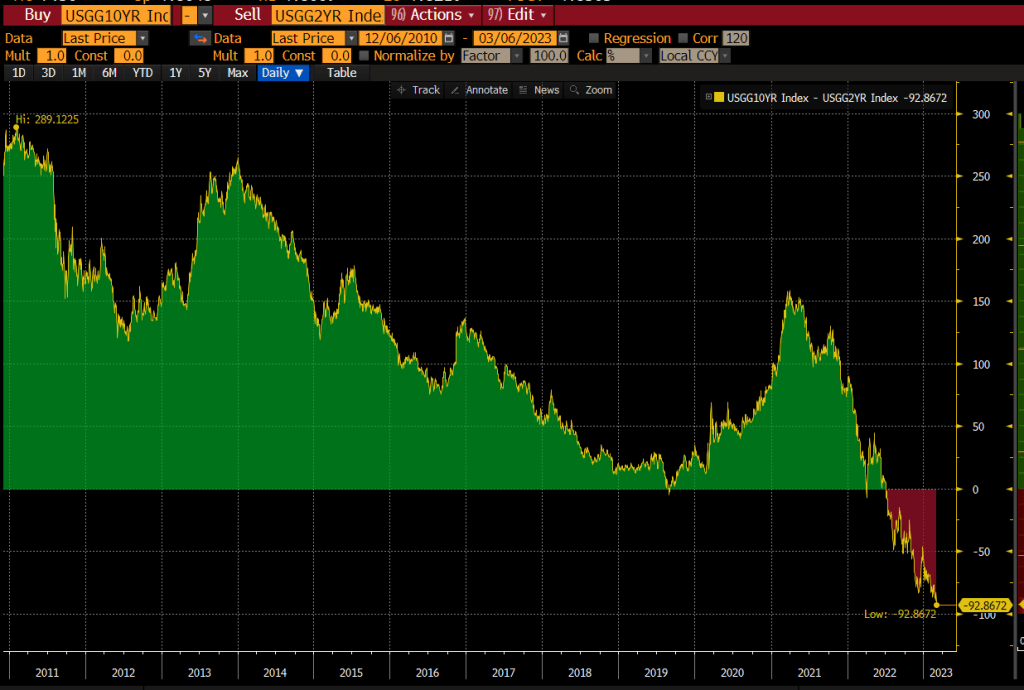

And the US Treasury 10Y-2Y yield curve is the most inverted since 1981.

Is Janet Yellen the “evil woman” from Crow’s song?

You must be logged in to post a comment.