Up, up and away in our inflationary balloon!

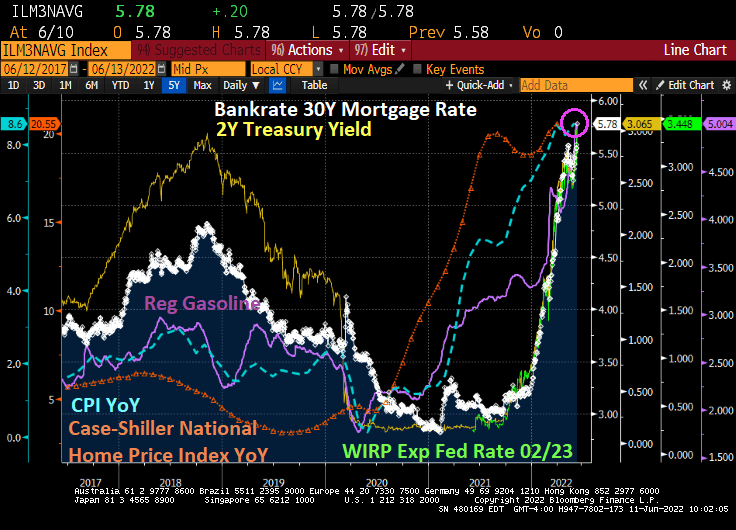

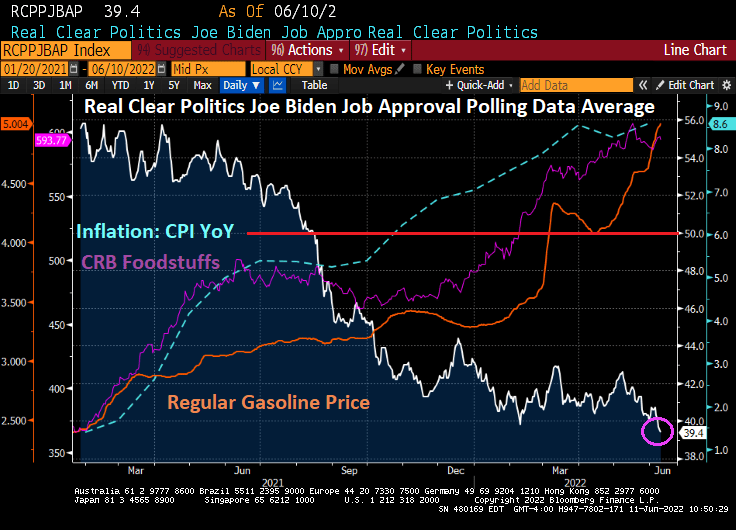

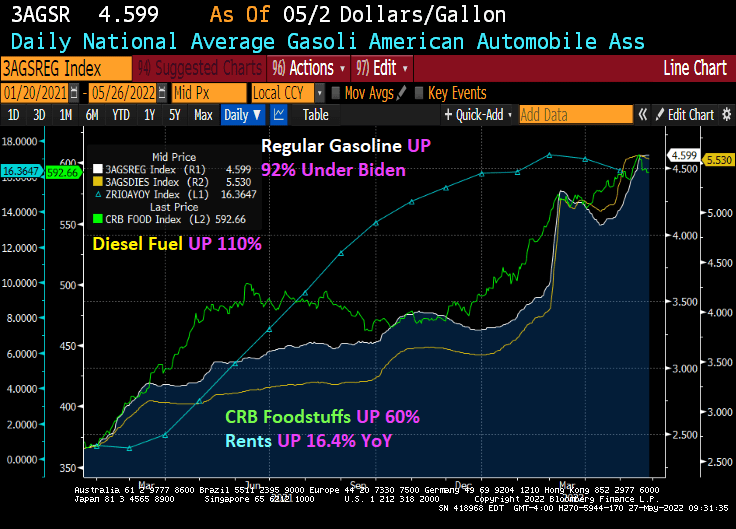

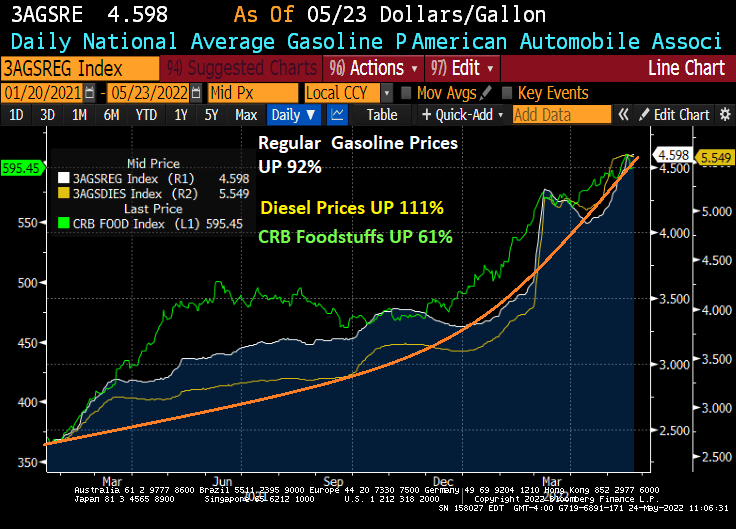

Regular gasoline prices have breached the $5 a gallon barrier, the highest in recorded history. And it is even worse in states like California where regular gas prices have been above $7 per gallon.

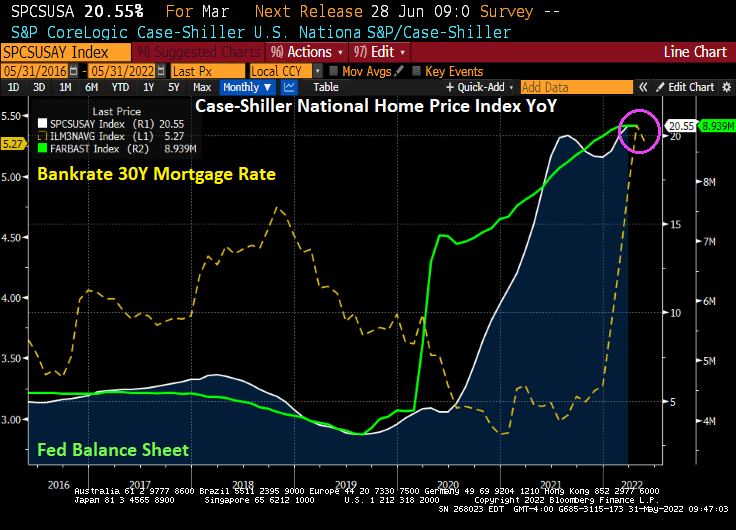

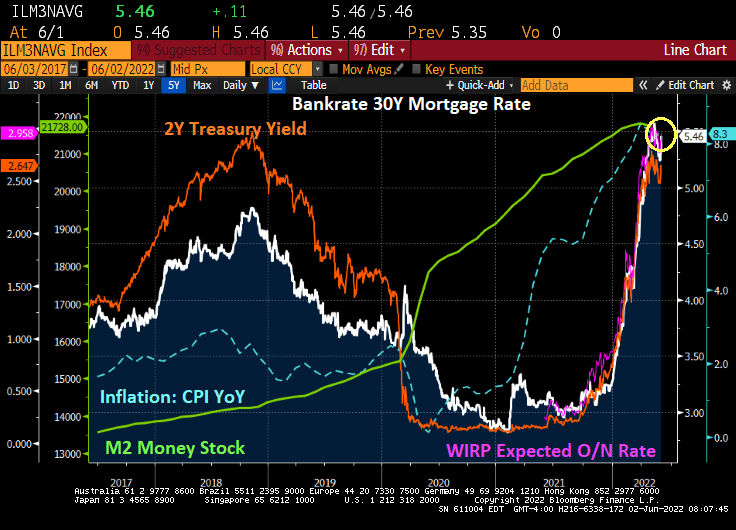

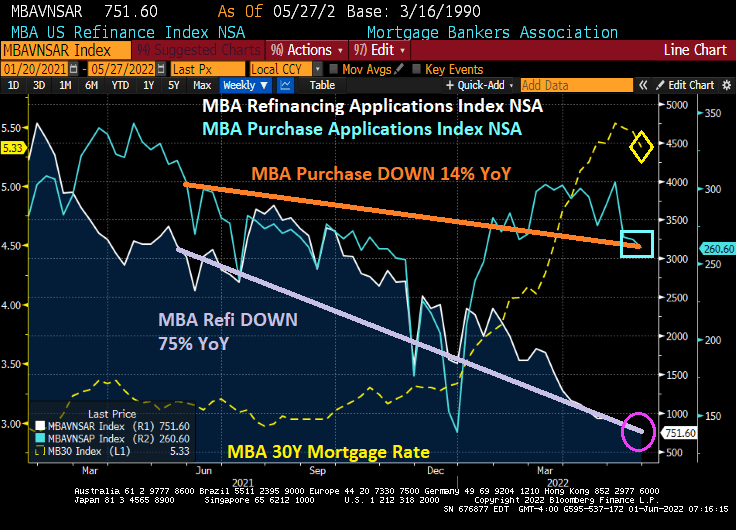

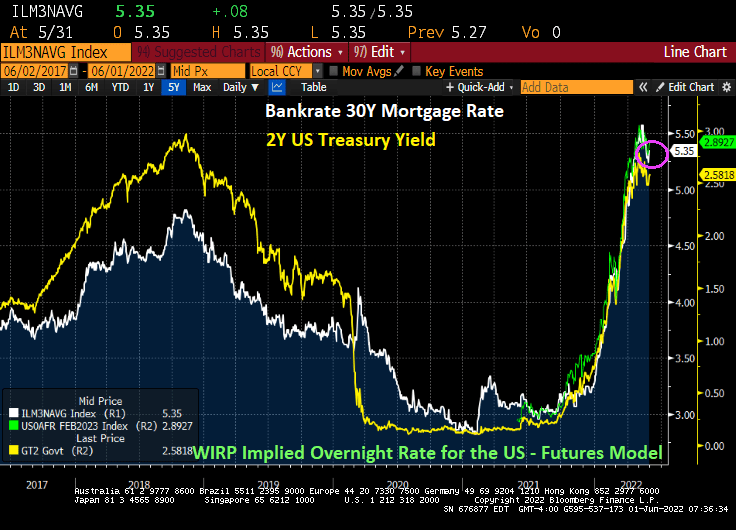

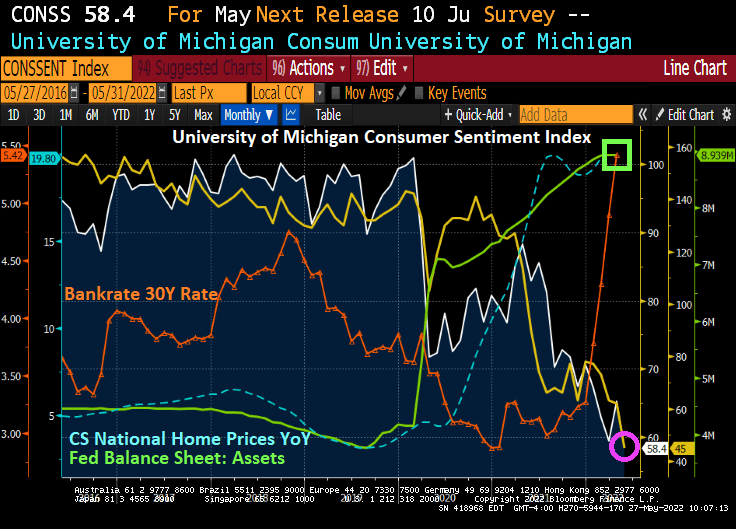

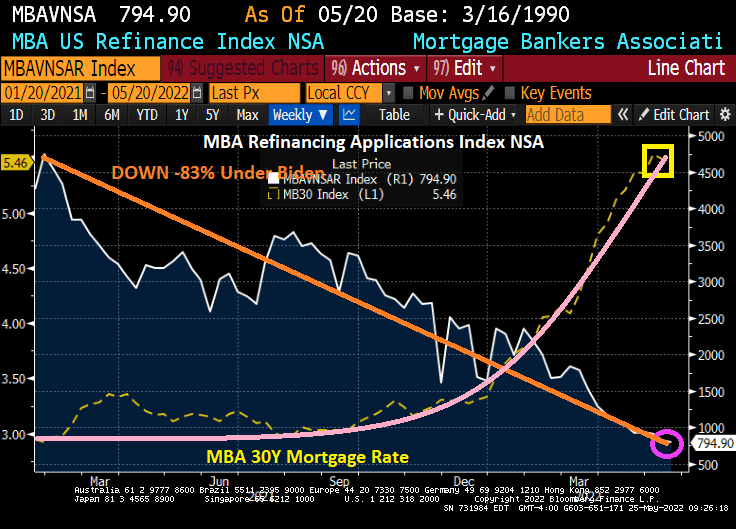

Bankrate’s 30-year mortgage rate is now 5.78%, the highest since 2008. And rising really fast as The Fed tightens the monetary noose.

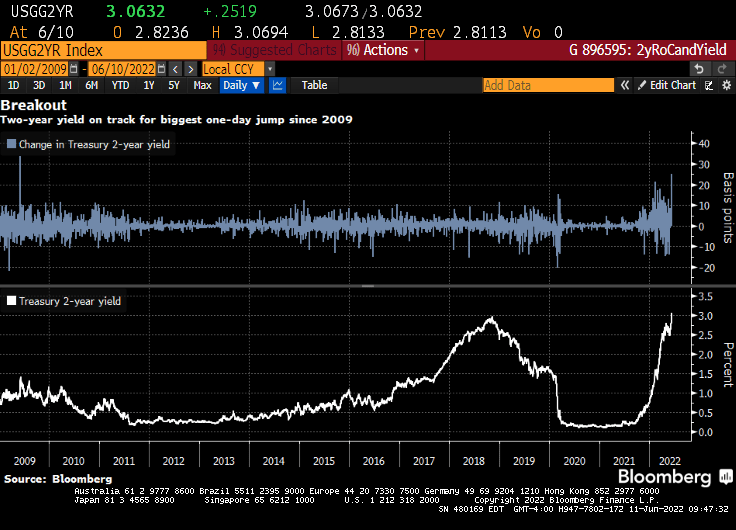

Speaking of noose tightening, the 2-year US Treasury Note yield is rising awfully fast.

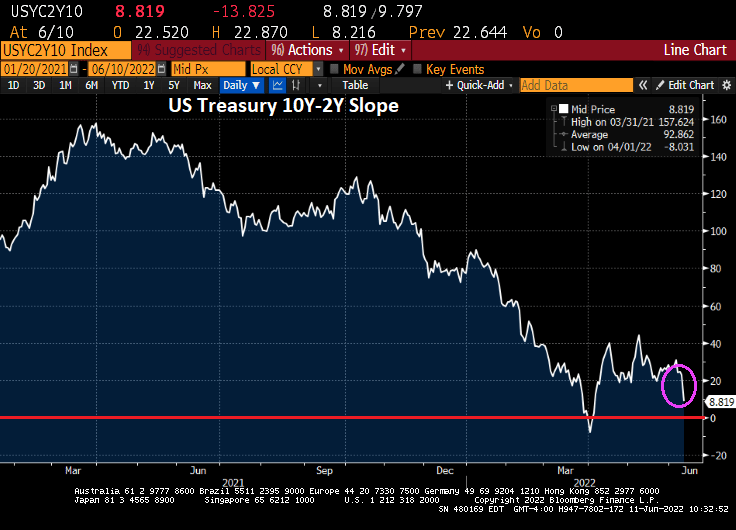

The US Treasury 10Y-2Y curve slope just flattened to 8.819 bps and challenging the 0% grade awfully fast.

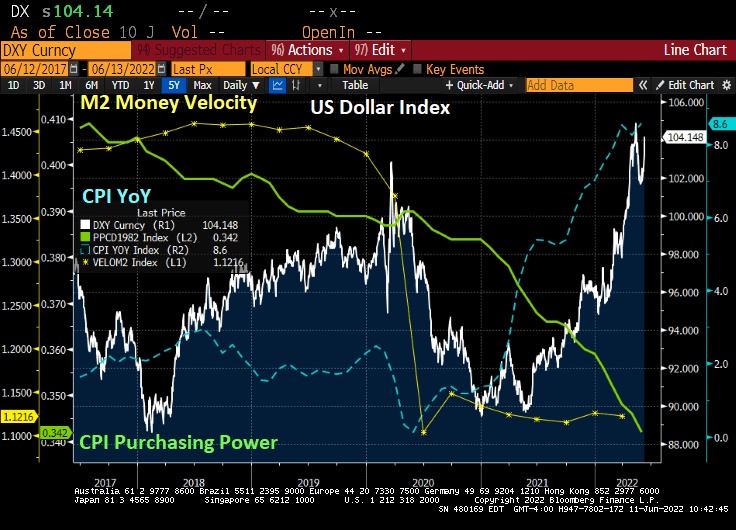

The US Dollar is soaring as US inflation soars, consumer purchasing power (green line) collapses along with M2 Money Velocity.

There is little doubt that soaring inflation, gasoline and food prices have hurt Biden’s popularity as well as the Democrats popularity ahead of the upcoming mid-year elections. People for the most part vote with their wallets.

According to estimates by Bloomberg Economics, US households will spend $5,200 more this year than they did last year on the same consumption basket.

That breaks down to $433 extra in expenditures every single month. That is what is called “the inflation tax.” And it hurts.

Call this The Inflation Tax Blues.

You must be logged in to post a comment.