US housing starts for October were less than expected. A 1.5% increase MoM was expected, but housing starts actually fell -0.7% MoM.

5+ unit (multifamily) starts were up 6.82% MoM. 1-unit single family detached units were down -3.89% MoM. Permits to build were up 4% MoM.

On a YoY basis, 1-unit start declined -10.6% as M2 Money growth continues to fall.

And 1-unit housing starts have fallen with the rapid decline in home buying sentiment.

1-unit starts have slowed to pre-COVID levels, thanks in part to The Federal Reserve’s money printing bonanza which may never end.

As housing sentiment crashes (due to rapid home price growth), we are seeing the demand for multi-family housing rise. 5+ unit (multifamily) starts were up 6.82% MoM in October.

I wonder if Biden’s Press Secretary Jen Psaki will argue that inflation is transitory … again?

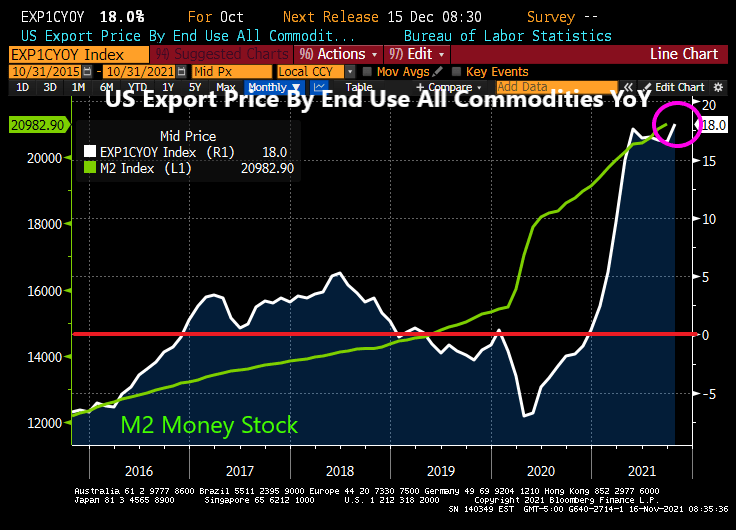

Well, the US is exporting inflation to our trading partners. US Export Prices by end use rose 18% YoY.

Of course, with the Biden Administration shutting down energy pipeline and drilling, it is not surprising.

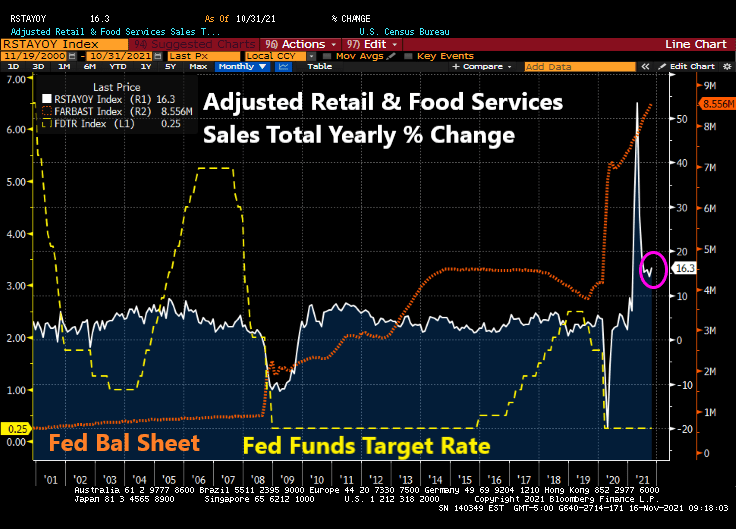

Then we have the advance retail sales numbers for October. Growing at 16.3% YoY with massive monetary stimulus still in play.

Then we have Federal Reserve Bank of St. Louis President James Bullard saying that the central bank should speed up its reduction of monetary stimulus in response to a surge in U.S. inflation.

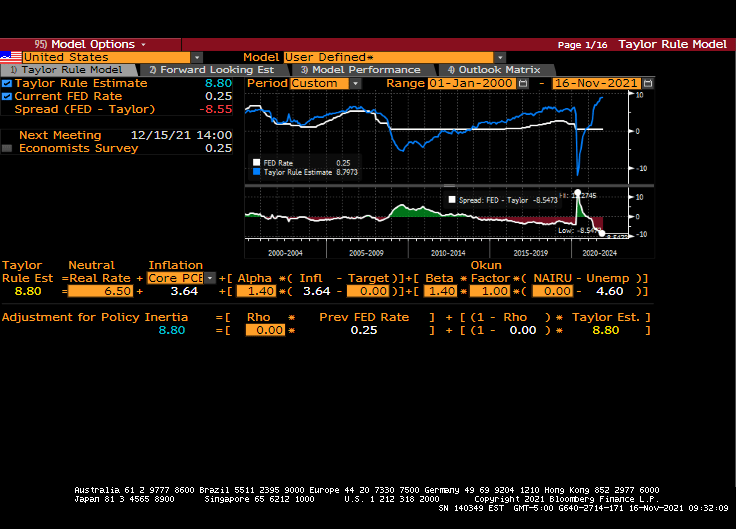

You mean like what Mankiw’s specification of the Taylor Rule model suggests??

How did healthcare insurance companies get a seat at the table for the massive infrastructure bill is beyond me.

President Biden and Congressional Democrats are celebrating the signing of the $1.2 trillion Infrastructure Bill at the White House. Remember, of the $1.2 trillion estimated price tag, less than 10 percent –$110 billion – will fund true infrastructure: bridges, roads, tunnels, and waterways.

And what the hell is healthcare doing in the infrastructure bill?

H.R. 3864 will restore a 2 percent cut in reimbursements to Medicare providers, on top of all the other federal payments reductions.

A second health care provision buried in the $1.2 trillion infrastructure bill delays implementation of the Medicare Part D Rebate Rule, a Trump-era rule that would inject competitive forces into the market for prescription drugs. Just like payment cuts, by delaying this rule, desperately needed drugs will remain unaffordable and therefore unavailable.

And they wonder why there is a going concierge medicine movement that won’t accept Medicare and healthcare insurance. It is The Red Hour for free markets.

“I am Landrieu.” Former mayor of the most corrupt city in the United States. Makes sense that Biden would choose Landrieu to coordinate the infrastructure plan.

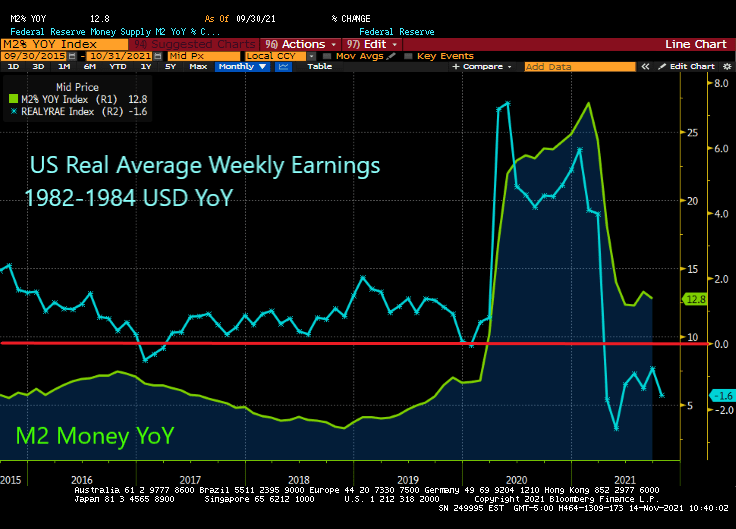

Highlights for Children has a popular segment called “What’s Wrong With This Picture?”

I give you my economics version of “What’s Wrong With This Picture?” It features The Federal Reserve’s M2 Money year–over-year compared with Real Average Weekly Earnings year-over-year.

Yes, M2 Money growth has “slowed” to 12.8% YoY while US Real Average Weekly Earnings YoY is now -1.6%. In other words, while M2 Money is still growing at a rapid pace, real weekly earnings growth is NEGATIVE.

The Fed continues to pump money into a bottle-necked economy while The Federal government pays people NOT to work.

The US Senate has a plan to fix the problem: Biden has nominated Saule Omarova, a dingbat law professor from Cornell (alma matter for The Office’s Andy Bernard), who proposes the following:

(1) Moving all bank deposits from commercial banks to so-called FedAccounts at the Federal Reserve;

(2) Allowing the Fed, in “extreme and rare circumstances, when the Fed is unable to control inflation by raising interest rates,” to confiscate deposits from these FedAccounts in order to tighten monetary policy;

And Ohio Senator Sherrod Brown (D-of course) thinks there is NO MORAL HAZARD PROBLEM with The Fed confiscating bank deposits for its own use?????

If I was attending Omarova’s confirmation hearing, my verdict would be ..

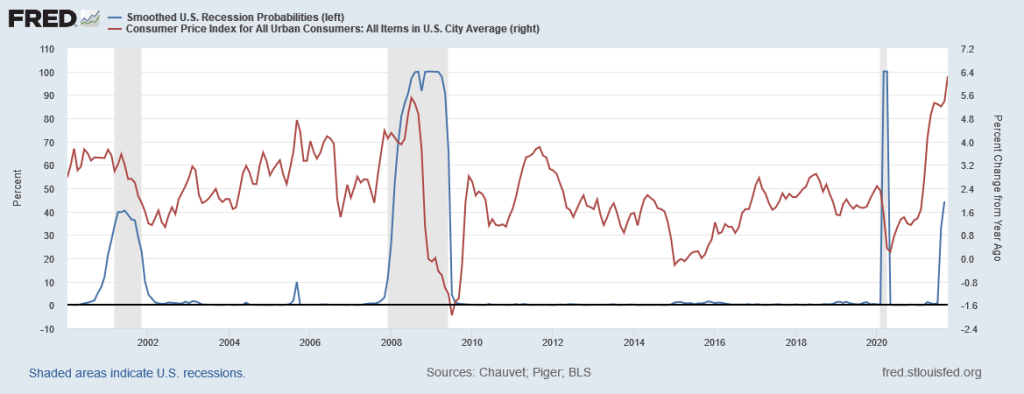

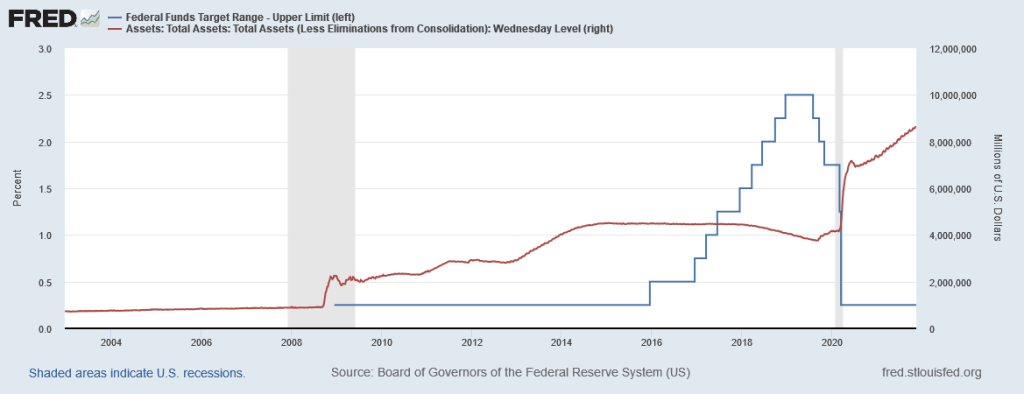

Nothing has been the same since the housing bubble of the 2000s, the resulting banking meltdown and the takeover of the economy by The Federal Reserve.

And since the 2000s housing bubble and financial crisis, The Federal Reserve has taken control of the economy resulting in M2 Money Velocity crashing to historic lows.

Policy blunders perpetrated by the Biden White House have made a bad problem worse.

For instance, oil prices are higher for two reasons. First, U.S. production has declined by about two million barrels per day since 2019, even as demand has recovered from the COVID-19-induced downturn. Oil markets are global, so the fall-off in output would not necessarily jack prices up, but our declining output needs to be offset by an increase elsewhere.

Enter OPEC, which has not restored output to the level necessary to bring down prices, despite repeated pleas from Biden.

Meanwhile, Biden has done a lot to discourage a resurgence in U.S. drilling and production. He has cancelled pipelines, threatened oil and gas producers with higher taxes, taken promising acreage out of play, such as the Arctic Natural Wildlife Refuge, slow-walked leasing and new drilling permits and, most recently, imposed new methane-curbing rules that make drilling more expensive.

What sensible person would invest in the oilfield in the face of such unrelenting hostility? Drilling activity is up, but nowhere near where it should be at $82 per barrel oil.

Another boost to inflation came from housing. With “shelter” accounting for some 40 percent of the CPI, economists have warned that fast-rising home prices would eventually seep into higher inflation readings. In October, we saw this occur, with the increase in the cost of shelter accelerating to 0.5 percent from September, an annualized rise of 3.48 percent. The CPI owners equivalent rent of residence rose to 3.13% YoY. Too bad home prices are increasing at almost 20% YoY.

One reason home prices have been increasing at nearly 20 percent per year is that the Federal Reserve has continued to buy up $15 billion worth of mortgage-backed bonds each month, keeping mortgage rates artificially low. The result has been a booming market, driving home prices, and now rents, higher.

At long last, the Federal Reserve has announced it will begin to throttle back its bond-buying program, including the purchases of mortgage-backed bonds. Critics think the Fed is behind the curve, having seriously underestimated price pressures.

Biden does not control the Fed, but he has made no secret of his preference for the easy money policies that have helped prop up the economy, and the stock market. Fed Chair Jerome Powell’s term ends in February; Biden has recently interviewed not only Powell but also Fed Governor Lael Brainard, a known dove and Obama appointee, for the position.

That these are the only two candidates he seems to be considering sends a clear signal. He will choose growth over stability, even if it means that inflation continues to accelerate. Unhappily, Powell is listening.

Finally, Biden has not only encouraged monetary excess, but has also endorsed big-spending packages that have put money in consumers’ pockets but also kept workers on the sidelines. The biggest shortage we have in this country today is labor. The labor participation rate is mired at 61.6 percent, 1.7 percentage points below the level in February 2020.

Studies have shown that the slew of benefits contained in the Cares Act and subsequent relief bills, including incremental unemployment benefits, expanded child tax credits and rent moratoriums, have offered Americans up to $100,000 per year while not working. These payments may have been necessary early in our recovery from the pandemic, but no longer are needed.

And then people are surprised that grocery prices are getting so f&^*ing high???

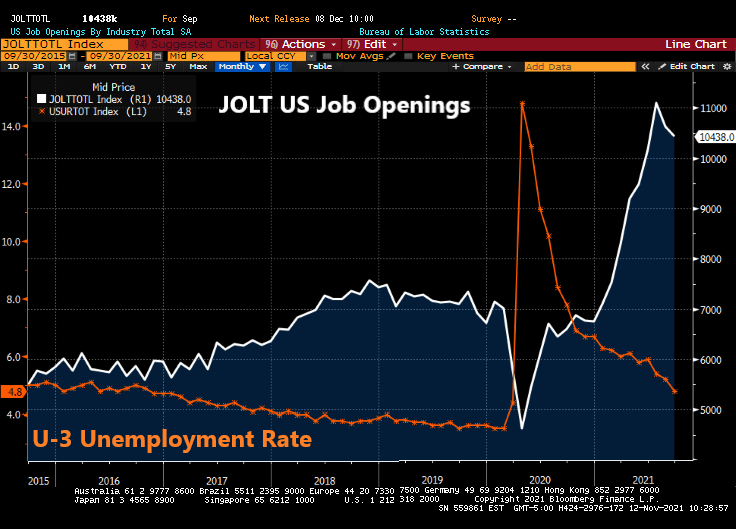

The Federal Reserve continues to JOLT markets with excessive monetary stimulus despite numerous reasons why they should back off.

For example, today’s JOLT report (US job openings) revealed that 10.4 million jobs were open in September. This is the fourth consecutive month of 1 million plus job openings, yet The Fed refuses to raise their target rate.

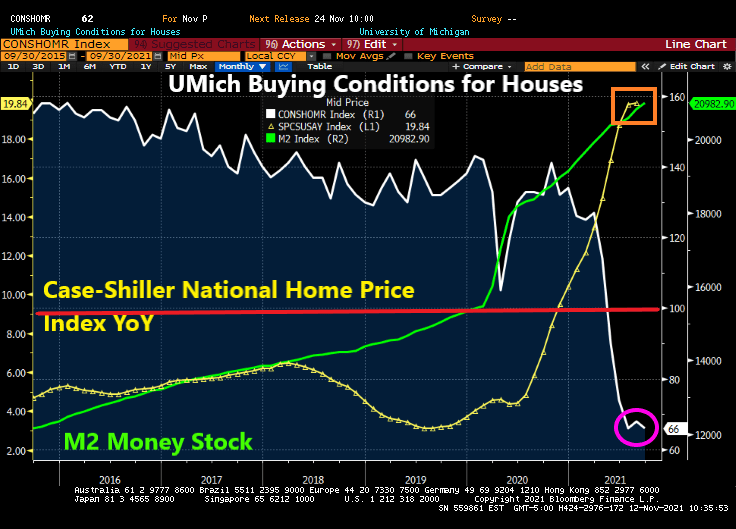

At the same time, the University of Michigan survey revealed that buying conditions for houses dropped to 66 (baseline of 100). To show how bad this is, buying conditions for houses was at 144 this time last year.

UPDATE: UMich revised their number downward to 62, the lowest since 1981.

In The Fed’s mind, they are still chasing at least 3.5% unemployment, the lowest rate under President Trump prior to COVID. But with perpetual million plus job openings GOING UNFILLED, trying to get to pre-COVID unemployment rate of 3.5% is a fool’s errand.

Of course, with The Fed helping to pump up house prices to largely unaffordable levels, it makes sense that enthusiasm for buying expensive homes has crashed.

Meanwhile, The Fed continues to JOLT the economy with excess stimulus.

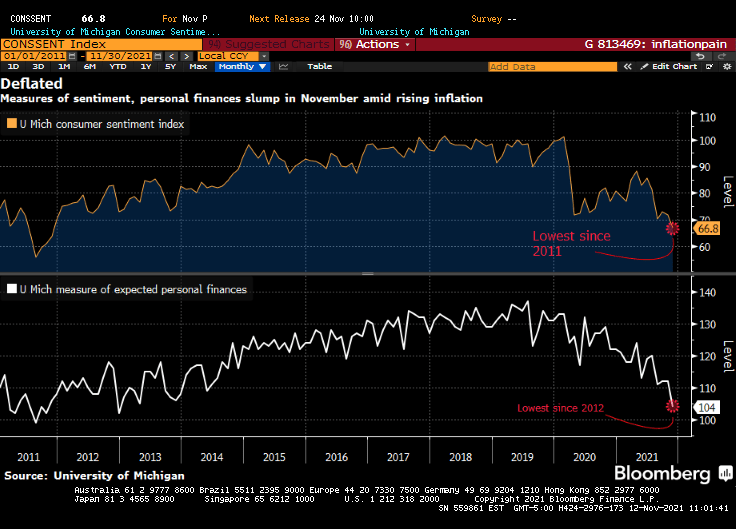

Overall inflation fears are leading to lowest consumer confidence since 2011.

Wu-Xia employs an approximation that makes a nonlinear term structure model extremely tractable for analysis of an economy operating near the zero lower bound for interest rates. It can be used to summarize the macroeconomic effects of unconventional monetary policy (ZIRP + QE). The Shadow Rate is now -1.7021%.

And you wonder why we have inflation and house prices going into orbit?

With inflation also going into orbit, we see that breakeven 10 year inflation rate rising above the 5Y5Y (nominal forward 5 years minus US inflation-linked bonds forward 5 years). In other words, the US has abnormally high inflation and is expected to grow and NOT be transitory.

The Shadow knows … that the US is hyperstimulated. And inflation isn’t going away anytime soon.

You must be logged in to post a comment.