Consumers are healthy? It is true that the US U-3 uemployment rate is low (3.6% versus 14.70% in April 2020 thanks to government shutdowns over Covid). But even though unemployment is low, consumer sentiment is at its lowest point since 1977.

Generally, consumer sentiment is high when unemployment is low, but not this time around. Currently, inflation is at the highest level since March 1980 even though consumer sentiment bottomed-out in April 1980.

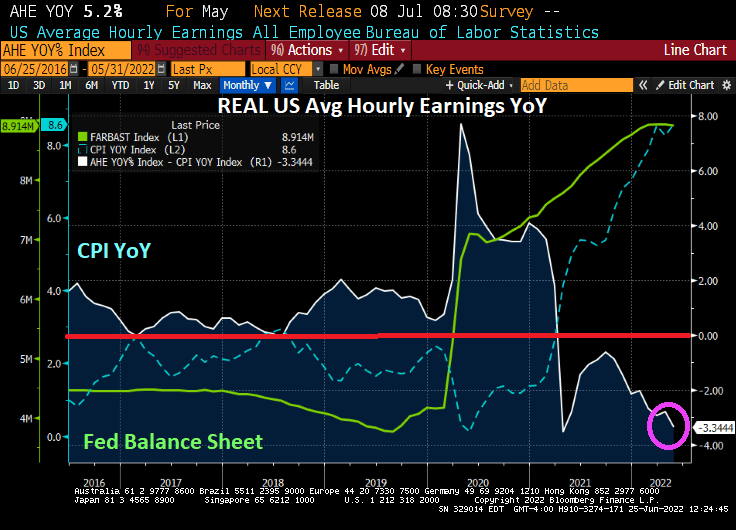

Here is my chart showing that REAL average hourly earnings growth YoY is negative and getting worse, hardly a sign of “healthy consumers.”

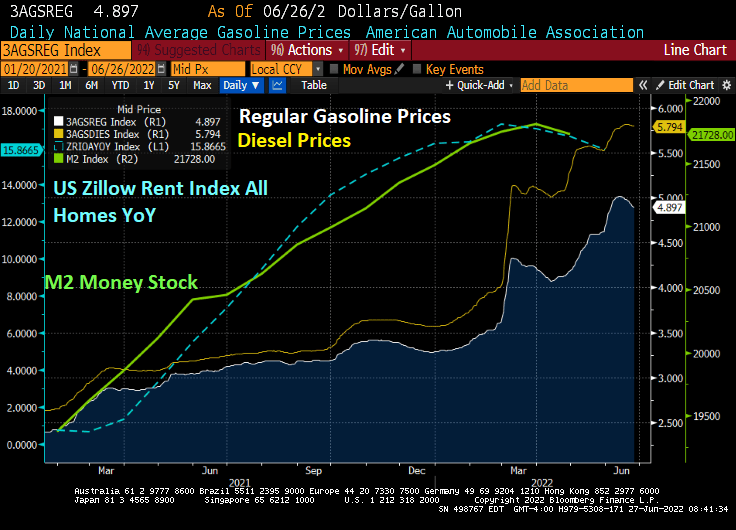

Of course, rising gasoline and diesel prices have risen dramatically since 2021, but are declining slightly thanks to the global economic slowdown (read “lower demand”).

And a M2 Money Stock (green line) declined, US rents (blue line) declined as well.

The US Treasury 10Y-5Y yield curve has gone into negative territory (which usually occurs before a recession). At the same time, US mortgage rates are climbing like Tom Cruise in “Top Gun: Maverick” to 5.87% as The Fed tightens its choke hold on markets.

The 10Y-5Y Treasury curve typically goes negative before a recession.

And then we have today’s PPI report (Producer Price Index), rising 10.8% YoY as M2 Money stock starts to decline a bit.

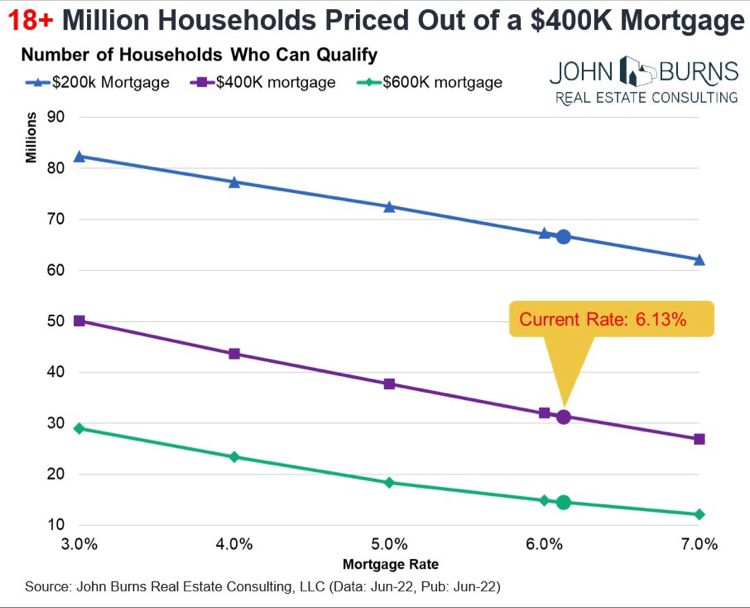

Here is a better view of mortgage rates under Biden/Powell.

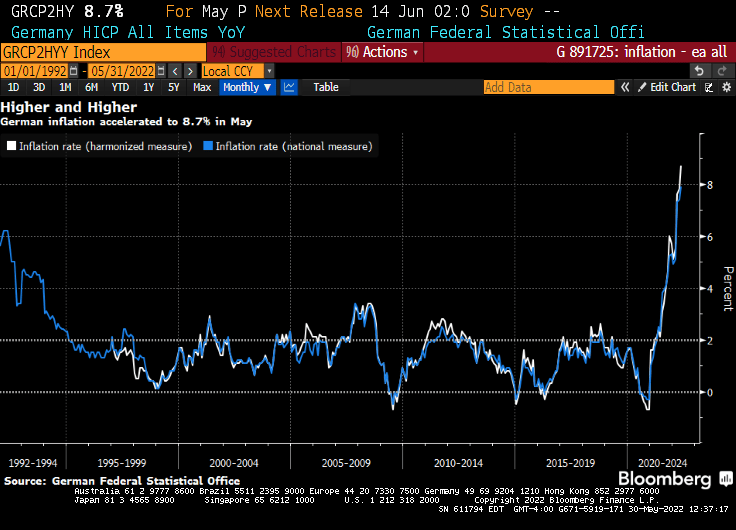

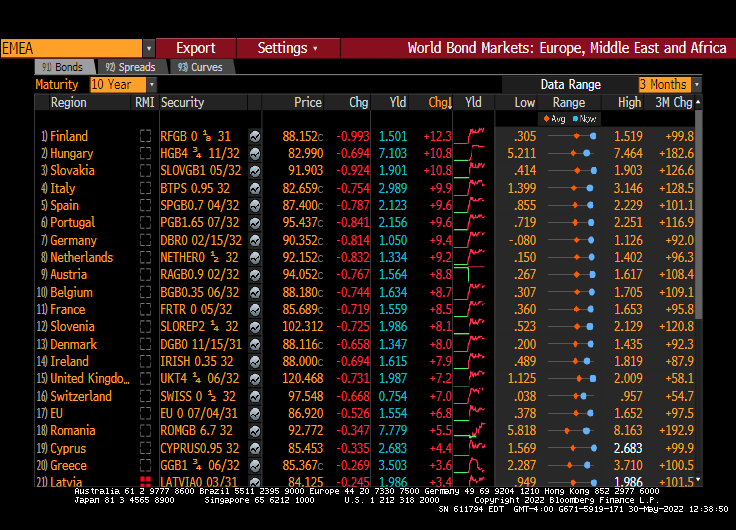

German inflation hit another post-World-War-II record high, piling pressure on The ECB’s need to exit from crisis-era stimulus after numbers from Spain also printed hotter than expected.

Driven by soaring energy and food costs, this morning’s data showed consumer prices in Europe’s largest economy surged 8.7% YoY – far hotter than the +8.1% expected (the highest since the start of the monthly statistics in 1963).

And top of that, the German 10-year Bund rate rose +9.4 BPS this morning, although Finland, Hungary and Slovakia all rose above +10 BPS.

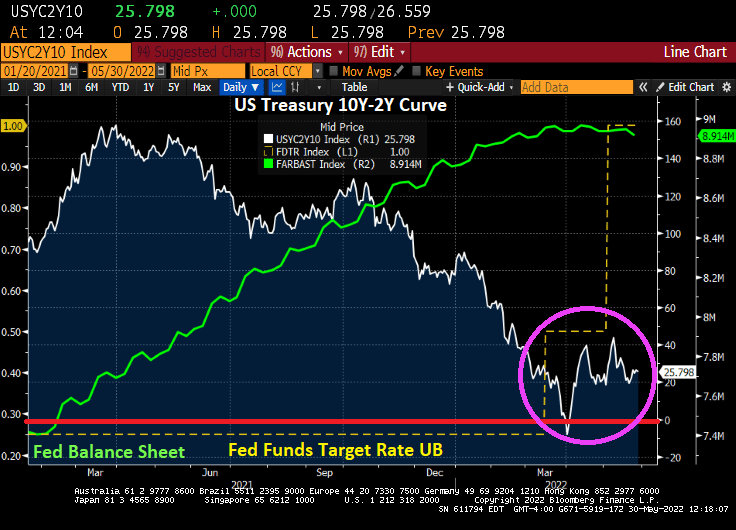

While US markets are closed today in honor of Memorial Day, the US Treasury curve (10Y-2Y) has stabilized at 25.8 basis points after the initial shock of The Fed finally raising rates for the first time under Biden.

Then there is this headline: Biden to Meet Powell to Discuss Economy Amid Inflation Pain. So much for Fed independence. I wonder if Powell will say “Joe, have you ever considered canceling your executive orders on oil and natural gas exploration?”

We have a double whammy facing investors, The Federal Reserve wanting to take away the monetary punch bowl and Federal energy policies that are crushing middle-class households and lower-wages workers.

But how do you hedge against The Federal Reserve tightening and Biden’s reckless energy policies?

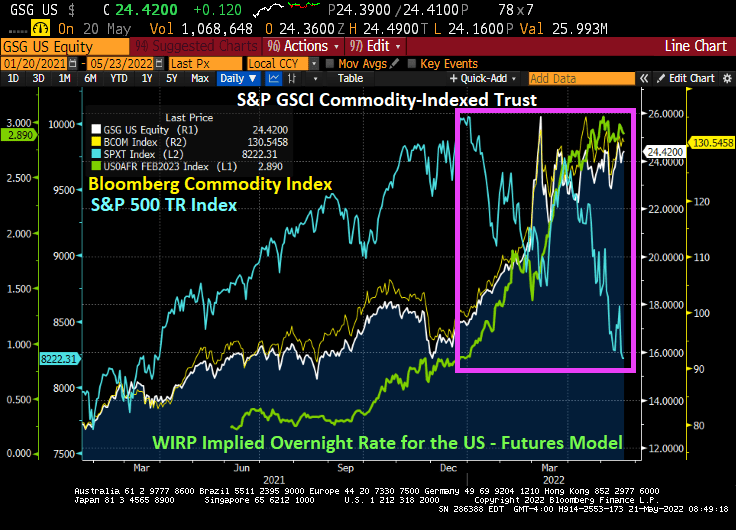

Take a look at investing in commodities (S&P GSCI Commodity-Indexed Trust and the Bloomberg Commodity Index) versus the S&P 500 Total Return index since The Fed began signaling that they would take away the monetary punch bowl.

Yes, commodities like food and gasoline/diesel prices are up dramatically under Biden’s energy policies (not to mention the USA’s proxy war with Russia).

The Fed seems determined to remove the Fed “Snake juice” from the economy.

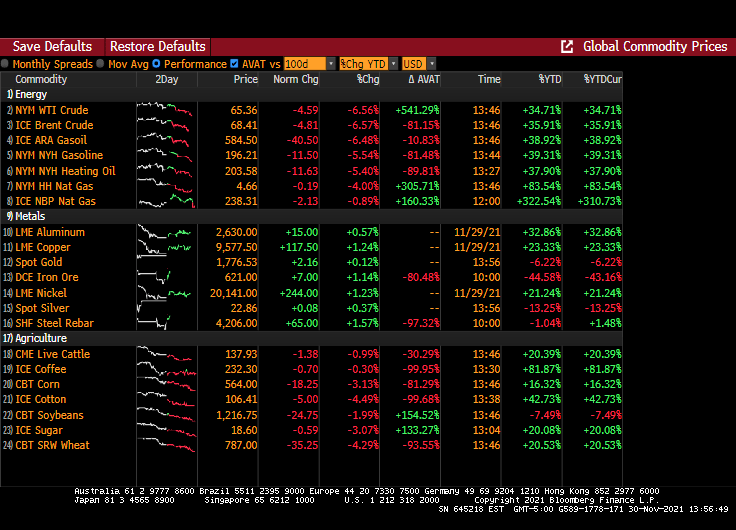

As the US is engulfed in inflation while The Federal Reserve is engaged in trying to fight inflation (well, sort of), we are seeing markets taking a shellacking, particularly commodities.

One indicator of a slowdown is declining commodity prices. Crude oil futures are down around -2.5%. Iron Ore is down -5% and steel rebar is down -3.21%.

Inflation numbers are due out Wednesday and are forecast to be 8.1% YoY (based on headline CPI). But combined with a slowing global economy, we get the dreaded “STAGFLATION.”

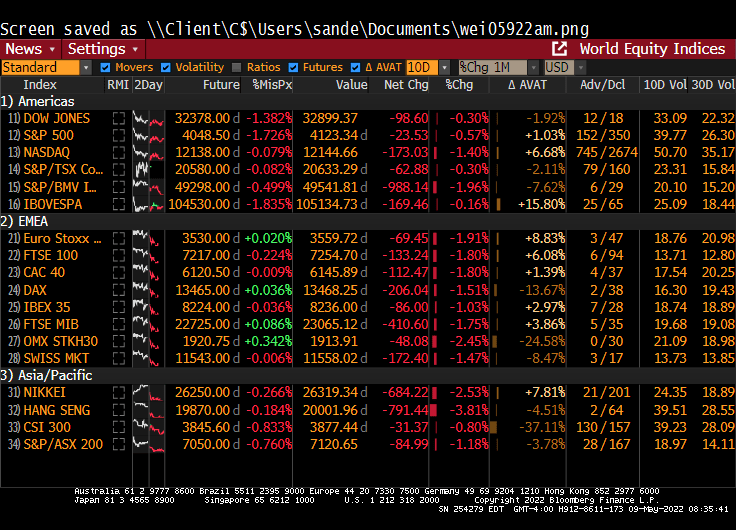

Meanwhile, the S&P 500 index futures are down around 1.726% for Monday open. Asian markets already got clobbered with the Hang Seng down almost -4%.

On the bond side, the 10Y Treasury Note yield rose to 3.20% early in the morning, but has retreated to 3.1447% as of 8:40am EST.

Both stock and bond market volatility measures are increasing.

So, is it a Blue Monday effect? Or global stagflation?

Raphael Bostic and Goldman Sachs are both calling for dramatic rate increases to fight inflation … that they helped cause with their monetary stimulypto. I call this The Fed’s March of the Toreadors as The Fed now attempts to kill the bull market.

(Bloomberg) — The Treasury yield curve flattened to the lowest level in over a year on Monday as the prospect of a super-sized Federal Reserve rate increase in March gained traction, weighing disproportionately on shorter-dated tenors.

Two-year U.S. yields climbed as much as 4 basis points after Raphael Bostic, the president of the Fed’s Atlanta branch, said the U.S. central bank could raise its benchmark rate by 50 basis points if a more aggressive approach to taming inflation is needed.

That narrowed the gap with ten-year counterparts — which rose about half as much — to the least since October 2020. The last time the Fed delivered a half-point increase to borrowing costs was at the height of the dot-com bubble in 2000.

The repricing extended a move spurred last week, after Fed Chair Jerome Powell underscored the policy maker’s determination to put a lid on inflation. The market positioning may have been exacerbated by hedge funds that had been leaning the wrong way before Powell’s address.

Traders are currently betting the Fed will deliver 32 basis points of tightening in March, more than fully pricing an increase of a quarter-point. That puts the implied probability of a 50-basis-point increase at almost 30%. The odds of such a move in December were zero.

Consumer prices rose an annual 7% in December, the fastest pace in almost four decades. Powell left the door open to increasing rates at every meeting, and didn’t rule out the possibility of a 50-basis-point hike.

In an interview with the Financial Times, Bostic stuck to his call for three quarter-point interest rate increases in 2022, while saying that a more aggressive approach was possible if warranted by the economic data. Bostic is a non-voting member of the FOMC this year.

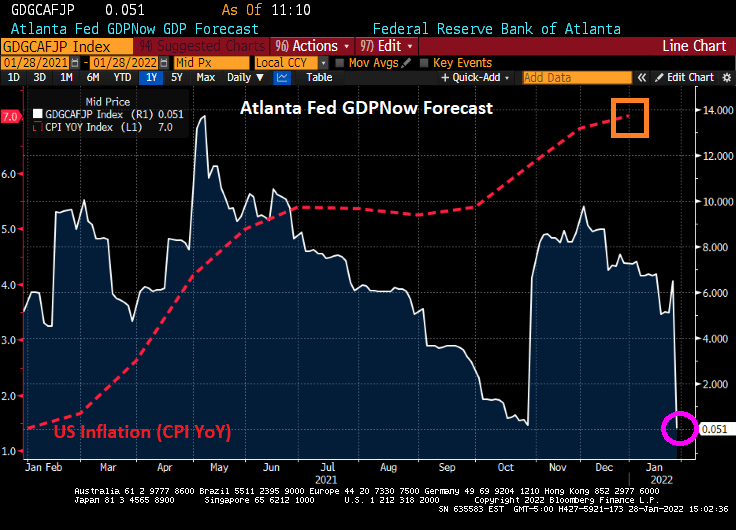

Since the rapid growth in inflation was caused by a combination of too much Fed stimulus, too much fiscal stimulus and “green” energy policies, it is unclear whether an increase of 50 basis points will do much, particularly if Bostic’s own Atlanta Fed GDPNow forecast of 0.051% is accurate. Raising ratesif the economy is slowing??

To be clear, Bostic and others are trying to signal The Fed’s intent well in advance to avoid a surprise knock-down of the stock market. Or a killing of the bull market.

I love listening to Fed talking heads (or Fear The Talking Fed). They mostly seem to acknowledge that inflation is a problem and that the excessive monetary stimulus should be reduced.

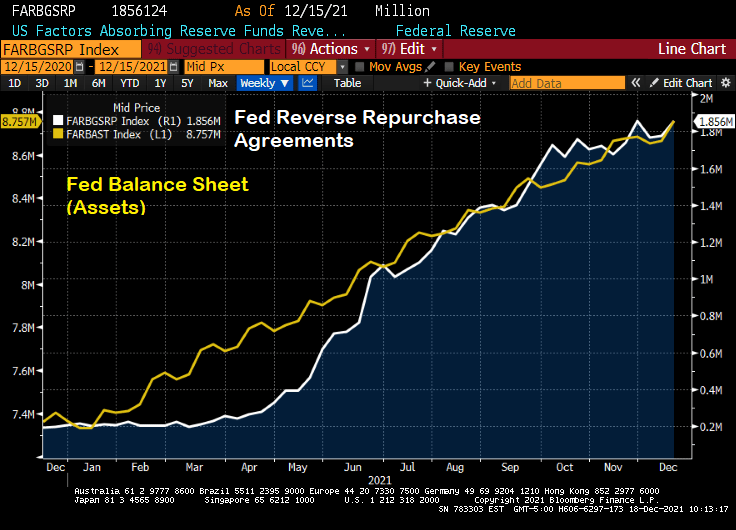

But then I see the chart of The Fed’s balance sheet and The Fed’s reverse repo operations.

Then we have Federal Reserve Governor Christopher Waller saying that Th Fed could start raising interest rates as early as its March 15-16 meeting, after deciding to end asset purchases sooner than planned. My question is … why wait until the March meeting?

Is it fear of the Omincron Variant (which sounds like a Frederick Forsyth thriller)? Does The Fed not want to rock the boat prior to the Christmas season? The US is at or near full employment, so what is the real reason for delaying a rate increase until March or June? Or the fear that Congress won’t pass Biden’s Build Back Better Act?

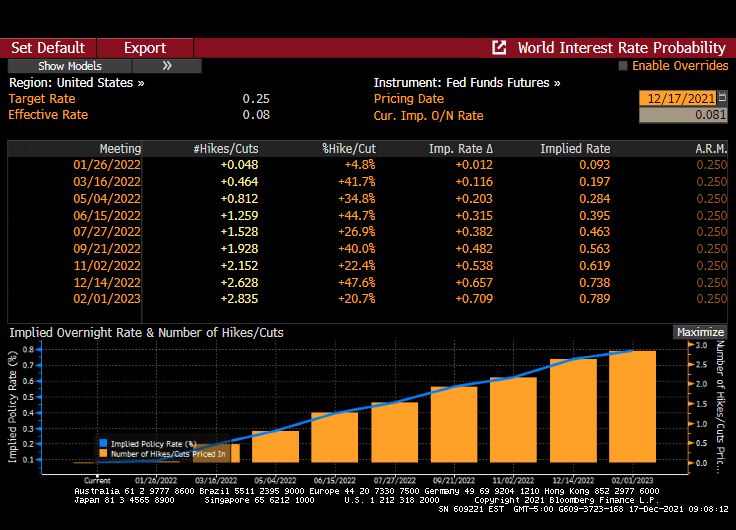

Fed Funds Futures infer that one rate hike will occur at the June Fed Open Market Committee (FOMC) meeting and one at the November meeting.

Calamity Jay Powell testified in front of the US Senate Banking Committee. He rattled markets by going hawkish about inflation, then gave The Fed an out by playing the COVID CARD (the latest Omicron Variant). Aka, the DEATH CARD.

Federal Reserve Chair Jerome Powell said the strong U.S. economy and elevated inflation could warrant ending the central bank’s asset purchases sooner than planned next year, though the new omicron strain of Covid-19 poses a fresh risk to the outlook.

“It is appropriate, I think, for us to discuss at out next meeting, which is in a couple of weeks, whether it will be appropriate to wrap up our purchases a few months earlier,” Powell said Tuesday. “In those two weeks we are going to get more data and learn more about the new variant.”

Powell made the comment in response to questions during a Senate Banking Committee hearing in Washington. The Fed is currently scheduled to complete its asset-purchase program in mid-2022 under a plan announced at the start of November; policy makers next meet Dec. 14-15, where they could make a decision to accelerate the tapering.

On his remarks, the stock market puked.

Well, if Powell followed the Taylor Rule, he would really scare Congress with raising The Fed Funds Target Rate to 14.94% based on an inflation rate of 6.20%.

And then we have HOUSE price inflation of near 20%. But The Fed doesn’t consider than inflation.

Then we have oil prices retreating -4.59%. Not, not due to Biden releasing the National Petroleum Reserve (NPR). Rather it is FEAR of The Fed raising rates and a corresponding slowdown in economic growth.

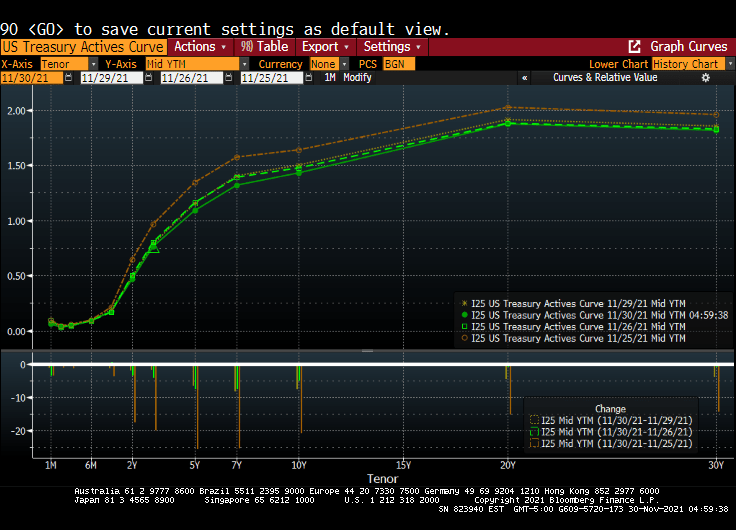

The latest scare hitting financial markets is the Omicron Variant (or Oh! Macron! Variant in France). While it caused an initial decline in global equity markets {Dow fell 900 points on early reports on Omicron), the Treasury market has been relatively unscathed.

For example, the US Treasury Actives curve dropped last Friday (the orange line represents the Wednesday before Thanksgiving), while the remaining three lines represent last Friday, Monday and Tuesdays (today). In other words, the US Treasury Actives curve has been quiet so far this week after Friday’s flattening.

The US Dollar Swaps curve shows the same dynamics. The dark blue line is last Wednesday, while the remaining lines are last Friday, this Monday and today. Not a lot happening after the initial Omicron fear factor was priced in.

Federal Reserve Chairman Jerome Powell believes that the omicron variant of Covid-19 and a recent uptick in coronavirus cases pose a threat to the U.S. economy and muddle an already-uncertain inflation outlook.

“The recent rise in COVID-19 cases and the emergence of the Omicron variant pose downside risks to employment and economic activity and increased uncertainty for inflation,” Powell said in remarks he plans to deliver to Senate lawmakers on Tuesday. “Greater concerns about the virus could reduce people’s willingness to work in person, which would slow progress in the labor market and intensify supply-chain disruptions.”

Do I detect FEAR in Powell’s voice? The odds of rate increases for next year just fell to one rate increase at the September 2022 meeting.

On the equity side, it seems to be all about whether The Fed will withdraw its support. Back in early 2018, then Fed Chair Janet Yellen and the FOMC started to shrink the Fed balance sheet (green line). This resulted in the “Smart Money Index” declining. The S&P 500 index received a jolt with the Fed stimulus around the COVID outbreak and have taken off like a jackrabbit. Despite the Smart Money Flow index being lower than in 2017.

So, is Omicron the “planet killer” or just another mild flu-like outbreak? The data is pointing towards the latter, but FEAR may cause it to be a bigger deal than is warranted.

You must be logged in to post a comment.