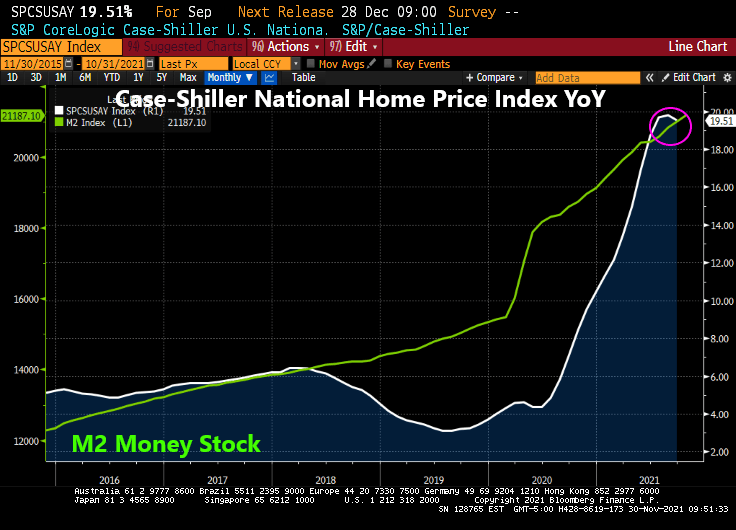

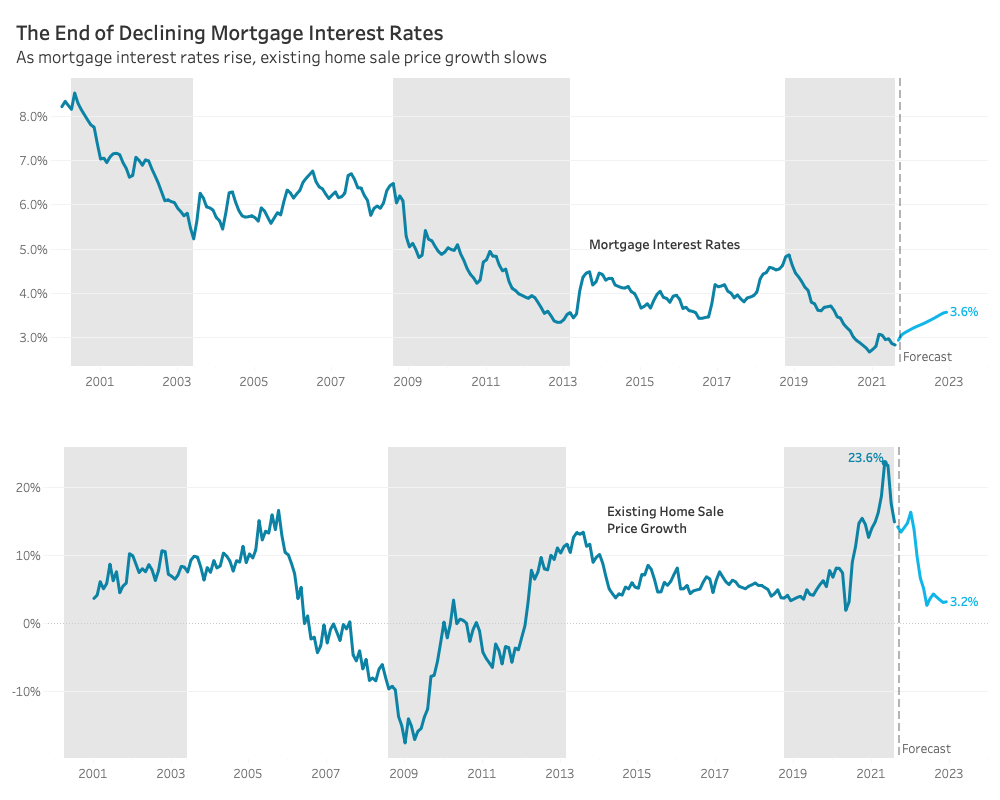

When I told Benzinga’s Phil Hall in an interview a while back that I thought US home price growth would slow, I didn’t consider the never-ending COVID epidemic (now with the Omicron Variant taking the stage. But at least the CoreLogic Case-Shiller National home price index (HPI) “slowed” in September from +19.84% to +19.51%.

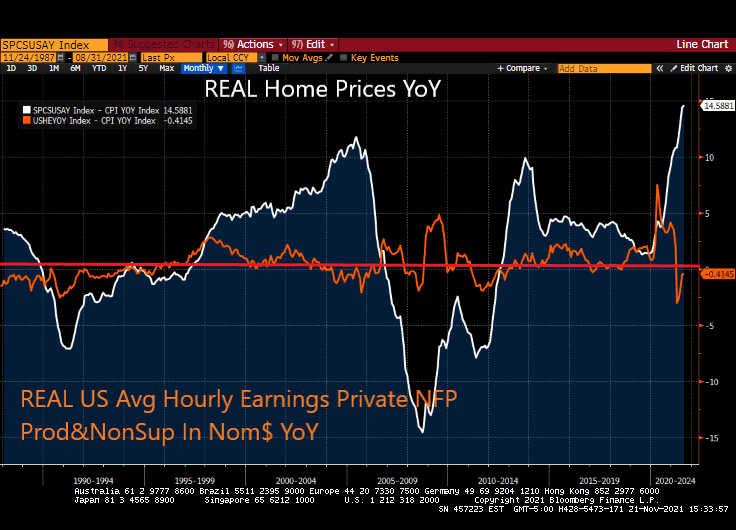

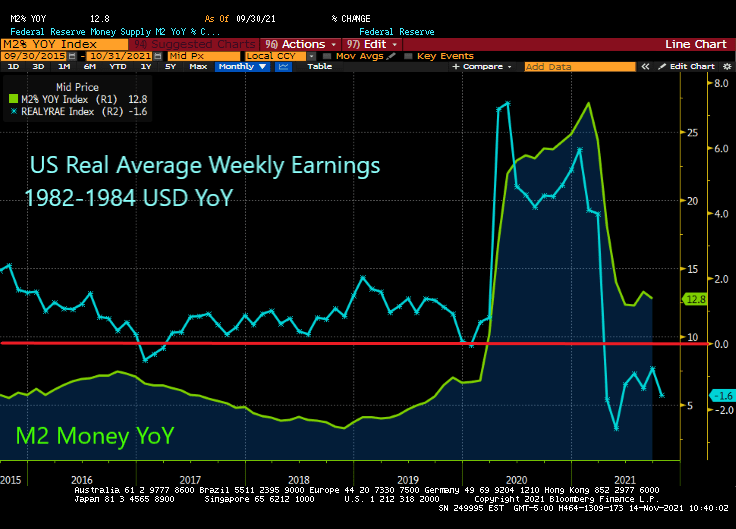

Once again, low available inventory of houses for sale coupled with outlandish Fed stimulus has resulted in a housing crisis where home price growth (+19.51%) exceeds hourly wage growth (+5.76%) by almost 4x.

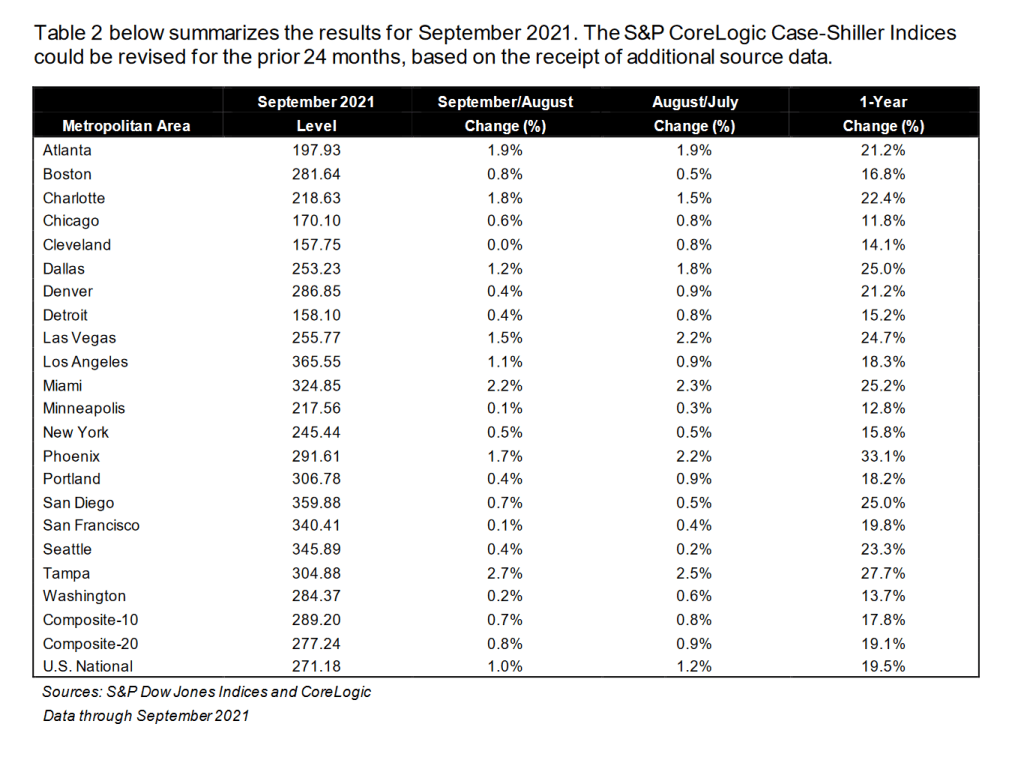

Where are all the home prices above 10% YoY? Every one of the 20 metro areas covered by Case-Shiller. Phoenix AZ leads at +33.1%. Chicago IL is the “slowest” at 11.8%.

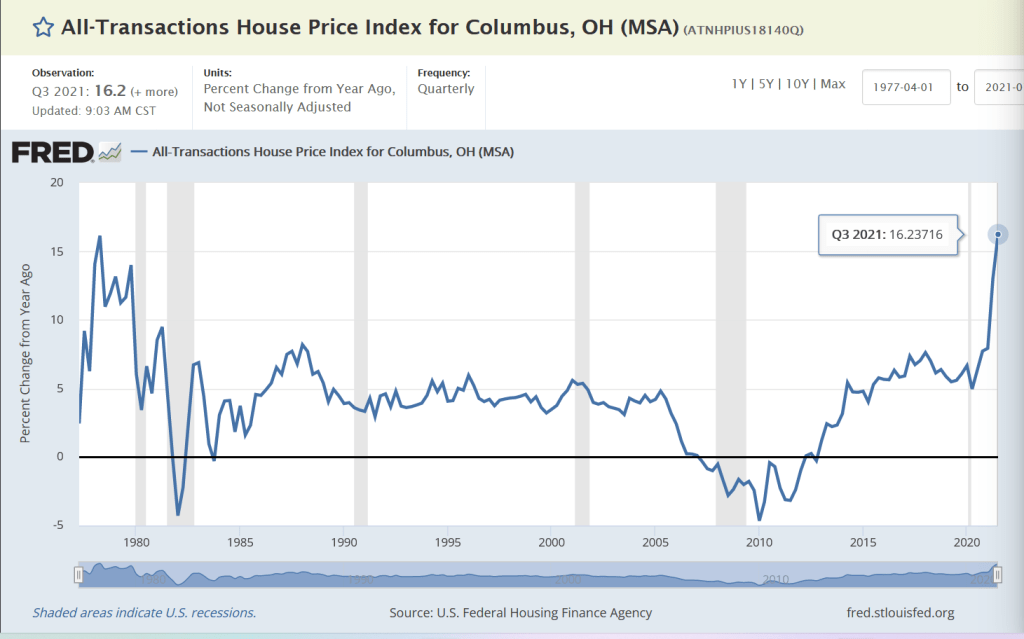

Although Columbus OH is the growth hub of the state, Case-Shiller only reports Cleveland. So here is Columbus’s all-transactions home price growth for Q3: +16.2% YoY placing Columbus at the top of the midwest metro areas of Detroit, Chicago, Minneapolis and Cleveland.

With the latest Omicron Variation (sounds like a Star Trek TV show episode), I will bet that The Fed will stay a little longer and keep rates low, leading to home price growth (with limited available inventory) to continue to grow at double digit speeds.

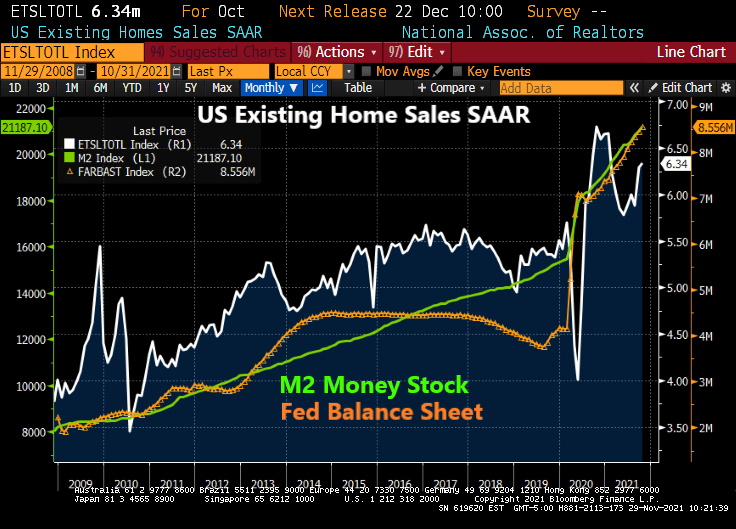

The Fed is printing SOOOO much money that the dollar should have a double eagle on it.

You must be logged in to post a comment.