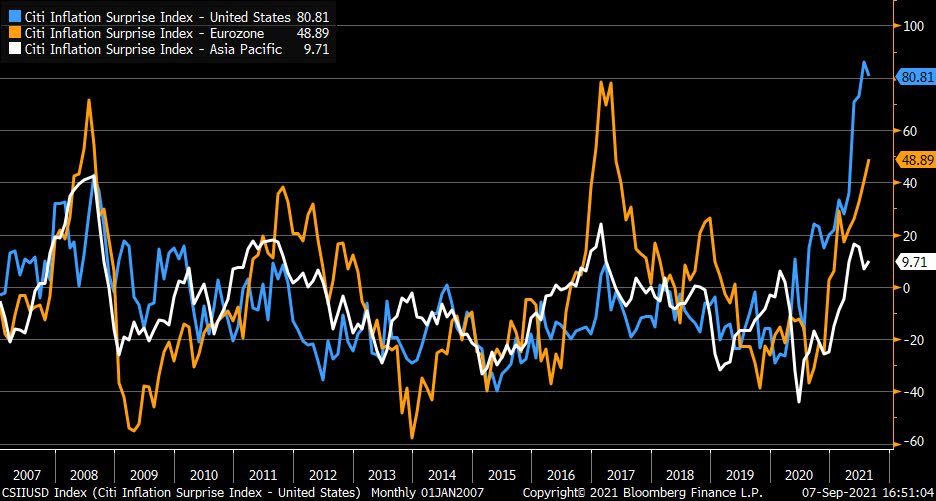

Phil Hall of Benzinga wrote a series of excellent articles in four parts for MortgageOrb (although “The Orb” has removed his name). Here are the links to his stories.

https://mortgageorb.com/the-fall-and-rise-of-the-housing-market-part-one

https://mortgageorb.com/the-fall-and-rise-of-the-housing-market-part-two

https://mortgageorb.com/the-fall-and-rise-of-the-housing-market-part-three

https://mortgageorb.com/the-fall-and-rise-of-the-housing-market-part-four

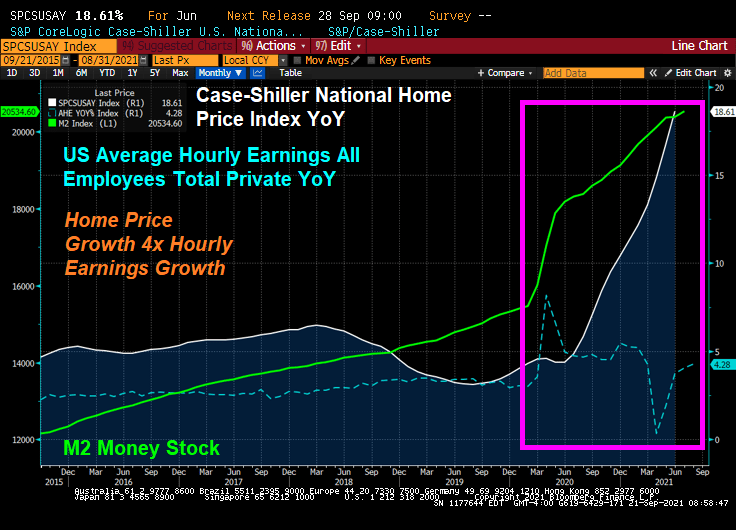

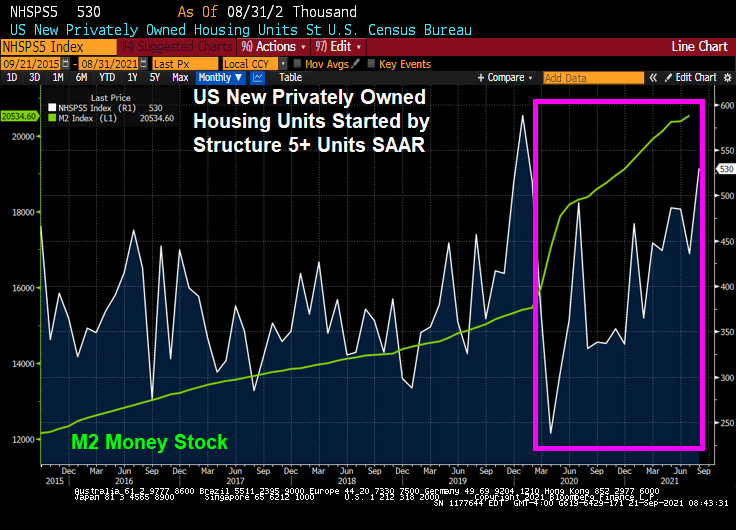

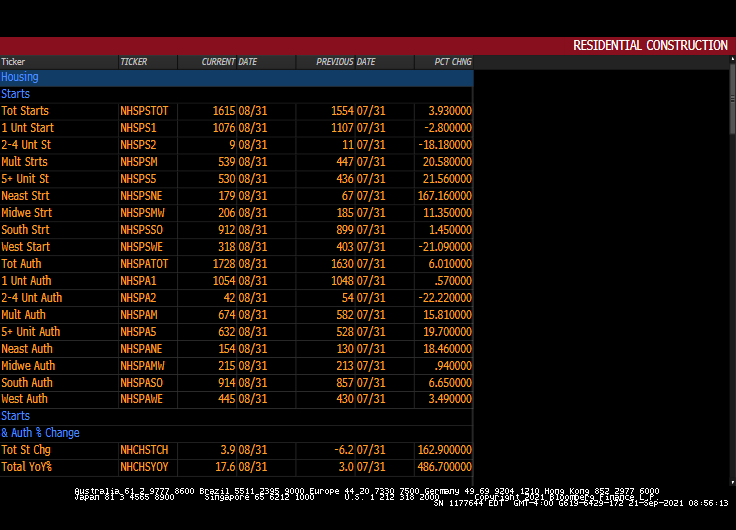

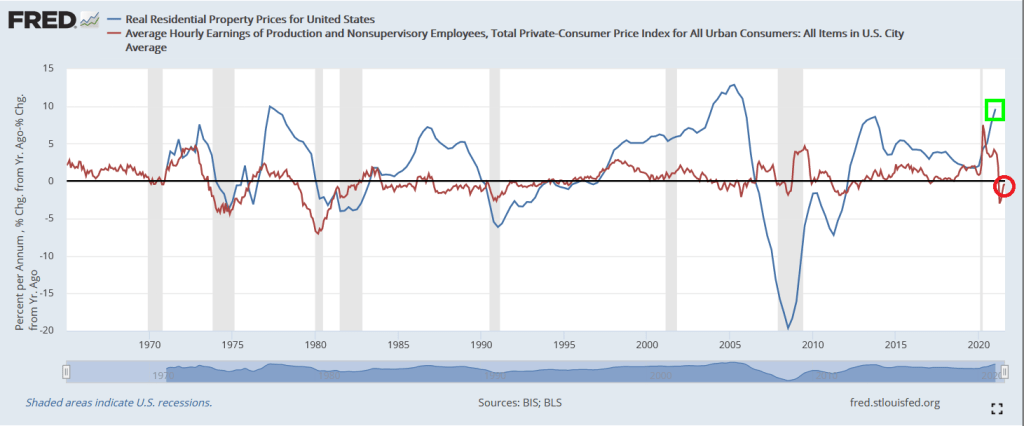

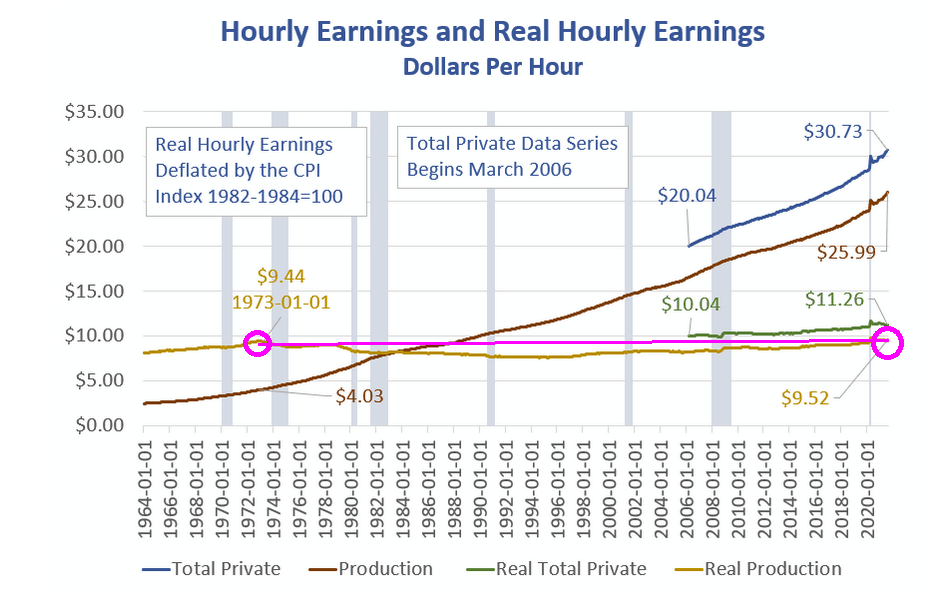

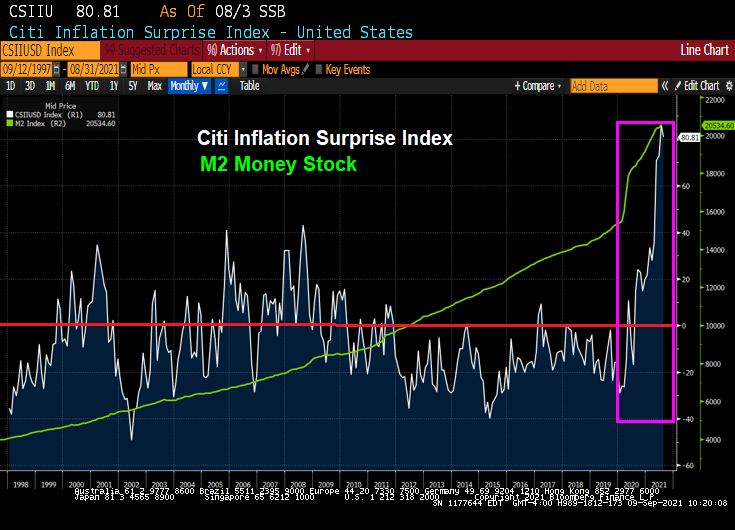

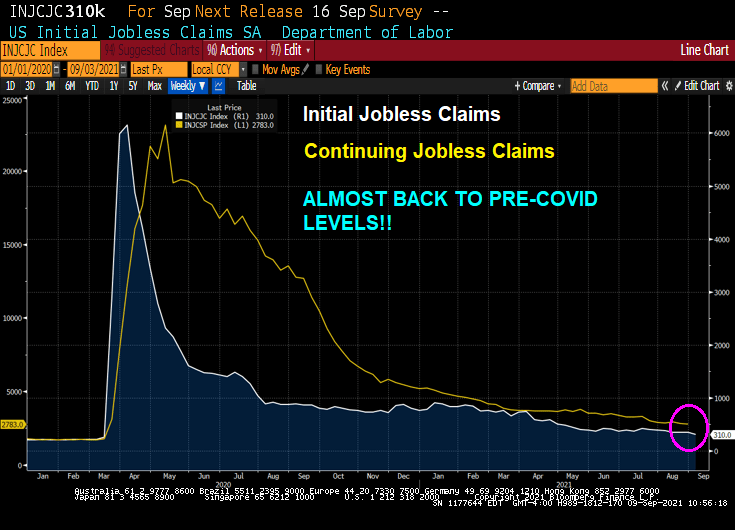

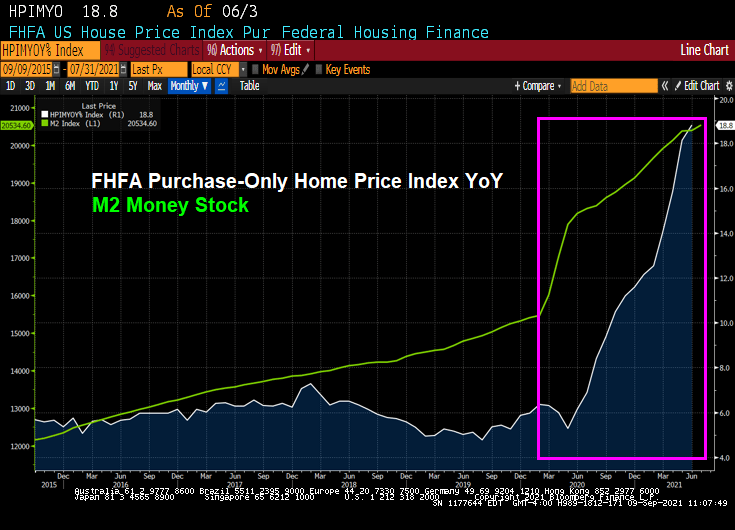

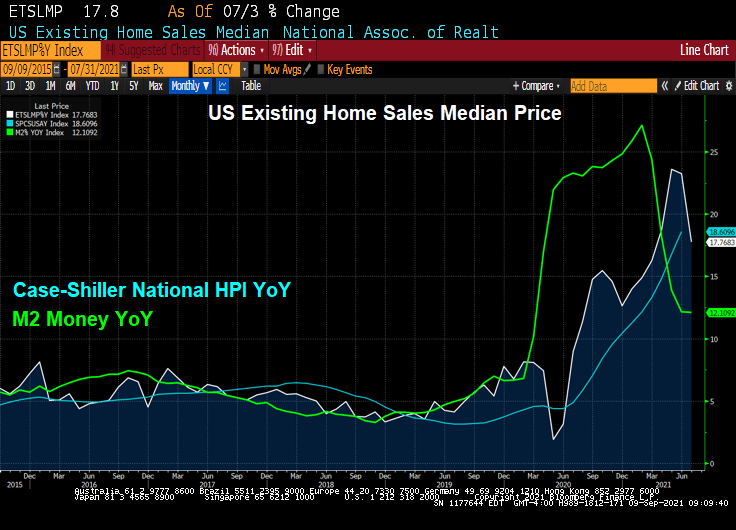

After re-reading these excellent articles on the housing bubble and crash, I thought I would take the opportunity to present a few charts to highlight the housing bubble, pre-crash and post-crash.

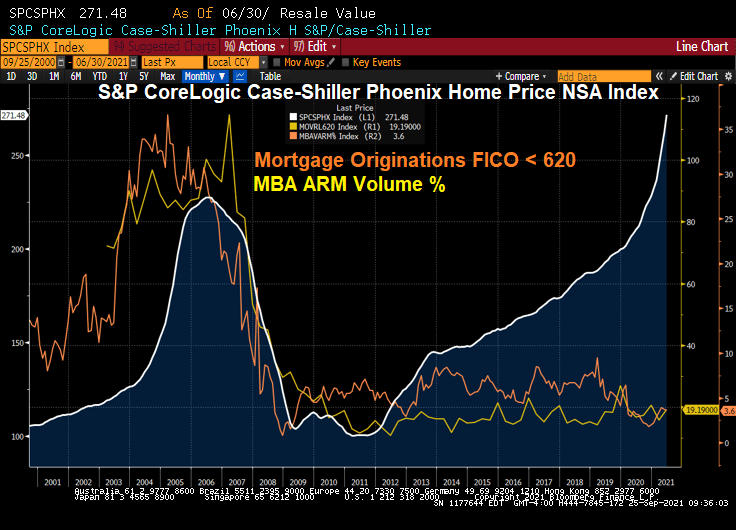

Here is a graph of Phoenix AZ home prices. Note the bubble that peaked in mid 2006. The Phoenix bubble correlates with the large volume of sub-620 FICO lending and Adjustable-rate mortgage (ARM) lending. Bear in mind, many of the ARMs prior to 2010 were NINJA (no income, no job) ARM loans.

What happened? Serious delinquenices at the national levels spiked as The Great Recession set in and unemployment spiked.

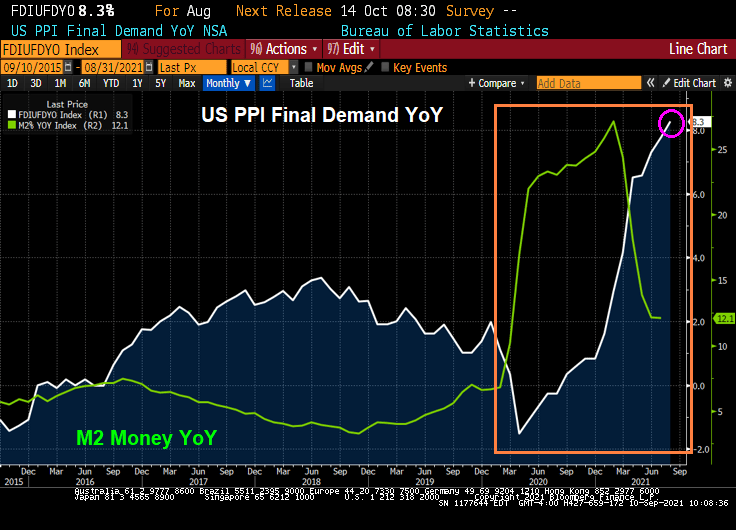

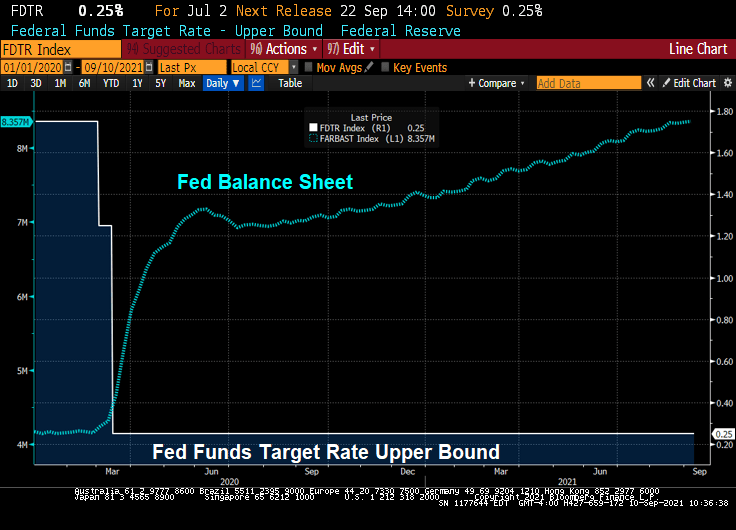

Since the housing bubble burst and surge in serious mortgage delinquencies, The Federal Reserve entered the economy with a vengeance. And have never left, and increased their drowning of markets with liquidity.

The Fed whip-sawing of interest rates in response to the 2001 recession was certainly a problem. They dropped The Fed Funds Target rate like a rock, then homebuilding went wild nationally and home prices soared thanks to Alt-A (NINJA) and ARM lending. But now The Fed is dominating markets like a gigantic T-Rex.

Oddly, then Fed Chair Ben Bernanke never saw the bubble coming. Or the burst.

Speaking of pizza, Donato’s from Columbus Ohio is my favorite. Founder’s Favorite is my favorite, but they do offer the dreaded Hawaiian pizza (ham, pineapple, almonds and … cinnamon?)

Bleech!

You must be logged in to post a comment.