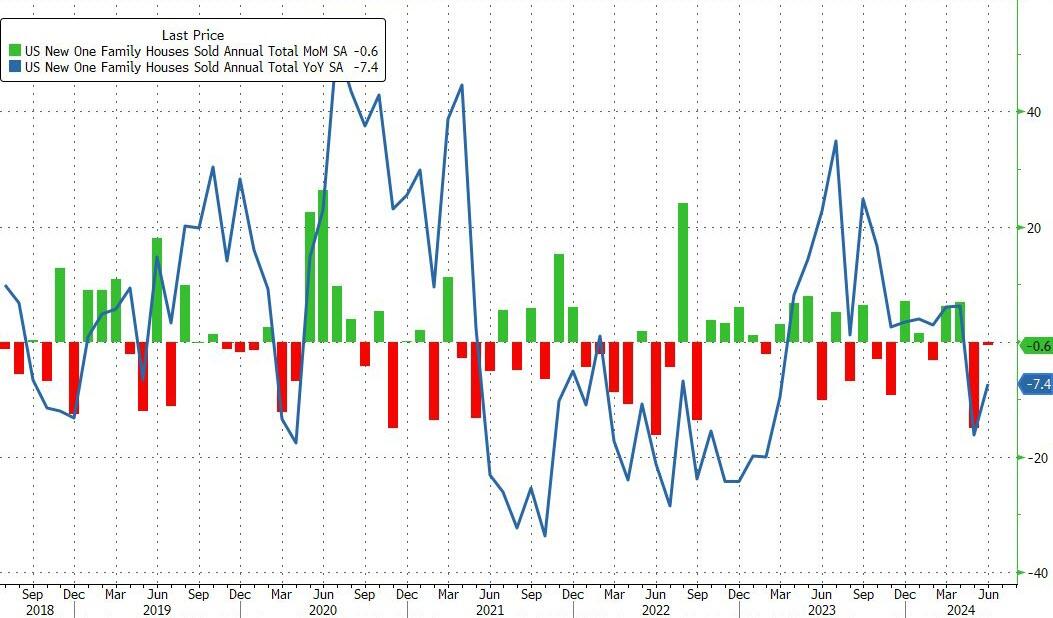

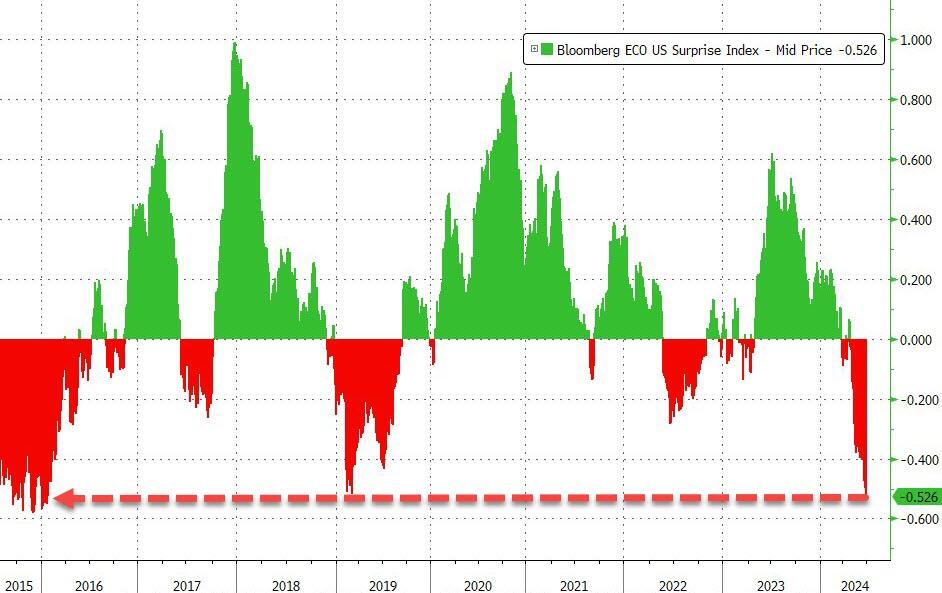

After a disappointing dump in existing home sales in June, new home sales just confirmed the slowdown, dropping 0.6% MoM (notably below the 3.4% MoM expected) and also saw a major downward revision in May from -11.3% MoM to -14.9% MoM. That leaves new home sales down 7.4% YoY…

Source: Bloomberg

That shift dragged the new home sales SAAR down to 617k – basically unchanged since 2016…

Source: Bloomberg

While the median new home price rose in June, it remains below the median existing home price…

Source: Bloomberg

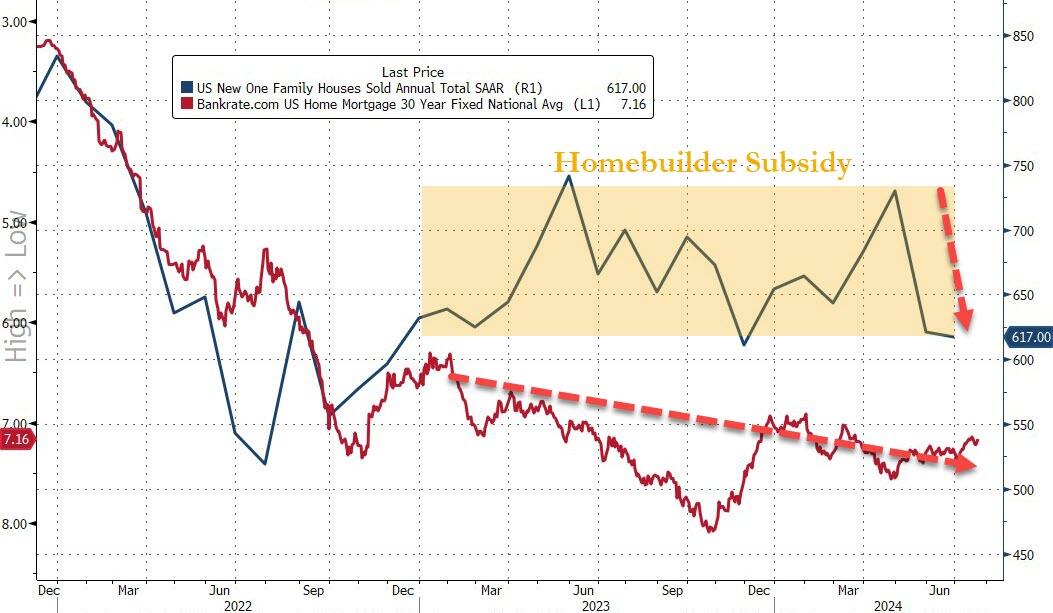

It appears the homebuilder subsidy fad is wearing off as mortgage rates show no signs of easing significantly…

Source: Bloomberg

Of course, none of this should be a surprise as homebuyer confidence has collapsed to an all-time record low…

Source: Bloomberg

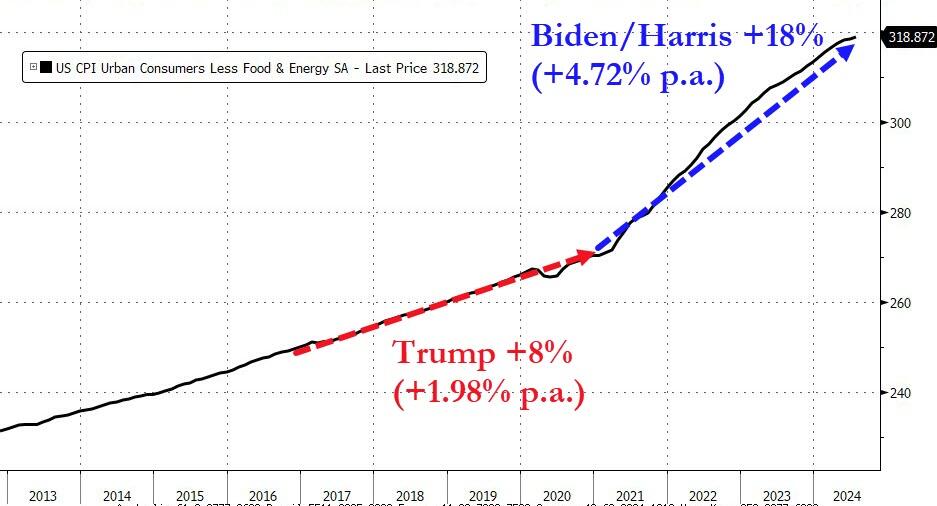

Will cutting rates help?

Probably not. Bidenomics is now called Harrisnomics (or Cacklenomics) since Harris as VP was the tiereaker in the US Senate. So, she holds some responsibility for the outrageous, wasteful spending in Washington DC.

Here is a chart of Non-commerciak net positions for US Treasuries, currently showing more bailing out of Treasury positions. Has the world sours on DC’s fiscal train wreck and The Fed?

Of course, budget deficits are a disaster with Biden/Congress spending like drunken sailors in port and showing no signs of letting up. The good news? At least a court struck down Biden’s illegal cancelation of student debt (a desperate attempt to win votes). That would have spiked the budget deficit.

As I pointed out yesterday, the UNFUNDED entitlements promised by the Federal government are now larger than that total national assets (business, household). In other words, if the US liquidated ALL assets, they couldn’t pay off the UNFUNDED entitlements. And good luck taking away the entitlements!

MMT is mostly magic! The Federal Reserve relies on “The Power of Magic” to fool people. For example, the massive increase in money printing following Covid and Biden’s disastrous economic policies (or FOLLICIES).

But there is also a fair amount of hypocrisy in the non-Austrian (e.g., mainstream, Keynesian, monetarist) critiques of MMT by mainstream economists. The truth is that most, if not all, of these economists share the same faulty presuppositions regarding what is euphemistically called “monetary policy.” The difference between mainstream and MMT economists is usually one of degree, not of kind.

Alan Greenspan, former Federal Reserve chairman (1987–2006) and most definitely not an MMT proponent, made a very MMT-friendly claim: “The United States can pay any debt it has because it can always print money to do that, so there is zero probability of default.” While this is literally true, and points to the fact that the nominal debt and dollars are not the issue, it overlooks the distortionary consequences from this manipulation on the entire structure of production. Nevertheless, such a claim is often also repeated by proponents of MMT, as if it contains some magic missing ingredient to unlock greater stores of wealth.

In fact, MMT provides a warranted critique to other schools of economic thought that share an underlying premise while not arriving at the same conclusions. That assumption is so-called monetary policy—that governments via a central banking monopoly ought to be the sole entity that issues and controls money as a policy instrument. The dubious justifications for this are that it provides greater economic stability and expansion of money and credit according to the needs of trade. (Both of these are false, theoretically and empirically.) That said, MMT and mainstream economics both share this presupposition, assuming the validity of monetary policy.

As an example of presenting the broad mainstream on the definition of “monetary policy,” the popular financial encyclopedia Investopedia has previously stated the following:

“Monetary policy is a set of tools that a nation’s central bank has available to promote sustainable economic growth by controlling the overall supply of money that is available to the nation’s banks, its consumers, and its businesses. . . . The main weapon at its disposal is the nation’s money (italics added).”

The casual use of the word “weapon” is apt. In the hands of a state monopoly, money can indeed be “weaponized.” Inflation is the artificial expansion of money and credit that has the effect of transferring wealth from all money holders to the inflater(s). This may be done under the guise of “policy”—appearing official, orderly, and legitimate—but it involves elites in power taking actions that would otherwise be criminal behavior (e.g., fraud and counterfeiting).

Even without the ethical-philosophical discussion on whether changing the money supply is fraudulent, economically, the consequences remain. The inflation of money and fiduciary media (artificial credit) causes economic miscalculations and boom-bust cycles, distorts the structure of production, encourages capital consumption, undermines the actions of individuals, discourages saving, transfers wealth from the citizenry to the government and those who are politically connected, affects money’s purchasing power, and has a whole host of other unintended effects. All this, of course, is done under the legal cover of “policy” to achieve “stable economic growth,” as well as ambidextrously maintaining the false dichotomy between full employment and inflation.

Enter MMT, which takes “monetary policy” concepts to their logical conclusions, demonstrating the consequences in a striking way, and mainstream economists quickly want to disassociate themselves from this “crazy” new idea. People may not appreciate some MMTers claiming what they do about inflation, government spending, full employment, and debt; yet politicians and monetary bureaucrats sure seem to act like they believe MMT.

MMT correctly observes that government—through a balance of taxation, deficit spending, inflation, and monetary policy—attempts to centrally control an economy and does, in fact, direct real resources toward its ends. These are common policy tools of the state and central banks. MMT would just like to leverage these tools to a greater extent and direct them toward different ends. Likewise, Investopedia had further clarified:

“The Federal Reserve is in charge of monetary policy in the U.S. The Federal Reserve (Fed) has what is commonly referred to as a dual mandate: to achieve maximum employment while keeping inflation in check.”

Is this above statement not basically a statement of the goals of MMT? Other economic schools of thought that accept the underlying presuppositions of the necessity of monetary policy are not fundamentally in disagreement with MMT on this point; in fact, they are in fundamental agreement. This undermines the ability of these schools to effectively deliver a fundamental critique of MMT rather than just disagreements about how and to what extent monetary policy is to be utilized.

Economic criticism on these points—whether from MMT to the “other side” or from the “other side” to MMT—involves inconsistency. By condemning the other, they condemn themselves because they share core presuppositions. The existence of MMT is effectively a reductio ad absurdum of so-called monetary policy. MMT reasonably asks: What if we did more of the same? Obviously, the degree to which something is done can be critiqued without abandoning the whole thing, but the flawed assumptions are twofold: (1) that there is “just the right amount” of monetary policy and (2) that there are certain enlightened experts who know what it is and only need monopoly over the money supply to achieve it.

Whether MMT or otherwise, proponents of so-called monetary policy essentially believe that money is a policy instrument (or weapon) to be wielded by government elites to rearrange prices, resources, and the structure of production contrary to the demonstrated preferences of millions of individuals. Therefore, the United States has been under a monetary policy regime of “stabilizers” who have argued about how to implement a fundamentally flawed “policy” for over a century.

Whenever this fails and destabilizes the economy, we are treated to critics who blame the free market and deregulation and who want to use monetary policy to “run the economy” differently.

Instead, we ought to abandon the fraud of monetary policy and heed the words of F.A. Hayek concerning the results of monetary policy that led to America’s Great Depression:

“We must not forget that, for the last six or eight years [up to 1932] monetary policy all over the world has followed the advice of the stabilizers. It is high time that their influence, which has already done harm enough, should be overthrown.”

Mortgage rates have actually risen as The Fed has increased M2 Money printng. Like DARK magic.

This isn’t the Sahm’s Club that is good fpr consumers. This is the club which crushes consumers. Better to be called Joe’s Club after our demented President Joe Biden.

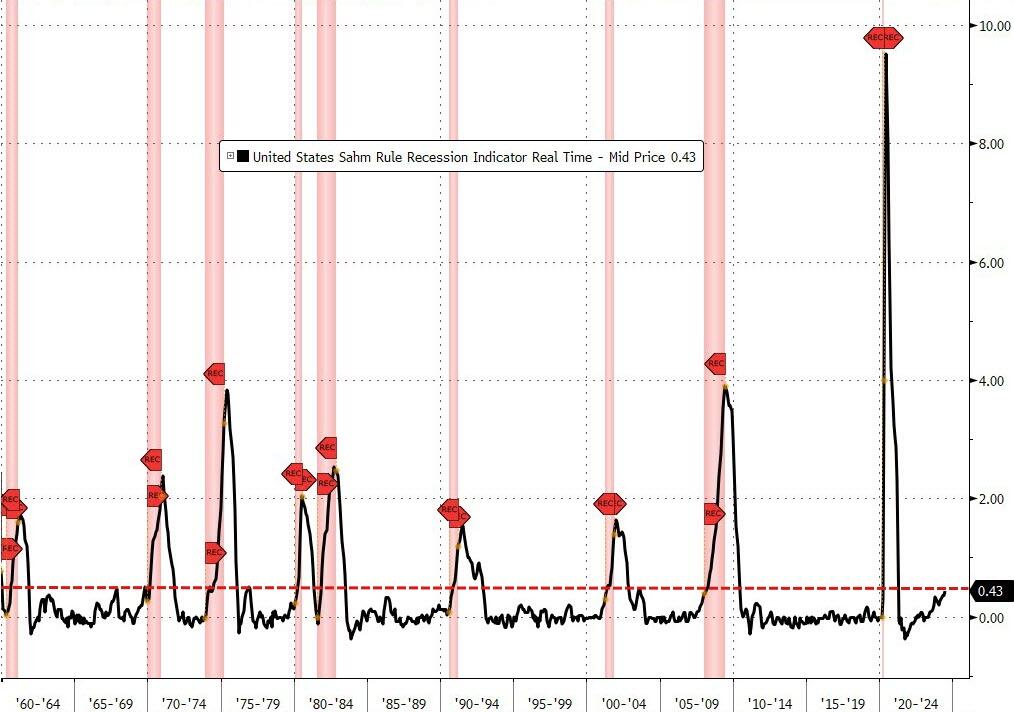

This uptick triggers the Sahm Rule, a real-time recession indicator, suggesting that the US economy is in, or is nearing, a recession. The Sahm Rule, developed by former Fed economist Claudia Sahm, is designed to identify the start of a recession using changes in the total unemployment rate.

According to the rule, a recession is underway if the three-month moving average of the national unemployment rate rises by 0.50 percentage points or more, relative to its low during the previous 12 months. With the June 2024 U-3 rate of 4.1 percent, the average of the last three months being 4.0 and the lowest 12-month rate of 3.5 percent in July 2023, this criterion has been met.

Sahm Rule indications (1960 – 2024)

Source: Bloomberg

Surveys had forecast the U-3 rate to hold steady at 4.0 percent in June, unchanged from May 2024. The seemingly small 0.1 percent uptick, however, carries substantial implications for the broader economy. One possible confounding effect of the signal is growth in the labor force: If the labor force grows rapidly and the economy does not generate enough jobs to match the increase, the unemployment rate might rise and the Sahm Rule may be triggered, even if overall employment is increasing.

The rise of initial claims over the past few weeks, and nine consecutive increases in continuing claims, support the June 2024 Sahm indication.

Source: Bloomberg

Equity futures were flat just after the release, while Treasuries rallied across all maturities.

In recent months, Fed Chairman Jerome Powell has indicated that “unexpected weakness” may prompt a start to an accommodative policy stance without the additional data sought regarding the pace of disinflation. Historically, an increase in unemployment rates and the onset of a recession have led to policy adjustments aimed at stimulating economic growth and mitigating job losses, and the reversal of the rate hikes which began in 2022 to mitigate the highest inflation in four decades has been widely anticipated.

While more data will be required to confirm the Sahm Rule indication, the impact of accelerating prices, interest rates at their highest levels since 2007, and commercially suppressive pandemic policies have probably caught up with US producers and consumers.

Biden’s version of Sahm’s Club. Where the economy tanks and all he and his wife Jill care about is staying in Power. Perhaps we should call the sagging US economy “Joe’s Club.”

Gimme two steps to sell my house. Are people getting out of dodge?? Calfornia Gpvernor “Greasy Gavin” Newsom sold his Sacramento home and moved to Marin County for better schools. Sacrramento active housing inventory is up 65.6% YoY.

Active housing inventory in May is up 27.5% YoY nationally, with Denver leading at 75.2% YoY. I highlight Columbus Ohio at +32.9% since that is where I live.

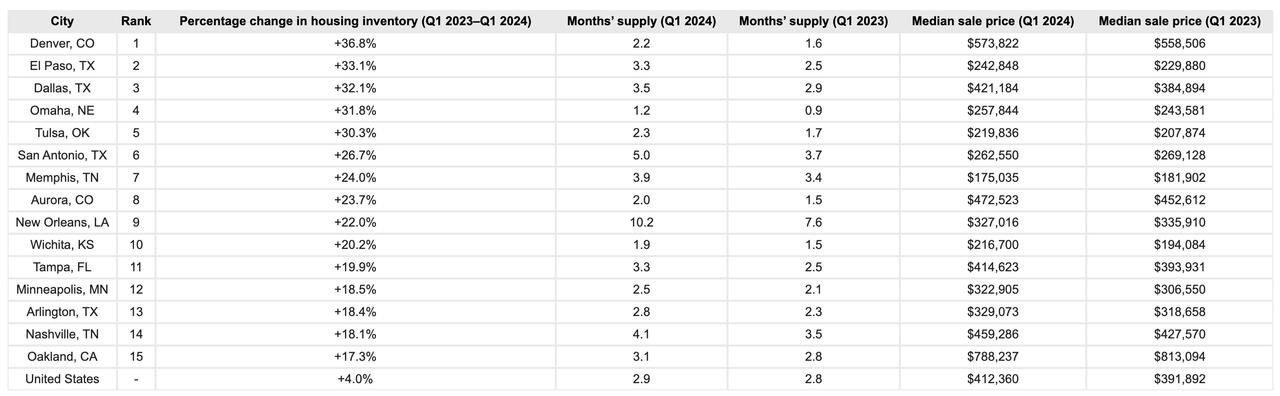

A new report from Construction Coverage has revealed where the largest increases in real estate inventory in the U.S. are taking place.

The report notes that the current housing shortage—which is now estimated to be between four million and seven million homes—can trace its beginnings to long before the COVID-19 pandemic. In the 10 years following the Great Recession, the United States constructed fewer new homes than in any other decade since the 1960s.

They write that the lack of housing affects certain areas more severely than others. Researchers ranked locations based on the percentage change in the average monthly housing inventory—the total number of active listings plus pending sales at the end of the month—between Q1 2023 and Q1 2024.

Data from a national level showed that U.S. housing inventory decreased from more than two million in 2012 to a low of approximately 630,000 at the start of 2022.

Over the same period, months’ supply—a measure of how long it would take existing inventory to sell if no new homes came on the market—plummeted from a national high of 7.5 months to a historic low of 1.1 months, the report adds.

It also noted that inventory has rebounded slightly since early 2022: throughout the first quarter of 2024, the national inventory hovered around 970,000 homes for sale, marking a 4.0% year-over-year increase.

Despite this uptick, existing inventory would sustain the current sales pace for just 2.9 months—a marginal increase from the 2.8 months’ supply recorded last year.

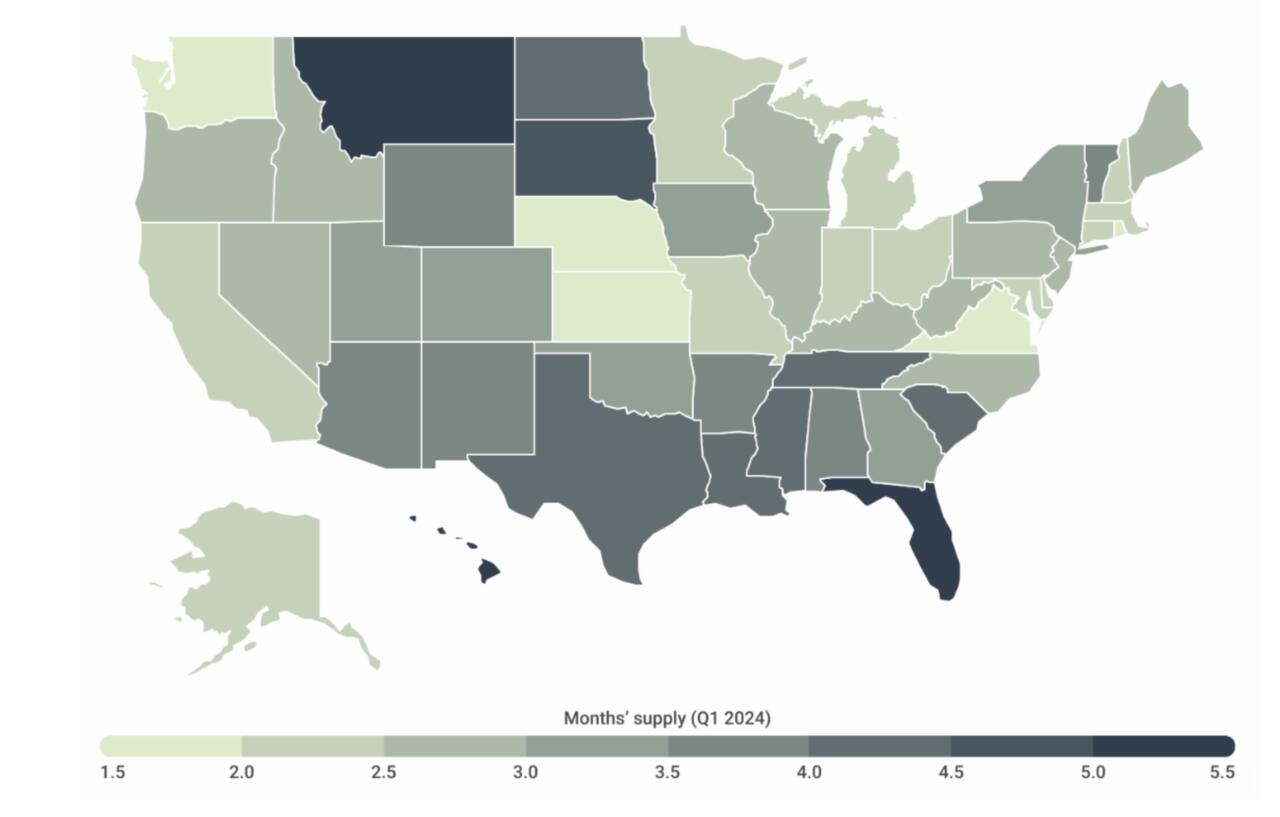

The report broke down trends by cities and states, finding that as of the first quarter of 2024, states with the lowest levels of supply are concentrated in and around the Midwest (such as Kansas with 1.5 months of supply) and the Northeast (including Rhode Island with 1.8 months of supply).

However, Washington also stands out for having some of the lowest levels of available housing nationally, with just 1.9 months of supply.

In contrast, several states in the South, led by Florida (5.2 months of supply), along with Hawaii (5.2 months) and Montana (5.1 months), present notably more favorable conditions for buyers.

Among the nation’s largest cities, Denver, El Paso, and Dallas recorded the largest year-over-year increases in housing inventory. At the opposite end of the spectrum, Las Vegas, Raleigh, and Chicago recorded the biggest declines.

The data is hardly a 2008-style collapse, but that doesn’t mean it isn’t noteworthy.

While the ‘turning of the tide’ still remains muted, the housing market is so large it rarely corrects swiftly. It’s important to notice, however, that rising inventory ticking higher – combined with mortgage rates now over 7% – could easily be telegraphing a correction in prices heading into 2025.

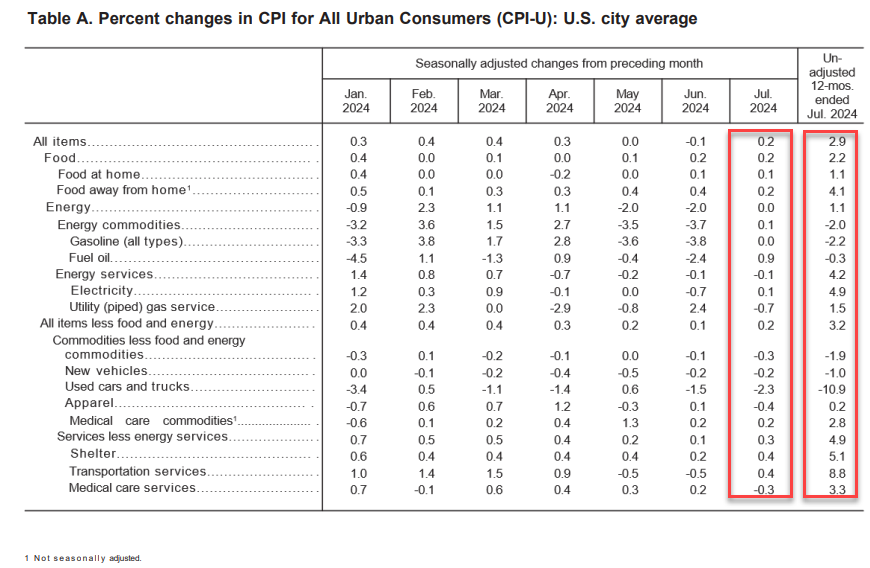

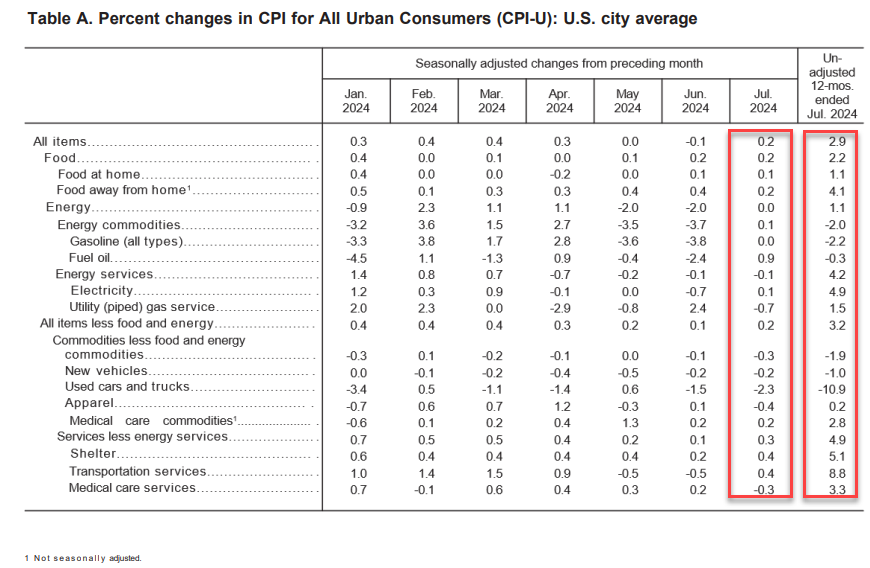

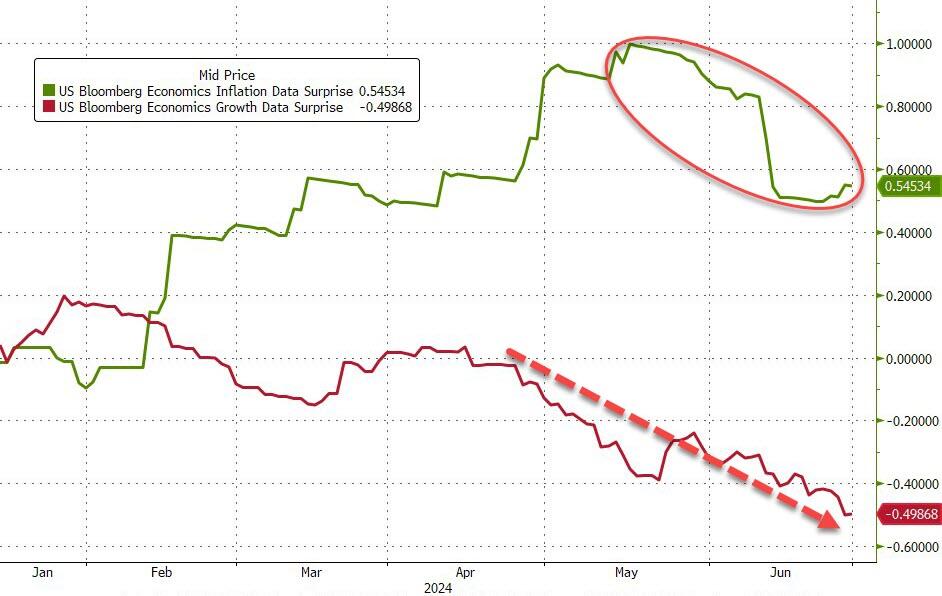

…which, many believe, will also drag down inflation (and it has been)…

Source: Bloomberg

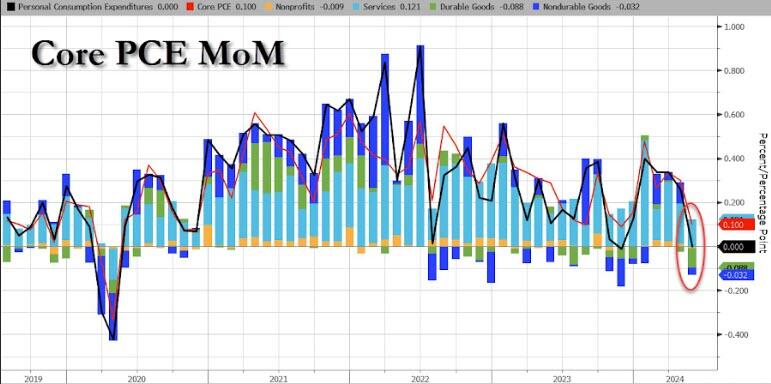

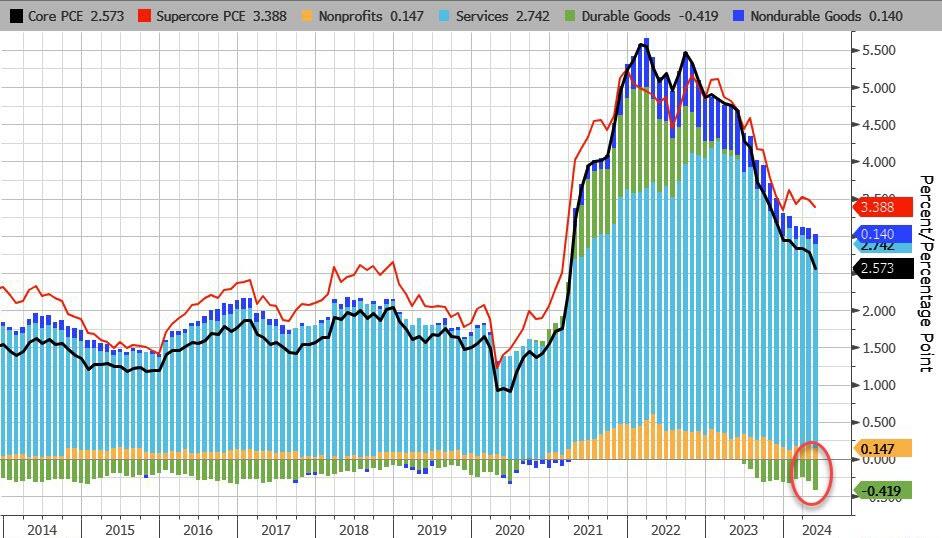

Today, we get to see The Fed’s favorite inflation indicator – Core PCE – which rose 0.1% MoM in May (after a revised +0.3% MoM for April) and in line with expectations. The headline PCE Price Index was unchanged MoM as expected as Durable Goods deflation trumped surging Services costs…

Source: Bloomberg

On a YoY basis, both headline and core PCE declined…

Source: Bloomberg

On a YoY basis, Durable Goods deflation is at its strongest in at least a decade…

Source: Bloomberg

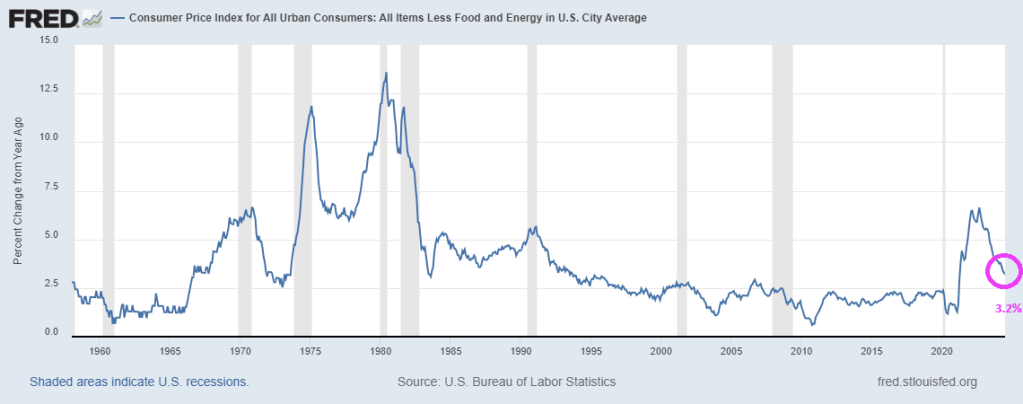

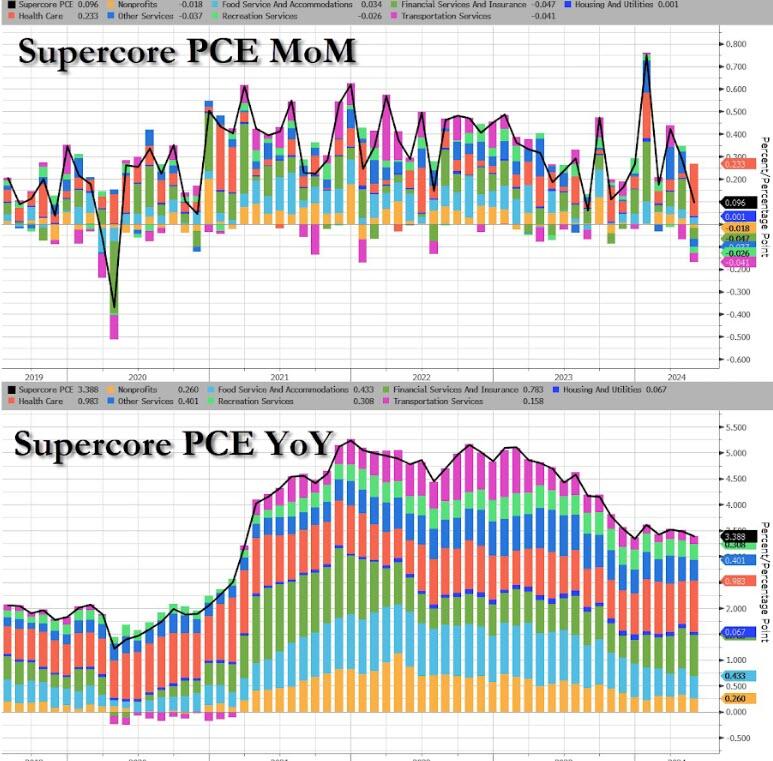

More notably, the so-called SuperCore PCE rose 0.1% MoM, which saw YoY slow to 3.39%… which is awkwardly stagnant at elevated levels…

Source: Bloomberg

That is the 49th straight monthly rise in SuperCore prices with Healthcare costs soaring…

Source: Bloomberg

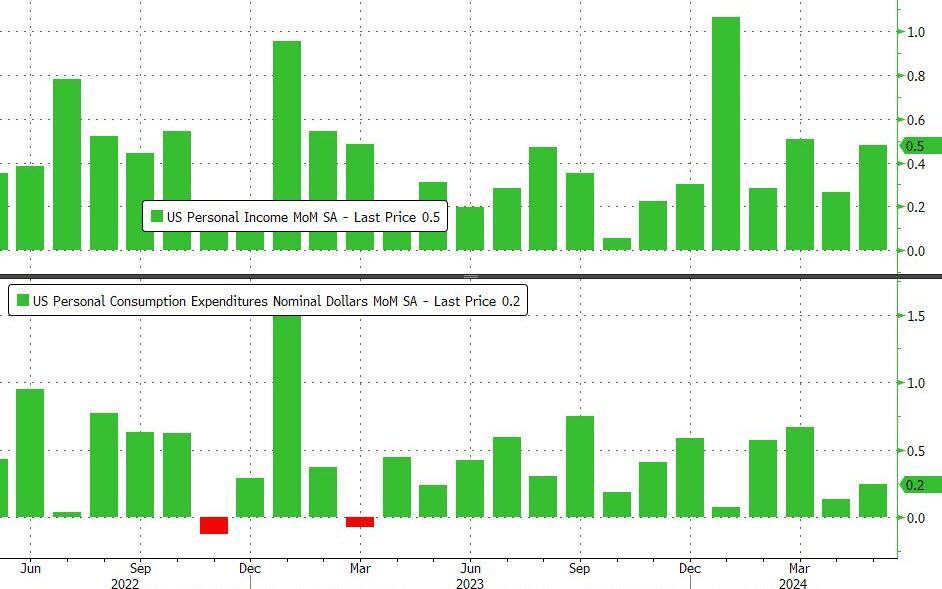

On a MoM basis, Income grew more than expected (+0.5% vs +0.2% exp) while spending rose less than expected (+0.2% MoM vs +0.3% exp)

Source: Bloomberg

Which accelerated both income and spending on a YoY basis (with the latter outpacing the former, of course)…

Source: Bloomberg

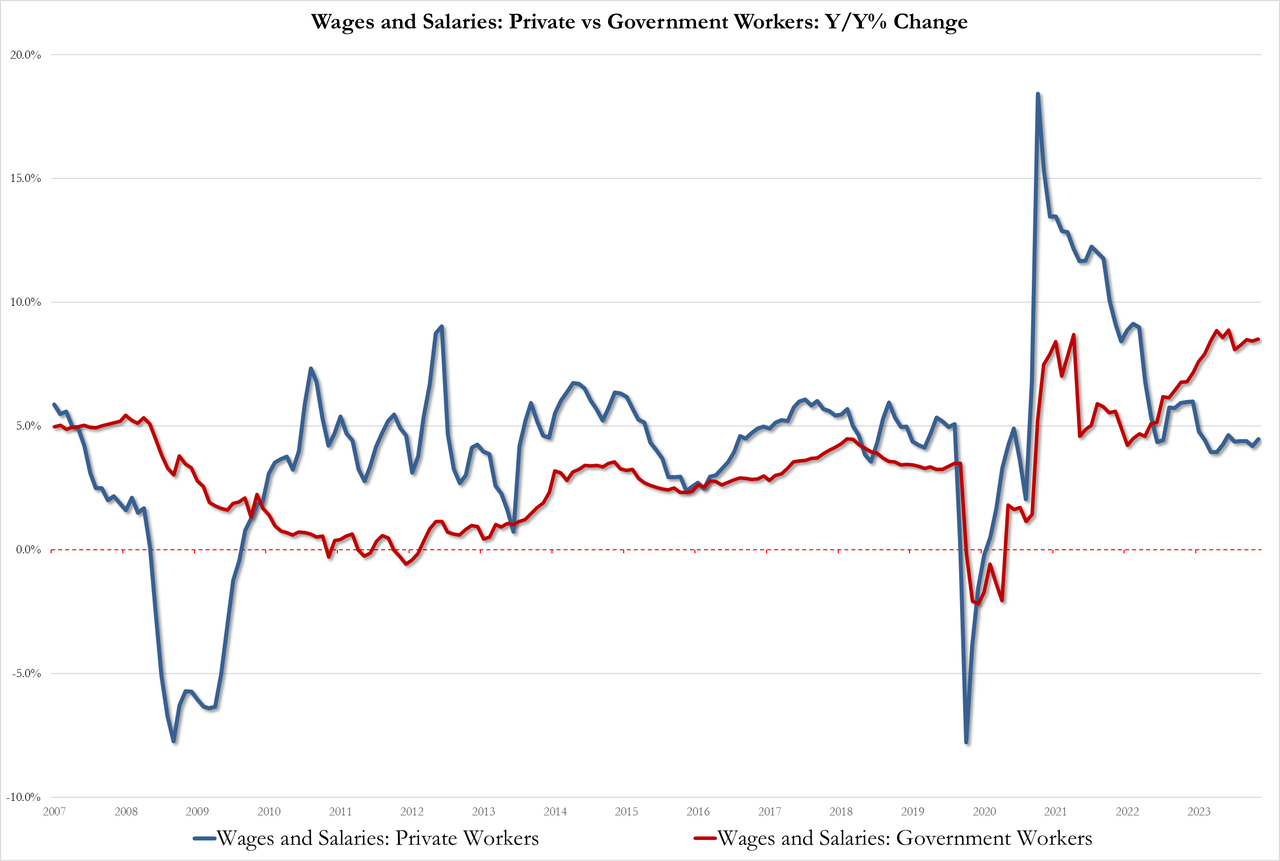

With wage pressures rising once again…

Government 8.5%, up from 8.4% but below the record high of 8.9%

Private 4.5% up from 4.2%

Source: Bloomberg

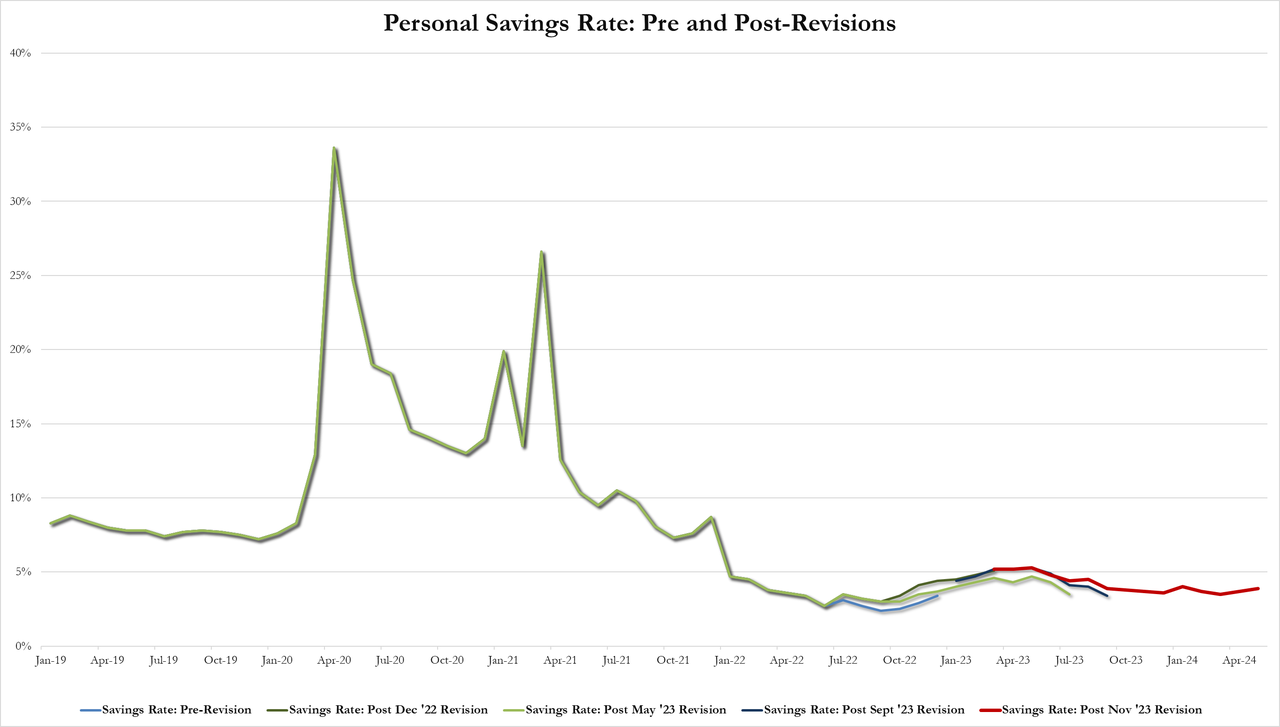

And after a series of revisions, the savings rate ticked up to 3.9% of DPI (from 3.7%) – the highest since January…

Source: Bloomberg

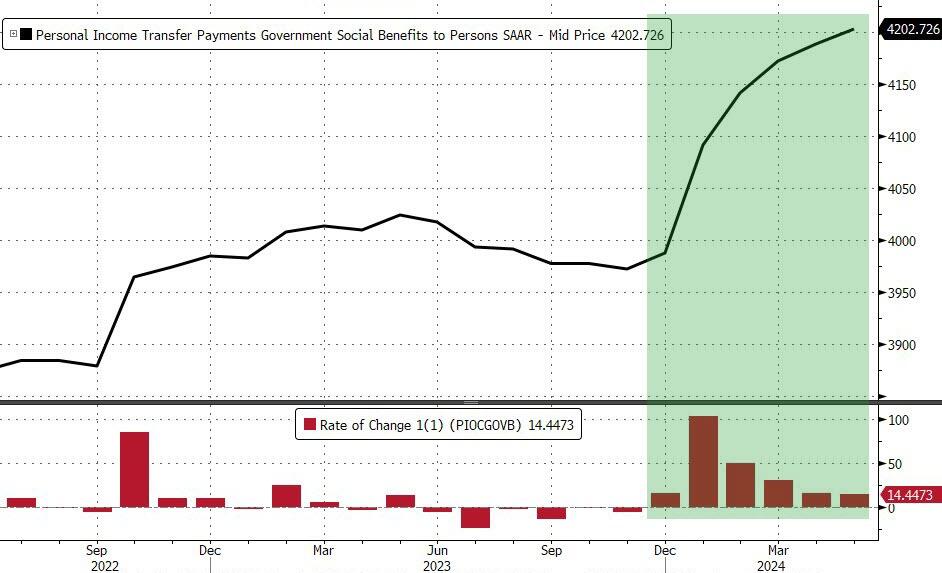

All of which takes place against a background of the sixth straight month of rising government handouts (well it is an election year after all)…

Source: Bloomberg

Finally, while acyclical inflationary pressures continue to drift lower, cyclical inflationary pressures remain extremely elevated…

Source: Bloomberg

A very mixed bag but nothing screams ‘automatic’ rate-cuts… and SuperCore refuses to budge.

But, below the hood of the last one we see some more interesting dynamics evolving as revenues and employment decline while prices re-accelerate…

Source: Bloomberg

This is the 25th straight month of contraction (sub-zero) for the Dallas Fed Services index and judging by the respondents’ comments, there is a clear place to point the finger of blame:

Poor national leadership and lack of confidence have eroded the business environment.

The Federal Reserve’s recent announcement of no rate cuts in the near future is concerning regarding the immediate and lag effect it could have on the local economy. We have received direct feedback from many of our clients in various industries, and they are increasingly concerned. They are freezing hires and spending, with many reducing spending. The primary reason is the economic stagnation locally and nationally affecting their businesses.

People are adjusting to new economic realities. Few are expecting salary increases and are instead making lifestyle adjustments to deal with higher living costs. Reality is also setting in for the apartment owners we serve. They understand rents aren’t going up and interest rates aren’t coming down. As rate caps expire and loans mature, lenders are having to adapt as well. Ultimately, a lot of private equity (much in the form of individual retirement savings put into syndications) is getting wiped out.

We need a rate cut before we will see any revenue improvement from home sales.

As elections draw near, the political environment worsens, creating more uncertainty in our business.

We feel inflation and fear of more inflation plus the rise in cost of living are holding consumers back. Hopefully we will adapt to the new realities soon.

Customers are concerned about the election, so they are holding off on large purchases.

The lack of building activity is shutting down the appliance industry.

Affordability has become an ever-increasing problem for new car dealers. The price increases of new cars combined with higher interest rates have put new cars out of reach for more and more people.

[Car] inventories continue to swell, and interest rates remain high. Our grosses are off, and margins continue to decline. Profits are down 20 percent from the prior year.

The economy is slowing. The consumer is more cautious and more reluctant to purchase at higher prices and payments.

And finally, this seemed to sum up just how business-owners feel in general about the current occupant of The White House:

“Our outlook depends heavily on the presidential election.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.