No, Joe Biden isn’t Joltin’ Joe Di Maggio (the Yankee Clipper). Joe Biden is a Socialist who loves government and hates free markets. I feel like Biden and his junta are emuilating the old Soviet Union and Communism. Those of us who still love free markets are back on the chain gang.

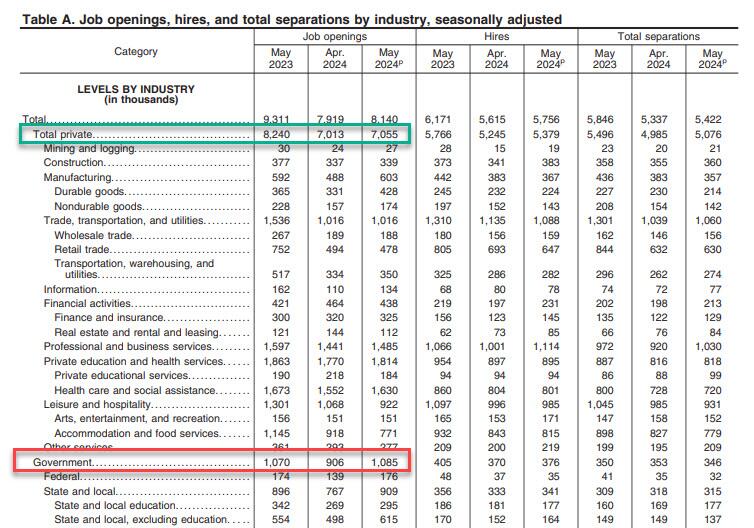

After two months of sharp declines in the number of job openings, moments ago Biden’s highly politicized Department of Labor reported that in May, the number of job openings unexpectedly spiked by a whopping 221K, to 8.140 million – far above the 7.950 million estimate – from a downward revised April print of 7.919 million, down 140K from the original print of 8.059 million.

Job revisions aside, there was only a 2.8% increase in private sector job openings in May. On the other hand, nonproductive job openings (aka, government) were up a staggering 20% in May.

C’mon man, hiring government workers doesn’t grow the economy in an organic way. Just a Soviet way.

S&P Global US Manufacturing PMI rose from 51.3 in May to 51.6 for the final June print (down very modestly from the 51.7 flash print).

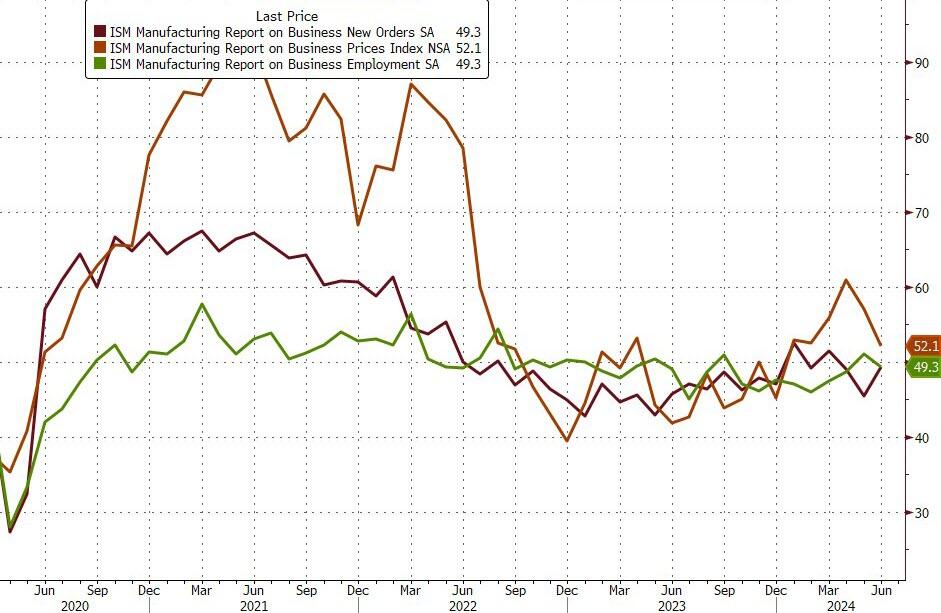

ISM US Manufacturing PMI dropped from 48.7 to 48.5 in June (well below the 49.1 expected)

Source: Bloomberg

Need more confusion…

S&P Global noted that higher supplier charges were signaled in June. Alongside rising labor costs, this resulted in a further marked increase in input prices. But, ISM saw Prices Paid plunge from 57.0 to 52.1, well below the 55.8 expected…

Source: Bloomberg

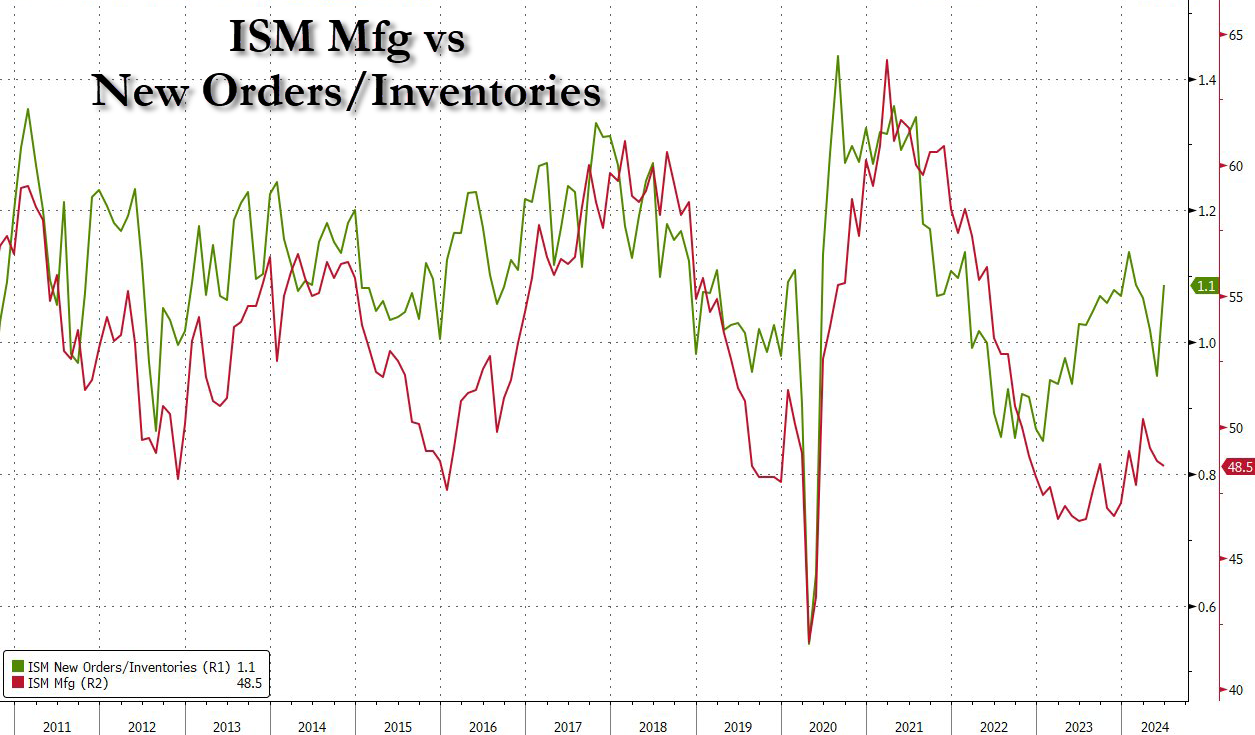

New orders rebounded in June but employment dropped back into contraction. On the bright side, Orders/Inventories (typically a leading indicator), ticked up in June…

“The S&P Global PMI survey shows US manufacturers struggling to achieve strong production growth in June, hamstrung by weak demand from domestic and export markets alike. Although the PMI has now been in positive territory in five of the first six months of 2024, up from just one positive month in 2023, growth momentum remains frustratingly weak.

“Factories have been hit over the past two years by demand switching post-pandemic from goods to services, while at the same time household and business spending power has been diminished by higher prices and concerns over higher-for-longer interest rates. These headwinds persisted into June, accompanied by heightened uncertainty about the economic outlook as the presidential election draws closer.“

Finally, despite the uptick, Williamson admits the truth under the surface of the survey:

“Business confidence has consequently fallen to the lowest for 19 months, suggesting the manufacturing sector is bracing itself for further tough times in the coming months.”

However, we are sure business owners everywhere were reassured by the commander-in-chief’s commanding performance in the debate last week. /sarc

Gimme two steps to sell my house. Are people getting out of dodge?? Calfornia Gpvernor “Greasy Gavin” Newsom sold his Sacramento home and moved to Marin County for better schools. Sacrramento active housing inventory is up 65.6% YoY.

Active housing inventory in May is up 27.5% YoY nationally, with Denver leading at 75.2% YoY. I highlight Columbus Ohio at +32.9% since that is where I live.

A new report from Construction Coverage has revealed where the largest increases in real estate inventory in the U.S. are taking place.

The report notes that the current housing shortage—which is now estimated to be between four million and seven million homes—can trace its beginnings to long before the COVID-19 pandemic. In the 10 years following the Great Recession, the United States constructed fewer new homes than in any other decade since the 1960s.

They write that the lack of housing affects certain areas more severely than others. Researchers ranked locations based on the percentage change in the average monthly housing inventory—the total number of active listings plus pending sales at the end of the month—between Q1 2023 and Q1 2024.

Data from a national level showed that U.S. housing inventory decreased from more than two million in 2012 to a low of approximately 630,000 at the start of 2022.

Over the same period, months’ supply—a measure of how long it would take existing inventory to sell if no new homes came on the market—plummeted from a national high of 7.5 months to a historic low of 1.1 months, the report adds.

It also noted that inventory has rebounded slightly since early 2022: throughout the first quarter of 2024, the national inventory hovered around 970,000 homes for sale, marking a 4.0% year-over-year increase.

Despite this uptick, existing inventory would sustain the current sales pace for just 2.9 months—a marginal increase from the 2.8 months’ supply recorded last year.

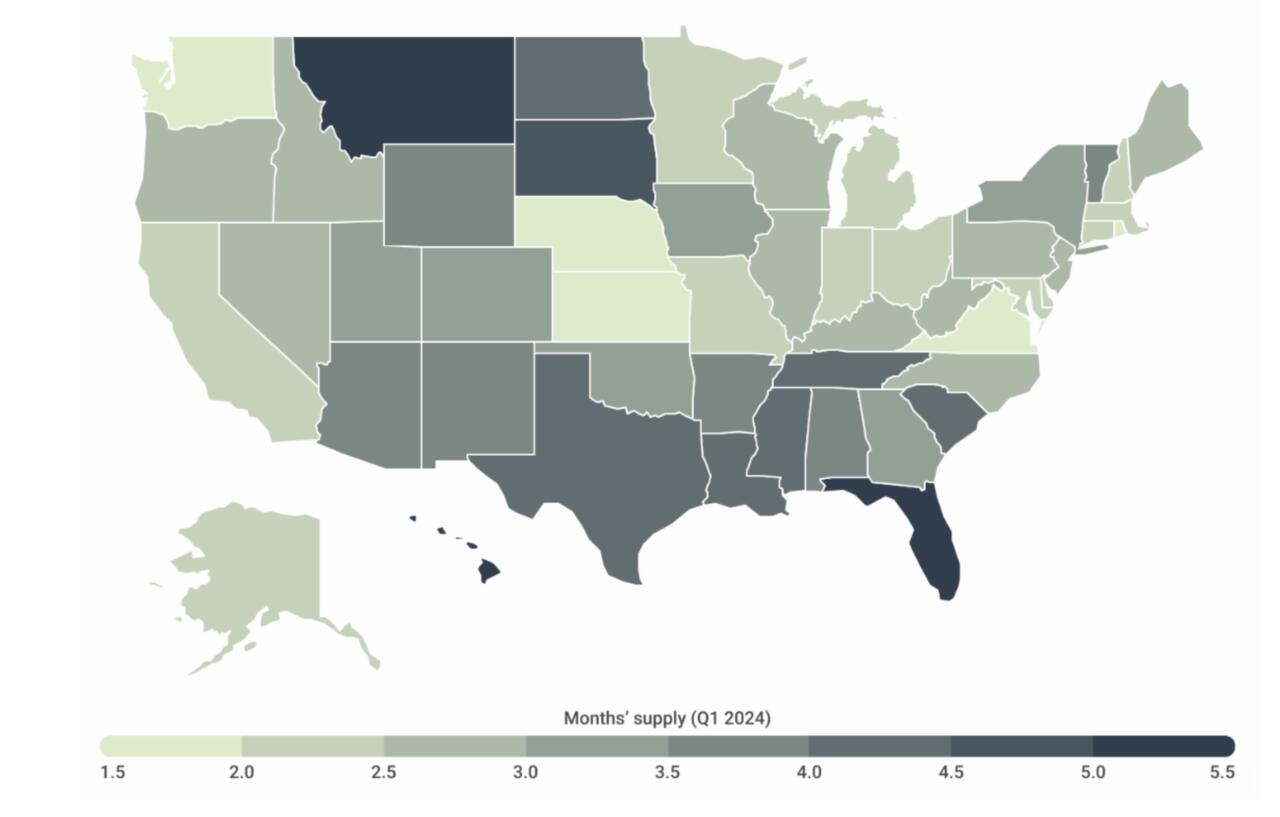

The report broke down trends by cities and states, finding that as of the first quarter of 2024, states with the lowest levels of supply are concentrated in and around the Midwest (such as Kansas with 1.5 months of supply) and the Northeast (including Rhode Island with 1.8 months of supply).

However, Washington also stands out for having some of the lowest levels of available housing nationally, with just 1.9 months of supply.

In contrast, several states in the South, led by Florida (5.2 months of supply), along with Hawaii (5.2 months) and Montana (5.1 months), present notably more favorable conditions for buyers.

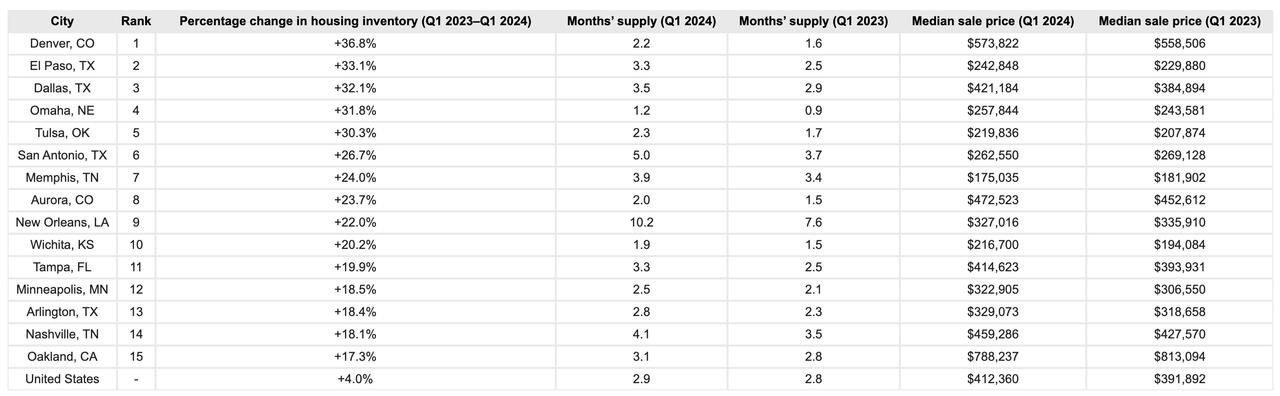

Among the nation’s largest cities, Denver, El Paso, and Dallas recorded the largest year-over-year increases in housing inventory. At the opposite end of the spectrum, Las Vegas, Raleigh, and Chicago recorded the biggest declines.

The data is hardly a 2008-style collapse, but that doesn’t mean it isn’t noteworthy.

While the ‘turning of the tide’ still remains muted, the housing market is so large it rarely corrects swiftly. It’s important to notice, however, that rising inventory ticking higher – combined with mortgage rates now over 7% – could easily be telegraphing a correction in prices heading into 2025.

During the first three months of 2023, U.S. office vacancy topped 20 percent for the first time in decades. In San Francisco, Dallas, and Houston, vacancy rates are as high as 25 percent. These figures understate the severity of the crisis because they only cover spaces that are no longer leased. Most office leases were signed before the pandemic and have yet to come up for renewal. Actual office use points to a further decrease in demand. Attendance in the 10 largest business districts is still below 50 percent of its pre-COVID level, as white-collar employees spend an estimated 28 percent of their workdays at home.

A new report from Moody’s offers yet another grim outlook that the commercial real estate downturn is nowhere near the bottom. Elevated interest rates and persistent remote and hybrid working trends could result in around 24% of all office towers standing vacant within the next two years. The office tower apocalypse will result in more depressed values that will only pressure landlords.

“Combining these insights, with our more than 40 years of historic office performance data, as well as future employment projections, our model indicates that the impact on office demand from work from home will be around 14% on average across a 63- month period, resulting in vacancy rates that peak in early 2026 at approximately 24% nationally,” Moody’s analysts Todd Metcalfe, Anthony Spinelli, and Thomas LaSalvia wrote in the report.

In a separate report, Tom LaSalvia, Moody’s head of CRE economics, wrote that the office vacancy rate’s move from 19.8% in the first quarter of this year to the expected 24% by 2026 could reduce revenue for office landlords by between $8 billion and $10 billion. Factor in lower rents and higher costs, this may translate into “property value destruction” in the range of a quarter-trillion dollars.

In addition to remote working trends, Moody’s analysts pointed out that the amount of office space per worker has been in a “general downward trend for decades.”

At the peak of the Dot-Com boom, office workers used an average of 190 sq ft. The figure has since slid to 155 sq ft in 2023.

“The argument for maintaining or even increasing remote work practices remains compelling for many businesses,” the analysts said, adding, “If productivity remains stable and costs can be reduced by forgoing physical office spaces, the rationale for mandating in-office attendance diminishes.”

Related research from the McKinsey Global Institute forecasts that office property values will plummet by $800 billion to $1.3 trillion by the decade’s end.

Moody’s expects vacancy rates to top out as office towers are demolished or converted to residential ones in the coming years.

“Right-sizing will continue over the next decade as the market shakes out less efficient space for flexible floorplans that support our relatively new working habits,” they said.

Earlier this year, Goldman analyst Jan Hatzius pointed out that a further 50% price decline would make office tower conversions financially sensible.

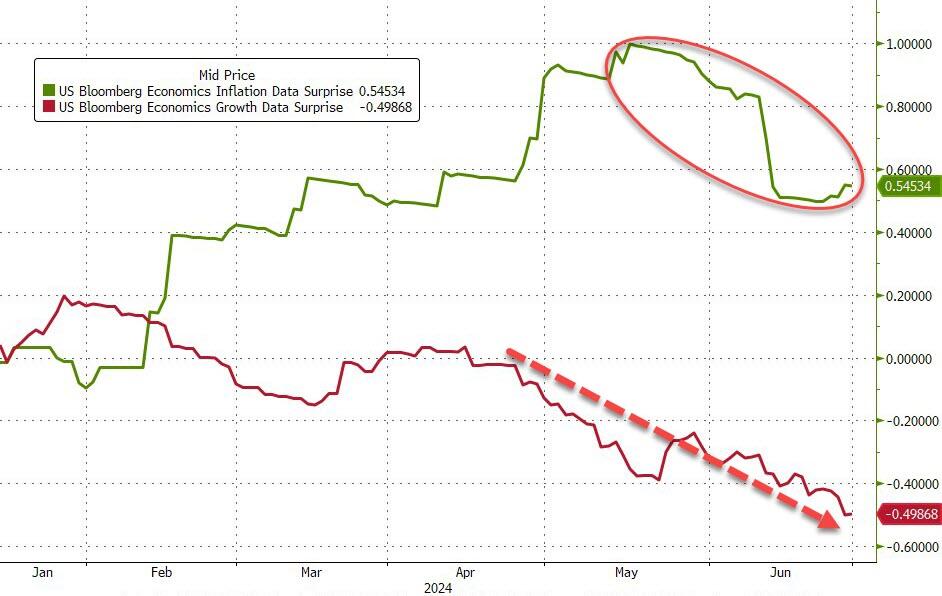

…which, many believe, will also drag down inflation (and it has been)…

Source: Bloomberg

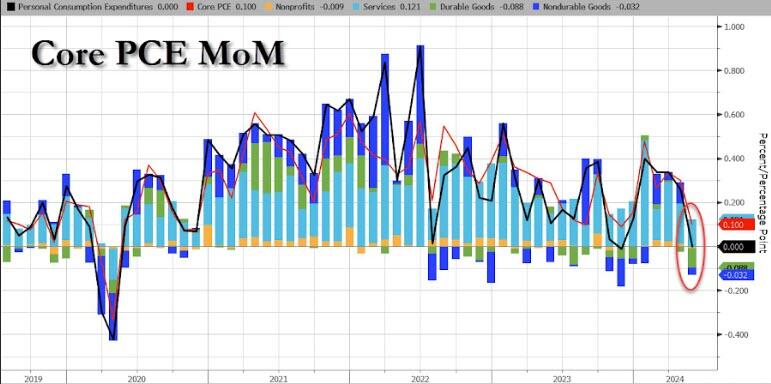

Today, we get to see The Fed’s favorite inflation indicator – Core PCE – which rose 0.1% MoM in May (after a revised +0.3% MoM for April) and in line with expectations. The headline PCE Price Index was unchanged MoM as expected as Durable Goods deflation trumped surging Services costs…

Source: Bloomberg

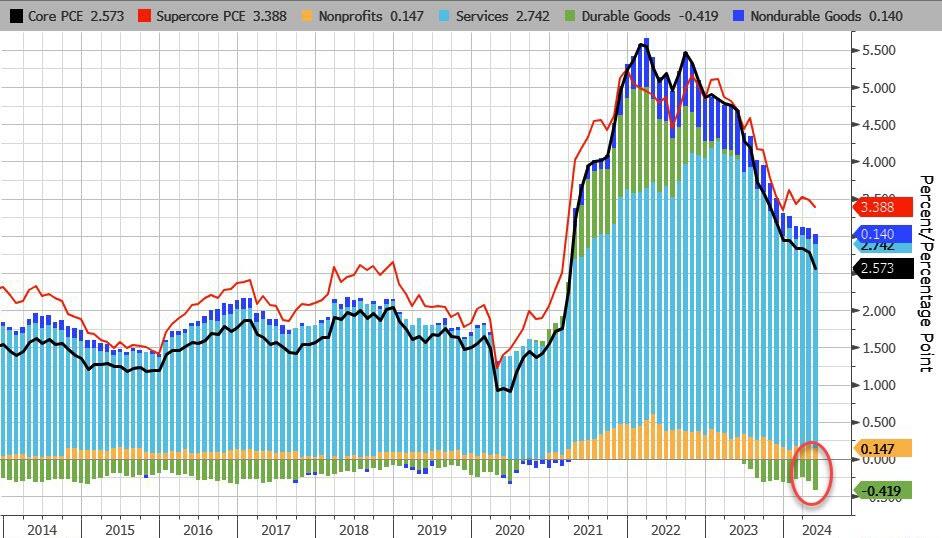

On a YoY basis, both headline and core PCE declined…

Source: Bloomberg

On a YoY basis, Durable Goods deflation is at its strongest in at least a decade…

Source: Bloomberg

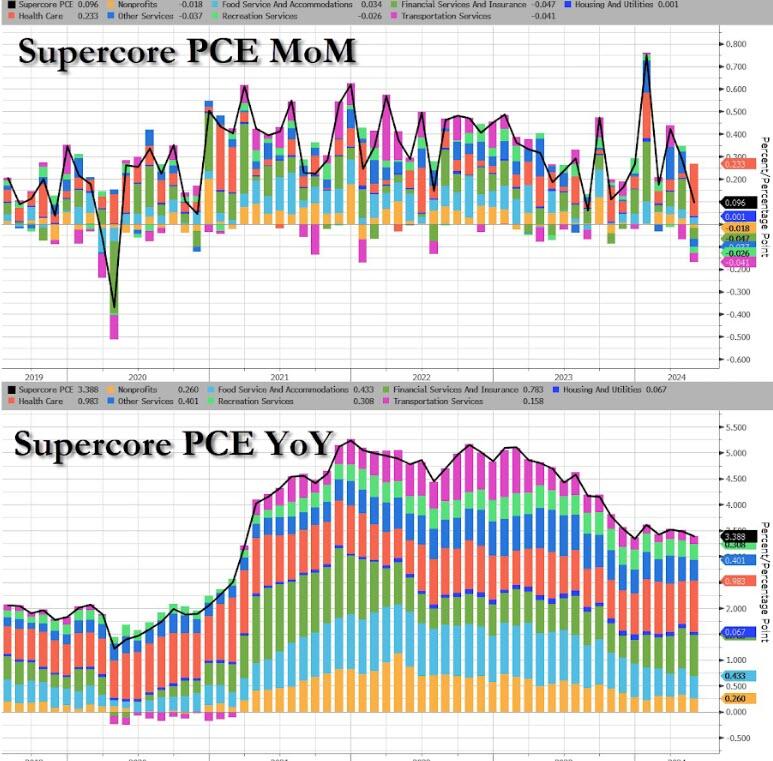

More notably, the so-called SuperCore PCE rose 0.1% MoM, which saw YoY slow to 3.39%… which is awkwardly stagnant at elevated levels…

Source: Bloomberg

That is the 49th straight monthly rise in SuperCore prices with Healthcare costs soaring…

Source: Bloomberg

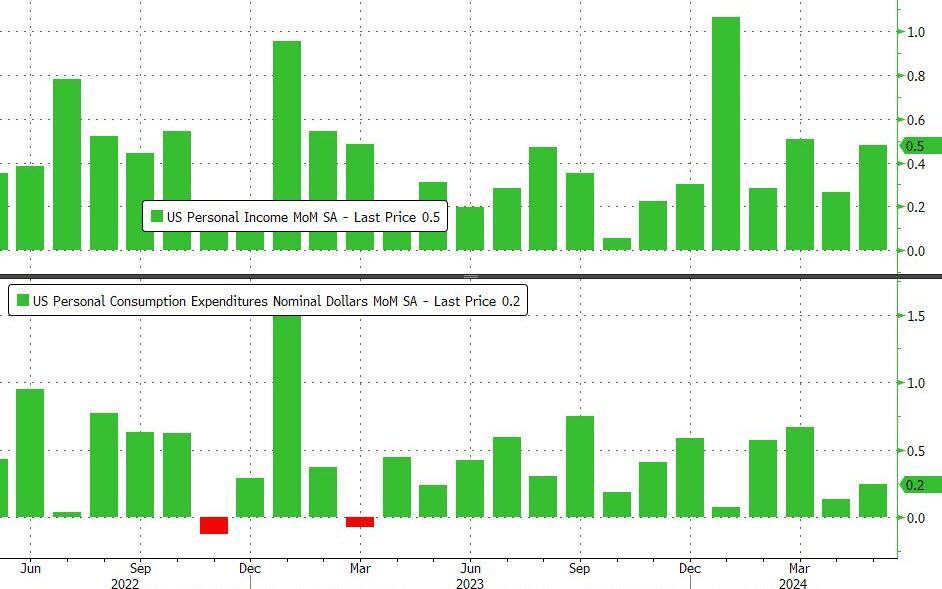

On a MoM basis, Income grew more than expected (+0.5% vs +0.2% exp) while spending rose less than expected (+0.2% MoM vs +0.3% exp)

Source: Bloomberg

Which accelerated both income and spending on a YoY basis (with the latter outpacing the former, of course)…

Source: Bloomberg

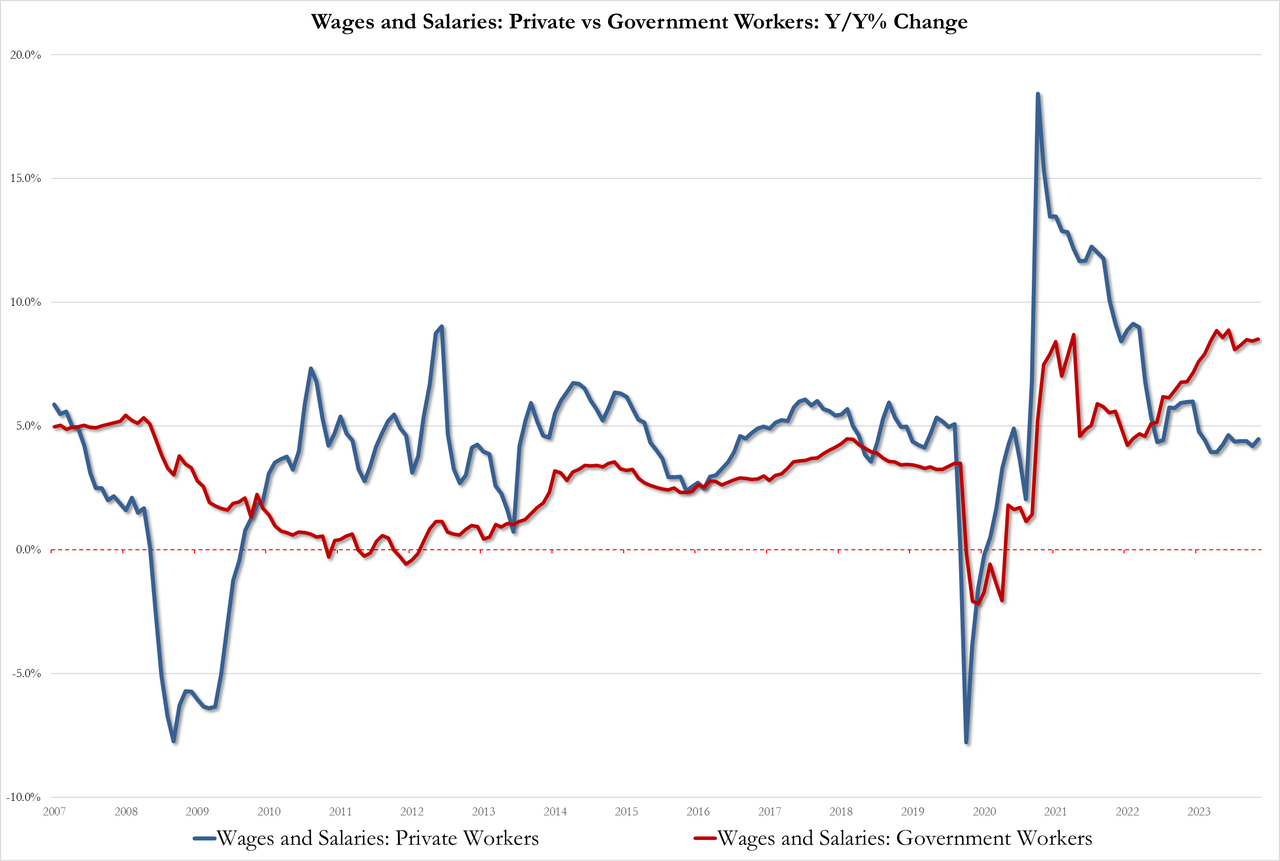

With wage pressures rising once again…

Government 8.5%, up from 8.4% but below the record high of 8.9%

Private 4.5% up from 4.2%

Source: Bloomberg

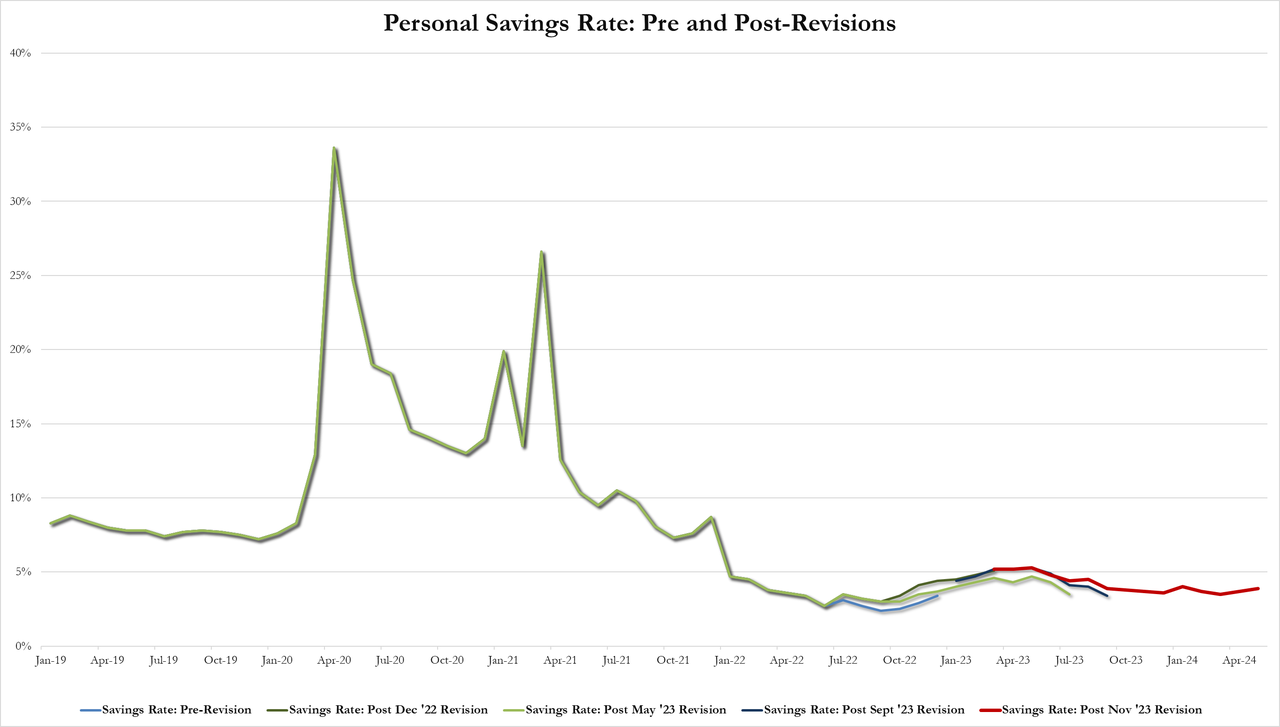

And after a series of revisions, the savings rate ticked up to 3.9% of DPI (from 3.7%) – the highest since January…

Source: Bloomberg

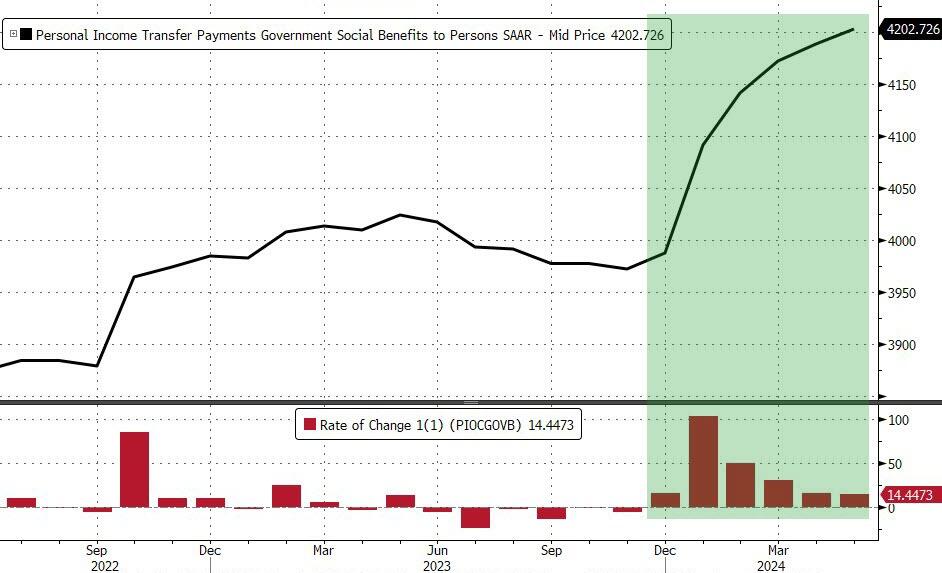

All of which takes place against a background of the sixth straight month of rising government handouts (well it is an election year after all)…

Source: Bloomberg

Finally, while acyclical inflationary pressures continue to drift lower, cyclical inflationary pressures remain extremely elevated…

Source: Bloomberg

A very mixed bag but nothing screams ‘automatic’ rate-cuts… and SuperCore refuses to budge.

It seems everything Biden touches turns to stone. This used to be called “The Medusa Touch” but I changing that to “The Biden Touch.” And that includes housing. Or we can simply sing along with the late Jimmy Buffet and “Wasting aways again in Bidenville.”

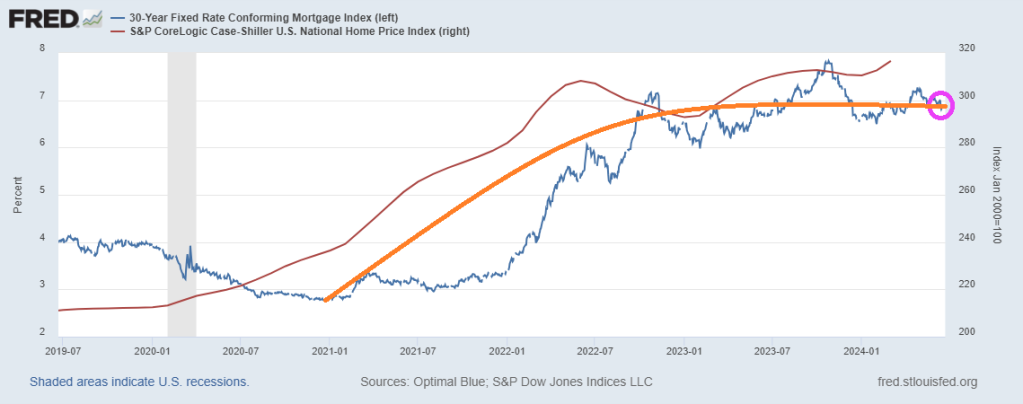

And near 7% mortgage rates aren’t helping (as The Fed continues its fight against Bidenflation).

New home sales crashed 11.3% MoM (after April’s 4.7% drop was revised up to a 2.0% MoM rise). That is the biggest MoM drop since Sept 2022…

Source: Bloomberg

This is the biggest YoY drop since Feb 2023, taking the SAAR down to the same level as it was in 2016…

Source: Bloomberg

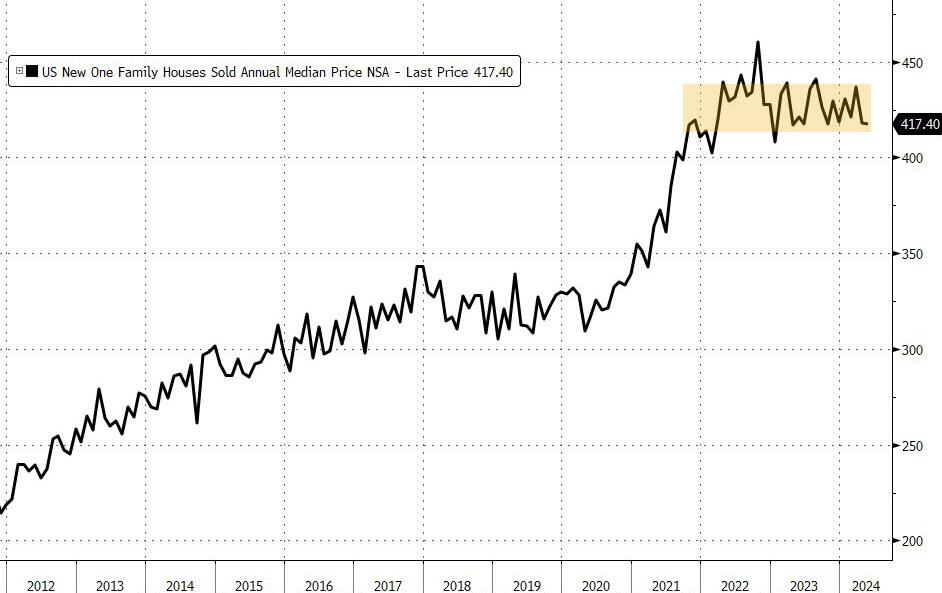

Median new home price fell 0.9% YoY to $417,400 – lowest since April 2023 – (with the average selling price at $520,000) with a big downward revision for April from $433k to $417k!…

Source: Bloomberg

For the first time since June 2021, median existing home prices are above median new home prices…

Source: Bloomberg

As BofA warned yesterday:

“The US housing market is stuck, and we are not convinced it will become unstuck anytime soon. After a surge in housing activity during the pandemic, it has since retreated and stabilized. We view the forces that have reduced affordability, created a lock-in effect for homeowners, and limited housing activity will remain in place through our forecast horizon “

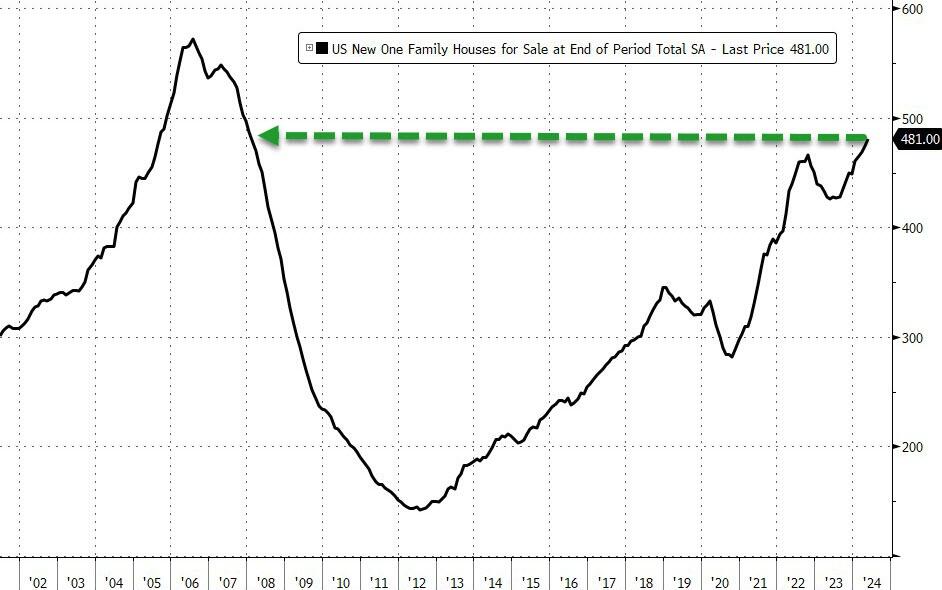

At the same time, the supply of available homes increased to 481,000, still the highest since 2008.

Source: Bloomberg

New home sales are catching down to the reality of mortgage rates continuing to hold above 7%…

Source: Bloomberg

It seems homebuilders finally gave up filling that gap in anticipation of an imminent Fed rate-cut to save the world.

Will Biden double down on his failed policies tonight in the CNN Presidential debate? Perhaps Joe can sing “Double Shot of Bidenomics.”

The jointly signed letter, first reported by Axios, says the economic agenda of U.S. President Joe Biden, a Democrat, is “vastly superior” to Trump’s, the former Republican president seeking a second term.

Read the source article from Reuters for the rest of the Marxist clown show. What Joe Stiglitz and other Leftist economists are cheerleading in the excessive post Covid spending spree that Biden and Congress went on. There is a different between a free market system and government directed spending, usually on large donors.

One source of crippling inflation under Biden is (wasteful) government spending, up 37.7% under Biden. Federal debt is up a nauseating 50% under Biden. These levels of spending and debt are NOT sustainable!

Another souce of inflation under Biden has been The Federal Reserve. With Covid. The Fed entered like gangbusters dropping their target rate to 25 basis points and massively increasing their balance sheet. Call this BIDEN 1. Then to squelch inflation, The Fed raised their target rate and slowly started to unwind the balance sheet. We saw a slowing of inflation. Nothing to do with Biden, although I am sure he will take credit for it at Thursday’s debate with Trump.

Inflation was growing rapidly in Biden 1, but inflation started to slow (Biden 2) as The Fed rapidly raised their target rate.

S&P/Case-Shiller released the monthly Home Price Indices for April (“April” is a 3-month average of February, March and April closing prices). The pace of appreciation has slowed from the previous month, reflecting the toll of 7% mortgage rates and low inventory.

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 6.3% annual gain for April, down from a 6.5% annual gain in the previous month. The 10-City Composite saw an annual increase of 8.0%, down from an 8.3% annual increase in the previous month. The 20-City Composite posted a year-over-year increase of 7.2%, dropping from a 7.5% increase in the previous month. San Diego continued to report the highest annual gain among the 20 cities in April with a 10.3% increase this month, followed by New York and Chicago, with increases of 9.4% and 8.7%, respectively. Portland once again held the lowest rank this month for the smallest year-over-year growth, with a 1.7% annual increase in April. … The U.S. National Index, the 20-City Composite, and the 10-City Composite upward trends decelerated from last month, with pre-seasonality adjustment increases of 1.2%, 1.36% and 1.38%, respectively.

After seasonal adjustment, the U.S. National Index and 10-City Composite posted the same month-over-month increase of 0.3% and 0.5% respectively as last month, while the 20-City reported a monthly increase of 0.4%.

“For the second consecutive month, we’ve seen our National Index jump at least 1% over its previous all-time high,” says Brian D. Luke, Head of Commodities, Real & Digital Assets at S&P Dow Jones Indices. “2024 is closely tracking the strong start observed last year, where March and April posted the largest rise seen prior to a slowdown in the summer and fall. Heading into summer, the market is at an all-time high, once again testing its resilience against the historically more active time of the year.

“Thirteen markets are currently at all-time highs and San Diego reigns supreme once again, topping annual returns for the last six months. The Northeast is the best performing market for the previous nine months, with New York rising 9.4% annually. Sustained outperformance of the Northeast market was last observed in 2011. For the decade that followed, the West and the South held the top posts for performance. It’s now been over a year since we’ve seen the top region come from the South or the West.

Of course, Fed Money Printing is helping drive home price growth. Perhaps too much!

Here is Jerome Powell, Chairman of The Fed Bubble Blowing Machine!!

In politics, it is usually discussed whether you are better off today than 4 years ago. Well, not if you are a renter or need to buy a home with mortgage financing.

If you are a homeowner, you are better off in terms of home equty. With the Case-Shiller National home price index up 34% since Biden’s selection as President. That is the good news.

The bad news? Property taxes are soaring and home insurance rates are up.

The worst news? The 30 year conforming mortgage rate is up 147% under Biden.

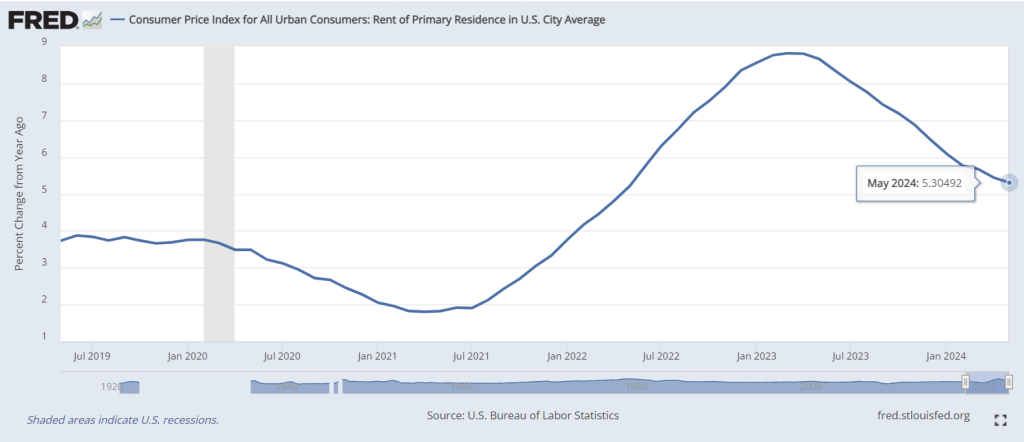

If you are a renter, you are worse off because of rising rents and the diffculty of transitioning to homeowership. Despite slowing, rental CPI is still growing at 5.3% YoY.

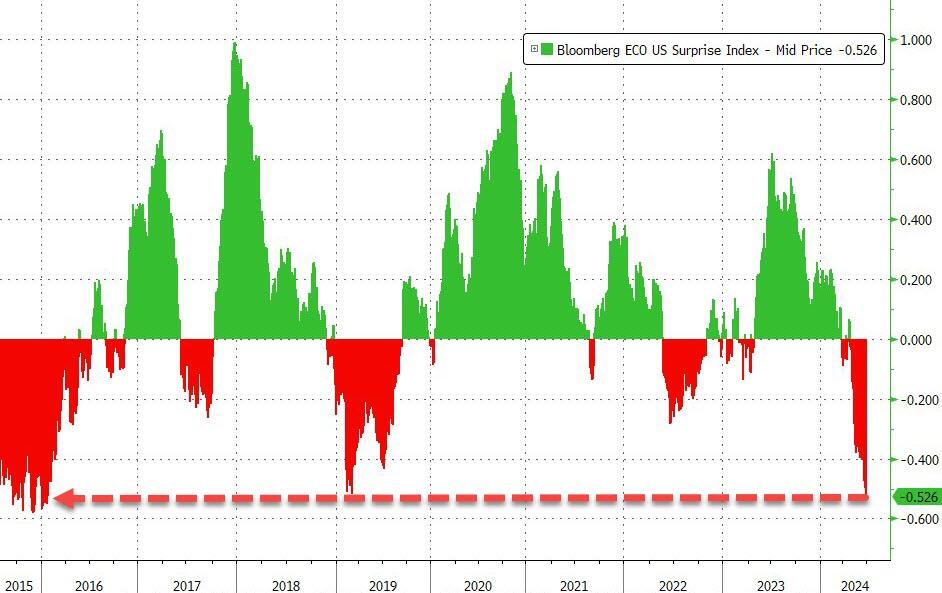

Well, perhaps bot a genuine surprise. We are aware that the US economy has been slowing as the massive fiscal and monetary stimulus from Covid is wearing out.

The economics surprise index slumped to -28.10, the lowest since 2022.

I feel like the US economy is experiening a Ragnarok change. With the giants (World Economic Forum/UN. etc) winning.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.