Bidenomics, the massive Federal spending spree that helped drive inflation to 40 year highs, is the most top-down Soviet-style command economy model imaginable.

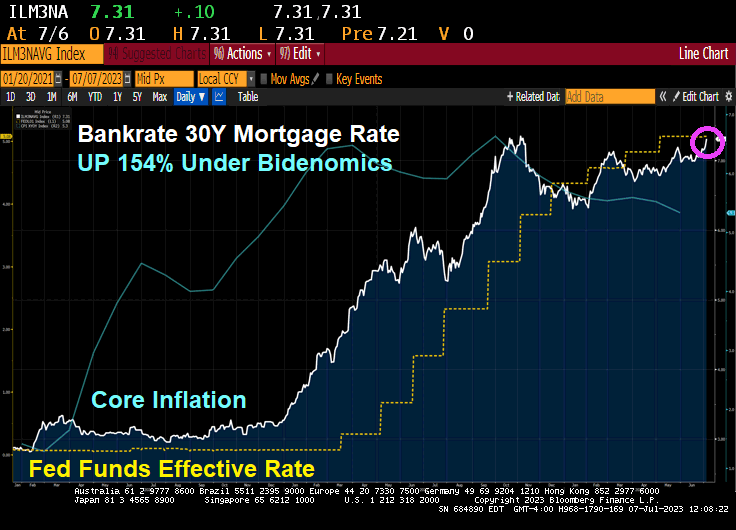

As The Fed battles Bidenflation, the 30-year mortgage rate has now risen to 7.31%, a far cry from 2.88% when Biden was installed as President. That is a 154% increase in the 30-year mortgage rate under Bidenomics.

As expected, The Federal Reserve raise their target rate by 75 basis points today. While that sounds like an inflation (blue line)-crushing rate hike, look at the slowly shrinking Fed Balance Sheet (gold line).

Of course, the risk of a recession (dark blue line) is on the increase.

Given the increasing likelihood of a recession, The FOMC’s Dots Project shows The Fed’s target rate increasing to 4.625% in 2023, then gradually declining to 2.5% in the long run.

Fed Funds Futures data points to a peak in May 2023.

Here is your weekend update on Treasury and Mortgage markets.

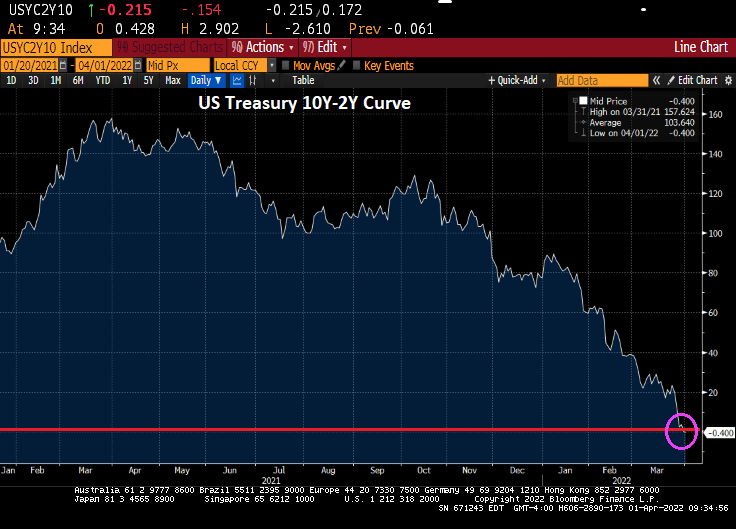

The current US Treasury 10Y-2Y yield curve just slipped further into reversion at -40.299 basis points, screaming impending recession. Oddly, The Federal Reserve has been leaving its balance sheet of Agency Mortgage-backed Securities (MBS) in tact (green line).

On the mortgage front, Bankrate’s 30-year mortgage rate index rose to 5.60% while the affordability-friendly 5/1 Adjustable Rate Mortgage (ARM) rate rose to 4.21%.

Currently, a 5/1 ARM borrower can save 139 basis points over the traditional 30-year mortgage rate.

Wasting away again in Biden/Pelosiville, looking for my lost inexpensive gasoline and food. Some people say that Putin is to blame, but we know its Biden/Pelosi’s fault.

The US Treasury 10Y-2Y yield curve just inverted, generally a precursor to a recession. Called it, nothing but net!

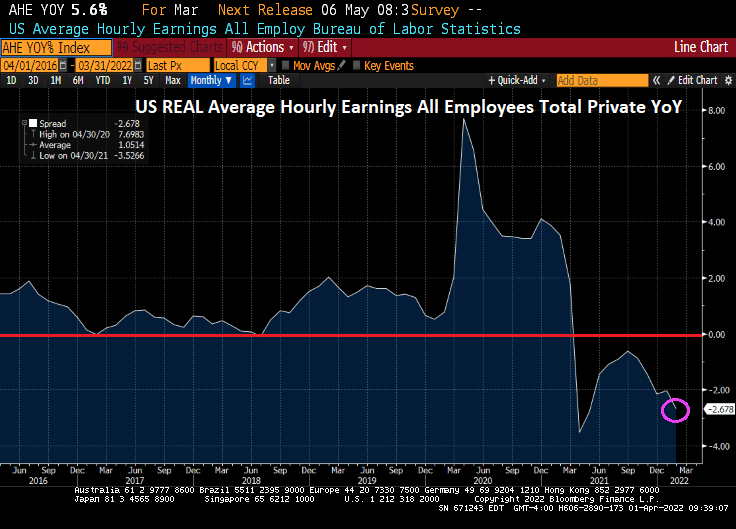

Meanwhile, today’s jobs report shows that Bidenflation is crushing America’s wage growth. While average hourly earnings grew to 5.6% YoY, we are still seeing inflation growing at 7.9% YoY meaning that inflation is reeling hurting the middle class and lower-income households.

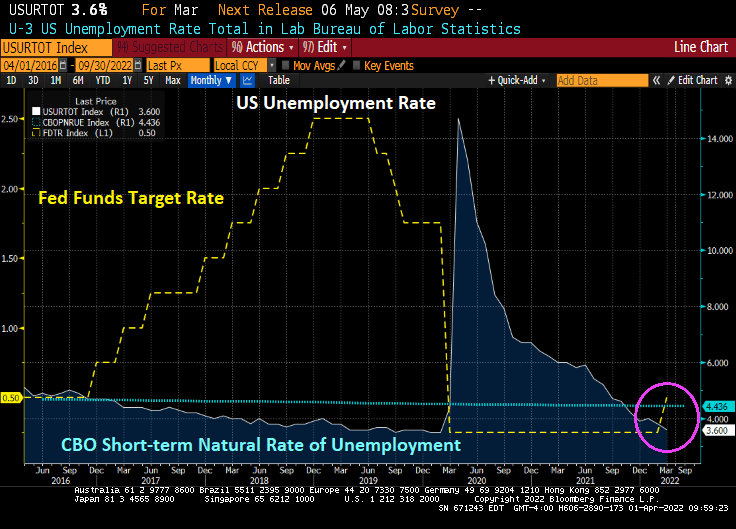

The good news is that the U-3 unemployment rate fell to 3.6%, almost back to the Trump-era unemployment rate of 3.5% prior to the Covid outbreak. And the unemployment rate remains below the CBO’s short-term natural rate of unemployment indicating that the labor market is OVERHEATED.

Today’s jobs report was pretty good, as we would expect from a recovery caused by governments shutting down economies, then reopening them. 431k jobs were added, but less than last month’s jobs added of 678k and less than the forecast 490k.

The number of people NOT in the labor force fell slightly, but it still around 100 million. The number of people holding multiple jobs to overcome Bidenflation rose to 7.5 million.

On the mortgage front, Bankrate’s 30-year mortgage rate rose to 4.90% as the 2-year Treasury rate (yellow) rises and the number of expected Fed rate hikes over the coming year is 9.26%.

The reason why the fear of ARMs is unwarranted is that ARMs generally have CAPS on rate increases, either in a given period or over the life of the loan. Of course, READ the loan terms to ensure that the ARMs has restrictive caps on rate increases.

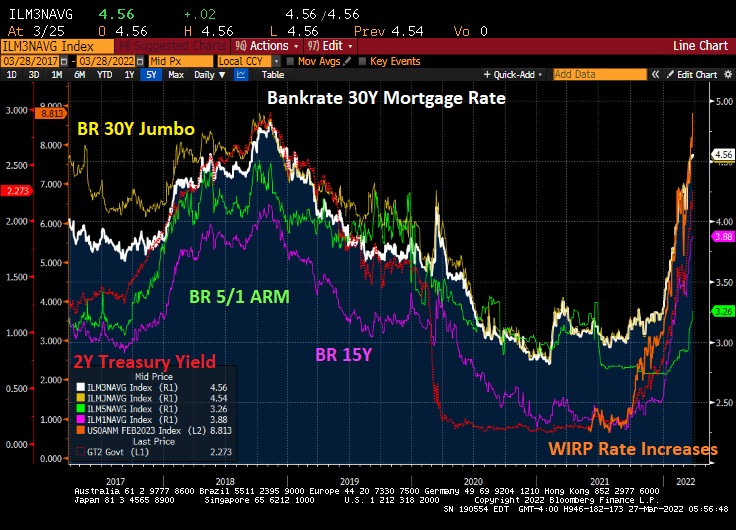

Currently, the 5/1 ARM is at 3.26% while the 30-year FRM is at 4.56%, a spread of 130 basis points.

Mortgage rates of all flavors are rising rapidly with the expectation of Federal Reserve Quantitative Tightening (QT). There are several headwinds that could counter The Fed’s QT efforts such as low GDP growth (Atlanta Fed’s GDPNow real-time GDP tracker is at 0.9% for Q1), the Russia-Ukraine invasion, approaching midterm elections, etc. But as of today, The Fed seems on a collision course with rising mortgage rates.

With the increasing likelihood of Fed rate hikes over the next year, we are seeing an increase in US ARM loan share from 4% to 7.9%, almost a doubling of ARM share. But FRMs are still over 90% of all mortgage originations.

Lending institutions would prefer consumers to use ARMs rather than FRMs since ARMs allow for the transfer on long-term interest rate risk to the borrower, while the FRM sticks the lender with long-term interest rate risk. Hence, we have Fannie Mae and Freddie Mac, the Government Sponsored Enterprises (GSEs) that allow lenders to originate FRMs and sell them to F&F. We are the only country with twin GSEs.

So, while most consumers would be better-off with an adjustable-rate mortgage, the structure of the mortgage market (particularly after the financial crisis) encourages lenders to originate FRMs and sell them to Fannie Mae and Freddie Mac.

But FEAR drives many US mortgage borrowers into the FRM space rather than getting an ARM with a lower interest rate, even if ARM caps would prevent the mortgage rate from rising more than 100 basis points over the life of the loan.

If The Fed does its expected “shock and awe” (or shock and awful), it will be more than the stock markets will crash. The housing market could crash too.

Take the current US housing situation with its limited inventory of listings combined with massive Fed stimulypto.

US 1-unit housing starts are down -4.1% in January. But heck, it is January! But on a year-over-year basis, 1-unit housing starts are down -2.4%. But what will happen if The Fed ACTUALLY withdraws its gargantuan monetary stimulus (green line)?

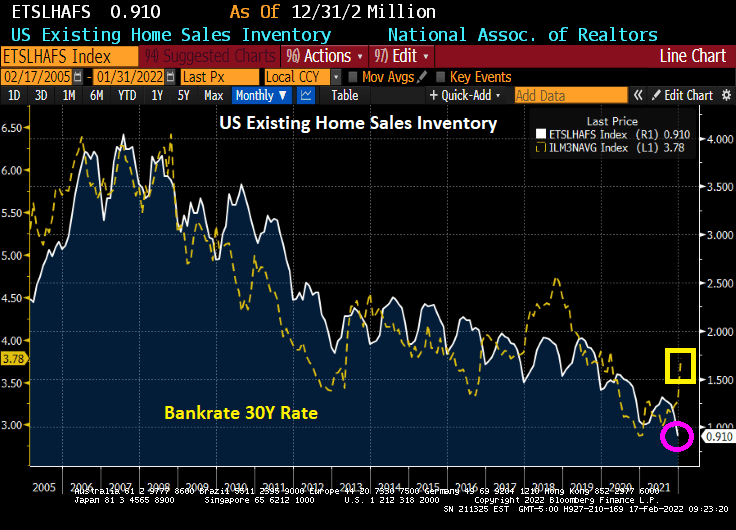

Existing home sales inventory continues to decline as Bankrate’s 30-year mortgage rate starts to climb with expectations of Fed “Shock and Awful.”

Say hello to The Federal Reserve Board of Governors!

You must be logged in to post a comment.