Its Saturday and I am dreading markets opening on Monday. But here is where we sit today.

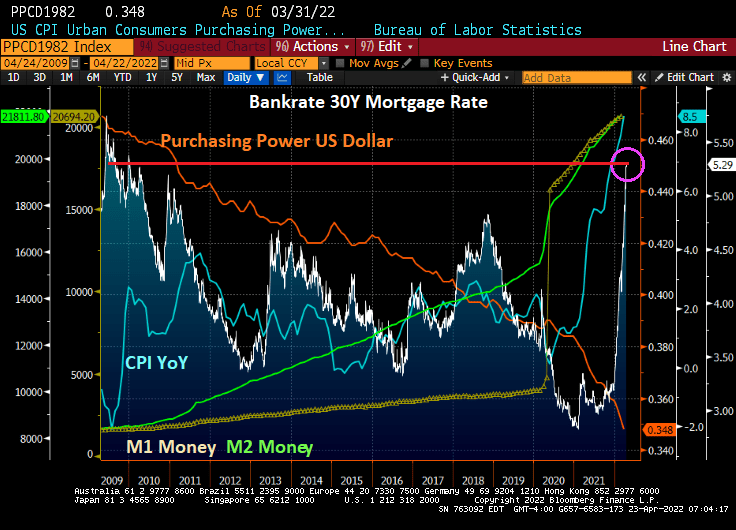

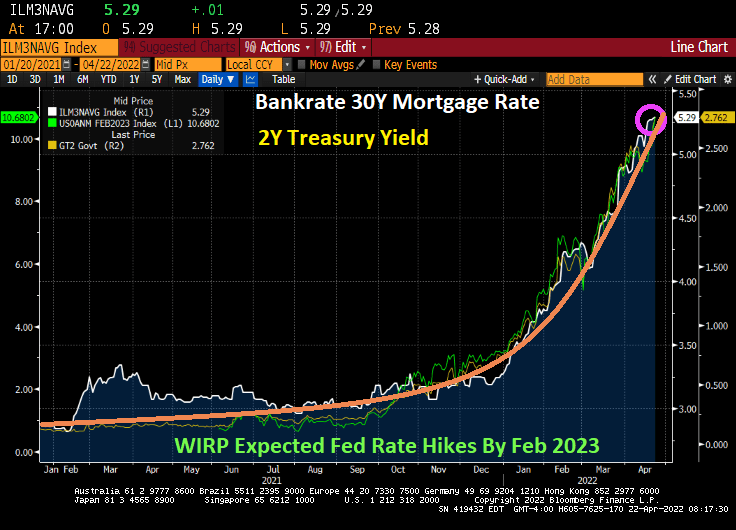

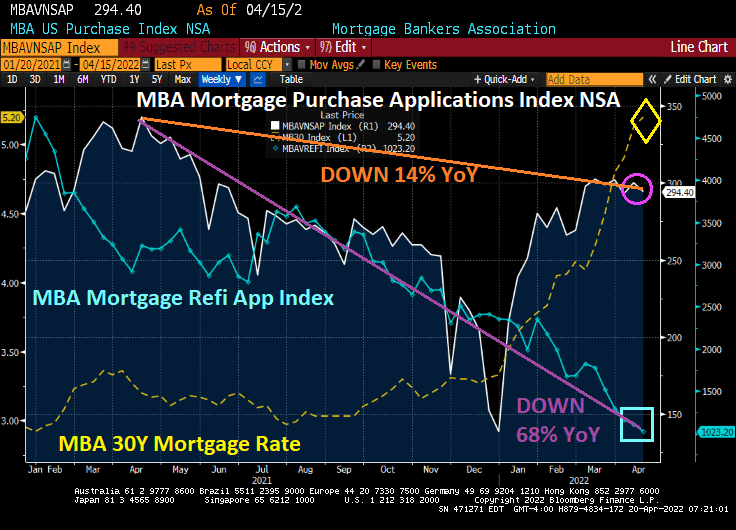

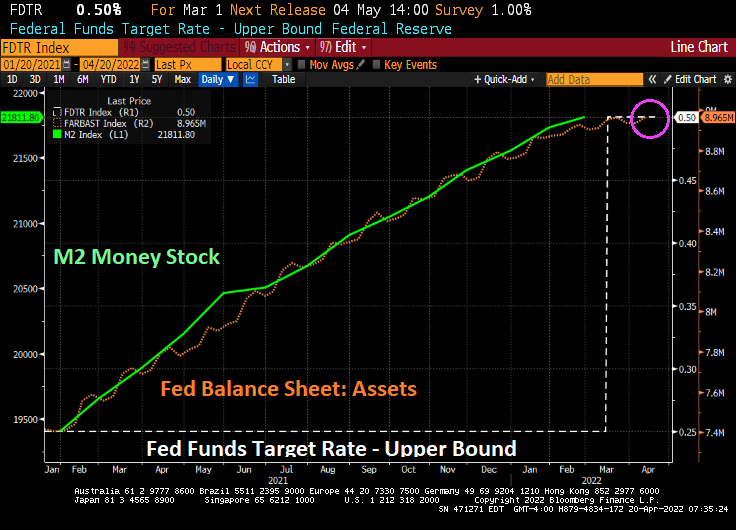

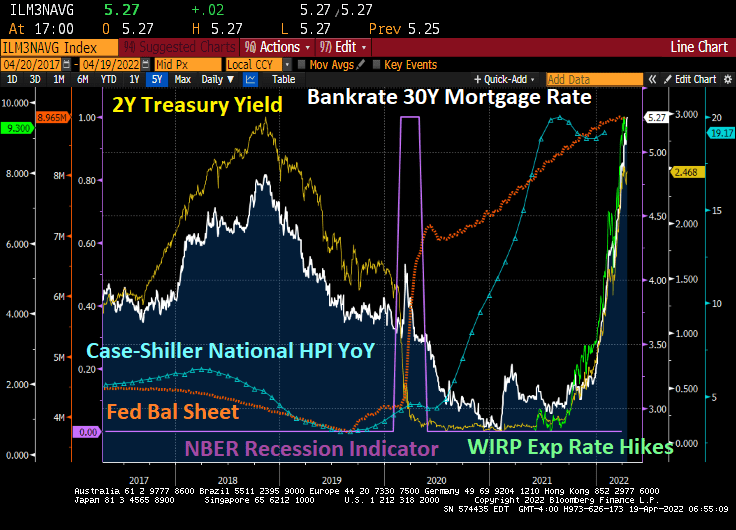

The 30-year mortgage rate has soared to 5.29%, the highest level since 2009 at the beginning of Obama’s Presidency. Since 2009, we have seen the purchasing power of the US Dollar decline further (orange line) while inflation (blue line) has soared. M1 (yellow) and M2 (green) has been growing since the financial crisis, but really took-off with the Covid outbreak in 2020 and The Fed’s massive overreaction coupled with Federal government stimulus.

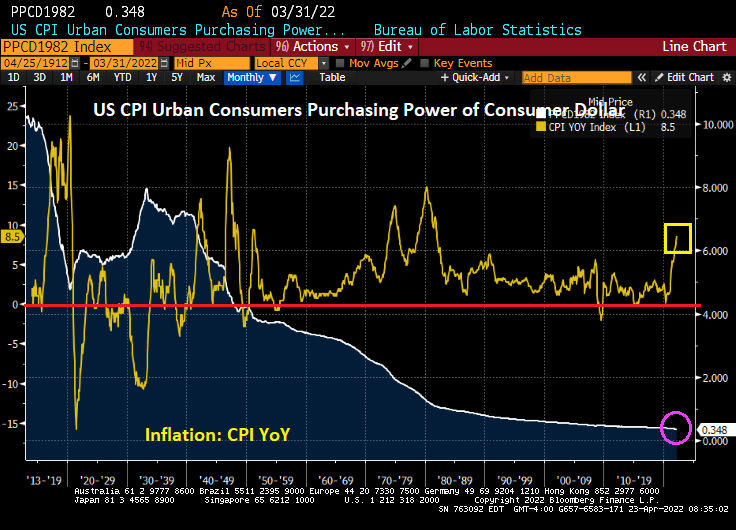

Since the creation of The Federal Reserve System under President Woodrow Wilson, the purchasing power of the US Dollar has collapsed so much that $10 in 1913 in worth 34.8 cents today. But notice that since 1949, the CPI YoY has rarely been negative meaning that prices are pretty much only going up.

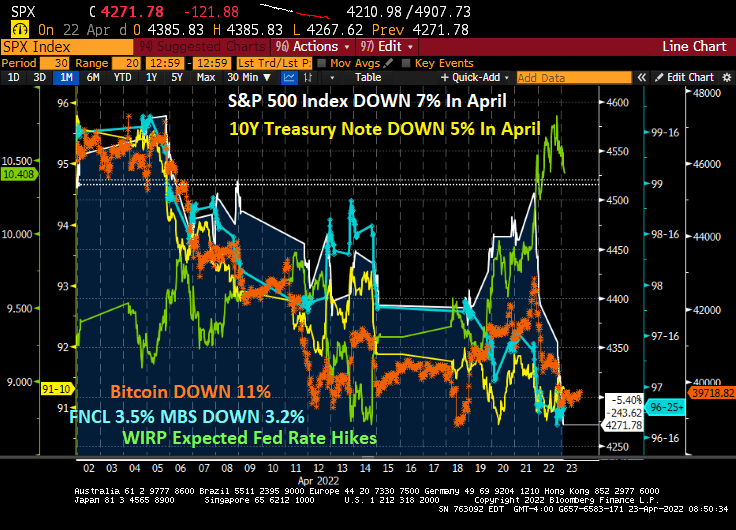

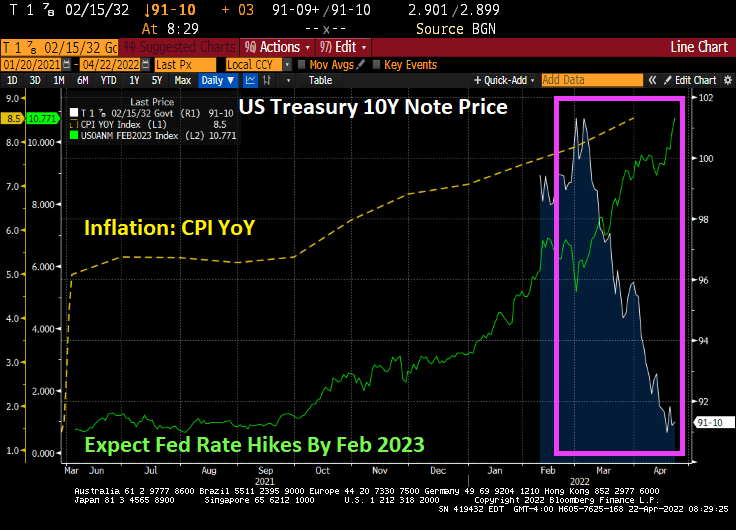

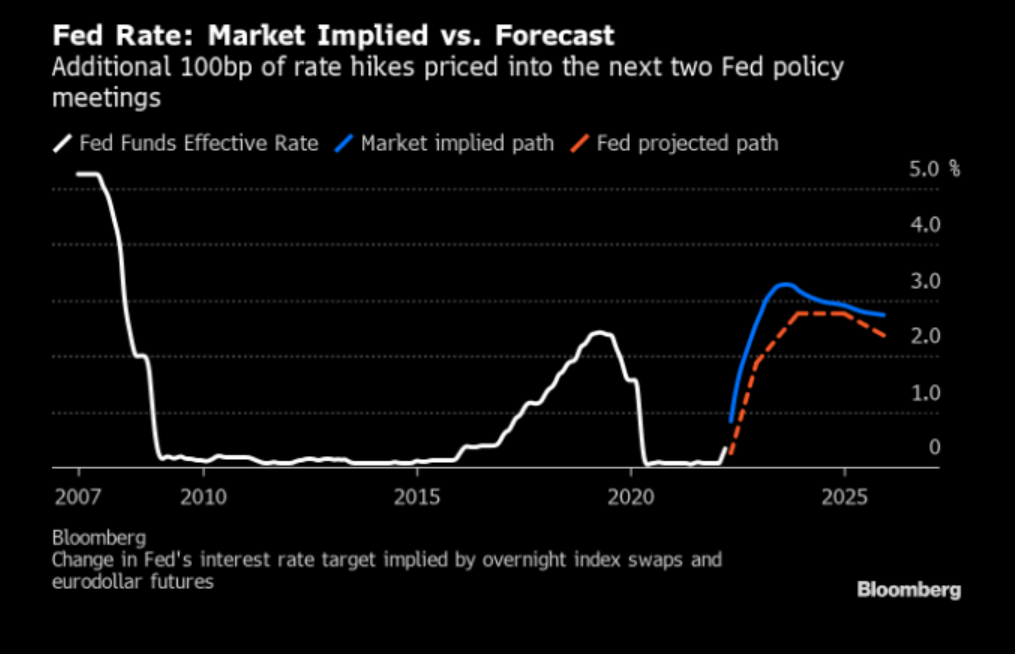

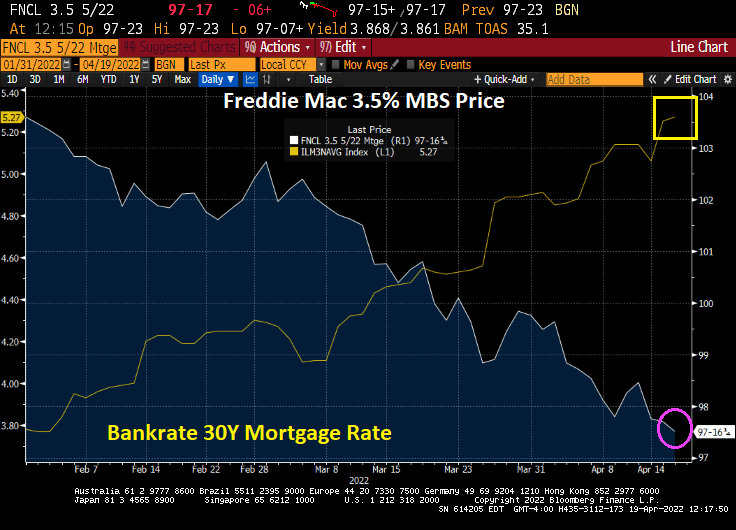

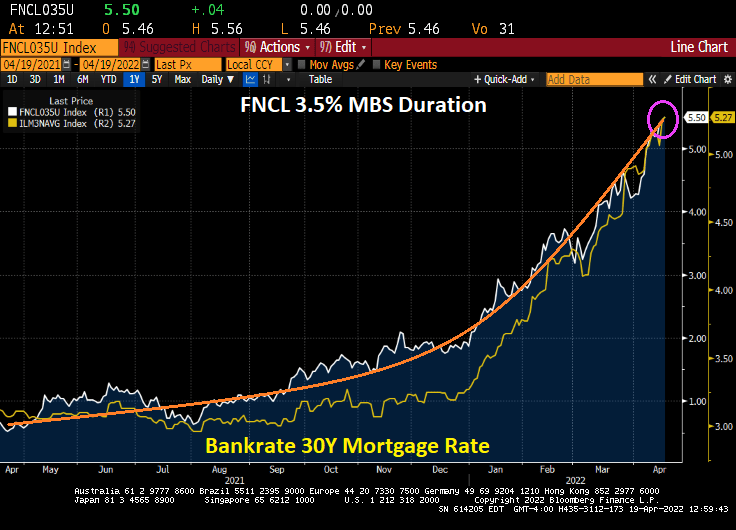

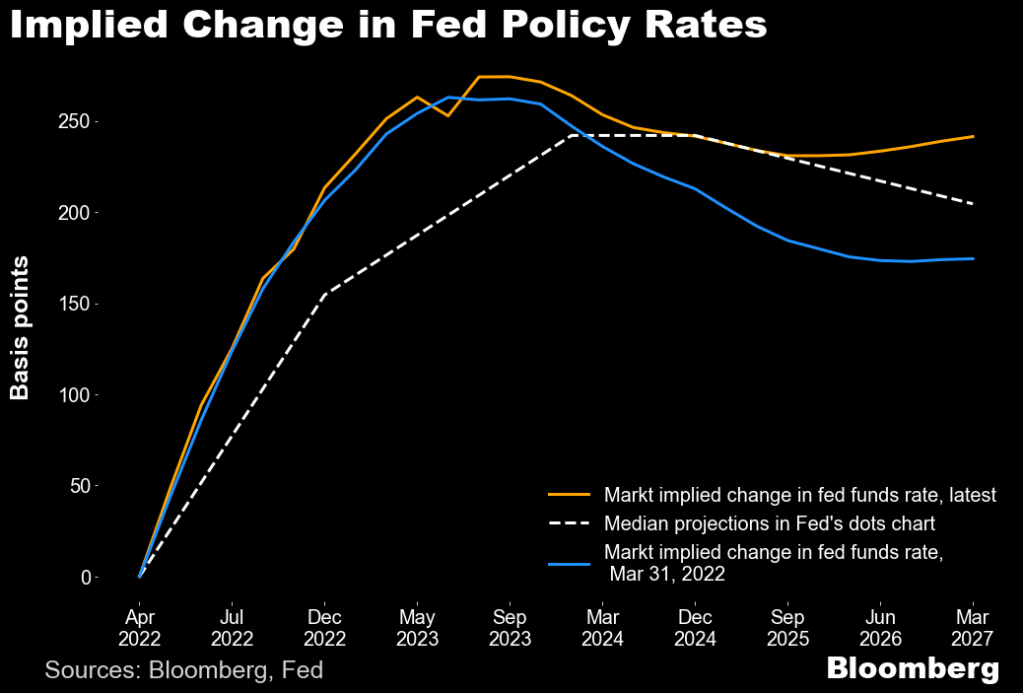

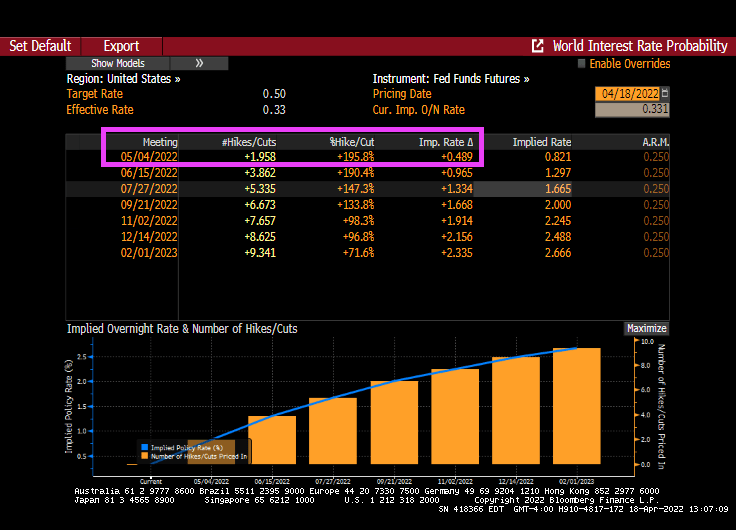

Instead of April showers bring May flowers, it is April expected Fed rate hikes (now 10.408 rate hikes by February 2023) bringing declining assets prices. In April so far, the S&P 500 index is DOWN 7%, the 10-year Treasury Note price is DOWN 5%, Bitcoin is DOWN 11%, the 3.5 coupon agency MBS price is down 3.2%.

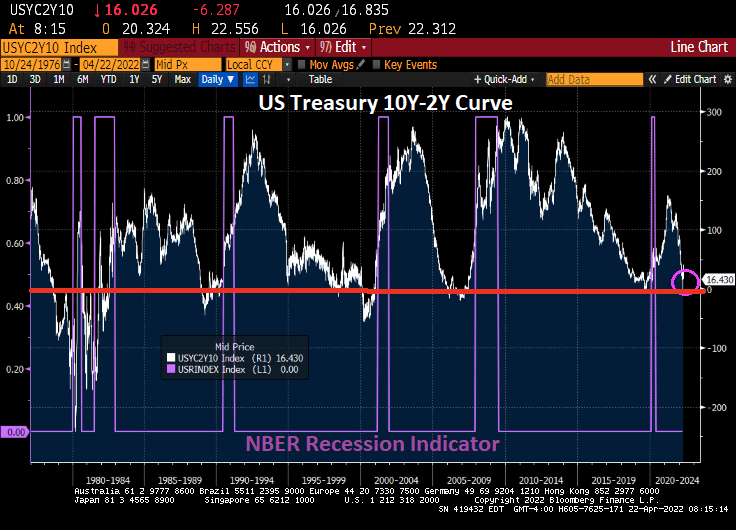

We are seeing increased volatility in both the equity and bond markets.

Well, Powell and The Fed are hurling fireballs at mortgage rates and asset prices in April.

You must be logged in to post a comment.