What a way to close out 2023! I need to find Happy Gilmore’s “Happy Place.”

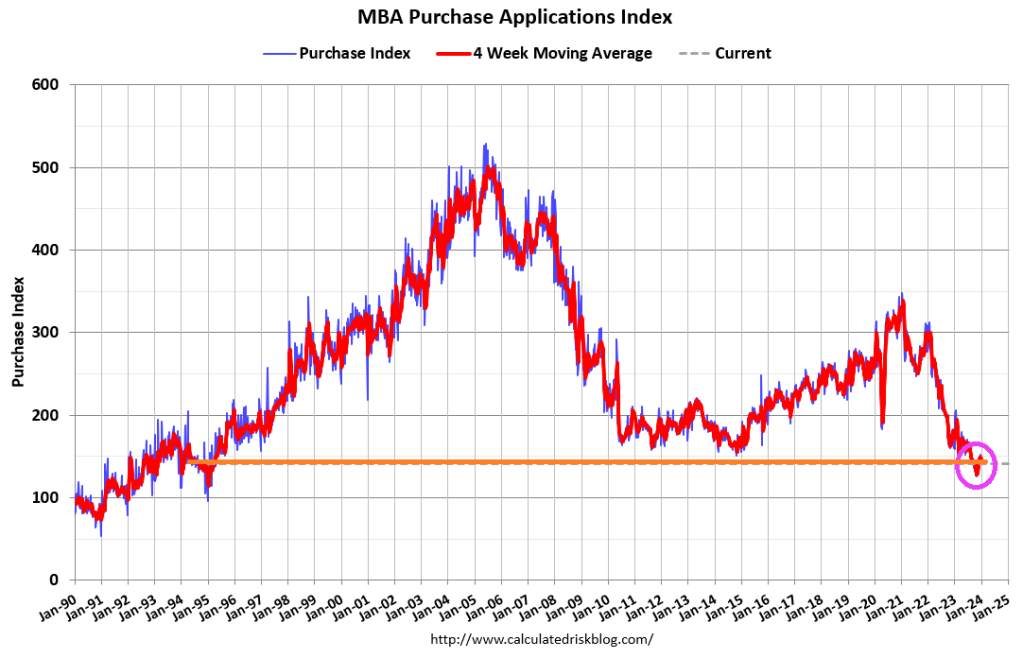

Mortgage applications decreased 9.4 percent from two weeks earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 29, 2023. The results include adjustments to account for the holidays.

The Market Composite Index, a measure of mortgage loan application volume, decreased 9.4 percent on a seasonally adjusted basis from two weeks earlier. On an unadjusted basis, the Index decreased 38 percent compared with two weeks ago. The seasonally adjusted Purchase Index decreased 5 percent compared with two weeks ago. The unadjusted Purchase Index decreased 34 percent compared with two weeks ago and was 12 percent lower than the same week one year ago.

The unadjusted Refinance Index decreased 43 percent from two weeks ago and was 15 percent higher than the same week one year ago.

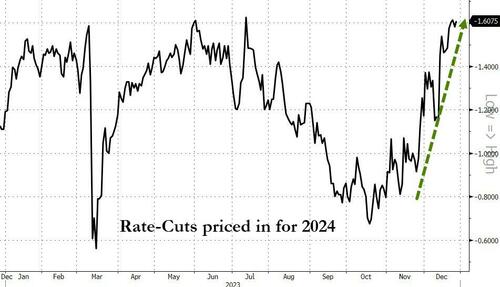

The Fed continues to fight inflation. but rates cuts are forecast for 2024. But remember, mortgage rates are down slightly, but still up 130% under Biden.

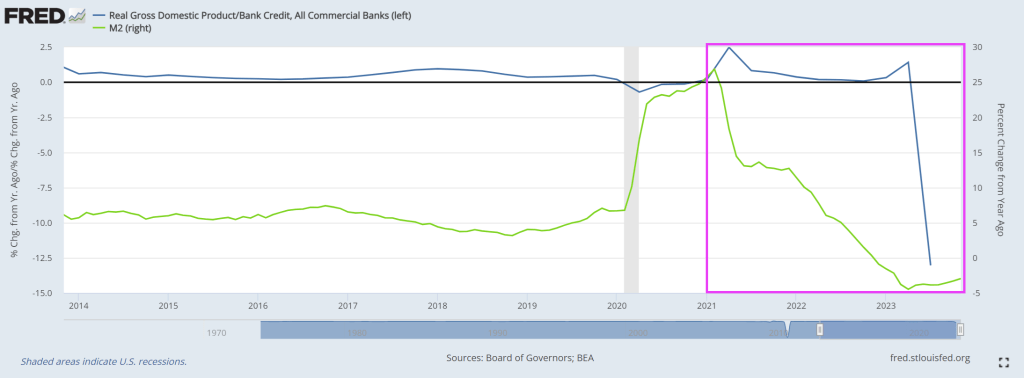

Take a look at this chart of real GDP YoY / Bank Credit YoY on the left axis and M2 Money growth on the right axis. I call this the velocity of bank credit. And it is sucking wind! Crashing to -13 in Q3.

Then we have US manufacturing PMI saw only two months in 2023 that were not in contraction and ended on a decidedly poor note with the final December print dropping to 47.9 (from 48.2 flash and 49.4 prior).

Source: Bloomberg

Across the board it was ugly with:

Renewed contraction in output as orders fall at sharper pace

Rates of inflation pick up

Joint-fastest drop in employment since June 2020

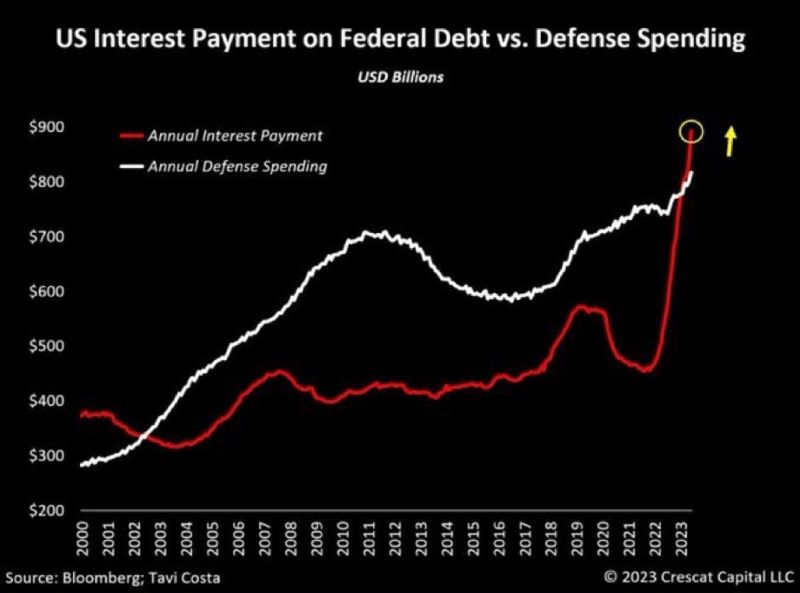

How bad is Biden’s fiscal policy? US interest payments on our bloated Federal debt is now higher than defense spending. Biden isn’t tuff enough to moderate spending or the border invasion.

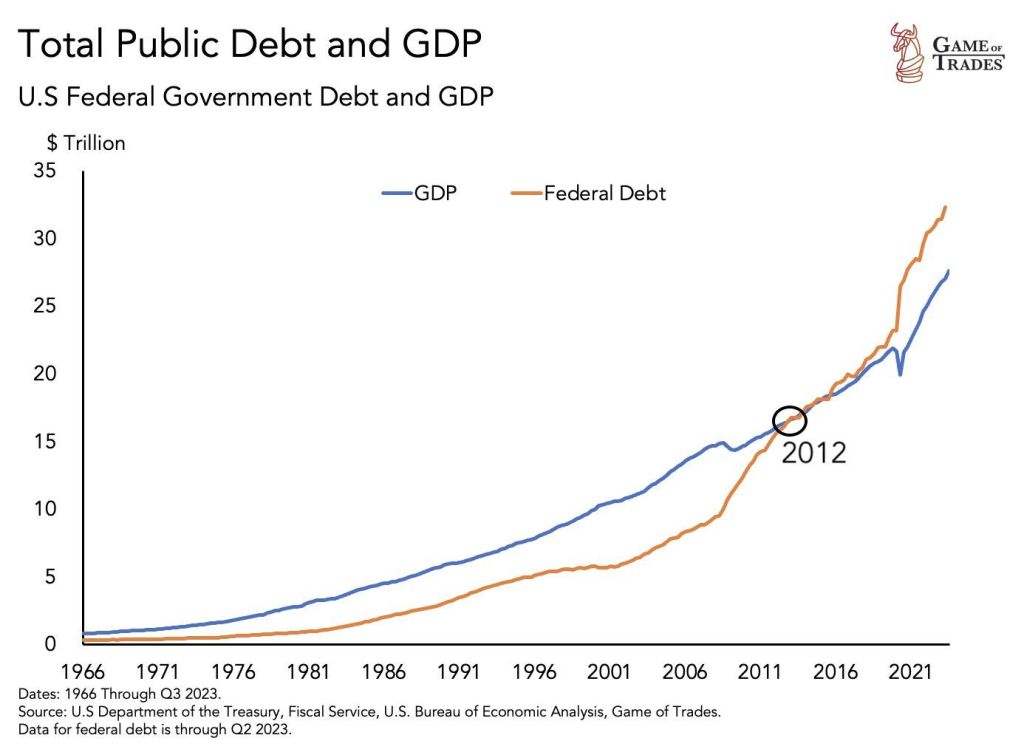

US government debt is now bigger than the US economy. This was unseen until 2012 when debt surpassed GDP for the first time.

In addition to almost $34 trillion in debt from our crazy spending, out-of-control government, we are on the hook for almost $213 TRILLION in unfunded liabilites (promises made to Americans that will likely not be honored).

The sad thing about the US Debt Clock summary is the $632,195 share per citizen of unfunded liabilties. That raises two questions. First, how can California’s Ken doll Governor Gavin “Greasy” Newsom give away free healthcare to ALL illegal immigrants? Second, since the invasion of illegal immigrants began under Biden/Mayorkas, will they be on the hook for the unfunded liabilities which they disordinately consume? Not likely. Maybe we should charge each illegal immigrant $632k admission fee.

California’s Ken doll Governor and fiscal imbecile Gavin Newsom.

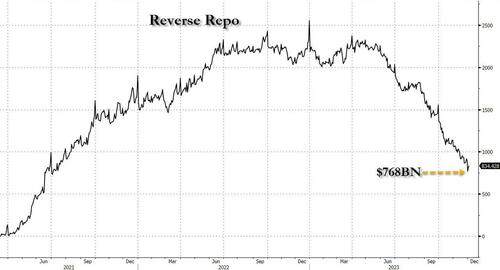

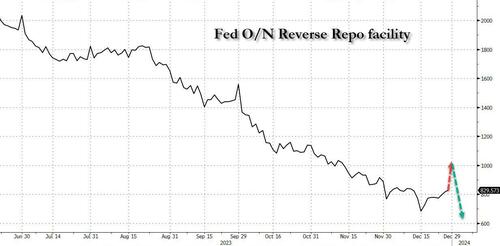

We didn’t have long to wait because just a few days later, on December 1 (just after the customary month-end window dressing period) when reverse repo tumbled to a fresh multi-year low of $765 billion…

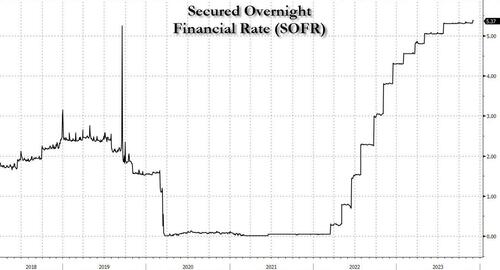

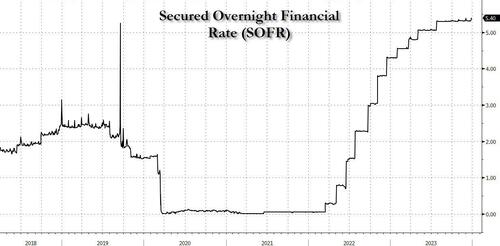

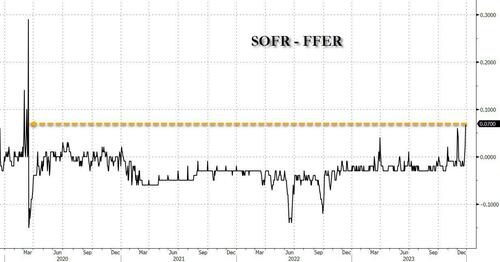

… things indeed broke as we explained in “Sudden Spike In SOFR Hints At Mounting Reserve Shortage, Early Restart Of QE” (in which we correctly previewed the coming Fed pivot at a time when most were still dead certain that Powell would only care about inflation for months to come): that’s when the the all-important SOFR rate (i.e., the new Libor) unexpectedly jumped 6bps to 5.39%, the highest on record…

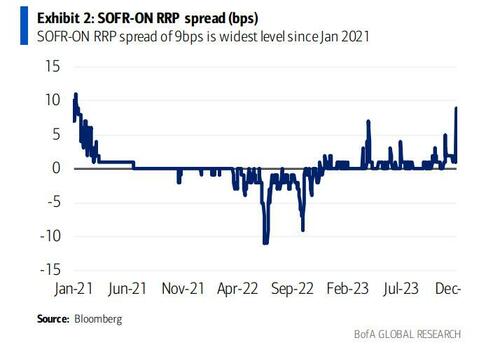

… also resulting in the largest SOFR spike vs ON RRP since Jan ’21, which hit 6bps.

The spike caught almost everyone by surprise, even such Fed-watching luminaries as BofA’s Marc Cabana because it was with “no new UST settlements, lower repo volumes, and lower sponsored bi-lateral volumes.” More ominously, and confirming our take from three weeks ago, Cabana warned at the time (full note here) that “the move is consistent with the slow theme of less cash & more collateral in the system” – i.e., growing reserve scarcity – and “may have been exacerbated by elevated dealer inventories, bi-lateral borrowing need, and limited excess cash to backstop repo. If funding pressure persists, it risks Fed re-assessment of ample banking system reserves & potential early end to QT.”

Then, the mini liquidity crisis disappeared almost as fast as it emerged, as SOFR rates eased off and the SOFR-Fed Funds spread normalized once GSE cash entered the market as it does every month….

… until today when not only did SOFR hit a new record high, ironically at a time when the market is pricing in more than 6 rate cuts in 2024…

… but the spread between the SOFR and the effective Fed Funds rate just spiked to the highest level since the March 2020 repo crisis…

.. with a similar move also observed in the spread between SOFR rate and the O/N Reverse Repo which similarly blew out to the widest since the start of 2021.

While there was no specific catalyst behind the sudden spike, two factors are the likely culprits: the year-end liquidity crunch, and the recent sharp increase in the Fed’s reverse repo facility, which has increased from a multi-year low of $683 billion on Dec 15 to yesterday’s $830 billion, and which STIR strategists expect will shoot up above $1 trillion in today’s final for 2023 reverse repo operation as a whopping $300+ billion in short-term liquidity in pulled from markets in just days.

That’s the bad news.

The good news is that come 2024 in a few hours, and specifically the first day of trading on Jan 2, we expect the reverse repo facility to plummet back to $700 billion once the year-end window dressing is over (especially with total US debt rising above $34 trillion to start the year), and floods the system with fresh liquidity which will stabilize the monetary plumbing at least until reverse repo dips below that key level of $700 billion at which point we expect the SOFR spikes to become a daily occurrence, and one which the Fed will no longer be able to ignore.

Indeed, one can already see traces of this in the repo market, where the rate on overnight GC repo first surged to 5.625% at the open on the final trading day of December before dropping to 5.45%, according to ICAP. It has since climbed back to 5.50%. But that’s still lower than where repo rates for Dec. 29 were trading during the prior session, as markets now start frontrunning the coming reverse repo liquidity flood.

Of course, once reverse repo eventually tumbles to $0 some time in March, all bets are off and the narrative shift to the next QE will begin.

“Say, can I sniff you if you take Trump off of Maine’s Presidential ballot??”

Nobody but Biden could so handicap an economy with horrible fiscal policies, massive debt, inflation and open borders. And then go to the Virgin Islands for yet another taxpayer paid vacation. Biden has spent 40% of his Presidency on vacations.

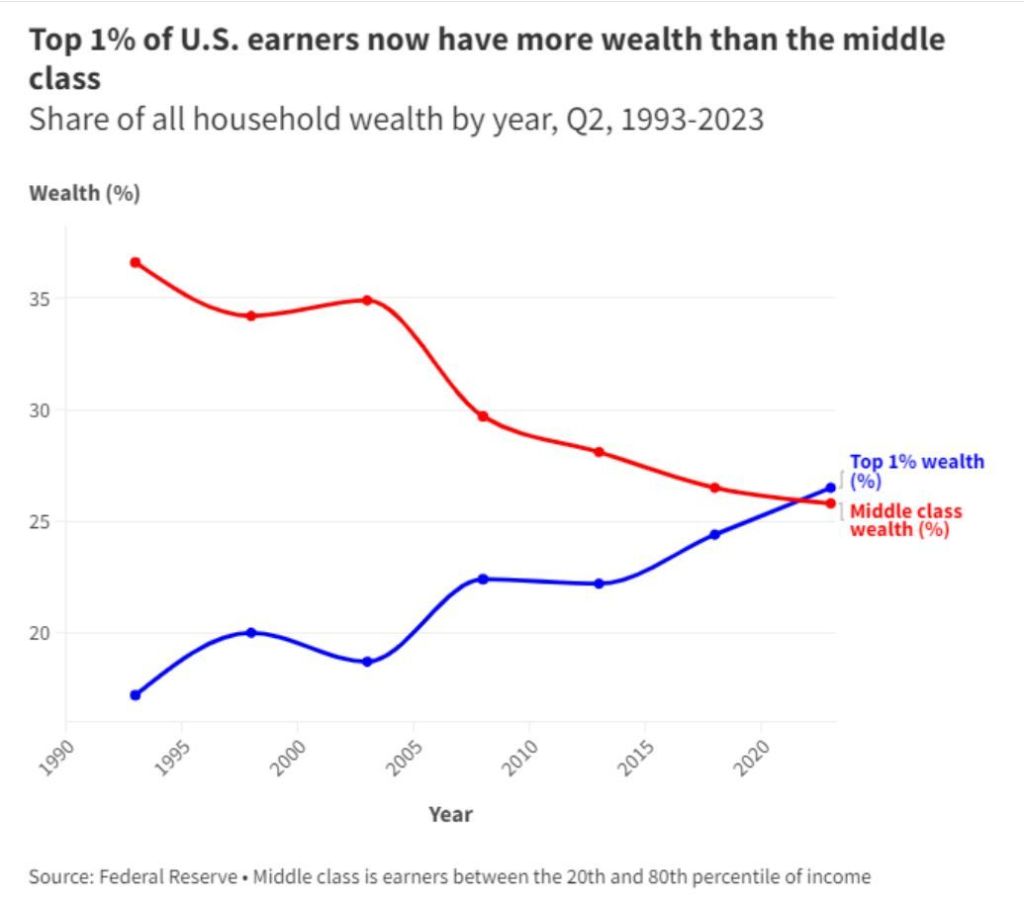

Bidenomics is a disaster for the US middle class. And Bidenomics with its inflation has led The Fed to counterattack and raises interest rates, leading to losses for The Federal Reserve (which is paid for by US Treasury) of over $130 billion.

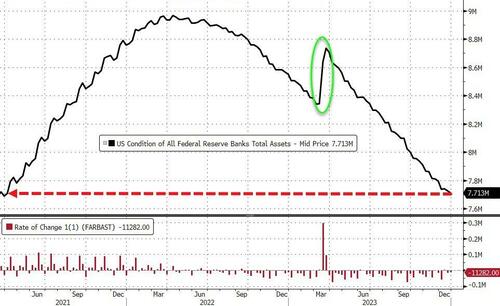

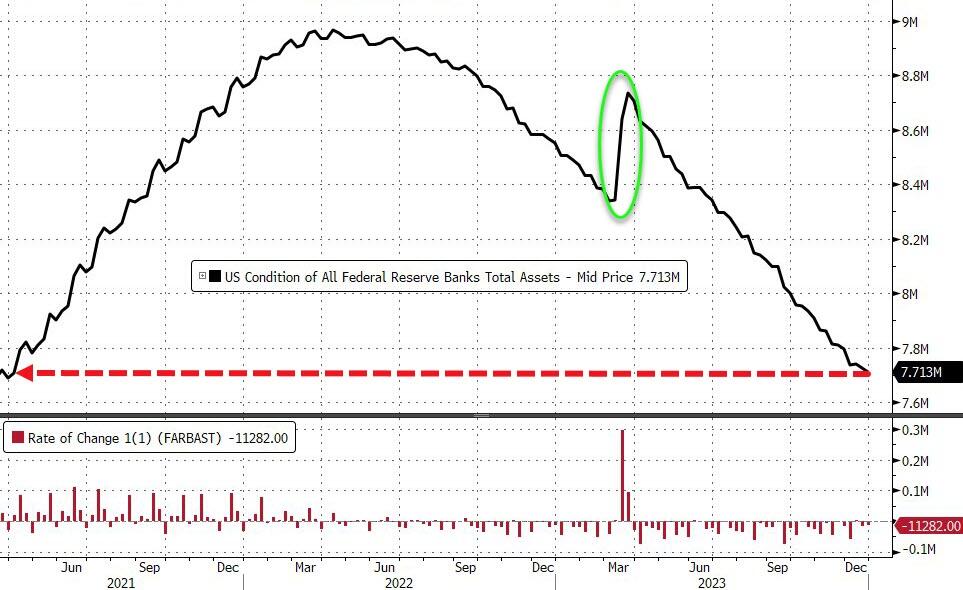

The Fed’s balance sheet shrank by $11.3BN last week to its lowest level since March 2021, but still remains elevated.

Source: Bloomberg

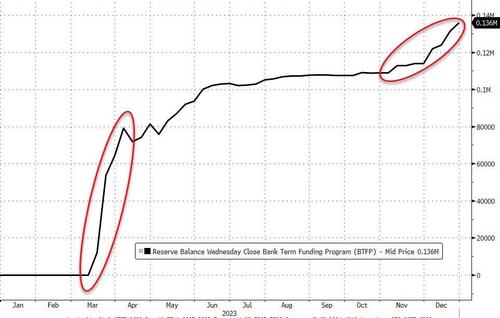

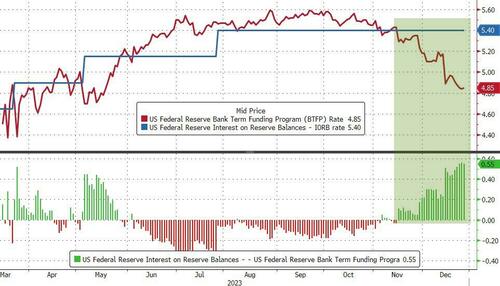

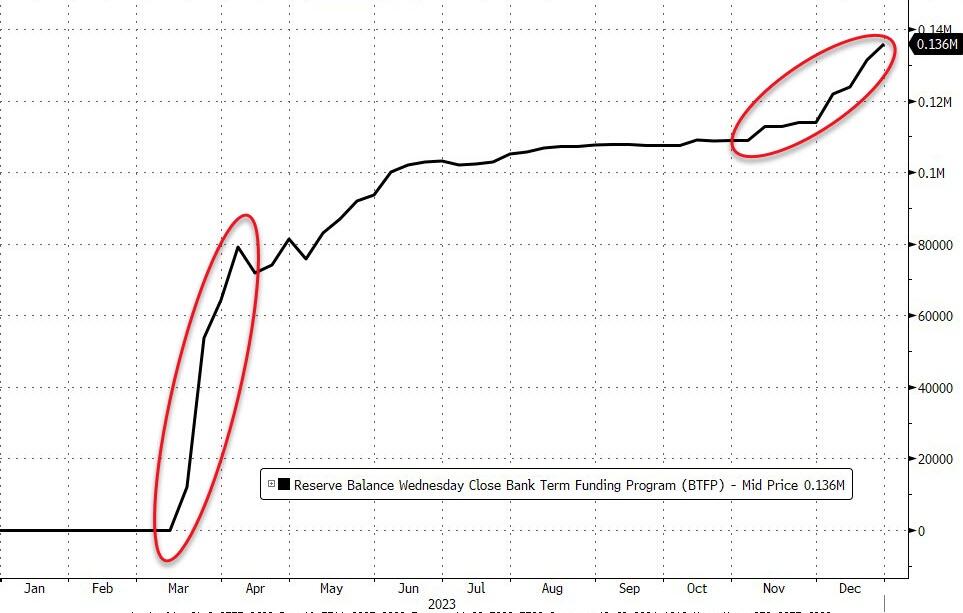

Usage of The Fed’s bank bailout facility rose by another $4.5BN last week to a new record high of $136BN…

Source: Bloomberg

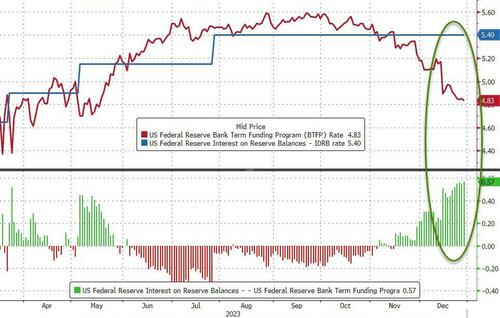

The BTFP-Fed Arb continues to offer ‘free-money’ (and usage of the BTFP has risen by $26.7BN since the arb existed):

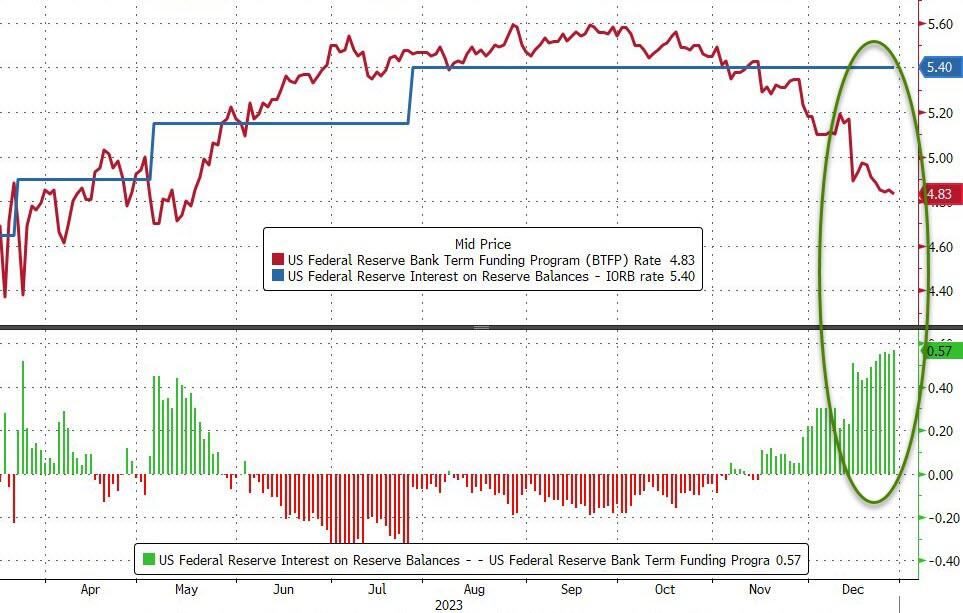

The rate on the Fed’s Bank Term Funding Program – which allows banks and credit unions to borrow funds for up to one year, pledging US Treasuries and agency debt as collateral valued at par – is the one-year overnight index swap rate plus 10 basis points.

That figure is currently 4.83%, down from 5.59% in September.

For institutions that have an account at the Fed, they can borrow from the BTFP at 4.83% and park that at the central bank to earn 5.40% – the interest on reserve balances.

Source: Bloomberg

The 57bp spread is the widest level since the Fed introduced the facility to support a struggling banking system after the collapse of California’s Silicon Valley Bank and Signature Bank in New York.

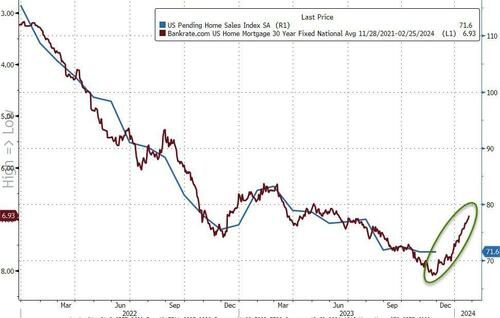

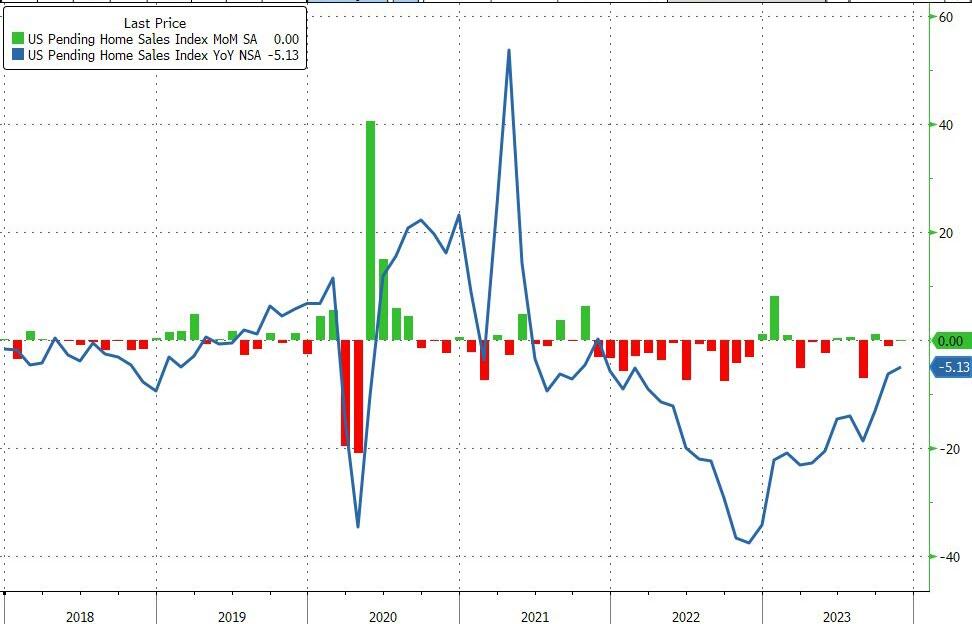

Alarm! With rampant inflation, The Federal Reserve has raised rates to tame inflation. And with the rate increases, US pending home sales have fallen -5% since last year.

That left Pending Home Sales Index still down over 5% YoY…

Source: Bloomberg

That leaves the Pending Home Sales Index at a new record low…

Source: Bloomberg

The index of contract signings for existing homes declined in the South, the biggest US housing market, to the lowest level on record.

Pending sales climbed in the other three regions.

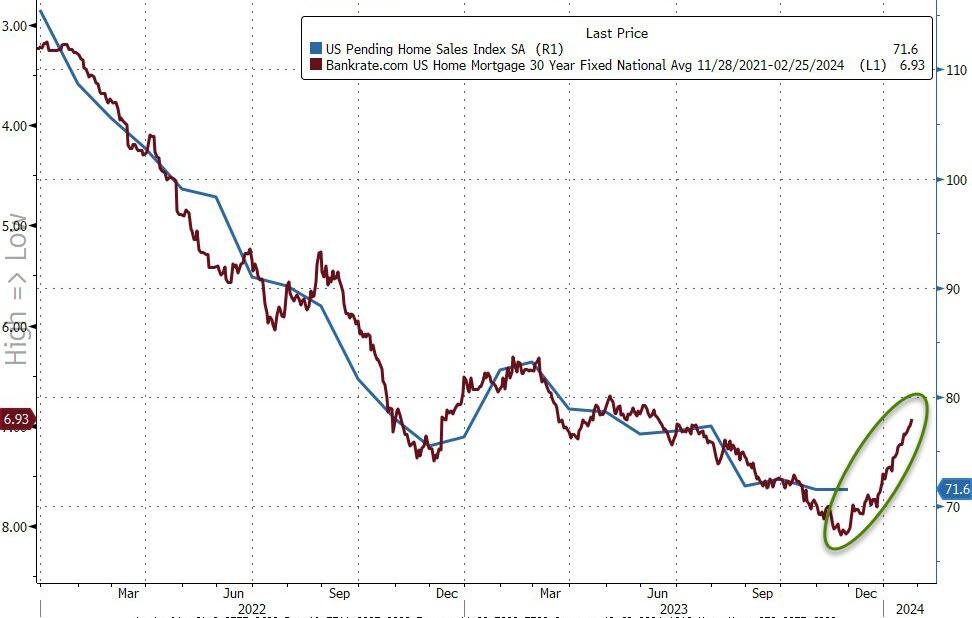

The trend in pending home sales appears to tracking mortgage rates (with about a one-month lag), suggesting things may be about to pick up more solidly in the next few months…

Source: Bloomberg

“Although declining mortgage rates did not induce more homebuyers to submit formal contracts in November, it has sparked a surge in interest, as evidenced by a higher number of lockbox openings,” Lawrence Yun, NAR’s chief economist, said in a statement.

“With mortgage rates falling further in December – leading to savings of around $300 per month from the recent cyclical peak in rates – home sales will improve in 2024,” Yun said.

Optimism – from a realtor – whoever would have thought!?

After witnessing three of the four largest bank failures in U.S. history in 2023, the attention of the media and the markets has turned elsewhere. Banking crisis? It is as though it never happened. Having fallen by some 40 percent in March, the NASDAQ Bank Index has recovered to within 15 percent of its high from February. In the last few months, nearly all markets have gone on a bull run, including bank stocks.

Yet, and despite the relative quiet, the banking sector is not in great shape. Here are some of the reasons why.

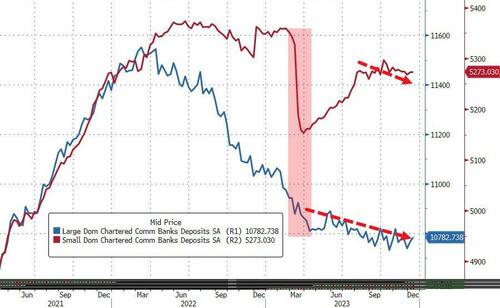

Banks continue to lose deposits. According to data from the Federal Deposit Insurance. Corp. (FDIC), U.S. banks have now lost deposits for six consecutive quarters. While the pace has slowed from the first quarter of 2023, in which nearly $500 billion of deposits were removed from the banking system, approximately $190 billion of deposits have been withdrawn in the last two quarters. Indeed, U.S. banks have lost a net $1.1 trillion of deposits since the beginning of 2022 when interest rates began to rise.

With customer deposits growing scarce, U.S. banks are instead relying on emergency funding lines from the Federal Reserve Banks and the Federal Home Loan Bank (FHLB) system. FHLB bond capital raising, of which the proceeds are used to fund the banks, is up 89 percent year over year through November and looks set to reach $1.1 trillion for 2023. Use of the Bank Term Funding Program, the emergency line put in place by the Fed in March 2023, reached an all-time high last week at $131.3 billion.

This does not reflect normal market operations.

This is a sign that the bank funding markets aren’t operating properly, and that the regulators are stepping in to help prop up the system.

The growing gap between the rate on the Federal Reserve’s nascent funding facility and what the central bank pays institutions parking reserves suggests officials will let the program expire in March, according to Wrightson ICAP.

“In justifying the generous terms of the original program, the Fed cited the ‘unusual and exigent’ market conditions facing the banking industry following last spring’s deposit runs,” Wrightson ICAP economist Lou Crandall wrote in a note to clients.

“It would be difficult to defend a renewal in today’s more normal environment.”

What happens then?]

So much for the liabilities side. But banks face challenges on the asset side as well.

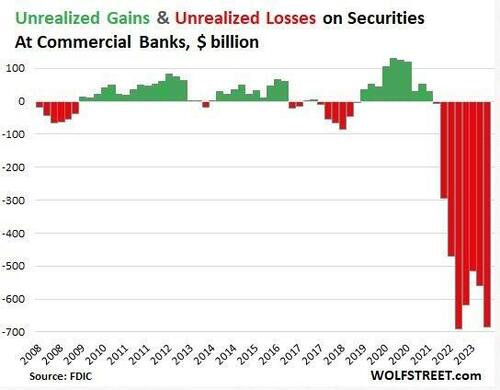

Unrealized losses on investment securities, which is the same problem that got SVB into trouble a year ago, continue to rise. U.S. banks reported unrealized losses of over $684 billion in the third quarter, up 22 percent from the second quarter. Of these unrealized losses on securities, $294 billion are categorized as available for sale (AFS), as opposed to held to maturity (HTM), whereby the bank intends to hold the asset and (hopefully) recapture principle at the end of the term. The high amount of AFS suggests that if interest rates remain “higher for longer,” then a portion of these losses will begin to realize in 2024 as they are sold by the banks. This will pressure profitability and capital levels.

Net income is declining across the banking system generally, but particularly among the smaller community banks. Credit quality is deteriorating, but has not yet reached crisis level. Commercial real estate continues to drive the increase in problem loans.

To grow (or at least slow the decline) of deposits, banks are going to have offer rates that are somewhat competitive with money market funds (considering that bank deposits are insured by the FDIC and thus relatively safe), and that offer positive real (i.e., after inflation) returns. With inflation persisting in the range of 3–4 percent, this means that banks will have to offer 4–5 percent to be relevant. This isn’t going to work for the banks. They won’t be able to maintain profitability. And it won’t work for the U.S. Treasury, which itself is committed to trillion-dollar bond issuances each quarter, which also must offer a positive interest rate above investor perceptions of inflation and the deteriorating fiscal condition of the U.S. government.

If funding costs rise further, or if unrealized losses begin to realize, banks will start taking hits to their capital levels. This will spook the markets, including depositors, and we may find ourselves in round two of deposit runs. To head off these challenges, some banks are looking to merge. There have been 78 bank deals announced in the second half of 2023, mostly among the smaller and community banks. But this won’t work in many situations where the result is the proverbial “two drunks holding each other up.”

Investor optimism is permeating markets going into year-end, with most all asset classes continuing to rise. But we must not lose sight of the banks. They are not out of the woods yet. While there is a “goldilocks” scenario in which the banking sector makes a soft landing, the risk of another set of bank failures in 2024 remains meaningful.

And we have 21 straight weeks of negative growth in bank credit. And The Fed still has a staggering amount of financial stimulus outstanding.

With all hell breaking loose around the world, President Biden has gone on yet another vacation, this time to the Virgin Islands to stay at the home of a big donor. But his handlers run things, not Vacation Joe.

C’mon Joe. The media has always reported bad news. Warm and fuzzy doesn’t anger people, but bad news does! And under Bidenomics, there has been a lot of bad news.

President Biden railed against corporate media before he and several family members headed by helicopter to Camp David, the presidential retreat in the mountains of western Maryland.

Before boarding the presidential helicopter, Biden was asked by one reporter: “What’s your outlook on the economy next year?”

The president responded: “All good,” adding, “Take a look. Start reporting it the right way.”

Sounds like Biden watched the Travola/Jackson flick “Basic” where the infamous line was uttered “Tell the story right.”

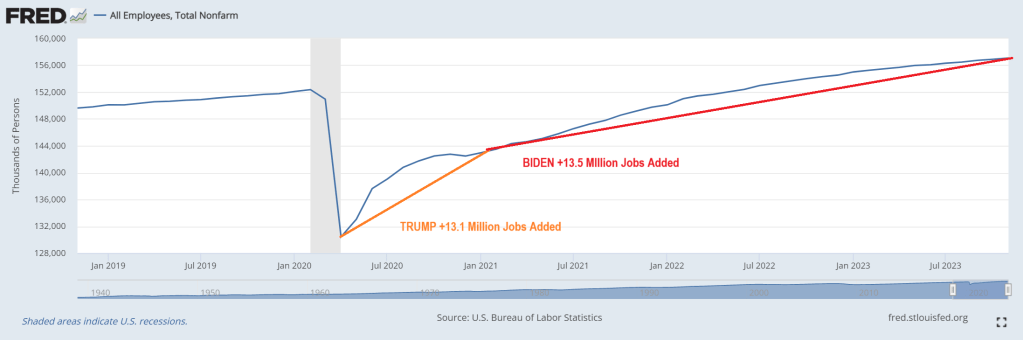

OK Joey, let’s tell the story right. After the horrendous economic shutdowns of local economics and schools in 2020, 15.1 million jobs were added after the shutdowns ended in just 10 months. Wow, that was simple! But under Biden’s Reign of Economic Error, only 15.5 million jobs were added over the next 34 months.

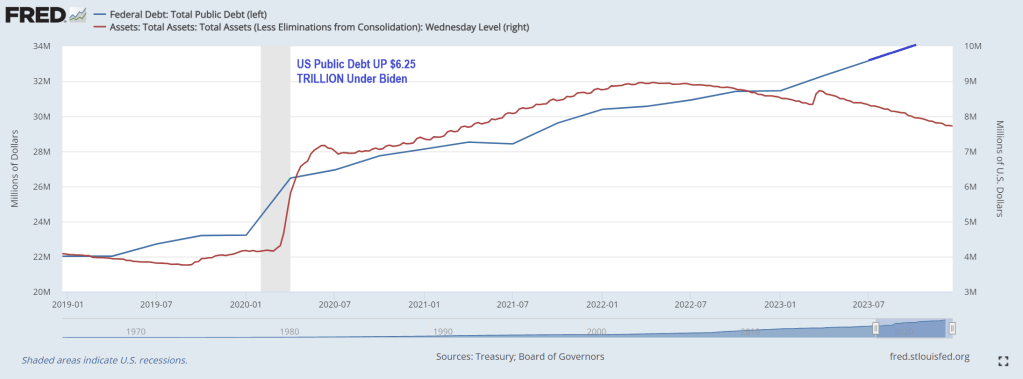

But Biden’s record on jobs comes at the expense of an additional $6.25 TRILLION IN PUBLIC DEBT.

With $34 trillion and rapdily growing debt and budget deficits, it is hard to find good news about Bidenomics.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.