Its just like The Fed. The Taylor Rule says that The Fed’s target rate should be 10.29%, but now the terminal rate has been lowered to 5.475%, almost half of where the target rate should be.

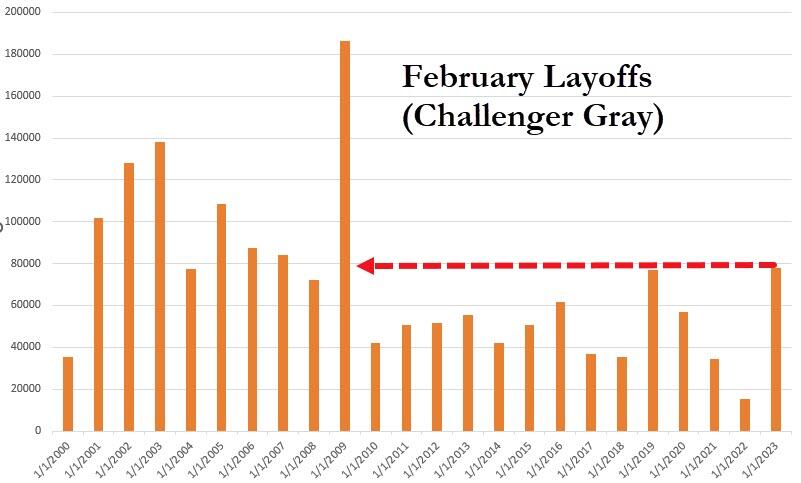

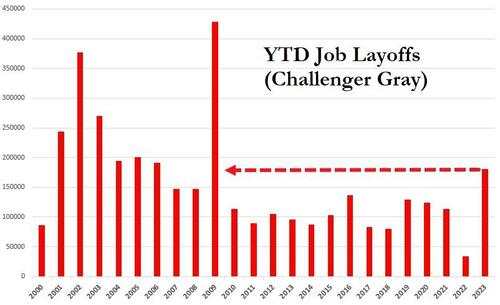

Today’s jobs report for February was a huge disappointment IFF you expected another blowout jobs report like the one from January (504k jobs added). February saw just 311k jobs added, a decline of -38.3% MoM.

And just like that, The Fed’s terminal rate fell to 5.475%, a far cry from the 10.29% rate according to the Taylor Rule.

Today’s Fed Funds Target rate is 4.75% leaving only 72.5 basis points to move.

Today’s market hurl? The Dow fell -300 points and Europe looks like WWIII just broke out.

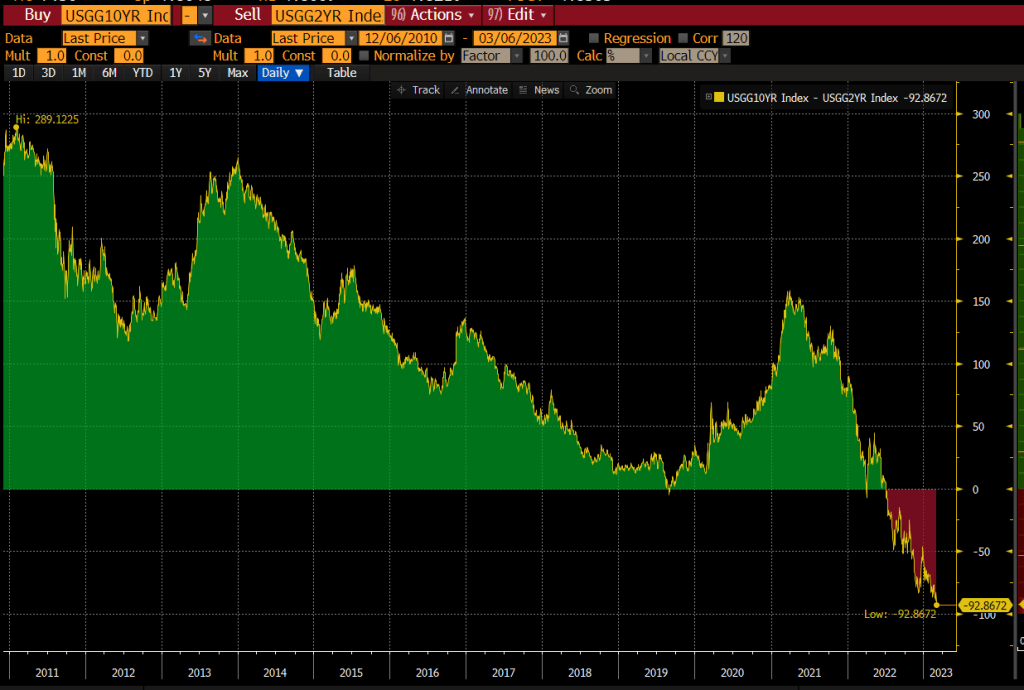

And the US Treasury 2-year rate plungeed -26.1 basis points.

Of course, Powell until recently followed the Yellen Rule. That is, keep rates at 25 basis points.

This is a classic communications breakdown between The Fed and the economy.

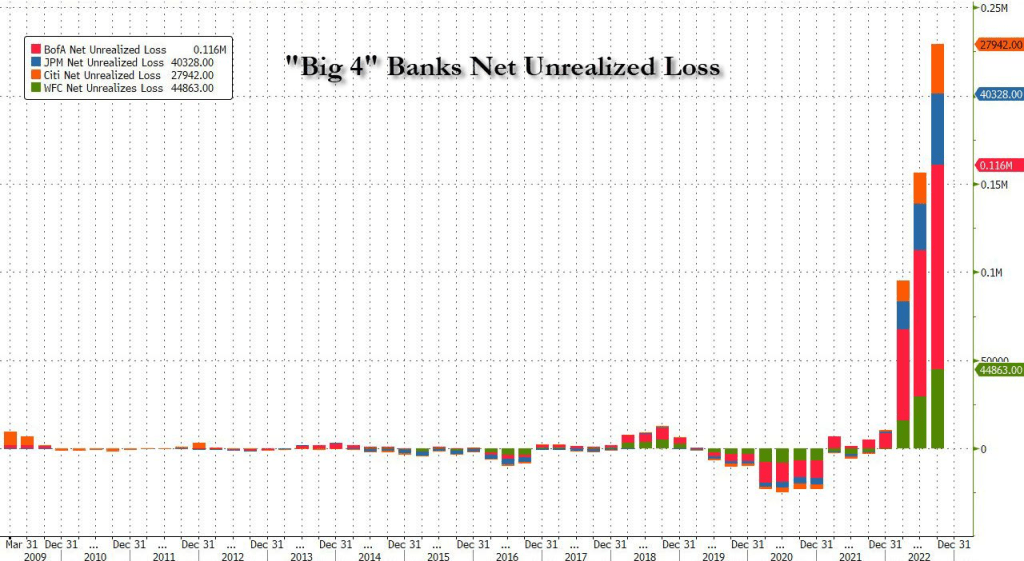

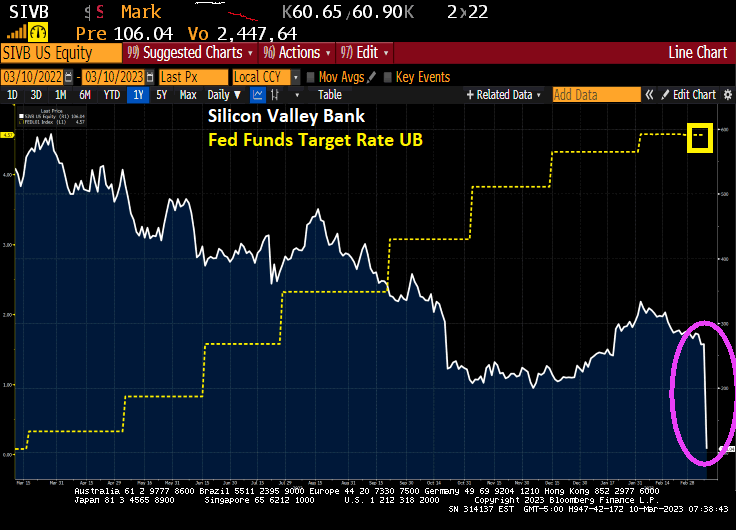

Let’s see if The Fed holds course with Silicon Valley Bank collapsing in biggest failure since 2008.

Silicon Valley Bank became the biggest US lender to fail in more than a decade after a tumultuous week that saw an unsuccessful attempt to raise capital and a cash exodus from the tech startups that had fueled the lender’s rise.

Regulators stepped in and seized it Friday in a stunning downfall for a lender that had quadrupled in size over the past five years and was valued at more than $40 billion as recently as last year.

The move by California state regulators to take possession of the lender, known as SVB, and appoint the Federal Deposit Insurance Corp. receiver underscores the impact that the US’s rapid interest-rate increase is having on smaller lenders. SVB is the second regional lender to fold this week after Silvergate Capital Corp. announced it was voluntarily liquidating its bank, spurring a broader selloff in bank stocks.

The FDIC has set up a bridge bank to handle the failure of SVB. VERY rare. The last bridge bank was for IndyMac Bank from LA.

SVP is the second biggest bank failure in US history after Washington Mutual (WAMU).

RIP Gary Rossington, the last remaining Lynyrd Skynrd original member.

You must be logged in to post a comment.