The Conference Board’s Leading Indicator should be called The Bleeding Indicator given that the leading index has declined to 10 straight months. This is happening as The Fed tightens monetary policy to combat inflation.

Leading indicators include economic variables that tend to move before changes in the overall economy. These indicators give a sense of the future state of an economy.

Ah, the start of a new week with Treasury Secretary Janet Yellen arguing (with a straight face) that there is no room in the Federal budget for cuts. Apparenly, Yellen never read any of the massive, pork-laden spending bills signed by Biden (no one else did in Congress either, nor did Biden).

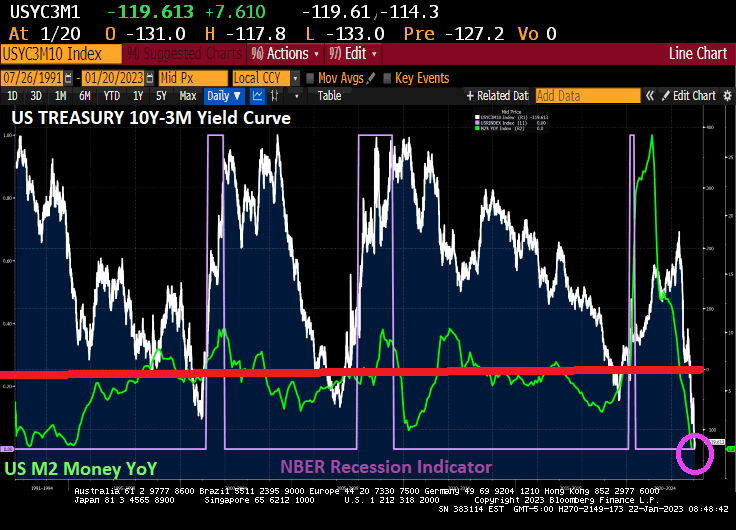

Let’s start with the US credit default swap (1 year). It remains high at 68.72 (the price of insuring against a US default). And the US Treasury yield curve (10Y-3M)? It remains deeply inverted at -114 basis points this morning signaling an impending US recession.

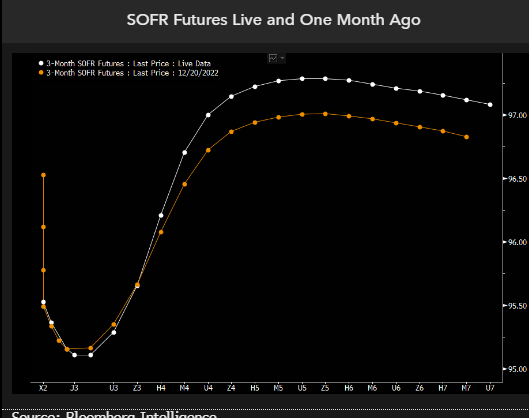

Then we have SOFR (Secured Overnight Financing Rate). SOFR futures are pricing for the Federal Reserve to hike rates a few more times and to start cutting before the end of this year. The pricing for the 2023 rate path is little changed from a month ago, but this year the market has priced in deeper cuts in 2024, with SOFR now seen below 3% by early 2025 before stabilizing. The implication is that hedging recession and significant rate cuts in 2024 now seems to be fully priced in, yet there’s a risk that the Fed cuts even deeper than the market is factoring in.

We think the market is partially preparing for the risk of even deeper rate cuts than linear instruments are pricing. To see how dramatic those are, we can look at options on SOFR futures and model what’s being priced by the volatility surface.

We are seeing the same story if we look at Fed Funds Futures data. Fed rate hikes until June, then rate cuts to follow.

How did Biden’s lawyers and now the DOJ figure out that Biden has classified documents all over the place? Probably from reading “The Hardy Boys.” Except that Biden didn’t cleverly hide classifed documents. Rather, he carelessly left them lying around at The Penn Biden Center and his home in Wilmington Delaware that he shared with his son, Hunter. And probably on the Amtrak train he would take from Wilmington to Union Station in DC. And probably at Chinatown Garden, a short walk from The White House.

The first headline I saw when I turned on Bloomberg.com was “DOJ Officials Find More Classified Documents at President Biden’s Home.” This is an improvement! So far, the task has been handled by Biden’s private attorneys who don’t have proper security clearance; at least the Justice Department is finally getting involved!

But back to the US yield curve. It is now the most inverted in 30+ years as M2 Money growth stalls. Inverted yield curves have preceded recessions in the past.

But as China reopens and Europe is experiencing a warmer winter than expected (meaning that Europe has sufficient natural gas reserves) and US inflation cooling,

we are seeing market-implied odds of a recession falling in January.

I am still betting on a recession in the second half of 2023.

First, US default risk as measured by credit default swaps remains elevated (primarily because Biden and Democrats refused to cut wasteful spending or reign in non-retirees on Social Security). And NY Fed’s Reverse Repos remain elevated.

And then we have Citi’s economic surprise index for the US at -17 as The Fed slows money growth to 0%.

I wish I knew a place where inflation and insane Federal government spending and policies doesn’t exist.

The Thrill Is Gone from the US housing market as M2 Money growth fells to 0%.

US Existing Home Sales fell -1.5% from November to December (MoM) to 4.02 SAAR units sold. That translates to a depressing -34% decline since December 2021 (YoY).

On the positive side, these numbers are better than expected (-3.4% MoM expected). Still, these numbers are pretty dismal.

Existing home sales MEDIAN PRICE fell to $366.9k as M2 Money growth vanishes. And inventory of existing homes for sale remains lower than pre-Covid levels.

Let’s see what Powell and the Gang (aka, The Federal Reserve Board of Governors) does with interest rates going forward.

Today, the 10-year Treasury yield is up 7.1 basis points, but the real action is in Europe where sovereign yields are up 11.5 bps in France, 9.8 bps in Germany and 18.6 bps in Italy.

Notice that the debt ceiling keeps on climbing once the Kabuki Theater of Democrats and Republicans is over.

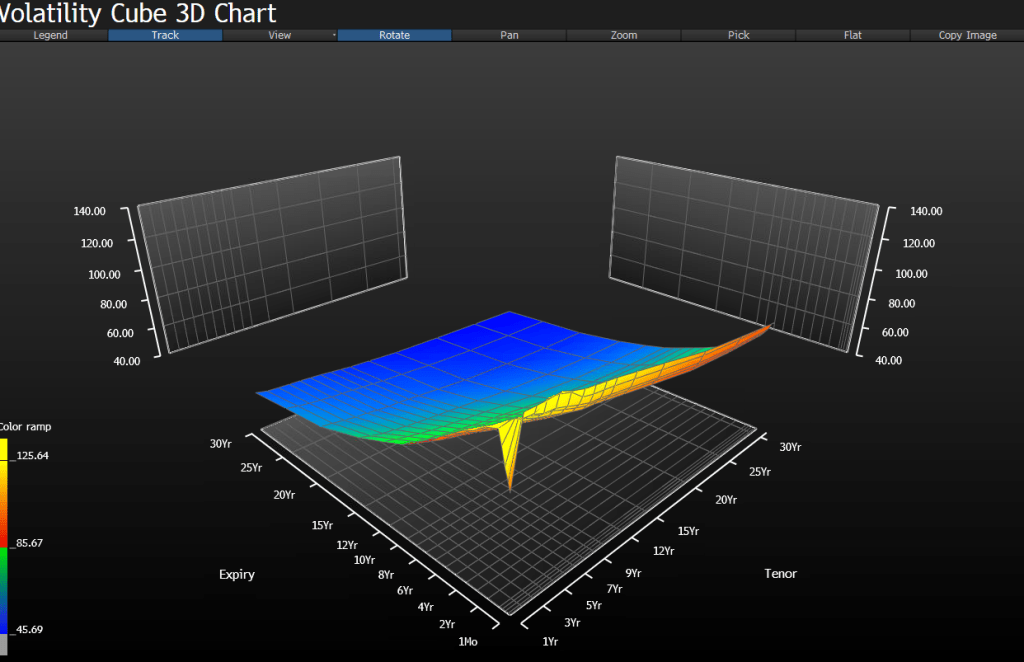

The Volatility Cube for the US CDS 1 year signals that it will all be over soon.

So, Yellen and Treasury are threatening us with taking away Social Security and Medicare if we don’t agree with their lavish Pelosi-like spending sprees and debt.

And why exactly is Janet Yellen flying to China? I admit Washington DC has lousy Chinese food, but at least I hope Yellen takes Hunter Biden with her to negotiate the impending US default and debt workout.

I watched Biden’s Press Secretary Karine Jean Pierre giving Biden credit for the lowest unemployment rate in US history thanks to his economic policies. And Biden mentioned that he inherited a terrible economy from Trump.

Hmmm.

Let’s let the data talk.

Covid was horrific (I almost died from it), but it was the government response to Covid there was disastorous. Government shutdowns (and the masking of the populace) killed off numerous small businesses and sent jobless claims soaring in 2020 (white line) and U-3 unemployment rate rose to the highest level since The Great Depression.

The response from The Federal Reserve was a massive printing of money (green line). And after governments stopped their economic shutdowns (coupled with massive money printing), we saw jobless claims and unemployment shrink rapidly BEFORE Biden took office as President.

The 1981 recession begat an epic borrowing of money by The Federal government (under House Speaker Tio O’Neill D-MA) and we saw another explosion in Federal debt under House Speaker Nancy Pelosi D-CA TWICE, once in 2009 following the financial meltdown and again in 2020 following the Covid economic lockdowns.

So does Trump get any thanks for the rapidly improving labor market before his ouster by Biden? Of course not. But who gets the blame for the staggering growth in Federal debt? House Speaker Nancy Pelosi.

The US did get positive wage growth under Biden, but due to inflation, American workers have experienced 21 straight months of NEGATIVE wage growth.

While Trump tried deregulation to free-up the US economy, Biden has consistently used regulation as a weapon of obidience. His slavish obidience to activist groups on the environment, which is a shame since temperatures have actually been coming down since 2016.

When you look at the data, Trump actually set in motion the jobs recovery, not Biden. Other than helping to create inflation, I can’t think of one positive thing Biden has done for the economy.

On an unrelated note, why is US FBI Director Chris Wray at the World Economic Forum in Davos Switzerland when there is a top secret document fiasco going on in DC and Delaware?

December’s housing construction numbers are a mixed bag. On the one hand, US housing starts are down -1.36% from November to December, but down -21,8% since December 2021 (YoY).

The good news? 1-unit (single family detatched) rose 11.26% from November to December (MoM). But 5+ (multifamily) starts are down -18.91% MoM.

But 5+ unit PERMITS are up 7.14%. Perhaps Hunter Biden can now rent an apartment rather than pay his father $50,000 a month in rent for Joe’s Wilmington Delaware house.

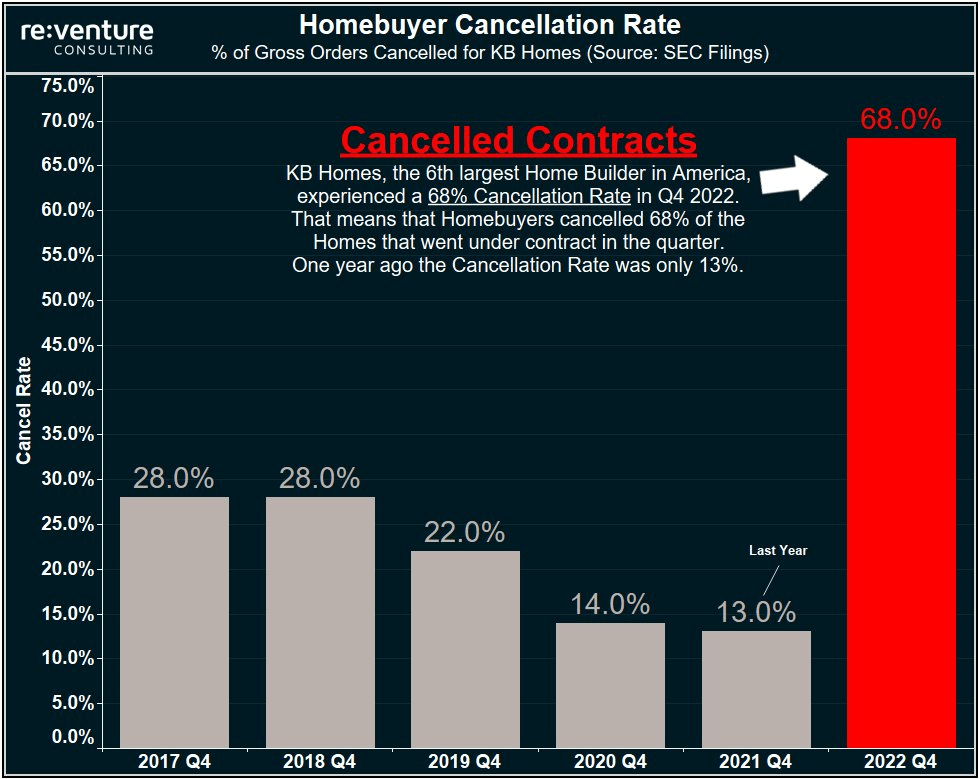

KB Homes experienced a 68% cancellation rate in Q4 2022.

This version of The Scream is one of four made by Edvard Munch, and the only one outside Norway. It is coming up for auction at Sotheby’s in New York.

Soft landing for the US economy? It is looking less and less likely. The bond market (10-year Treasury yield) just shed -14.1 basis points. As I always told my investments students, any 10 basis point shift in the 10-year Treasury yield is significant.

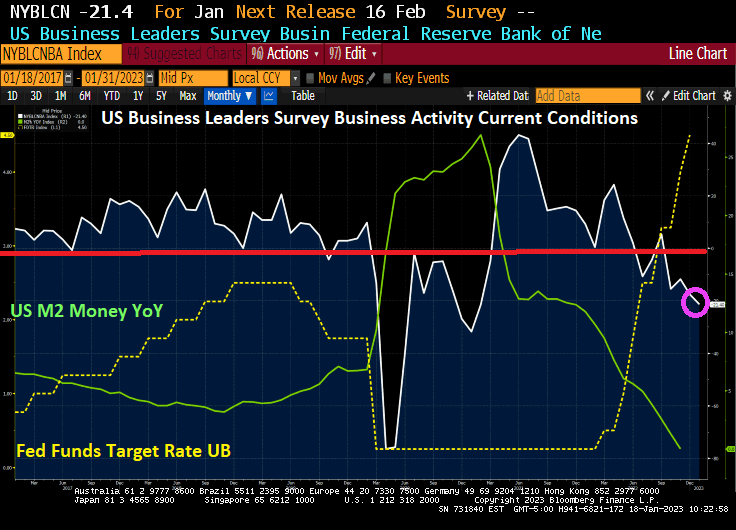

Let’s start wit the US business leaders survey of current conditions. It just crashed to -21.4

Then we have US industrial production, down -0.7% in December. And is up only 1.65% year-over-year as M2 Money growth stalls.

Capacity Utilization plunged more than expected to 78.7% (79.5% exp).

Biden claiming the US economy is strong is pure Fantasy Island.

Today, Jean Pierre annouced that Biden’s economic plans are working.

Mortgage applications increased 27.9 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 13, 2023. But mortgage applications are 60% lower than the same week last year.

The Refinance Index increased 34 percent from the previous week and was 81 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 25 percent from one week earlier. The unadjusted Purchase Index increased 32 percent compared with the previous week and was 35 percent lower than the same week one year ago.

Here are the stats.

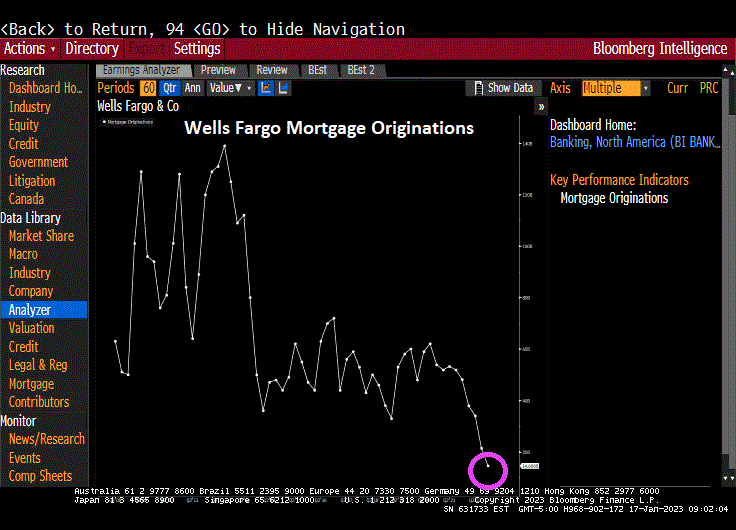

One lender in particular, Wells Fargo, smells blood in the economic waters, and has cut back mortgage originations.

Just remember, mortgage applications generally rise in the first part of the year until May, then start slowing until the last week of the year. This is called seasonality. But despite the fast growth this year, purchase applications are still down -35% compared to last year at this time.

You must be logged in to post a comment.