The Federal Reserve slowed its drive to rein in inflation and said further interest-rate hikes are in store as officials debate when to end their most aggressive tightening of credit in four decades.

Policymakers lifted the Fed’s target for its benchmark rate by a quarter percentage point to a range of 4.5% to 4.75%. The smaller move followed a half-point increase in December and four jumbo-sized 75 basis-point hikes prior to that.

The unanimous decision by the Federal Open Market Committee was in line with financial market expectations.

Markets are forecasting a pivot after the June meeting in 2023.

The face of The Federal Reserve. Although Yellen is now Biden’s Secretary of Treasury.

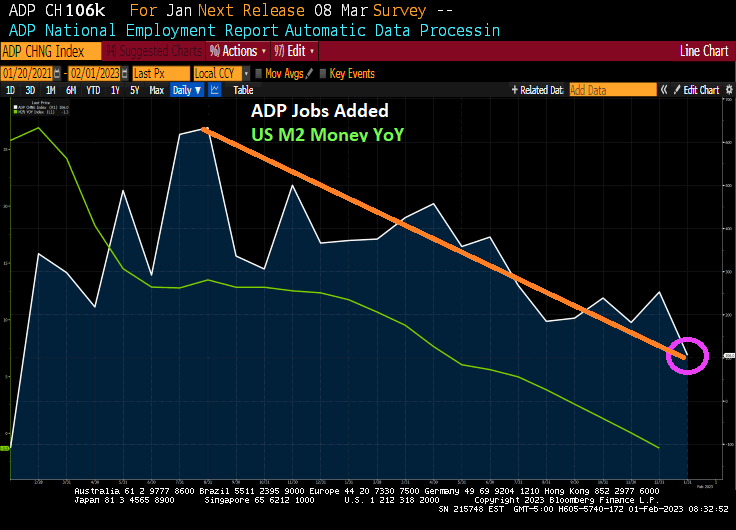

The US economy is slowing down. In fact, ADP jobs added just printed at 106k in January, the lowest reading since August 2021. ADP jobs added follows the slow down of M2 Money growth YoY as The Fed tightens its monetary policy.

Do I detect a trend (orange line)?

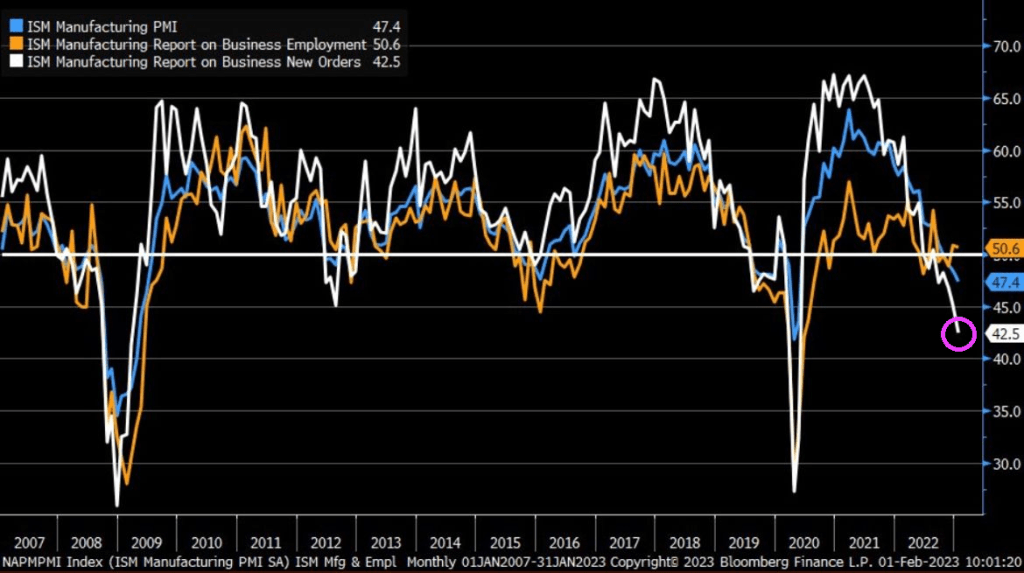

Speaking of trends, check out ISM Manufacturing New Orders. Lowest since Great Recession of 2008 (if I exclude the government economic shutdown Covid recession).

I doubt that January’s ADP report or the ISM Manufacturing report will be mentioned in Biden’s State of the Union address.

The January mortgage applications book is closed. And we are off to another year of rising applications until May. Then the downhill slide.

Mortgage applications decreased 9.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 27, 2023.

The Refinance Index decreased 7 percent from the previous week and was 80 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 10 percent from one week earlier. The unadjusted Purchase Index increased 7 percent compared with the previous week and was 41 percent lower than the same week one year ago.

US mortgage rates have been steadily declining since November 2022.

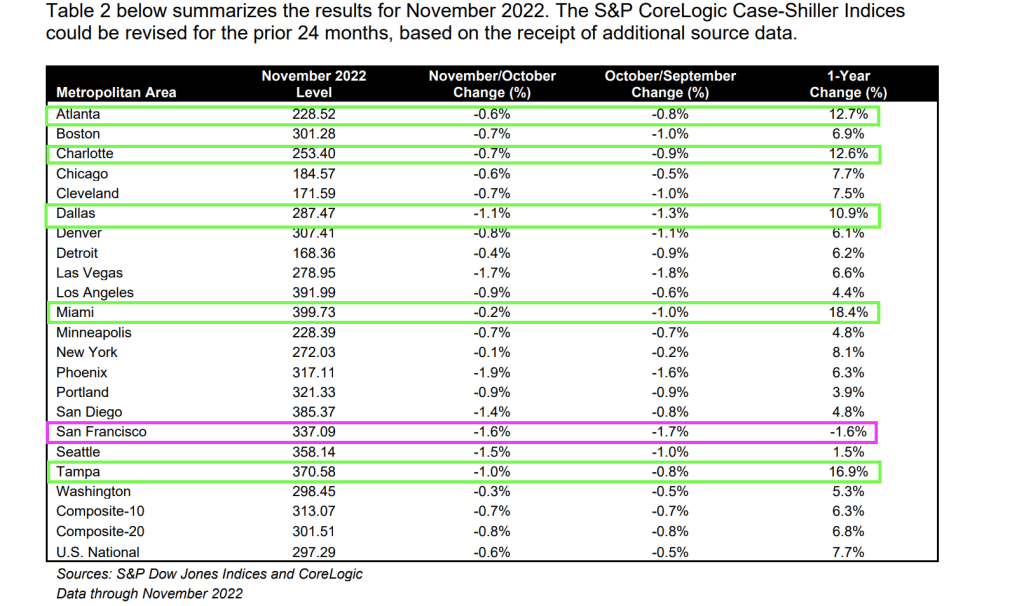

On a year-over-year (YoY) basis, the Case-Shiller National home price index slowed to 6.77%. On a month-over-month (MoM) basis, the CS National index fell -0.54%. That is the 5th straight month of home price declines.

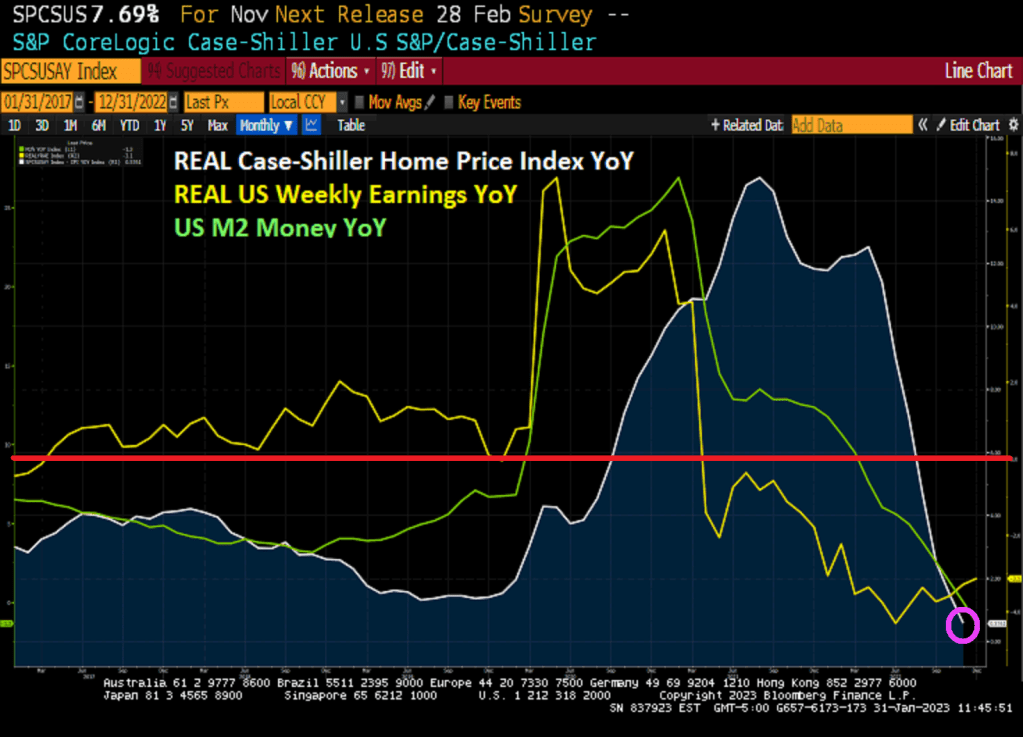

In REAL terms, the Case-Shiller National home price index is up only 0.58% YoY as REAL Weekly Earnings growth is negative at -3.1% YoY.

Only San Francisco fell on a YoY basis (down -1.6%). Five metro areas were above 10% and they are all in the South. Atlanta, Charlotte. Dallas, Miami and Tampa.

On MoM basis, every metro area in the Case-Shiller 20 index saw price declines from October to November.

The Federal Reserve’s Open Market Committee (FOMC) is meeting on Wednesday. What will they do?

First, The Fed Funds Target (upper bound) is above the Core US inflation rate YoY. Second, M2 Money growth YoY has slowed to -1.3%.

Of course, the members of the FOMC might decide that this is not enough and may keep raising rates and shrinking The Fed’s enormous balance sheet.

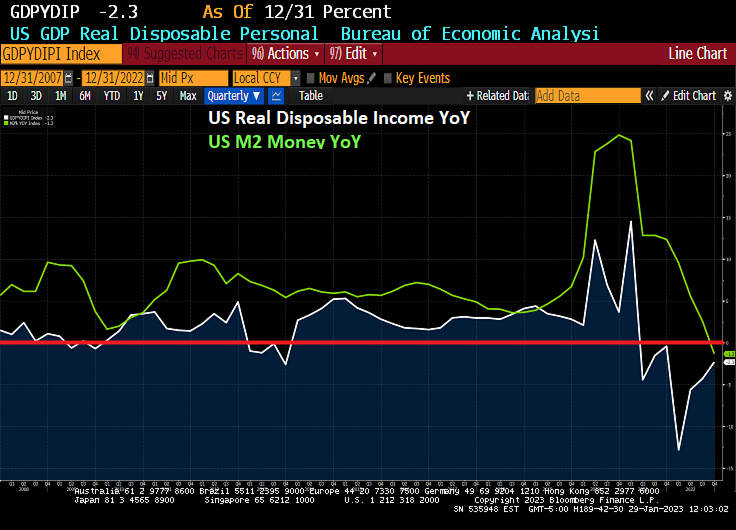

In the “Haven’t they suffered enough?” arena, US real disposable income has fallen by -21% since Biden was sworn-in as President.

On the other hand, the Taylor Rule is still pointing to a target rate of 10% (we aren’t even half way there at 4.50%).

Oh and the price of insuring against a US debt default remains elevated (since Biden and Schumer are baving like arrogant bullies) and are refusing to negotitate over spending cuts.

The 1Y CDS volatility cube indicates that it will all be over soon.

Welcome to the wonderful world of Bidenomics, giving the US 40 year highs in inflation leading The Federal Reserve to remove its enormous monetary stimulus (known as “The Punch Bowl.”

I previously pointed out that US Real GDP was actually less than 1% year-over-year (YoY) in 2022, hardly a fantastic number given the trillions in Biden/Pelosi/Schumer spending (Omnibus, Infrastructure, etc) and Powell/Fed’s whopping monetary stimulus in 2020. But real disposable income, the amount households have left to spend after adjusting for inflation, had been falling for 7 straight months.

In fact, REAL disposable personal income peaked in March 2021, shortly after Biden was sworn-in as President in Janaury 2021 at $19,213.9 billion (or $19.214 TRILLION). As of December 2022, real personal disposable income had fallen to $15,213.0 or $15.213 TRILLION. That is a loss of $4 TRILLION since March 2021. Or a -21% Loss in Real Disposable Income.

I was interviewed by James Rosen at Fox News on the exploding US debt and whether it is a problem. I said “Yes, the sheer size of the US debt load in unsustainable and will get worse if interest rates rise.” Well, here we are!

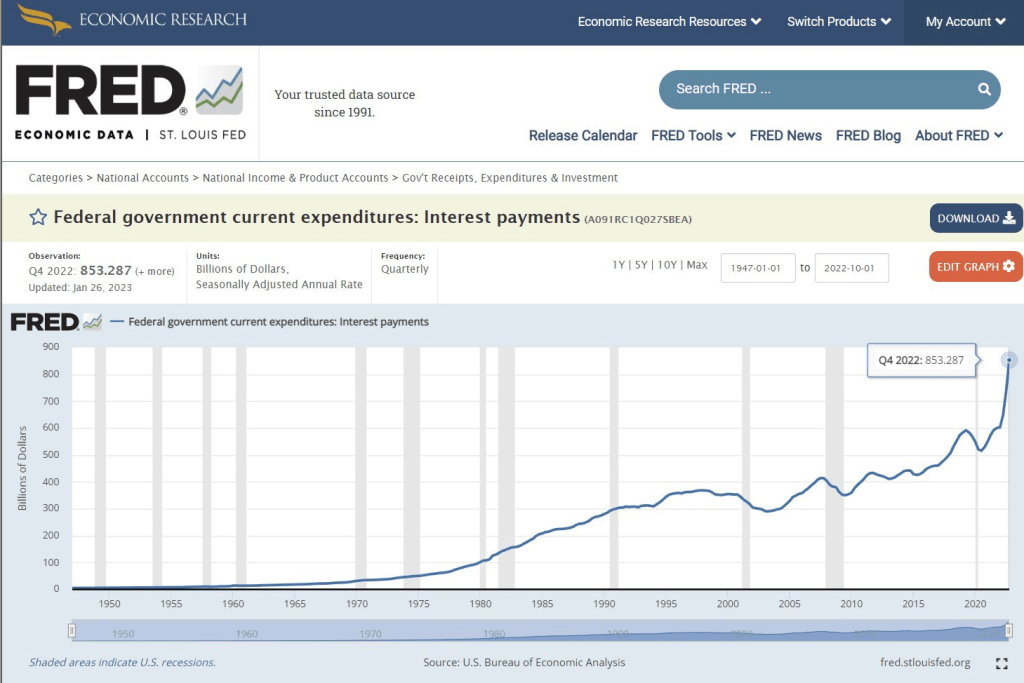

The US paid $853 billion in interest for the $31 trillion in debt in 2022.

That is more than the US Defense budget in 2023.

If the Fed keeps rates at at these levels (or higher), the US we will be at $1.2 trillion to $1.5 trillion in interest paid on the debt.

The US govt collects about $4.9 trillion in taxes.

Thanks for this, Biden, Pelosi, Schumer! Aka, The Spend Squad!

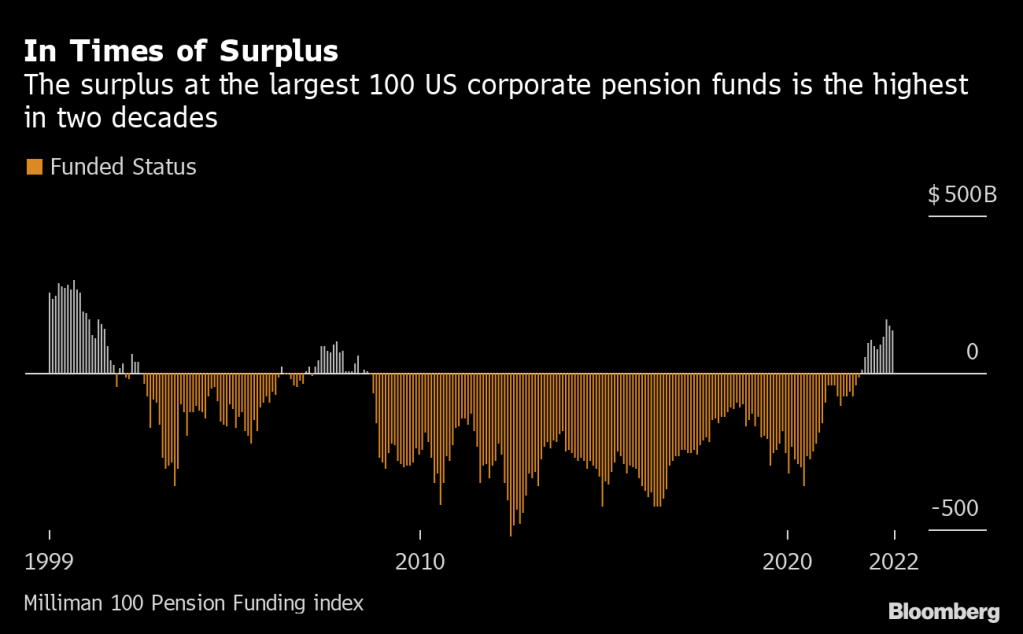

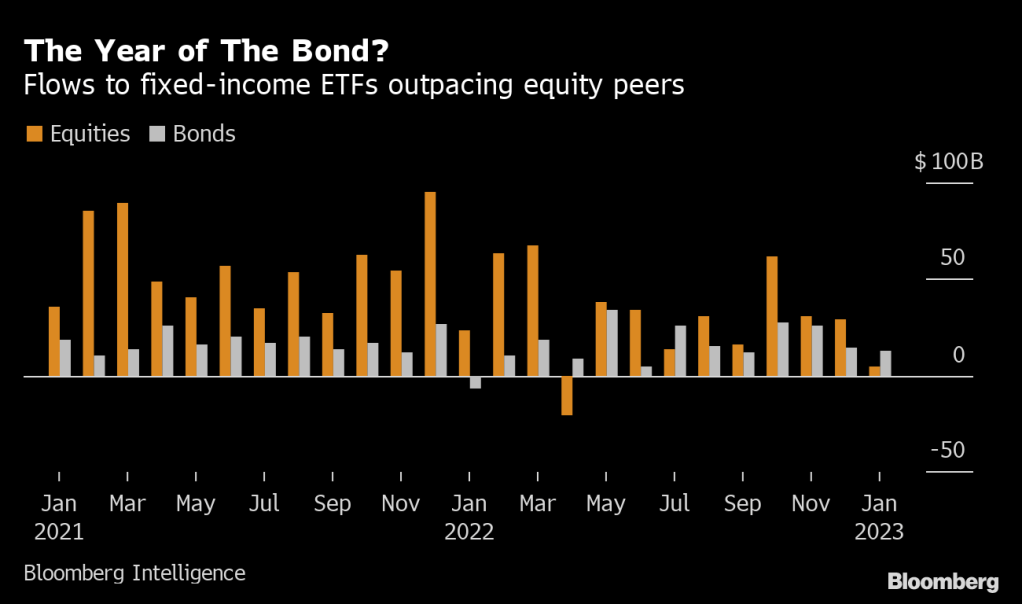

Despite polticians like President Biden cheerleading his great economic accomplishments and Treasury Secretary Janet Yellen dipping into Social Security to fund the Federal government (much like Biden’s dipping into the Strategic Petroleum Reserve), there are serious problems facing America’s middle class and low-wage workers. Inflation is still brutal (but slowing) and REAL weekly earnings growth has been negative for 21 straight months (meaning that Biden’s bragging about wage growth has been destroyed by the inflation created by his energy policies and massive spending sprees). Personal spending rate YoY has plunged -53.5% to cope with inflation. To quote Joe Biden (Chauncy Gardner), “All is well in the garden.” But all is not well in the garden. As a result, we are now seeing pension funds jumping from stocks to bonds.

(Bloomberg) For some of America’s biggest bond buyers, the soft-versus-hard-landing debate on Wall Street might be a sideshow. They’re getting ready to swoop in with as much as $1 trillion, no matter what happens.

One of the pillars of the trillion-dollar pension fund complex is now awash in cash after struggling under deficits for two decades. This rare surplus at corporate defined-benefit plans, thanks to surging interest rates, means they can reallocate to bonds that are less volatile than stocks — “derisking” in industry parlance.

Strategists at Wall Street banks including JPMorgan Chase & Co., Bank of America Corp. and Wells Fargo & Co. say the impact will be far-reaching in what’s already being coined “the year of the bond.” Judging from the cash flooding into fixed income, they’re just getting started.

“The pensions are in good shape. They can now essentially immunize — take out the equities, move into bonds and try to have assets match liabilities,” Mike Schumacher, head of macro strategy at Wells Fargo, said in an interview. “That explains some of the rallying of the bond market over the last three or four weeks.”

An irony of pension accounting is that a year like last year, with its twin routs in stocks and bonds, can be a blessing of sorts to some benefit plans, whose future costs are a function of interest rates. When rates climb, their liabilities shrink and their “funded status” actually improves.

The largest 100 US corporate pension plans now enjoy an average funding ratio of about 110%, the highest level in more than two decades, according to the Milliman 100 Pension Funding index. That’s welcome news for fund managers who suffered years of rock-bottom interest rates and were forced to chase returns in the equity market.

Now, they have an opportunity to unwind that imbalance and Wall Street banks pretty much agree on how they’ll use the extra cash to do it: buying bonds, and then selling stocks to buy more bonds.

Already this year fixed-income flows are outpacing those of equity funds, marking the most lopsided relationship since July.

How much of that is due to derisking by pension funds is anyone’s guess. Some of the recent rally in bonds can be ascribed to traders hedging a growth downturn that would hit stocks hardest.

But what’s obvious is their clear preference for long-maturity fixed-income assets that most closely match their long-dated liabilities.

Pension funds need to keep some exposure to stocks to boost returns, but that equation is changing.

Once a corporate plan reaches full funding, their aim is often to derisk by jettisoning stocks and adding fixed income assets that line up with their liabilities. With the largest 100 US corporate defined benefit funds riding a cash pile of $133 billion after average yields on corporate debt more than doubled last year, their path is wide open.

With yields unlikely to go above their peak level once the Federal Reserve hits its terminal rate of about 5% around the middle of the year, there’s rarely been a better time for them to make the switch to bonds.

Even if growth surprises on the upside and yields rise, causing bonds to underperform, the incentive is still there, said Bruno Braizinha, a strategist at Bank of America.

“At this point and considering where we are in the cycle, the conditions are favorable for de-risking,” Braizinha said in an interview.

JPMorgan’s strategist Marko Kolanovic estimates derisking will lead pension managers to buy as much as $1 trillion of bonds; Bank of America’s Braizinha says a $500 billion buying spree is closer to the mark.

How about gold? As the probability of a US debt default looms (as Bride of Chucky Schumer stomps his feet and says ” No budget cuts!”) and the US Treasury 10Y-3M yield curve remains inverted, gold is soaring.

Perhaps pension funds should by gold rather than cryptos.

Kansas City is a wonderful city. But the KC Fed’s Services Survey is not. In fact, it plunged to -11 for January. Rough start to the new year.

The decline in the KC Fed survery mirrors that of other regional Fed indices, indicating a slowdown in the US economy as The Fed withdraws the monetary punch bowl,

Despite the hoopla, remember that US Real GDP growth only grew at less than 1% on a year-over-year basis in 2022.

You must be logged in to post a comment.