(Forbes) – Credit Suisse’s Zoltan Pozsar argues Bretton Woods II crumbled when the G7 countries seized Russia’s foreign exchange reserves. Keeping money inside financial institutions like the IMF was considered risk free. That is clearly no longer the case. Similarly, Bretton Woods I collapsed when Nixon took the US of the gold standard back in 1971 when dollars were convertible to gold at a fixed exchange rate of $35 an ounce. This led to Bretton Woods II, backed by “inside money” or the dollar, which itself is not linked to gold or any other commodity.

Now the basis of this system, which has operated for the past 50 years, is being called into question. The sanctions on Russia, which showed that reserves accumulated by central banks can simply be taken away, raised the question of “what is money?”

That question may explain why Pozsar believes a huge shift in the way the world organizes money and reserves is now underway, “creating a “Bretton Woods III backed by outside money,” (gold and other commodities). Including crude oil and bitcoin.

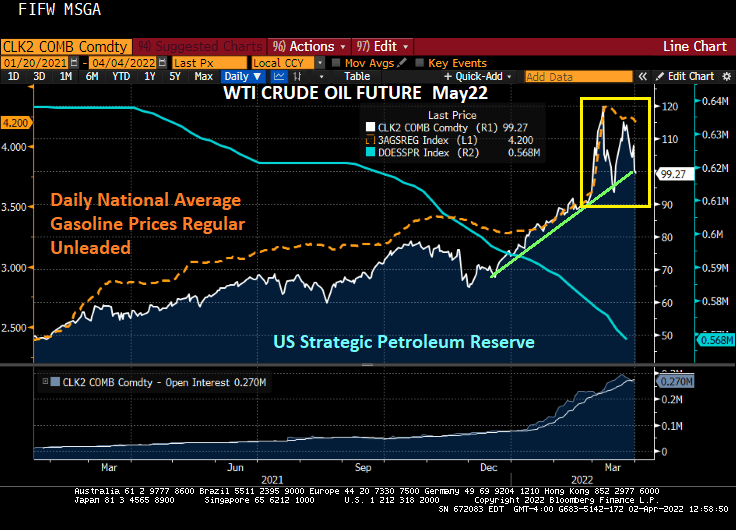

At least crude oil has fallen below $100 as Biden merrily drains the Strategic Petroleum Reserve (SPR). Gasoline prices have fallen slightly as this is being done before the midterm elections with political, not economic, intent. Once the midterms pass, will Biden continue draining the SPR until there is little left forcing the US to convert to “green energy”?

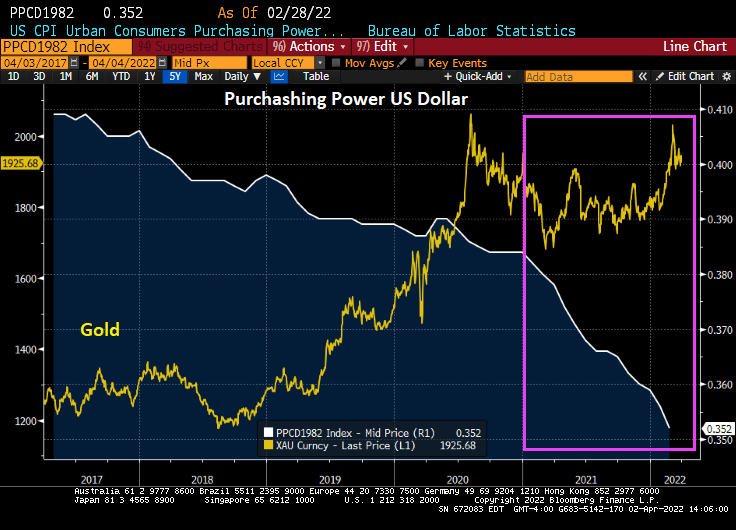

The purchasing power of the consumer dollar took a plunge under Biden as other commodities such as Bitcoin and crude oil soared.

An alternative asset, gold, have generally risen under Biden’s Reign of Error, but particularly after the Russian invasion of Ukraine.

Politicians love to spend money, often recklessly. And with The Fed monetizing Federal government expenditures, the purchasing power of the US dollar for consumers is sinking faster than The Titanic.

You must be logged in to post a comment.