Tennessee Ernie Ford sang it best. $36 tons of debt. Another day older and deeper in debt. Notice virually no political candidate will acknowledge or discuss.

The federal government spent $1.8 trillion more than it collected in tax revenue in fiscal year 2024, according to figures released Friday by U.S. Treasury Department.

Congress has run a deficit every year since 2001. In the past 50 years, the federal government has ended with a fiscal year-end budget surplus four times, most recently in 2001.

The deficit for fiscal 2024 was $1.8 trillion, or $138 billion higher than the prior year’s deficit. As a percentage of GDP, the deficit was 6.4%, an increase from 6.2% in fiscal 2023. The 2024 deficit is $196 billion lower than in 2023, excluding the effect of the Supreme Court’s 2023 decision in Biden v. Nebraska regarding student loan programs, according to year-end data from the September 2024 Monthly Treasury Statement of Receipts and Outlays of the United States Government.

And then we have the REAL disaster in the form of unfunded liabilities of $220 TRIILLION (or $651,000 per citizen). For a family of 5 citizens (like my household), that amounts to $3.26 MILLION per household of 5.

Imagine Kamala’s filibustering a response to a question about the national debt and unfunded liabilities. Other than “Donald Trump.”

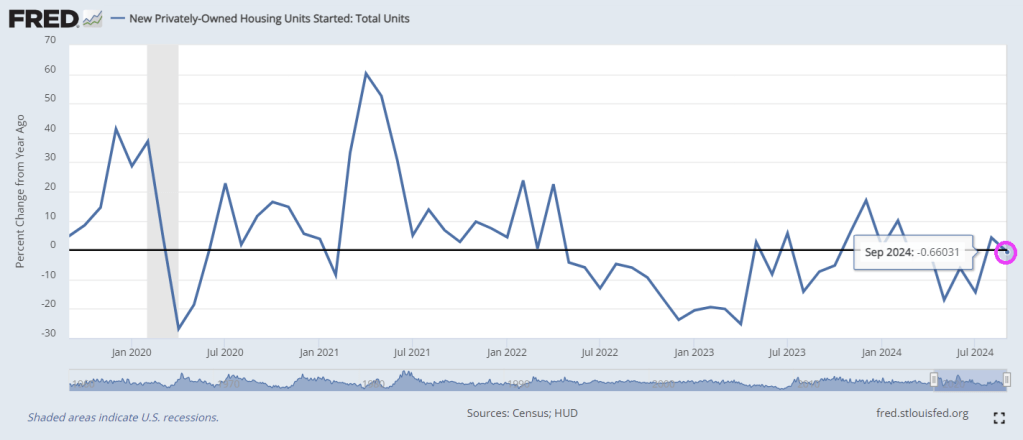

After surprising top the upside in August, Housing Starts and Building Permits disappointed in September, declining more than expected (-0.5% MoM and -2.9% MoM respectively)…

Source: Bloomberg

Under the hood, multi-family permits plunged 10.8% MoM (and multi-family starts dropped for the second straight month). Single-family starts rose 2.7% MoM and permiots inchjed higher by 0.3% MoM…

Source: Bloomberg

Rate-cut expectations appear to have taken the excitement out of the building market…

Source: Bloomberg

Housing Completions also dropped (but the BLS thinks construction jobs continue to rise non-stop)…

Source: Bloomberg

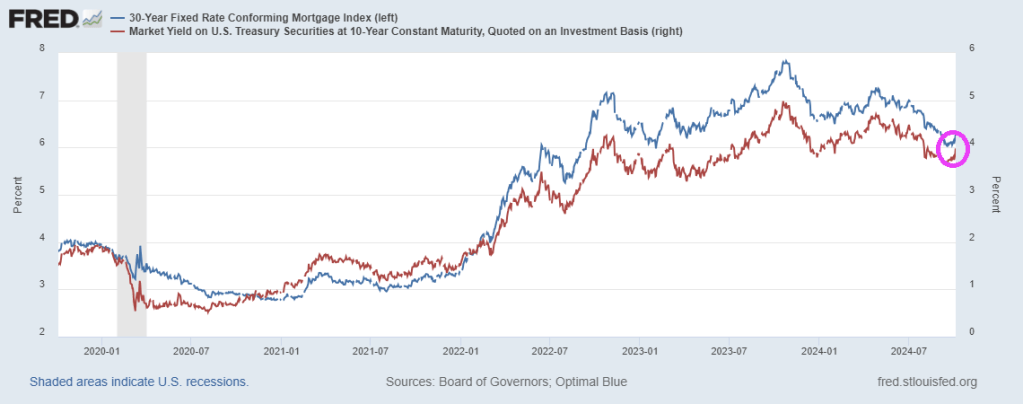

So, The Fed cuts short-term rates… mortgage-rates rise… and builders slow their building plans… that’s not how it’s supposed to work!

Mortgage rates are rising again with Friday’s surprising jobs report. But as it just a false election report. If Rasmussen is correct, mortgage rates should FALL again.

The Presidential and Vice Presidential debates thus far feature weak moderators asking lame questions. For example, there are still 97 hostages stll held by Hamas and what would the candidates do to get them released? (Hint: Trump/Vance would have sensible responses. Harris would just laugh and say she was raised in a middle class family and Walz would look like a deer in the headlights. Then we have national debt of $36 trillion, $271K per taxpayer.

But the hidden bomb that will never be discussed is unfunded liabilities (entitlements) such as Social Security and Medicare. Currently, unfunded liabilities are $219 TRILLION or $650K per citizen.

Of course, Biden/Harris have let the southern border wide open to criminals and uneducated Democrat voters who will voter for MORE entitlements.

So, when will the lame debate moderators ask HARD questions? And can Harris attempt to answer one hard question without laughing or falling back on lame “I was raised in a middle-class household.” etc.

Whenever the 10Y-2Y Treasury yield curve slope goes negative, it is following by positive slope … then recession. Like clockwork.

Following every recession since the 1970s, the 10Y-2Y Treasury yield curve slope has risen, then declined. This time around, the 10Y-2Y Treasury curve has remained negatively-slope long than usual suggesting a larger than normal snapback. Into a hard landing.

Democrats in particular love hard landings because that green lights them for massive wasteful spending.

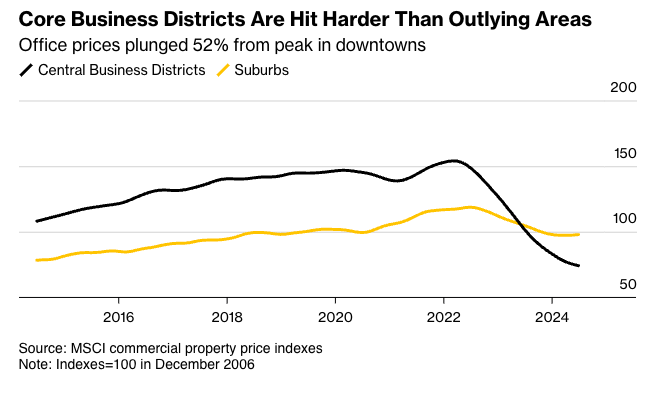

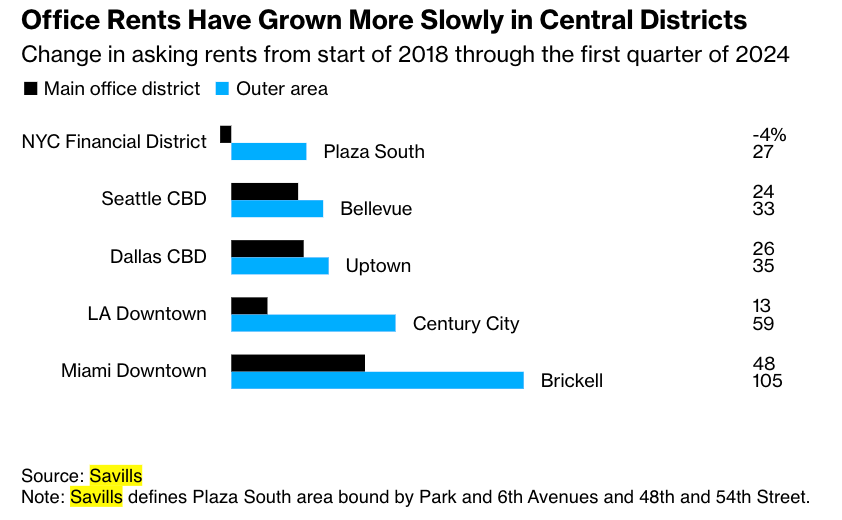

Commercial real estate market challenges are more severe for older office towers in downtown metro areas than those outside city centers. The mismatch between funding needs and available credit in a high-interest-rate environment has also intensified the strain on building owners, as elevated tower vacancy rates persist across many markets due to the ongoing trend of remote work becoming the norm.

Aging business districts from Los Angeles to Chicago to Boston of zombie towers with high vacancy rates that have no use in today’s economy.

Big landlords, including Brookfield, Blackstone, and Starwood Capital Group, have walked away from older downtown towers in recent quarters.

The latest data from MSCI shows office values in metro areas have crashed 52% from their highs. Some of the worst declines have occurred in San Francisco, Manhattan, Washington, and Boston.

Source: Bloomberg

Between 2019 and 2023, about $557 billion of value evaporated from US offices due to a multi-year slide in demand, with older towers quickly falling out of favor with companies, according to an estimate by economists at Columbia and New York universities. CBRE Group noted that only 2% of towers in the US are considered top-tier, with rents 84% higher than the rest of the market.

Data from brokerage Savills shows office rents in business districts have grown slower than rents for similar buildings outside metro areas.

Source: Bloomberg

The move to new towers highlights how, for decades, the bubbles in legacy downtown districts, fueling economies, have ended for now, and older towers will have to be torn down.

To be very frank. It’s a crisis. Democrats running the crime-ridden metro area are delusional and blinded by their woke religion as the city’s population recently crashed to a 100-year low, and violent crime remains a major issue.

We’ve had conversations with multiple folks at wealth management and investment banking firm Stifel Financial about the latest shift of operations outside the dying business district to a new tower in a much safer and newer district. At first, Stifel contemplated leaving the city for the suburbs because far-left Democrats in City Hall could not enforce law and order.

CRE foreclosures are on the rise.

Don’t forget about Soros-funded district attorneys not enforcing the law in large cities. Expect more of the same if Harris/Walz win the election.

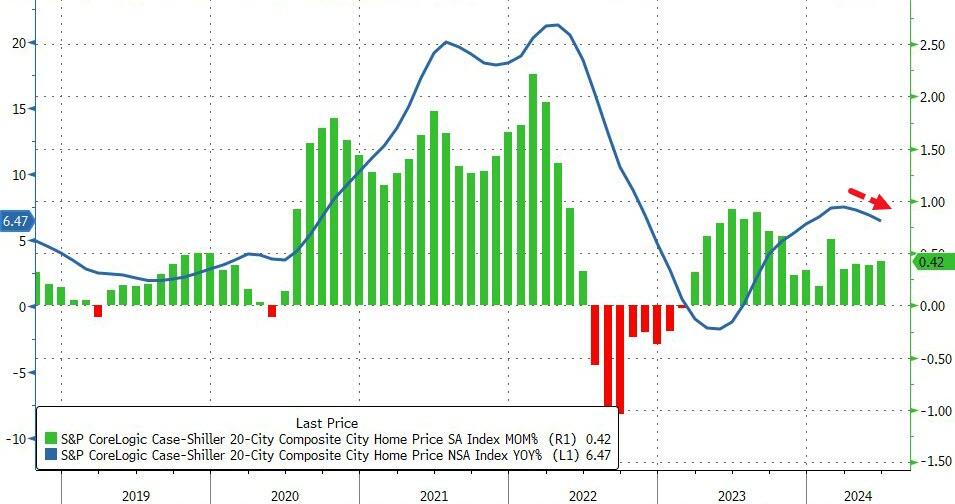

Big bubbles! US home pricest hit an all-time high as The Fed keeps its foot on the monetary gas pedal following the Covid economic shutdown in 2020.

Home prices in America’s 20 largest cities rose for the 16th straight month in June (according to the latest data from S&P CoreLogic – Case Shiller – data today), up 0.42% MoM (hotter than expected and accelerating from May). On a YoY basis, prices rose 6.47%, but notably that is the third straight monthly slowdown in the pace of price appreciation…

Source: Bloomberg

Overall, US home prices reached a new record high in June (as median new home prices continued to tread water)…

Source: Bloomberg

Home prices continue to track Fed Reserves closely, but a turning point may come soon…

Source: Bloomberg

Given the smoothing and heavy lag in the Case-Shiller data, it’s hard to find a causal relationship between prices and mortgage rates…

Source: Bloomberg

But, with prices reaccelerating and mortgage rates already back below 7.00% – in anticipation of The Fed – WTF does Powell think is going to happen when he actually starts cutting with prices at these record highs.

The Freddie Mac HP index shows the variation in home price growth. New Jersey coastal towns of Atlantic City and Ocean City grew at 10% YoY while Lake Charles LA declined by -2% YoY.

The US is already at $35+ trillion with unfunded liabilties totalling $218+ trillion. Of course, the Biden Administration is attempting to cut Medicare for seniors and raise the price while handing out unlimited benefits to illegal immigrants.

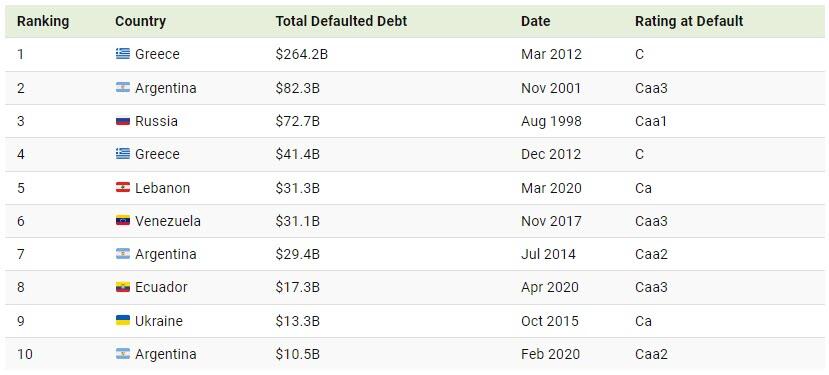

.Given the financial burden of war, the country suspended interest payments on international debt over the last two years, which was set to expire on August 1, 2024.

Without this new debt restructuring, this default would have ranked among the 10 largest in recent history. The last time Ukraine defaulted on its debt was in 2015, after Russia’s invasion of Crimea.

Below, we show the biggest sovereign debt defaults between 1983 and 2022:

Greece’s $264.2 billion default in 2012 stands as the largest overall, unfolding when the country was mired in recession for the fifth consecutive year.

The country defaulted again just nine months later, making it the fourth-largest ever. Leading up to the crash, Greece ran significant deficits despite being one of the fastest-growing countries in Europe. Furthermore, in 2009, the newly elected prime minister revealed that the country was $410 billion in debt—substantially more than previous estimates.

With the second-highest default recorded, Argentina failed to repay interest on $82.3 billion in foreign debt in 2001. Like Greece, it is a repeat offender, defaulting numerous times since independence in 1816. Today, Argentina is the largest debtor to the International Monetary Fund, despite being Latin America’s third-largest economy.

Following next in line is Russia’s 1998 default on $72.7 billion in loans, coinciding with a currency crisis that erased more than two-thirds of the ruble’s value in a matter of weeks. That year, several other countries including Venezuela, Pakistan, and Ukraine defaulted on their debts after the Asian Financial Crisis of 1997 spurred instability in global financial markets.

Just as 1998 saw a wave of defaults, 2020 was a year marked by major debt upheavals. Due to the pandemic and collapsing oil prices, it was a record year for sovereign defaults, reaching seven in total. Among these, Lebanon, Ecuador, and Argentina saw the largest defaults amid deepening fiscal pressures.

Harris is just another free-spending politician who will eventually lead the US into default. But at least Harris/Walz exude joy.

At least Harris/Walz haven’t adopted (stolen) the phrase “Work makes one free”.

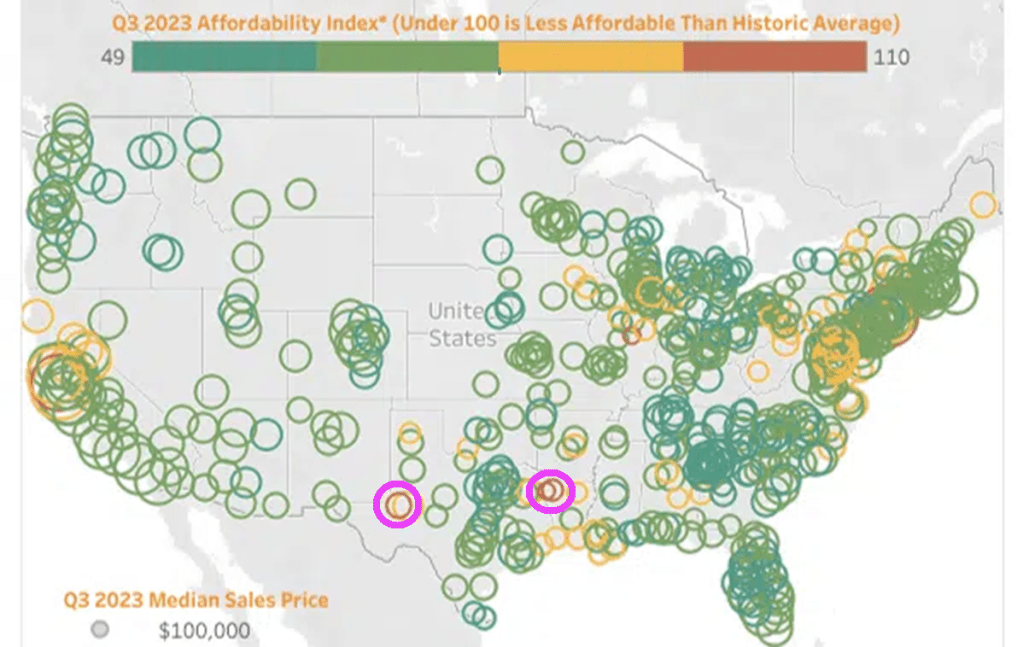

Although the Attom data is from Q3 2023, not much has changed. Under Biden (and his HUD Secretary Marcia Fudge, Fed Chair Jay Powell, and Treasury Secretary Janet Yellen), I did manage to find TWO AFFORDABLE areas to live: Shreveport Louisiana and Midland/Odessa Texas. The housing market remains unaffordable for millions of Americans.

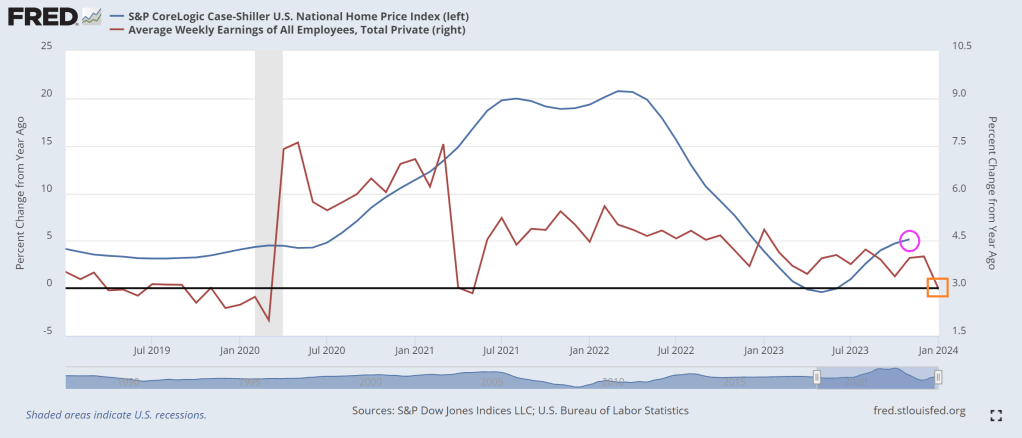

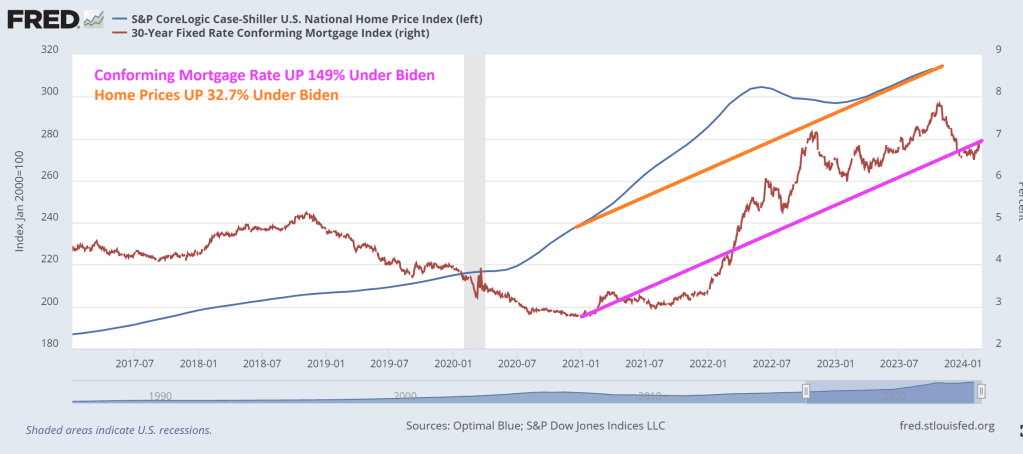

I am not surprised given that the Case-Shiller National home price index has risen by 32.7% under Biden while mortgage rates are up … 149%.

Robin Hood is a legendary heroic outlaw originally depicted in English folklore and subsequently featured in literature, theatre, and cinema. Traditionally depicted dressed in Lincoln green, he is said to have stolen from the rich to give to the poor. Politicians have created the new “Forgotten Man” by Amity Shlaes.

However, politicians like Joe Biden, Chuck Schumer, Mitch McConnell are “reverse Robin Hoods” dressed in business suits (although Jamie Raskin D-MD is often seen wearing a bandana and John Fetterman D-PA is often seen in a hoodie and shorts). They instead enact policies that steal from the middle class and give to themselves and the donor class. How do you think that politicians like the Bidens, Obama, Clintons and AOC go in broke and emerge as multi-millionaires?

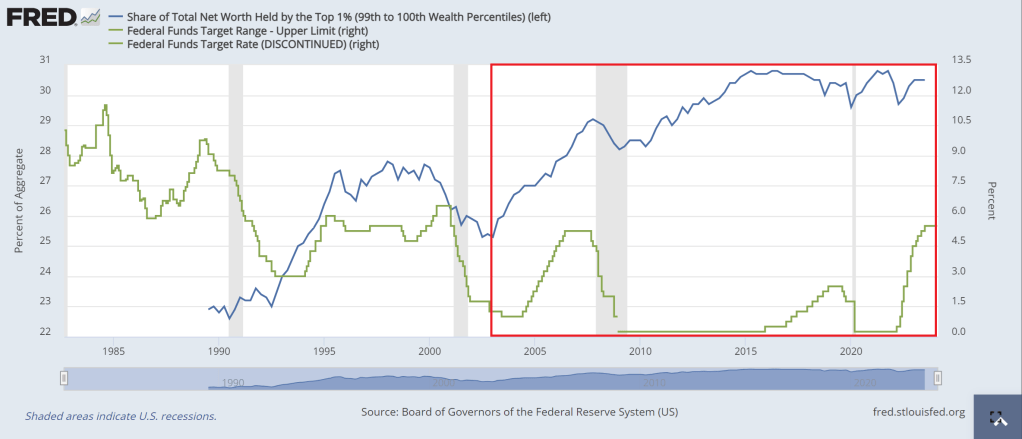

Part of the problem with the reverse Robin Hood model is the Federal Reserve itself. They helped punish the 99% with inflation due to excessive money printing. The share of total net worth held by the top 1% has exploded since The Fed’s rate cuts following the 2001 recession. The Fed has never lowered rates since to levels we saw prior to the 2001 recession, although The Fed is getting close.

Then we have the green energy hysteria (which like pornography excites the brain and distorts logical thinking). Wealthy donors have received a massive windfall (along with China) from Biden/Congress’s green energy spending (scam). The middle class and low-wage workers are now playing higher utility bills (sacrificial lambs on the altar of global warming … or cooling) along with seeing gasoline and diesel prices far higher than before Biden was elected. Gasoline prices are up 46.25% under Biden and diesel prices are up 55.6%.

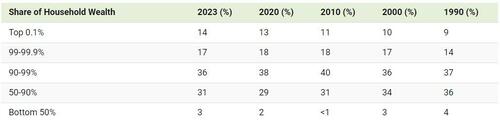

I like this chart of the distribution of household wealth by income group. The top 1% (the elite Pelosi class, are getting wealthier and wealthier. The 90-99% group are doing well, but not as well as the top 1%. The bottom 50% (who the Washington DC elite class seems to have forgotten about)

Here is a table of the same data.

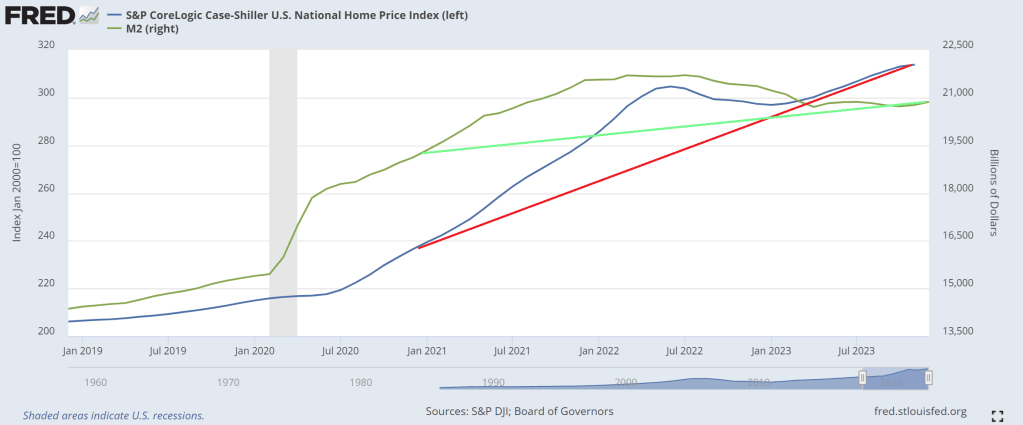

Then we have the exploding mortgage rates under Biden. Rates are up over 155% under Old Grandad Joe Biden. Another shot through the heart of the middle class. And Washington DC is to blame.

Speaking of Washington DC millionaire elites, I want to share this picture with you. Hillary Clinton is NOT Robin Hood but an example of a REVERSE Robin Hood.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.