Calamity Jay Powell is no longer mentioning “transitory” when it comes to inflation, but does Powell and the FOMC have the moxie to ACTUALLY raise rates more than a smidge??

(Bloomberg) — Team Transitory is throwing in the towel.

In a clear sign that the Federal Reserve is shifting to tighter monetary policy, Jerome Powell — who’s spent months arguing that the pandemic surge in inflation was largely due to transitory forces — told Congress on Tuesday that it’s “probably a good time to retire that word.”

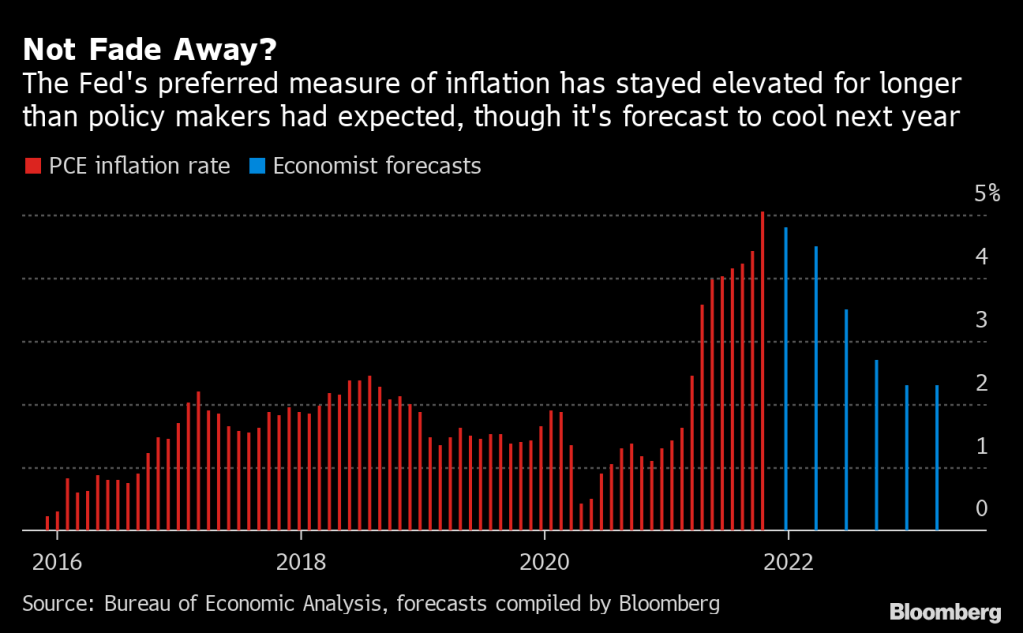

The Fed chair, tapped last week for another four-year term, still thinks inflation will ebb next year.

But in testimony before the Senate Banking Committee, he acknowledged that it’s proving more powerful and persistent than expected, and said the Fed will consider ending its asset purchases earlier than planned.

A number of economists are forecasting cooling inflation next year, which gives Powell an excuse to NOT raise rates, other than just a bit.

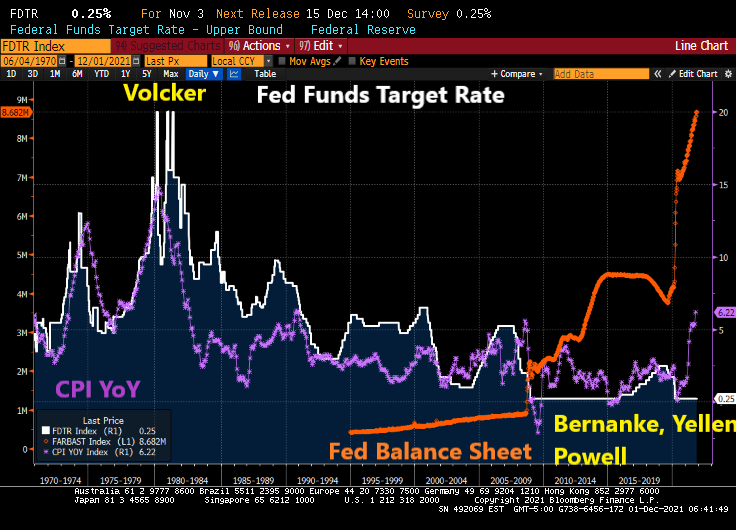

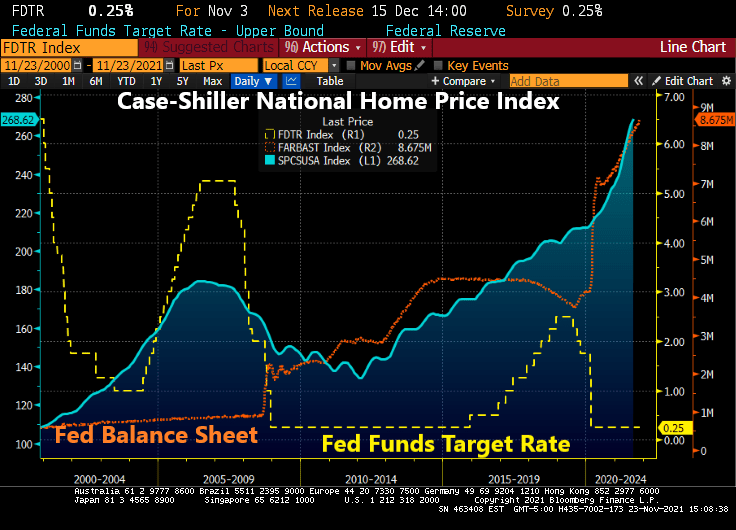

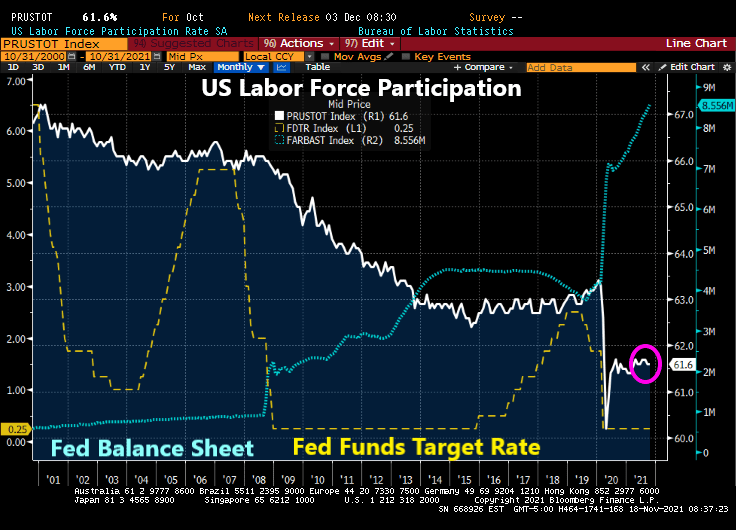

For a little history, inflation was rampant in the 1970s and early 1980s. Fed Chair Paul Volcker, all 6’7 of him, raised the Fed Funds target rate (white line) to 20% on several occasions. The result? Inflation cooled from over 14% in 1980 to 2.46% by 1983. But since 2008, Fed Chairs Bernanke, Yellen and Powell have been the ANTI-Volckers … keeping the Fed Funds Target rate near zero for the the most part and adopted their gut-wrenching quantitative easing programs that are still here today.

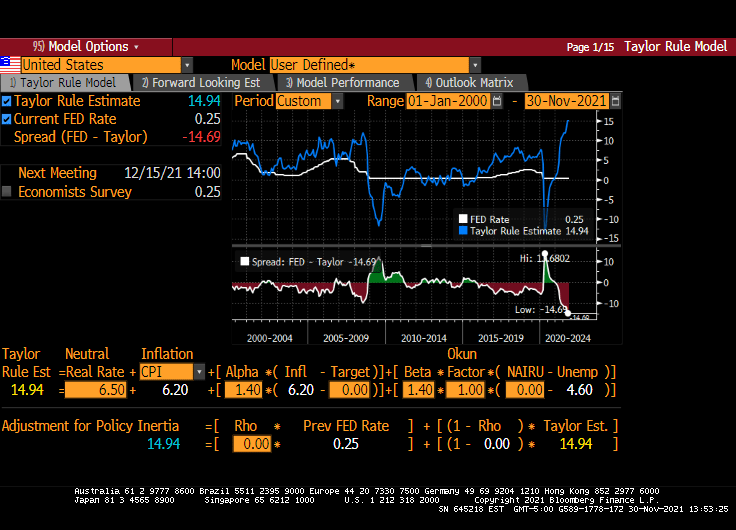

Of course, Powell could do what Volcker did (and the Taylor Rule suggests) and raise their target rate to 15% to cool inflation.

But does Powell and the other FOMC members have the moxie to really cool inflation? Frankly, no. Powell until yesterday played the TRANSITORY card and still believes that inflation will cool by 2022.

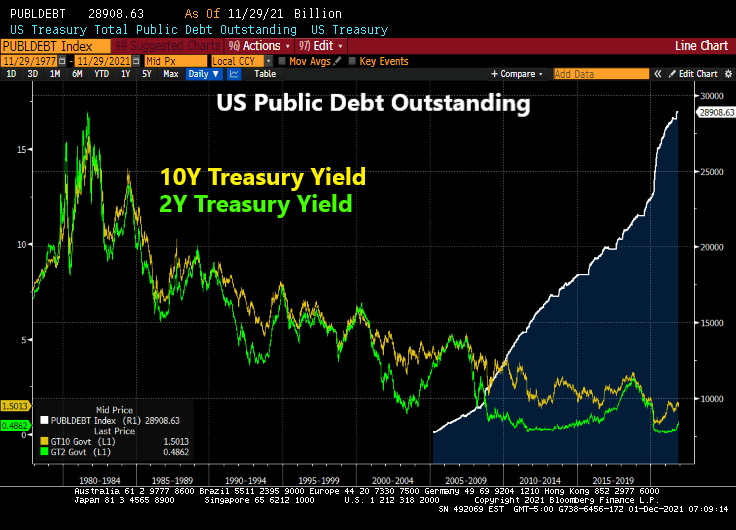

True, the Federal government has binged on borrowing (up 172% since January 2009). And with Biden and Congress trying to spend trillions more (much of which will be added to the public debt rolls, so increasing interest rates ala Volcker is very problematic.

And then there is always the good ‘ole excuse not to raise rates if needed. Other than admitting that The Fed is monetizing Federal government spending to which there is no end in sight.

Given Fauci’s alleged strong belief in “science” he could play Esqueleto in a remake of Nacho Libre.

You must be logged in to post a comment.