As I discussed yesterday, the Misey Index under Biden remains elevated compared to that of Trump pre-Covid despite massive financial stimulus from Green Man (The Federal Reserve under Jerome Powell).

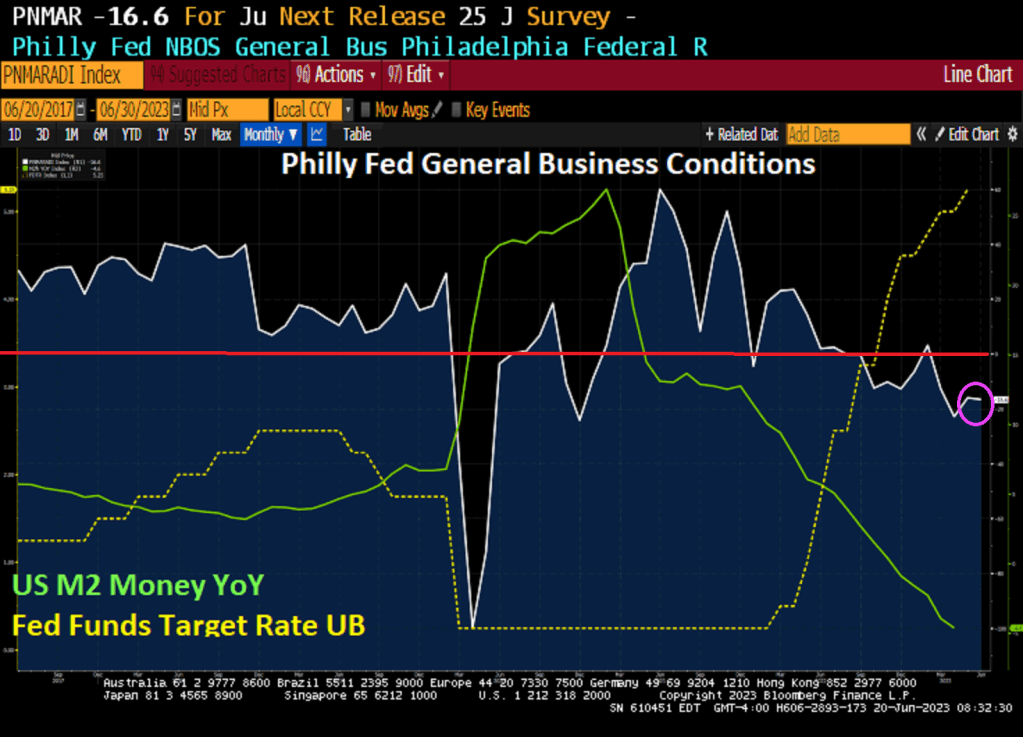

Now we have more evidence of an impending recession with the Philly Fed General Business Conditions index falling to -16.6 in June as Green Man (M2 Money growth) stalls.

Federal Reserve Chair Jerome Powell (aka, Green Man) will have an opportunity this week to clarify what many found a confusing message on the path of interest rates, with the added task of assuring Democrats and Republicans the economy is on track.

The Fed chief will face questions from lawmakers on Wednesday and Thursday, his first testimony on Capitol Hill since early March, before banking-sector turmoil prompted sharp criticism of the Fed and forced officials to rethink their policy strategy. Since then, the most acute financial strains have eased, but questions remain about the extent to which tighter credit will weigh on the economy, and what that means for the Fed.

Powell will need to reassure Republicans the Fed is not backing down from its campaign to contain price pressures, while pointing Democrats to the resilience of the economy as officials prepare to raise rates further this year.

“The Democrats are nervous because they would rather declare victory and move on,” said Stephen Myrow, a managing partner at Beacon Policy Advisors and a former George W. Bush Treasury official. “I think they’re going to try to caution this time against further increases. But Republicans are just going to hammer away and act like inflation hasn’t come down.”

Powell will be fresh off the Fed’s June 13-14 meeting, where he and his colleagues left rates unchanged for the first time in 15 months but signaled they may deliver two more hikes this year. Fed watchers and investors struggled to digest the message from Powell’s post-meeting press conference, and lawmakers last week said they planned to press him for an explanation.

“Right now there’s a lot of confusion about the next step,” Thom Tillis, a Republican senator from North Carolina, said Thursday.

Well, Senator Mel Tillis, there is no confusion. The DC Elites and Big Banks don’t want to disrupt the flow of money to the political donor class (including China and Ukraine payments to Biden’s family, now up to $30 million). The Fed may raise rates one more time and claim victory again their “War on Inflation!” then start cutting again as the Presidential election approaches.

Jerome Powell (aka, Green Man).

You must be logged in to post a comment.