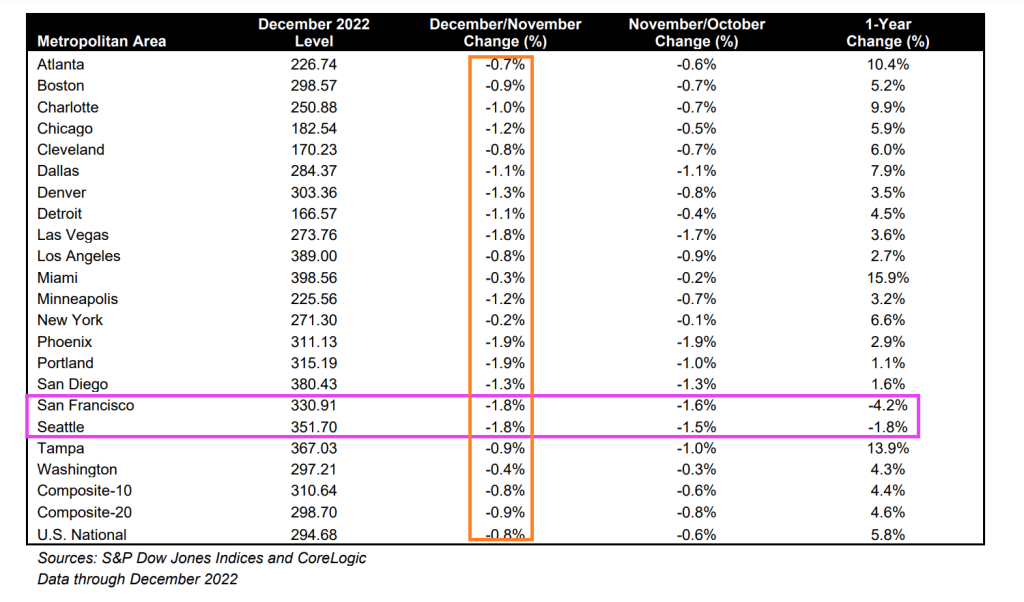

Only Seattle and San Francisco experienced negative growth in home prices on a year-over-year basis. All of the top twenty metro areas experience negative month-over-month price declines from November to December.

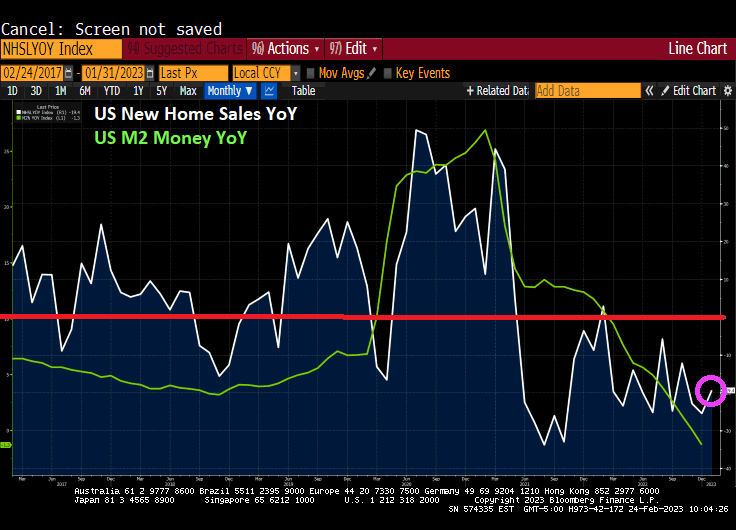

Another sign of a not healthy economy is housing. New Home Sales collapsed -19.4% from January 2022 (aka, year-over-year or YoY).

If I were Joe Biden, I would be touting the month-over-month numbers, up 7.20% from December to January. But the reality is that year-over-year new home sales are down -19.4%.

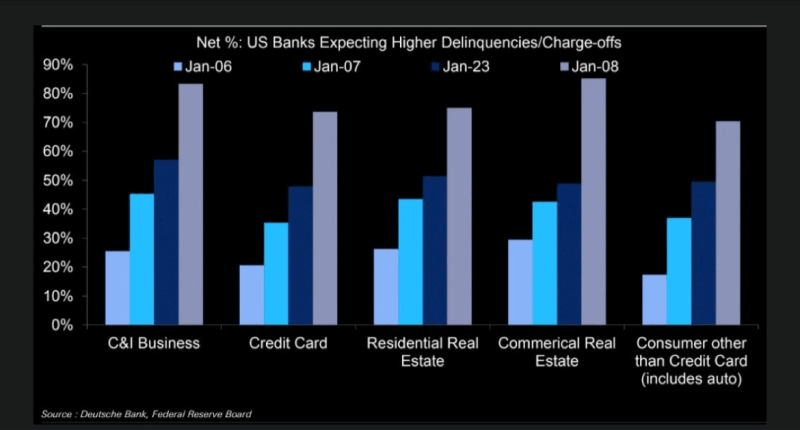

Also, on the “Alarm!” front, US banks are expecting higher delinquencies, including on residential mortgages.

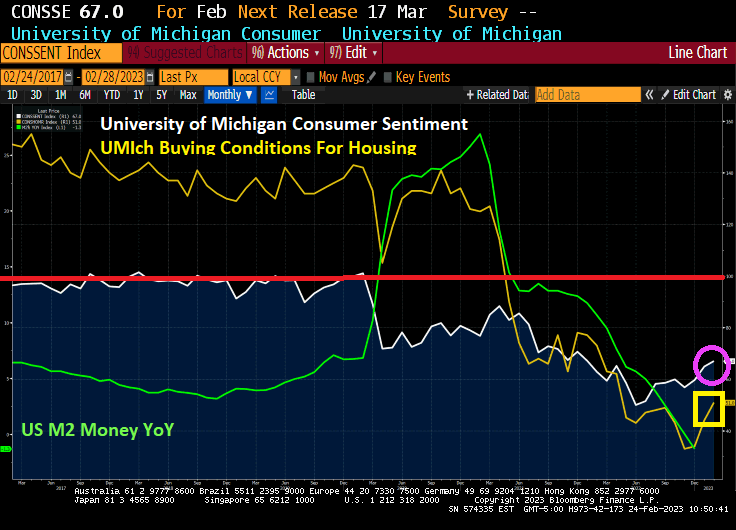

University of Michgan consumer sentiment for housing is rising, but still woefully below the 100 benchmark.

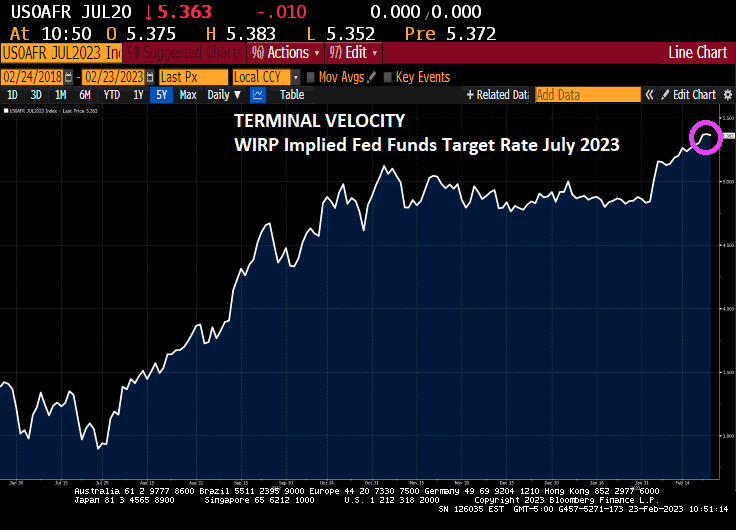

The terminal Fed Funds target rates is now 5.363% for the July FOMC (Fed Open Market Committee) meeting in 2023.

This comes as US Q4 GDP was revised lower on weaker consumer spending, revised downward to 1.4%

With the revision of Personal Consumption, real GDP was revised downward to 2.7% annualized QoQ.

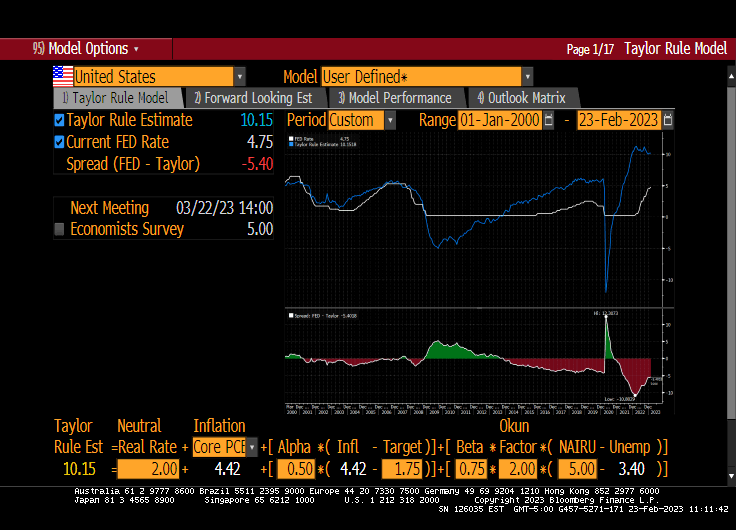

The Taylor Rule estimate for The Fed Funds Target rate is 10.15%. The Fed is only at 4.75%, so there is a long way to go! Except that The Fed doesn’t follow any useful rule like the Taylor Rule. Just the “seat of the pants” rule.

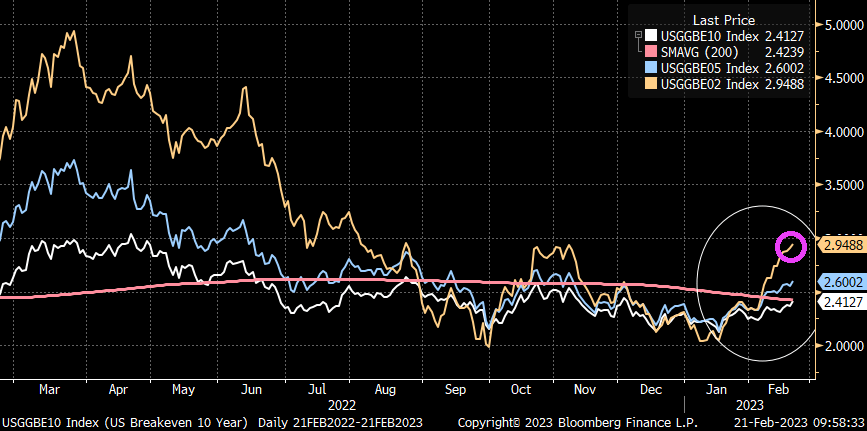

But before I go for experimental therapy for my brain tumor, I will leave you with this diddy. Inflation expectations are on the rise, not falling like Biden and Yellen keep screaming.

US inflation is causing The Federal Reserve to raise interest rates, and mortgage applications are suffering.

Mortgage applications decreased 7.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending February 10, 2023.

The Refinance Index decreased 13 percent from the previous week and was 76 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 6 percent from one week earlier. The unadjusted Purchase Index decreased 5 percent compared with the previous week and was 43 percent lower than the same week one year ago.

The MBA contract rate rose 3.4% from 6.18% to 6.39% as The Fed tightens.

And if you believe the Taylor Rule (as opposed to The Fed’s current politically-based decisions), The Fed’s target rate should be 10.15% and The Fed is less than half way there at 4.75%.

The Fed is expected (by investors in Fed Funds Futures) to rise to 5.283% by the July FOMC meeting, then decline to under 5% by January ’24.

Speaking of Fed rate hikes, January’s red hot retail sales (up 3% MoM) is surely going to drive inflation UP and The Fed will keep raising rates.

US REAL average hourly earnings fell … again … to -1.8% year-over-year (YoY) from a revised -1.6% YoY in Deember. That makes 22 straight months of negative hourly earning growth.

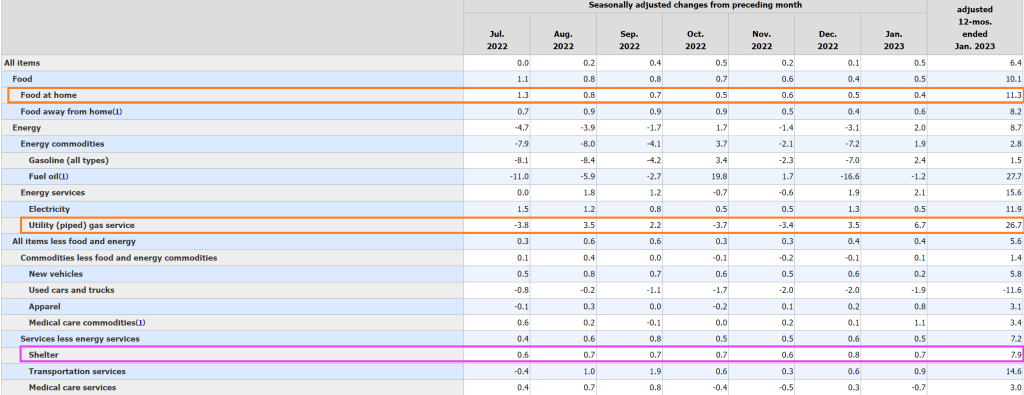

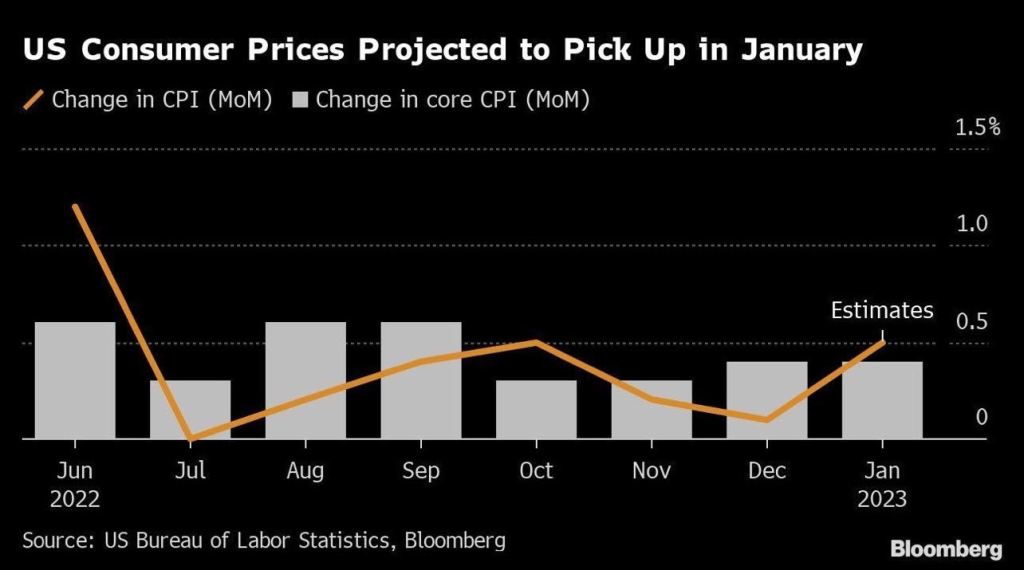

CPI Month-over-month (MoM) was revised upward for December, and increased from 0.1% in December to 0.5% in January. CORE CPI remained unchanged from the upward revision in December to 0.4% MoM.

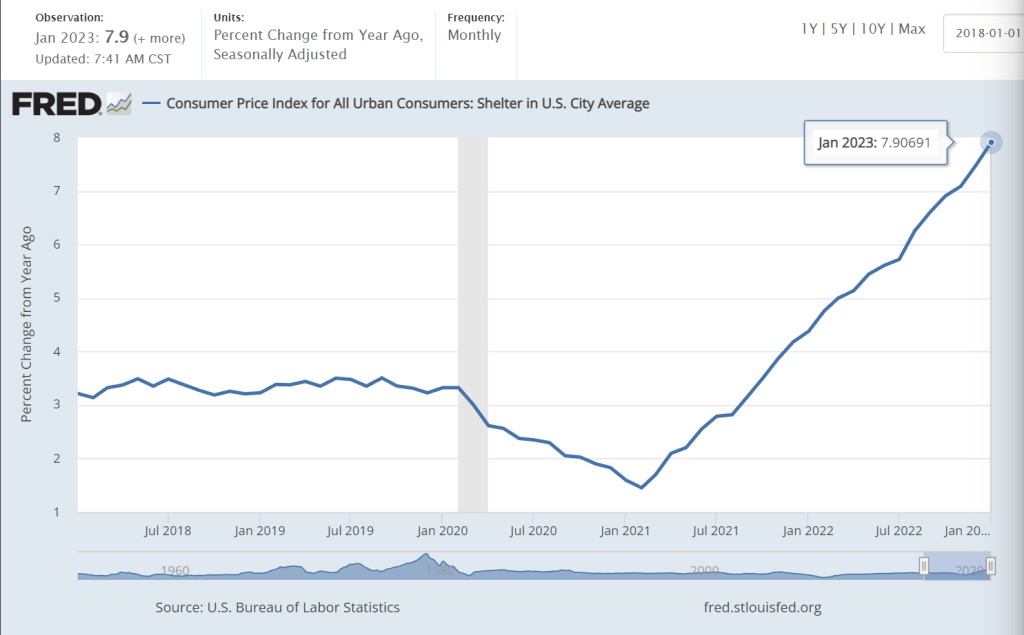

Components of inflation include FOOD AT HOME (up 11.3% YoY), utility (piped) gas service (up 26.7% YoY) and shelter (up 7.9% YoY). So, the middle-class inflation tax (food, heating, housing) remains high.

Do I detect a trend in shelter inflation??

Hey, I thought Treasury Secretary Janet Yellen said inflation was transitory. 22 straight months of negative hourly earnings growth seems more permanent than transitory.

While much of the US is down from 2022 peaks in home price. but it is The West where home prices are down the most (just like 2008 where the Inland Empire of California, Phoenix and Las Vegas crashed in term of home prices).

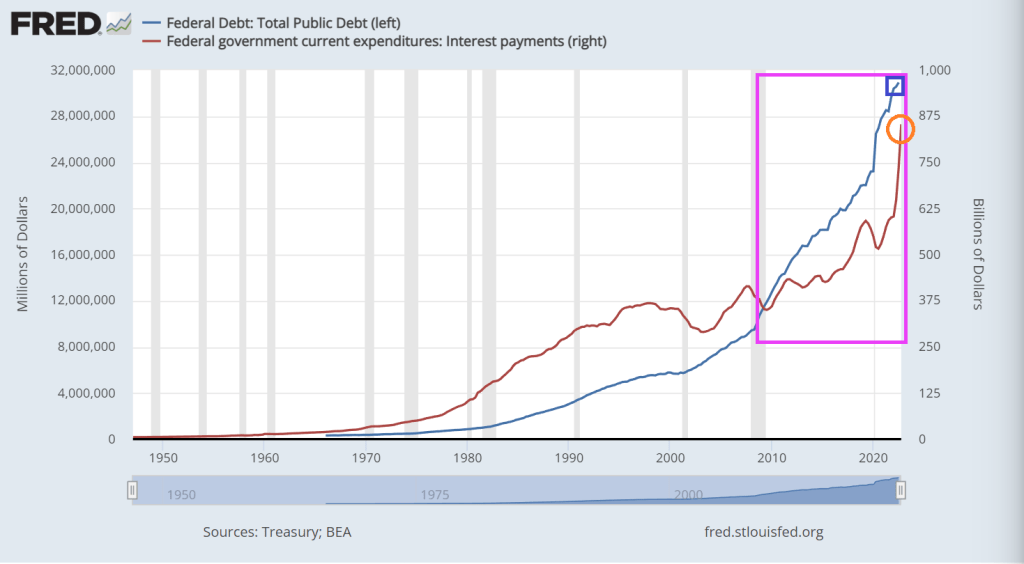

Nothing has been the same since Nancy Pelosi (CA-D) became Speaker of the House in January 2007. In fact, US public debt was at $8.68 trillion when she was handed the gavel and US public debt now sits at $31.55 trillion. That is a whopping 264% increase in the nation’s debt under free-spending SanFranNan. To Pelosi, there is no such thing as too much debt.

To be fair, Pelosi had plenty of help. We had Barack Obama and Joe Biden assume the Presidency in 2009 and in between we had RINOs (Republicans in name only) John Boenher and Paul Ryan as House speakers. In the Senate, the US has had Harry Reid (NV-D), Chuck Schumer (NY-D) and breifly Mitch McConnell (KY-R) as majority leaders. Of course, he had Donald Trump as President for 4 years then a return to the Obama-Biden Presidency with Old Joe as President for the past 2 years.

This chart show how deranged Congress and the Administration became since 2007. On October 3, 2008, President George W. Bush signed the $700 billion Emergency Economic Stabilization Act (EESA) of 2008 after Treasury Secretary Henry Paulson asked Congress to approve a bailout to buy mortgage-backed securities that were in danger of defaulting.

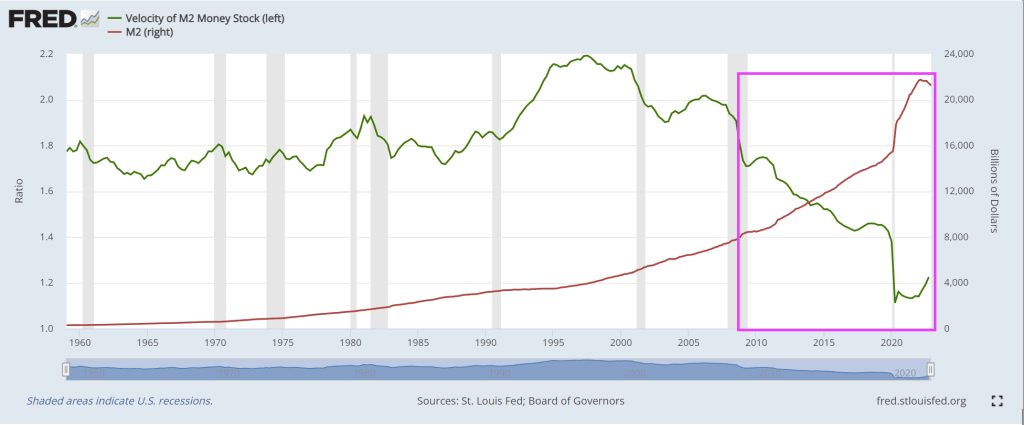

Since 2007, the US has expereienced a housing bubble burst and ensuing financial crisis (2008/2009), then a Covid economic shutdown in 2020 requiring (in the mind of Statists) massive Federal spending in the form of Covid Relief (aka, the American Rescue Plan) for $1.9 TRILLION, then Infrastructure Spending bill for $1 TRILLION, the Inflation Reduction Act (really a green energy spending bill dressed up as an inflation reduction measure) and the infamous pork-laden Omnibus bill. All this Federal spending has driven up M2 Money by 200% since Pelosi first became House speaker.

Look at the chart of M2 Money Velocity (GDP/M2 Money) since Pelosi became House Speaker. It has collapsed.

Pelosi is also notable for her “You have to pass the bill to see what’s in it” speech on the Affordable Care Act and childishly tearing up on camera a copy of Donald Trump’s State of the Union address.

Meanwhile, the US has $181.5 Trillion in UNFUNDED LIABILITIES that will require MORE debt to be issue. Social Security unfunded liability is now $22.46 trillion and Medicare unfunded liability is up to $35 trillion. But if you dare mention “reform” to these massive entitlement boondoggles, President Biden and Senate Majority Leader Chuck Schumer will say “Republicans want to take away your Social Security!” That isn’t what Rick Scott (FL-R) said.

Unfunded liabilities per citizen is now $542,457. I propose that all illegal immigrants crossing the Mexican border (or Canadian border) per forced to pay their share of unfunded liabilities as an entry fee..

While Congress debates cutting spending (Hint: Childish Biden and Schumer said no to any cuts to spending), the US Debt Star gets closer to completion.

Biden’s State of the Union address saw him bragging about his record job creation (actually, it was the private sector, not Biden than created jobs) and historic unemployment rate. What Biden didn’t mention (along with not discussing the porous Mexican border with fentanyl pouring across or why he failed to shoot down a Chinese spy balloon until after it has passed over numerous military reservation) is that the unemployment rate always hit a low point just prior to a recession.

So, here we sit at 3.4% unemployment. But we also see the US Treasury yield curves (10Y-3M and 10Y-2Y) remaining deeply inverted.

The US Treasury 10-year yield is up 5.5 basis points today.

And Bankrate’s 30-year mortgage survey rate is up slightly today.

You must be logged in to post a comment.