I don’t think this is a record that Biden can run on for re-election: 21 straight months of NEGATIVE REAL WAGE GRWOTH. Fortunately for Fed Chair Jay Powell, he is not an elected official.

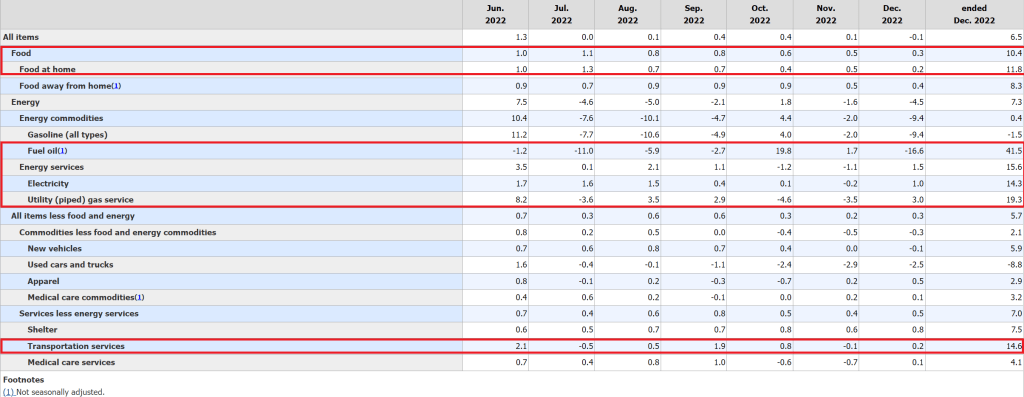

The December inflation report still shows elevated inflation in the US, but only -0.1% since November (MoM), but still high compared to last year (6.5% YoY). That is still over 3x The Fed’s target inflation rate of 2%.

While headline inflation fell to 0.1% MoM, CORE inflation (removing food and energy) rose again 0.3% MoM and 5.7% YoY.

What exactly went up in price in December? Food and energy were all over 10% YoY growth.

At 6.50% YoY headline inflation, the Taylor Rule suggests a Fed Funds Target rate of … 13.13%. Well, I guess that Powell will say there is more rate hikes to be done.

It is the start of a new year and, like clockwork, residential mortgage applications are rising (at least until May). But it is important to realize that purchase mortgage demand is down 44% from the same week last year (YoY). And refinancing mortgage applications are down 86% YoY.

Mortgage applications increased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 6, 2023.

The Refinance Index increased 5 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index increased 47 percent compared with the previous week and was 44 percent lower than the same week one year ago.

You can see the beginning of the new year in pink outline, purchase apps up 47% since the previous week (WoW). But you can see the general decline in both purchases and refinancing applications YoY as M2 Money growth stalls.

Talk about seasonality! If you want to feel optimistic about the mortgage market, just look at the first week of 2023. Declining mortgage rates are helping fuel short-term mortgage demand.

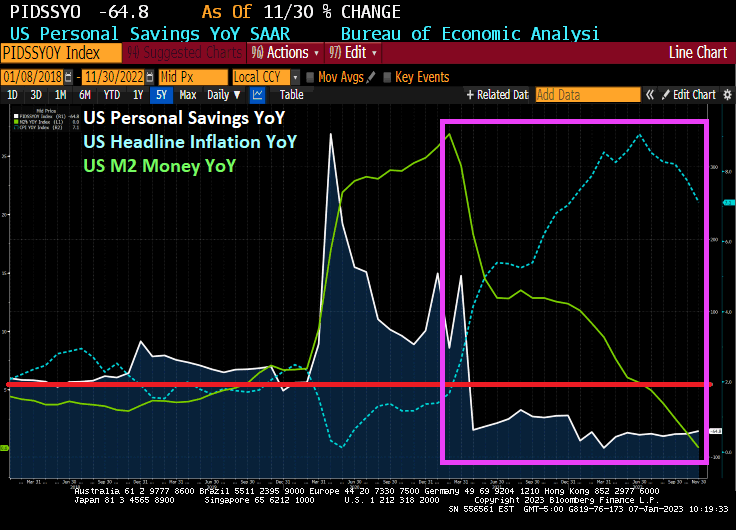

As we are painfully aware, inflation is still high at 7.1% Year-over-year (YoY). To cope with inflation, consumers have been gutting their savings and increasing their use of credit. In November, consumer credit increased 7.9% YoY while personal savings fell -64.8% YoY.

The good news? Inflation month-over-month is expected to be 0% tomorrow.

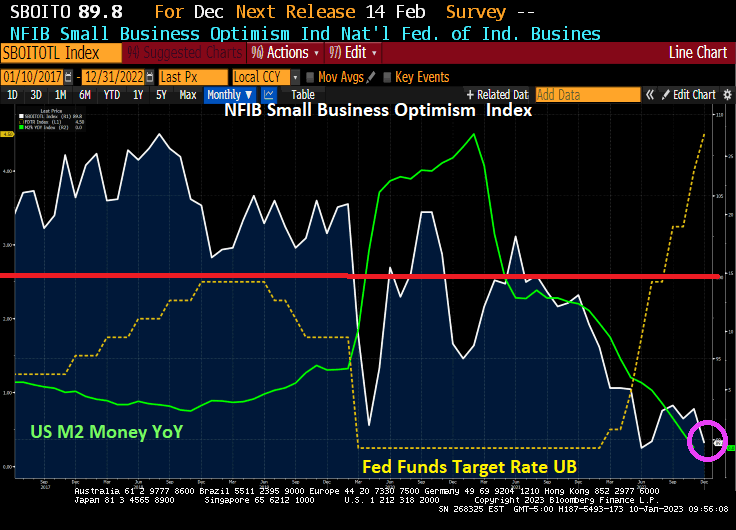

The NFIB Small Business Optimism Index is plunging and just fell below 90. The index was above 100 before the Wuhan virus outbreak in 2020, but has only been at 100 or above for only two months under Biden. And the trend is definitely looking bleak as The Federal Reserve fights inflation with M2 Money growth having collapsed to 0% YoY growth.

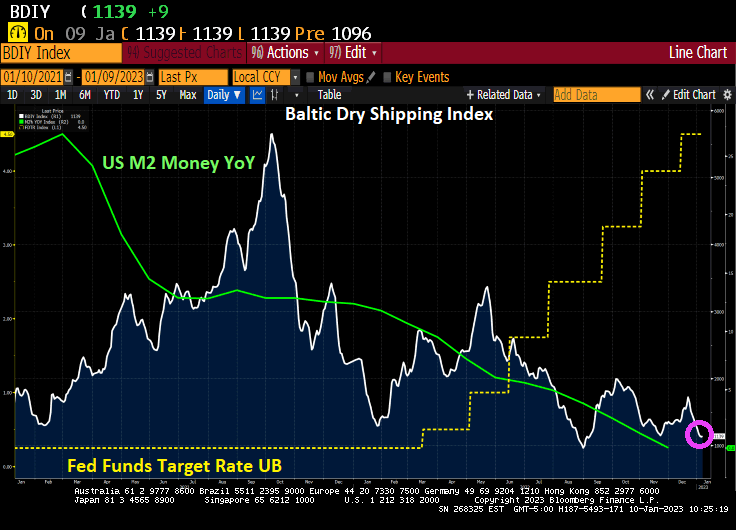

And the Baltic Dry shipping index is falling with M2 Money growth YoY.

I wonder what Fed Chair Jerome Powell is thinking?

The Federal Reserve will be the backstop of the Treasury market this year to alleviate dysfunction resulting from its increasing size and the retreat of regular buyers.

That’s the view of Credit Suisse Group AG analyst Zoltan Pozsar, who in a note to clients Friday predicted the Fed will restart asset purchases during the summer of 2023.

In Pozsar’s analysis, relative-value funds won’t buy Treasuries unless they cheapen a lot relative to overnight index swaps, and banks with sagging reserves are more likely to tap the funding markets than to buy Treasuries. FX-hedged buyers have been “priced out,” and geopolitical events have reduced large reserve managers’ appetite for US debt, he said.

Flagging demand from marginal buyers will depress demand for Treasury auctions, sparking selloffs in equities, credit and emerging markets, according to Pozsar.

“This is a ‘checkmate-like’ situation,” he wrote. “The Fed won’t be a pivot and the terminal rate may have to go higher still, neither of which augurs well for either risk assets or Treasuries.”

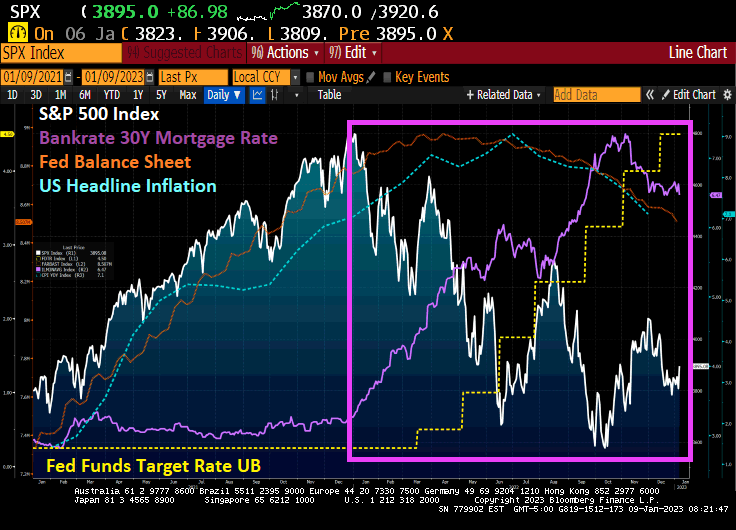

As The Fed started to raise rates (yellow line) to fight inflation (blue dashed line), the S&P 500 index started to fall. Note that The Fed’s balance sheet (purple line) is mirroring the inflation rate.

Fed Funds Futures point to Zoltan’s reversal in June 2023.

Will The Fed pivot? Zoltan says yes, the talking Fed heads say no.

US headline inflation began to soar as soon as Joe Biden became President. A combination of massive stimulus spending related to the Covid economic shutdown and his war on fossil fuels, driving up gasoline and diesel fuel prices. In other words, headline inflation rose from 1.4% Year-over-year (YoY) at the end of December 2020 to 9.1% YoY in June 2021. It has now simmered down to 7.1% YoY as The Fed continues to remove monetary stimulus.

How have consumers coped with inflation caused by massive Federal spending and Biden’s anti-fossil fuel policies? In November, personal savings dropped -64.8% YoY. This marks 20 straight months of declining personal savings.

US M2 Money growth YoY is now … 0%. That is the lowest in US history.

The December jobs report is out and the top-line number is … 223k jobs were added. That is strong enough to give The Federal Reserve the green light to raise rates.

But while it was a good jobs report, it shows the inflation tax in full view. Hourly wage growth year-over-year (YoY) was 4.6% in December. Unfortunately, the inflation tax was 7.1% in November. If we assume that the inflation rate in December is the same, the REAL hourly wage growth was -2.5% YoY.

But it is likely that headline inflation cooled a bit in December as The Fed continues tightening. But unless headline inflation cooled to 4.6% YoY, the inflation tax is positive and destructive.

The average weekly hours employed fell to 34.3 while U-3 unemployment rate fell.

Here are the rest of the numbers.

The most glaring data point is Full-Time Workers -1K; Part-Time Workers +679K.

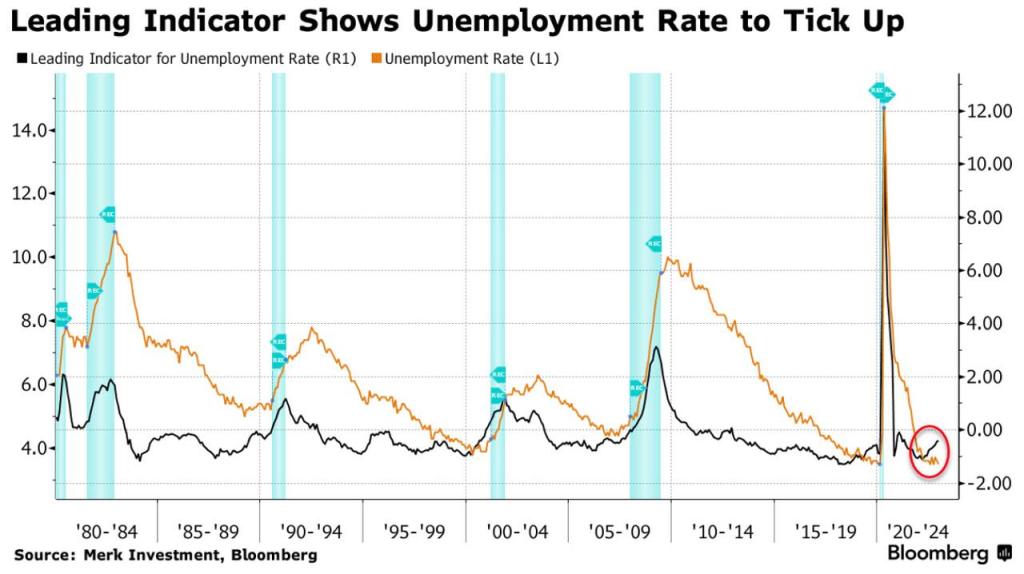

And the leading indicator for unemployment is ticking up.

Silvergate Capital Corp. shares plunged after the bank said the crypto industry’s meltdown triggered a run on deposits, prompting the company to sell assets at a steep loss and fire 40% of its staff.

Customers withdrew about $8.1 billion of digital-asset deposits from the bank during the fourth quarter, which forced it to sell securities and related derivatives at a loss of $718 million, according to a statement Thursday. Executives said on a conference call that Silvergate may become a takeover target.

“In response to the rapid changes in the digital asset industry during the fourth quarter, we took commensurate steps to ensure that we were maintaining cash liquidity in order to satisfy potential deposit outflows, and we currently maintain a cash position in excess of our digital asset related deposits,” Chief Executive Officer Alan Lane said in the statement.

The collapse of Sam Bankman-Fried’s FTX sparked a crisis for Silvergate, which held deposits for FTX units and Alameda Research, the trading firm at the heart of the crypto exchange’s downfall. Lawmakers are also scrutinizing the bank.

Silvergate plunged 44% to $12.34 at 9:48 a.m. in New York, the steepest decline since the La Jolla, California-based company went public in November 2019. The stock is down 91% in the past 12 months. Signature Bank, which said in December that it intended to shed as much as $10 billion deposits from digital-asset clients, fell 5.8% to $111.05.

Silvergate Capital Corporation operates as a bank holding company. The Company, through its subsidiary Silvergate Bank provides a banking platform for innovators, especially in the digital currency industry, and developing product and service solutions addressing the needs of entrepreneurs. Silvergate Capital serves customers in the United States.

Silvergate once saw the crypto industry as giving it a huge growth opportunity. Over the course of a decade, it transformed itself from a firm catering to small businesses into a publicly traded company known for providing banking services to major crypto clients such as Coinbase Global Inc. and Gemini Trust Co. — as well as FTX and Alameda Research.

At least Solana is on the rise.

Sam Bankman-Fried will go down in history as commiting one of the greatest financial frauds in world history. Why did he have four meetings with Biden’s top staffers prior to FTX’s crash and burn?

And with it, ISM Manufacturing Report for December is showing weakness. New orders (orange line) is down to 45.2 (below 50 is contraction) and the prices paid is down to 39.4 (white line). All this is happening as The Fed raises its target rate (yellow line) and removes monetary stimulus (green line).

This gives us “The Devil’s Tower” looking economic spike after massive Covid-related monetary stimulus and Federal government repeated stimulus.

Speaking of Already Gone, look at the US Treasury 10Y-2Y yield curve with slowing M2 Money growth. Yield curve inversion is more about vanishing M2 Money growth than it is a forecast of recession.

Mortgage applications generally nosedive in the last two weeks of the year (seasonality effect), but Federal Reserce monetary tightening to fight inflation is making the last two weeks worse than usual.

Mortgage applications decreased 13.2 percent from two weeks earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending December 30, 2022. The results include adjustments to account for the holidays. It marked the lowest mortgage applications since 1996.

The Market Composite Index, a measure of mortgage loan application volume, decreased 13.2 percent on a seasonally adjusted basis from two weeks earlier. On an unadjusted basis, the Index decreased 39.4 percent compared with the two weeks ago. The holiday adjusted Refinance Index decreased 16.3 percent from the two weeks ago (2WoW) and was 87 percent lower than the same week one year ago (YoY). The seasonally adjusted Purchase Index decreased 12.2 percent from two weeks earlier. The unadjusted Purchase Index decreased 38.5 percent compared with the two weeks ago and was 42 percent lower than the same week one year ago.

Notice that purchase applications are declining with slowing M2 Money growth showing the impact of The Fed trying to remove the punchbowl.

The week-over-week (or WoW) numbers are pretty bad.

You must be logged in to post a comment.