19 nations now have inverted 10yr-2yr yield curves.

And housing inventory for sale growth is soaring out West and in Tennessee?

At least Ohio is seeing a modest increase in housing inventory for sale.

On a parting note (before I watch the Ohio State Buckeyes annihilate the Rutgers Scarlet Knights tomorrow at 3pm EST, reverse repos parked overnight at The Fed just hit an all-time high. Apparently, banks don’t believe Janet Yellen’s inflation is transitory mumbo-jumbo.

The scalding inflation rate crippling middle class Americans and low-wage workers is causing The Federal Reserve to take action by finally tightening their monetary policy.

As such we are seeing a rapid decline in the US housing market in terms of sales. For August, pending home sales declined -22.5% YoY as expectations of further Fed rate hikes (blue line) soars. Note that impact of The Fed’s and Federal government “sugar rush” after the Covid outbreak in early 2020 and its impact on pending home sales.

Speaking of a sugar crash, risk parity ETF is down 32% from high.

The culprit? The Federal Reserve’s Panzer onslaught! With its leader, Heinz Wilhelm Guderian Jerome Powell.

The Dow is up 500 points today on the expectation that The Fed will stop tightening in the face of global chaos.

As UK 10yr yields fall -50 BPS!! And US T-10 yield drop -20.8 basis points.

Here is a photo of The Federal Reserve attacking American consumers to reduce inflation caused by Biden’s green energy policies and insane spending by Biden/Pelosi/Schumer.

Will Janet Yellen and Jerome Powell be awarded Panzer assault medals for 1) leaving monetary stimulus too large for too long then 2) suddenly tightening stimulus?

Well, The Federal Reserve is doing what they wanted … crushing the housing market as they fight inflation.

Today we get our first glimpse of the carnage in the housing market from August. With mortgage rates having soared and homebuilder sentiment tumbling (and permits plunging), it should be no surprise that existing home sales were expected to fall for the 7th straight month (-2.3% MoM vs -5.9% MoM in July).

Somewhat surprisingly, existing home sales ‘only’ fell 0.4% MoM in August (from a revised 5.7% MoM drop in July), but that is still 7 consecutive drops. This left existing home sales down 19.87% YoY.

Look at existing home sales YoY as M2 Money Yoy crashes.

Median prices YoY for existing home sales plunged to 7.63% while inventory for sale (yellow line) remains depressed.

As people are painfully aware, The Federal Reserve is on a mission … to hike interest rates to tame inflation back to 2%.

So, we saw a small surge in mortgage applications last week as the expectations of Fed rate hikes sinks in and households try to lock in mortgage rates.

Mortgage applications increased 3.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 16, 2022. Last week’s results include an adjustment for the Labor Day holiday.

The Refinance Index increased 10 percent from the previous week and was 83 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 1 percent from one week earlier. The unadjusted Purchase Index increased 11 percent compared with the previous week and was30 percent lower than the same week one year ago.

At least the percentage of ARMs remained the same, 9.1%.

By the way, the theme song for the US version of the TV show “The Office” was written by Jay Ferguson, the primary singer for the ’60s band Spirit (that performed “I’ve Got A Line On You!”).

Today will be another Fed rate hike, expected to be a whopping 75 basis points. The S&P 500 tends to rally (green line) after the FOMC announcement. What will happen today?

Even Obama’s economic advisor, Larry Summers, is wondering why Biden won’t allow pipelines to be build to reduce energy prices and reduce inflation.

Having said that, US mortgage rates are now the highest since 2008 and continue to rise with the expectation of more Fed rate hikes this year. Even core inflation is on the rise motivating The Fed to do more tightening since they aren’t receiving any help from Biden on energy or Congress in terms of massive spending of our money.

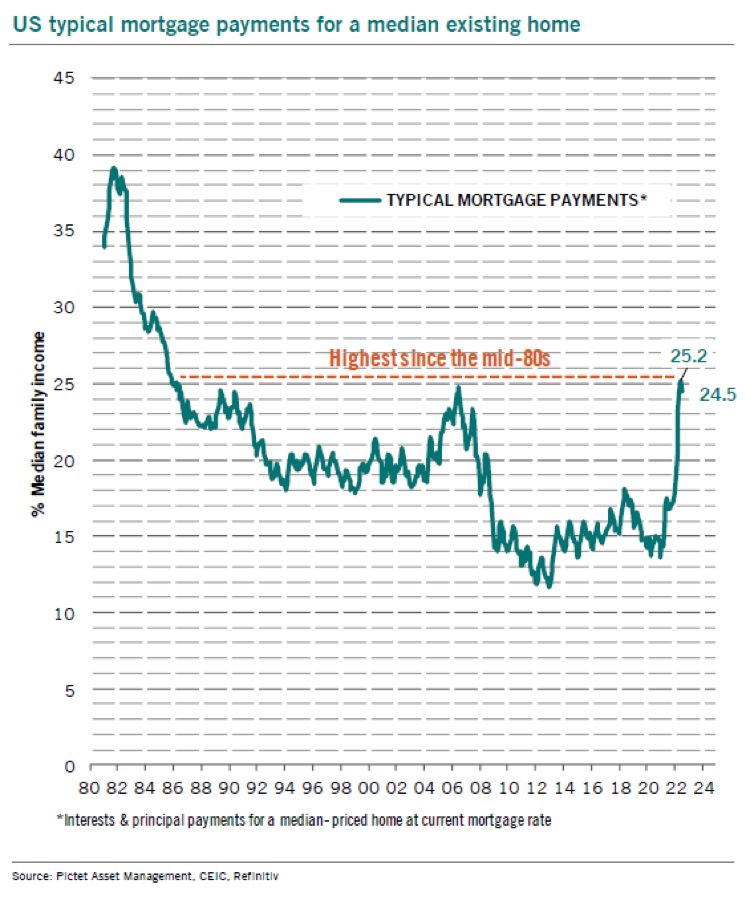

Mortgage payments for a median existing home in the US is back to the mid-1980s.

Data from Fed Funds futures implies that The Fed will raise their target rate to 4.50% by March 2023, then slowly lower rates.

Futures are down with the prospect of a 75 basis point bump in rates tomorrow. The Dow Jone Mini is down -167 points.

The National Association of Home Builders market index fell more than expected in September to 46, the lowest reading since 2012 (if I exclude the Covid economic shutdown).

Note that the NAHB market index is declining along with at the increase in the 30yr mortgage rate.

Inflation is stubborn because “goin’ green!” by 1) restricting US fossil fuel production and exploration and 2) Biden/Congress endless spending splurge since Covid. So, The Federal Reserve has a tough problem: cooling inflation while US energy prices are up 54% under Biden. And those higher energy prices have percolated through the entire economy in terms of food prices and heating prices.

Where do we sit? The US Treasury 10yr-2yr yield curve remains inverted (a sign of impending recession). Mortgage rates are the highest in 14 years as The Fed tightens.

If we look at Fed Funds Futures data, we can see that traders expect The Fed’s target rate to rise to 4.395% by March 2023’s FOMC meeting. Then traders expect The Fed to take their enormous foot off the tightening pedal.

Yes, inflation is crushing the middle class and low-wage workers. Average hourly earnings YoY after we subtract inflation are negative.

Taylor Rule? Currently, the Taylor Rule based on Core inflation of 4.56% YoY suggests a Fed target rate of 9.14%. Since traders anticipate the target rate to peak at 4.395%, The Fed will almost be halfway towards cooling inflation.

The problem is … Fed Chair Powell and Treasury Secretary Yellen don’t like rules limiting their “power.” Powell and Yellen think the Taylor Rule is a New Jersey ham product.

As inflation rages thanks to Biden’s energy policies and insane Federal spending, The Federal Reserve is trying to cool inflation (or Bidenflation).

As The Fed tightens, the 30-year mortgage rate has risen to 14 year highs. And home prices are still hot, hot, hot (though slowing). But consumer sentiment for housing remains in the doldrums (UMich Buying Conditions For Houses).

The good news? Atlanta Fed’s GDPNow real-time GDP tracker shows the US economy at positive growth of 0.521%. Ok, that is kind of lousy given the massive Fed stimulus and Federal spending since Covid.

M2 money velocity demonstrates the lousy return of Fed/Federal government “investment”.Near the lowest level in US history.

So, The Fed will have to destroy the US economy to save us from Bidenflation (bad energy policies and out-of-control Federal spending).

And more good news! The NASDAQ composite index is down only -1% today!

US mortgage applications dropped to the lowest level since 1997. I wonder if President Biden will invite boring crooner James Taylor back to the White House to sing about the collapsing mortgage market? Perhaps he can sing “Shower The People” and change the lyrics to “Shower ON The People.”

Mortgage applications decreased 1.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending September 9, 2022. This week’s results include an adjustment for the observance of Labor Day. The Refinance Index decreased 4 percent from the previous week and was 83 percent lower than the same week one year ago. The seasonally adjusted Purchase Index increased 0.2 percent from one week earlier. The unadjusted Purchase Index decreased 12 percent compared with the previous week and was 29 percent lower than the same week one year ago.

The Bankrate 30-year mortgage rate is now at the highest level since 2008 at the advent of Fed’s QE.

As The Fed takes away the massive monetary punch bowl, mortgage rates have risen to the highest since November 2008. And with the withdrawal of monetary stimulus (raising Fed Target Rate), mortgage purchase applications have declined.

Here is a photo of The Federal Reserve fighting the housing and mortgage market.

You must be logged in to post a comment.