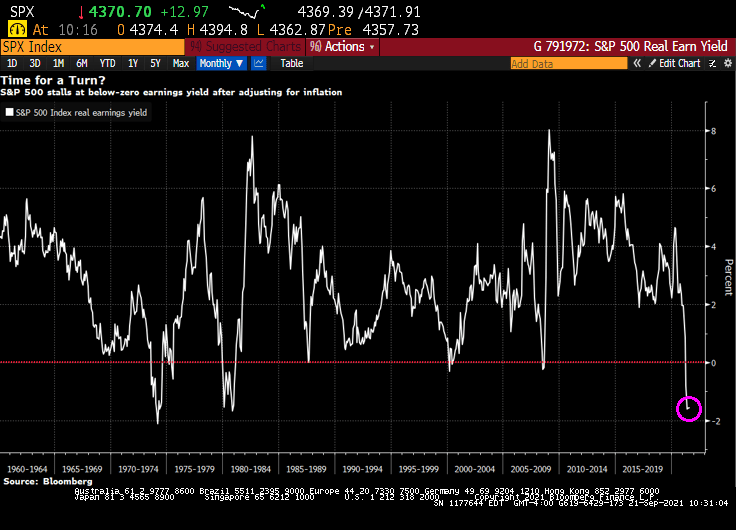

The stock market mildly rebounded from yesterday’s mild correction, but a glaring problem remains: S&P 500 real earning yields are negative.

With all the Federal government fiscal stimulus and Federal Reserve monetary stimulus, we are seeing inflation and that inflation is eating away at S&P 500 earnings yield.

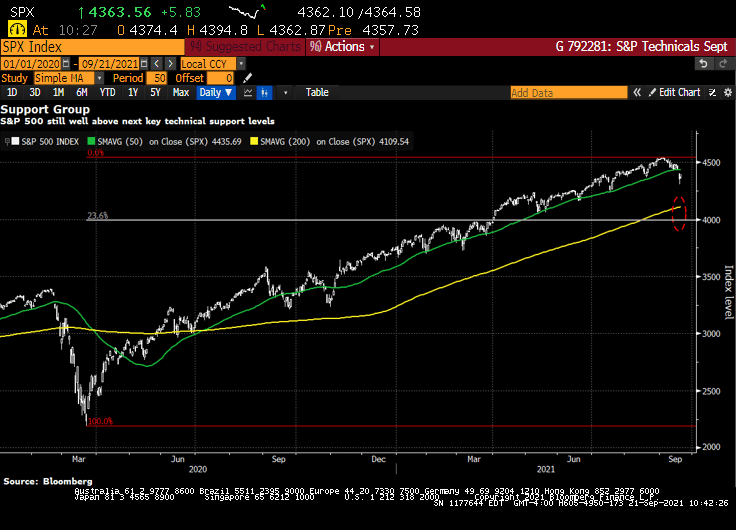

The S&P 500 is still well above key technical support levels.

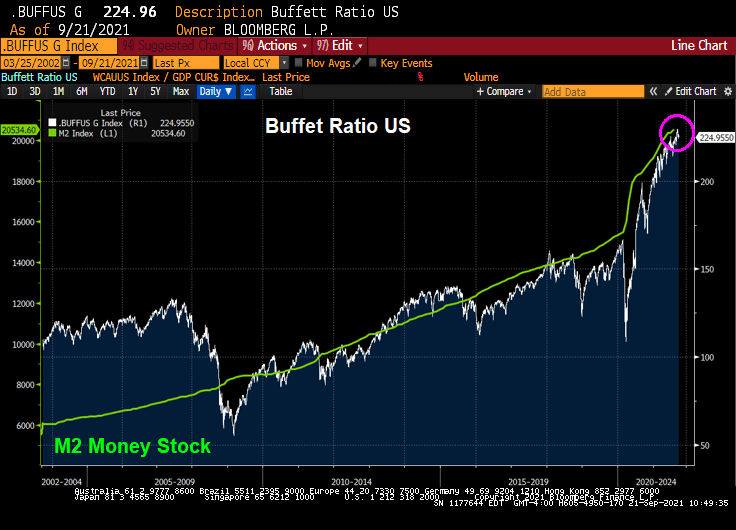

However, the Buffet ratio is raging along with Fed stimulus.

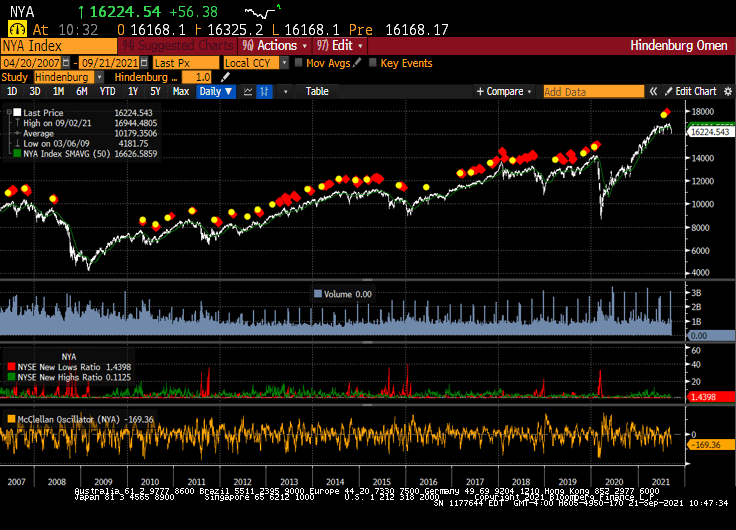

And the Hindenburg Omen is flashing RED!

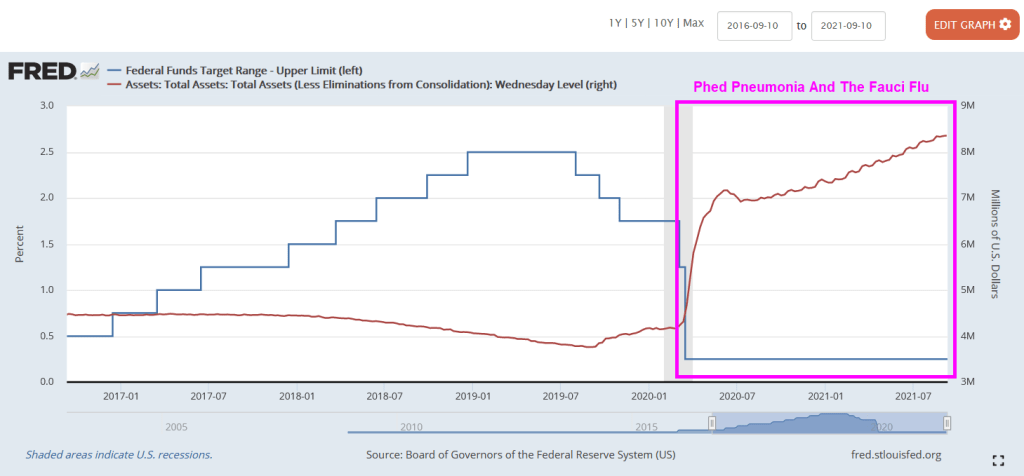

The mystery of the Flying Fed is whether they will withdraw their massive monetary stimulus or not.

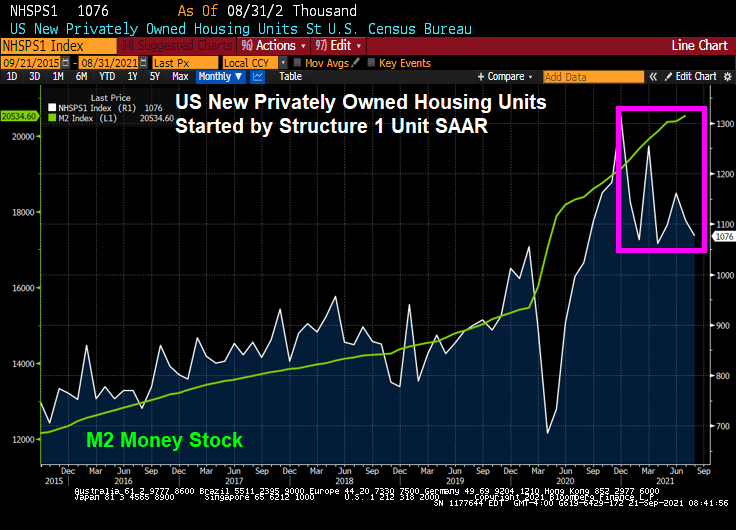

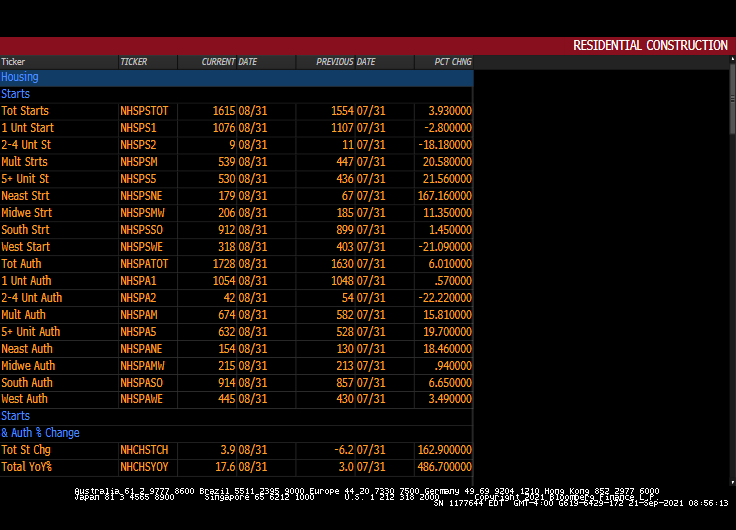

The unorthodox monetary stimulus from The Federal Reserve and stimulypto-level spending by the Federal government has resulted in a surge in US housing starts. But that thrill may be gone if the stimulypto is removed.

(Bloomberg) -By Olivia Rockeman- U.S. housing starts rose by more than expected in August, suggesting that the supply and labor constraints that have been holding back construction eased in the month.

Residential starts rose 3.9% last month to a 1.62 million annualized rate after an upwardly revised July print, according to government data released Tuesday. The median estimate in a Bloomberg survey called for a 1.55 million pace.

Building permits, meanwhile, increased 6% in August, the biggest gain since January, reflecting a sizable jump in multi-family units. Permit applications for single-family homes also edged higher.

The data suggest that builders are making some construction headway despite limited availability of land, labor and materials, which has slowed residential starts from a 15-year high in March. Despite the bottlenecks, housing starts remain mostly above pre-pandemic levels, which is expected keep construction activity elevated for some time.

1-unit (single family detached) starts got a tremendous jolt from The Fed’s monetary stimulus and Federal governments fiscal stimulus. But government stimulus wears out.

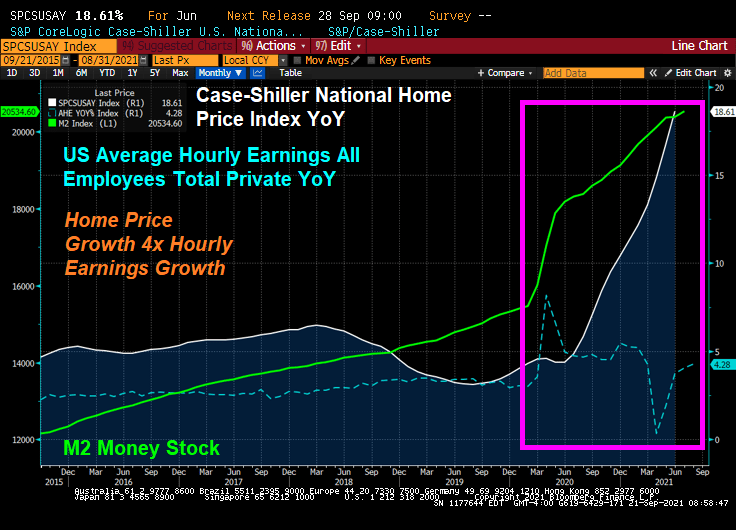

Given the high cost of housing in the USA, particularly in coastal metro areas, we see home price growth raging at over 4 times hourly earnings growth.

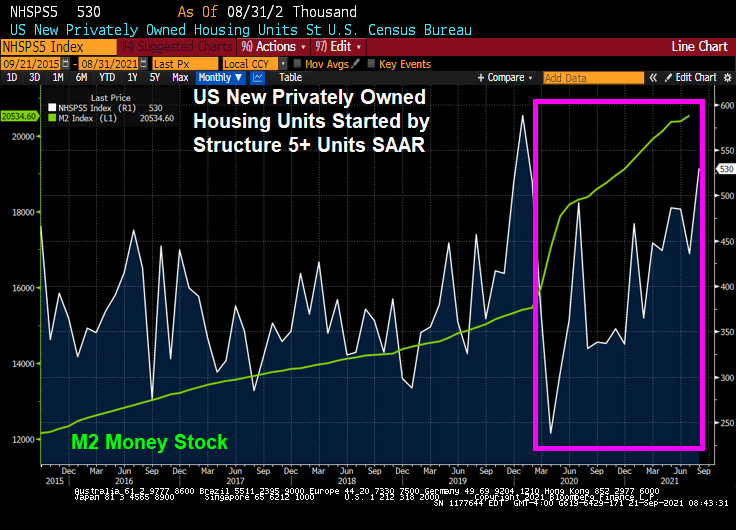

As a result, we are seeing a burst of 5+ unit (multifamily) housing starts. Note the burst of 5+ housing starts prior to Covid striking in early 2020.

Permits for 1-unit housing are up only slightly but 5+ unit permits are up 19.7%.

Remember, the withdrawal of fiscal stimulus will lead to a big fiscal cliff.

(Bloomberg) — The S&P 500 Index extended its decline past 2% Monday afternoon amid growing investor jitters about China’s real estate crackdown potentially sparking a financial contagion. And the Hang Seng fell 3.30% overnight.

The benchmark gauge was down 2.1% as of 12:08 p.m. in New York. All of the 11 major industry groups declined, with the energy, financials and materials sectors leading the losses. The tech-heavy Nasdaq 100 index slumped 2.4%, while the blue-chip Dow Jones Industrial Average retreated 1.9%.

By 2:33pm, the Dow is down 2.55%, NASDAQ down 3.15%.

Volatility also soared, with the Cboe Volatility Index — often called Wall Street’s “fear index” — jumping as much as 29% to 26.75, the highest level in over four months.

“While the Evergrande situation is front and center, the reality is, stock market valuations are overstretched and the market has enjoyed too long of a break from volatility and Monday’s stock market declines are not surprising,” said David Bahnsen, chief investment officer at the Bahnsen Group, a wealth management firm.

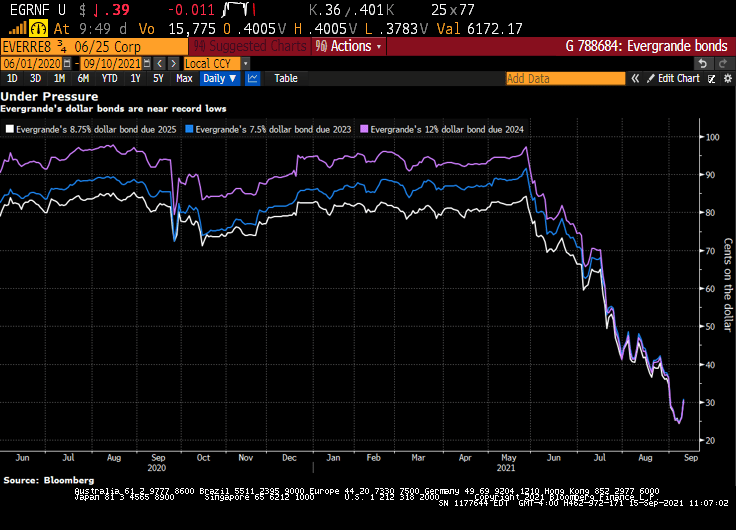

As Evergrande bonds continue to tank.

Meanwhile, most commodity prices are falling … except for UK Natural Gas Futures which are up 16.5%!

Kind of a drag … when Federal government stimulus fades just as The Fed tries to decide on slowing its balance sheet expansion.

(Bloomberg) — In the coming Year of the Taper, it’s the fiscal version that will really bite.

The chatter in U.S. financial markets is all about the Federal Reserve’s yet-to-be-announced reduction of its bond purchases. That’s obscuring something important: the already-under-way cutback of the federal government’s budgetary support — which is likely to have a much bigger impact on economic growth next year.

The U.S. expansion looks set to slow sharply in the second half of 2022 as measures that propped up the economy during the pandemic — from stimulus checks for households to no-cost financing for small companies — fade from view.

That will be the case even if President Joe Biden manages to win Congressional approval for the bulk of his $3.5 trillion Build Back Better agenda. The spending will stretch over years, with limited impact in 2022. It will also be at least partly paid for by tax increases that slow the economy down rather than speed it up.

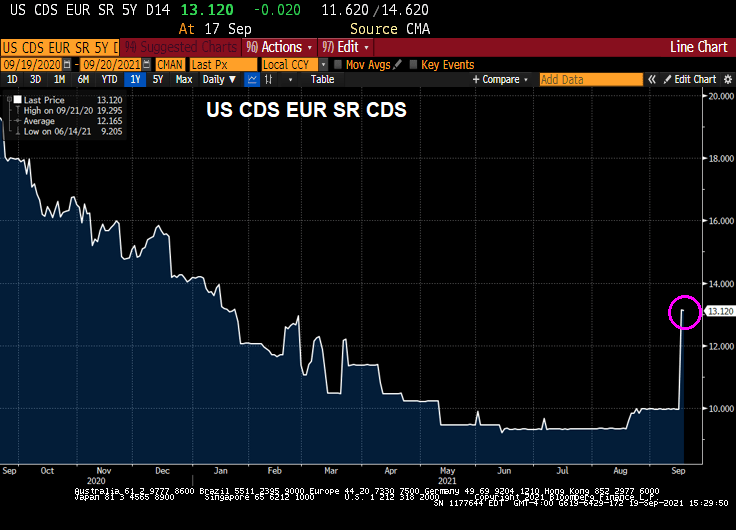

And then the is Treasury Secretary Janet Yellen renewing her call for Congress to raise or suspend the U.S. debt ceiling, saying the government will otherwise run out of money to pay its bills sometime in October.

We can see the CDS market reacting … slightly … to Yellen’s concerns.

But next to Argentina’s CDS, the US looks positively tame.

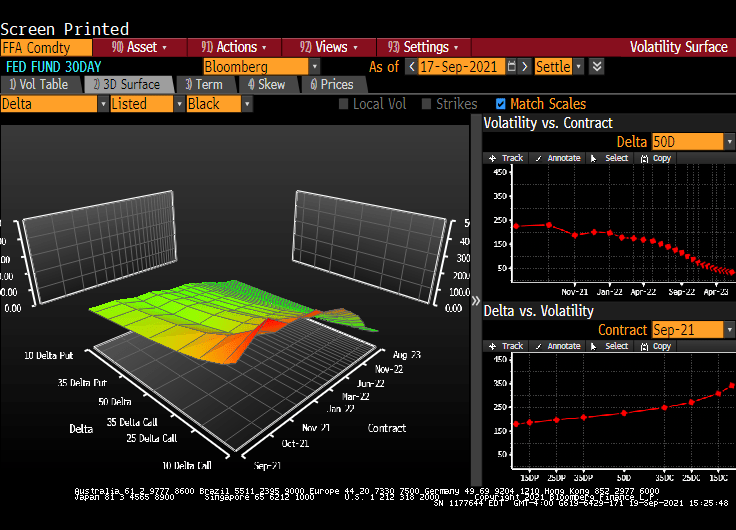

And there is a little disturbance in the Fed Funds Futures volatility.

Then we have the volatility cube showing The Fed’s rate suppression at the short end and expected volatility in the future.

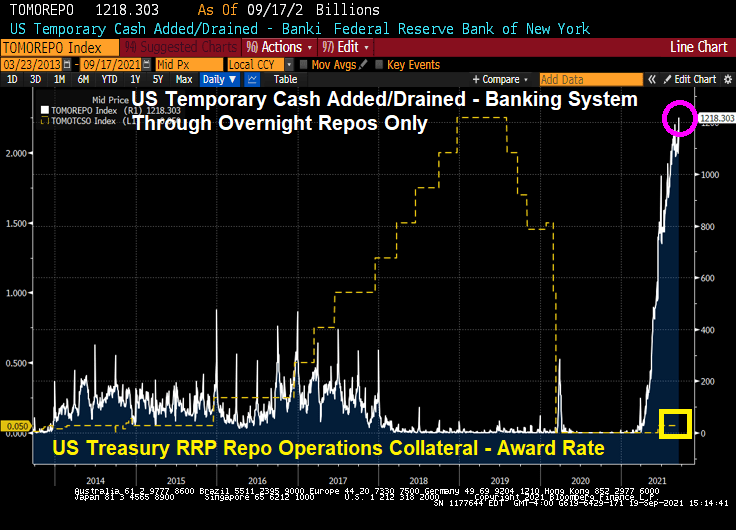

And there we have The Fed’s temporary repo facility hitting an all-time high.

The next Federal Reserve Open Market Committee (FOMC) meeting is next week with an announcement on Wednesday, September 22nd.

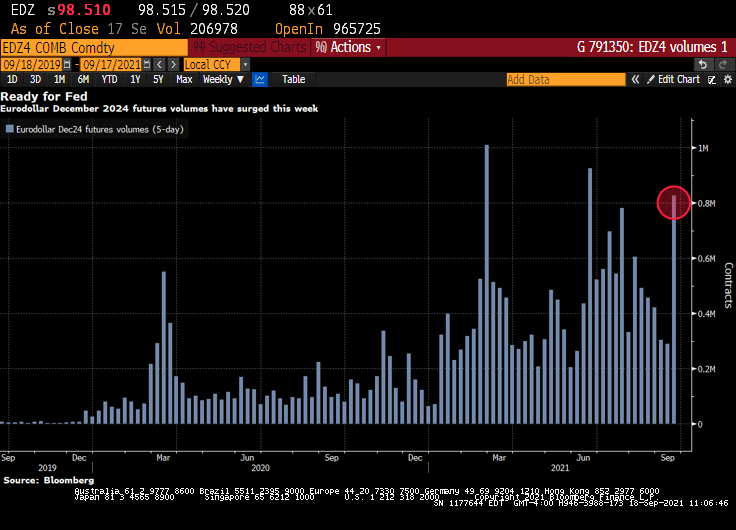

(Bloomberg) — Volume in the December 2024 eurodollar futures contract has surged Friday, approaching 200k, highest in the strip. Weekly volume exceeds 800k ahead of next week’s FOMC meeting. The December 2024 contract is a proxy for the Fed’s taper timeline, similar to the belly of the Treasuries curve (aka, the belly of the beast).

As of 2:30pm ET, nearly 197k Dec24 eurodollar contracts had traded, bringing weekly total to 816k, third most in its lifetime; notable flows on the day have included three block trades for 5k each:

The contract also appeared in curve trades including 9.3k Sep24/Dec24 3-month, 18.9k Dec23/Dec24 12-month and 24.8k Dec22/Dec24 24-month

The Dec22/Dec24 eurodollar spread has been in the spotlight since Morgan Stanley recommended the steepener in June as a way to exploit the disconnect between expectations for the pace and timing of Fed rate increases

As of today, we see a kink in the US Dollar Swaps curve at 21m.

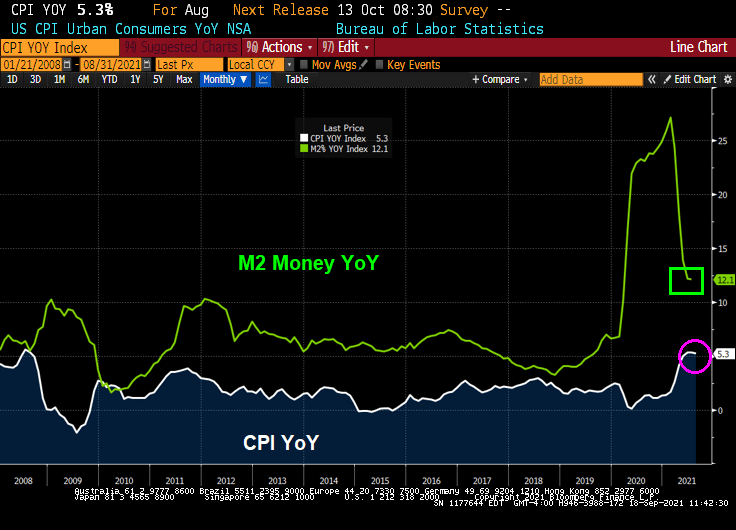

With inflation the highest since 2008, and M2 Money still growing at 12.1% YoY, it is time for The Fed to take it foot off the accelerator pedal.

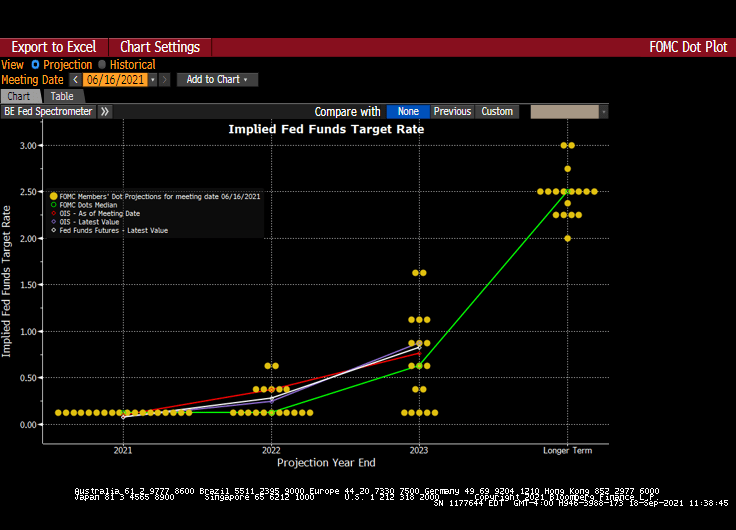

The Fed’s Dots Plot as of the last FOMC meeting indicates a willingness to let the Fed Funds Target rate start rising again after over a decade of rate suppression.

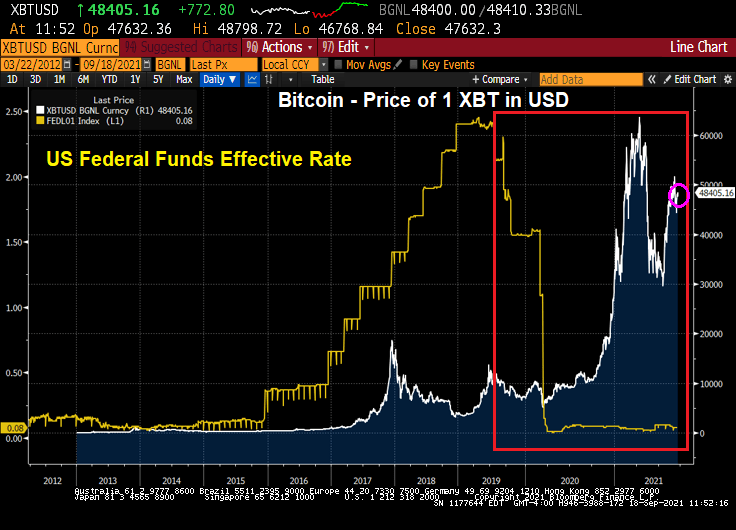

Given the fear of The Fed tapering (eventually), is it any wonders alternative investments such as Bitcoin have risen as The Fed cut rates?

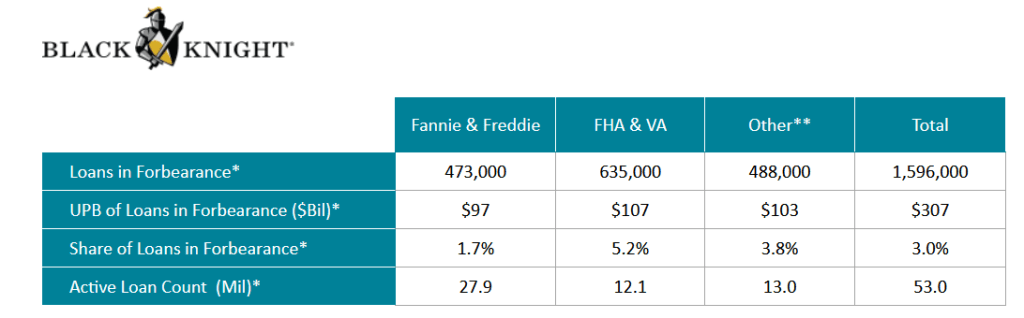

The Covid epidemic hit the single-family mortgage market hard in early 2020, leading mortgage lenders and servicers to offer FORBEARANCE to borrowers who were having trouble making their mortgage payments due to loss of hours or a loss of job.

The good news? Active forbearance plans are much lower today than at their peak after the Covid epidemic struck in early 2020 with active forbearance plans peaking in May 2020.

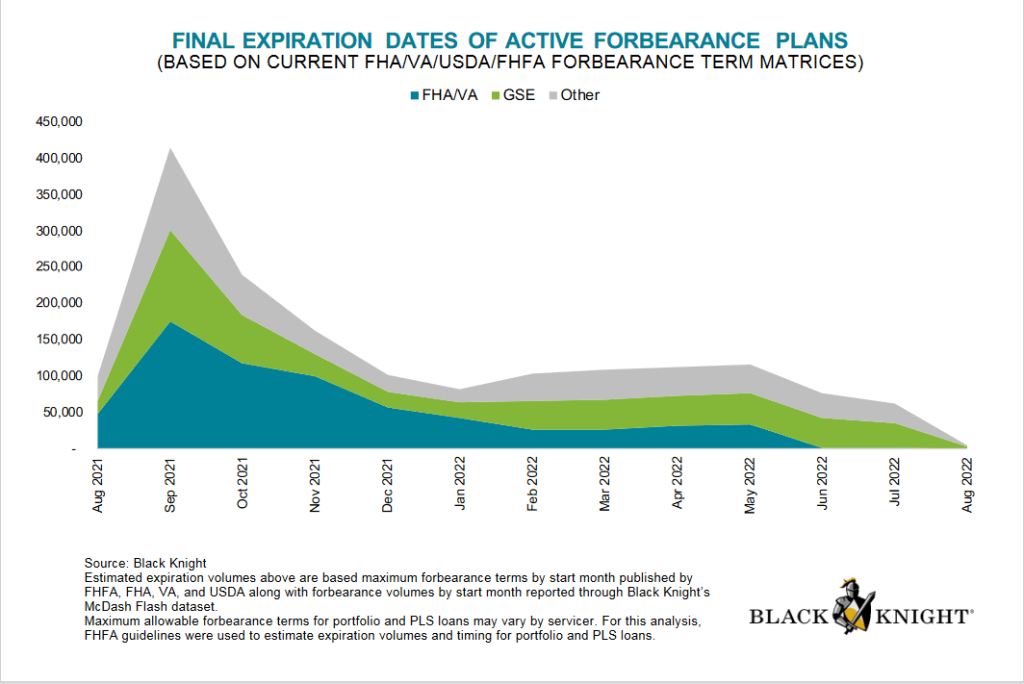

Forbearance plans are due to expire in

What is forbearance, you ask? Forbearance is when a mortgage servicer or lender allows a borrower to temporarily pay their mortgage at a lower payment or pause paying your mortgage. The borrower will have to pay the payment reduction or the paused payments back later.

Despite forbearance, Fannie Mae still reported $7.2 billion in net income in Q2 2021. Notice the difference between single-family SDQ and the SDQ rate without forbearance. Freddie Mac reported $3.7 billion in Q2 2021 net income.

Here is a look at Fannie Mae’s net income over the past year and SDQ rates.

Under the existing seller/servicer eligibility requirements, the Agency SDQ Rate is defined as 100 multiplied by (the UPB of mortgage loans 90 days or more delinquent or in foreclosure for Fannie Mae, Freddie Mac, and Ginnie Mae/Total UPB of mortgage loans serviced for Fannie Mae, Freddie Mac, and Ginnie Mae). Beginning with the financial quarter ending Jun. 30, 2020, the Agency SDQ Rate will include an adjustment for mortgage loans in a COVID-19-related forbearance plan that are 90 days or more delinquent and were current at the inception of the COVID-19-related forbearance plan. The UPB of such mortgage loans shall be multiplied by .30 and added to the UPB for SDQ mortgage loans for the purposes of determining the numerator in the calculation of the Agency SDQ Rate.

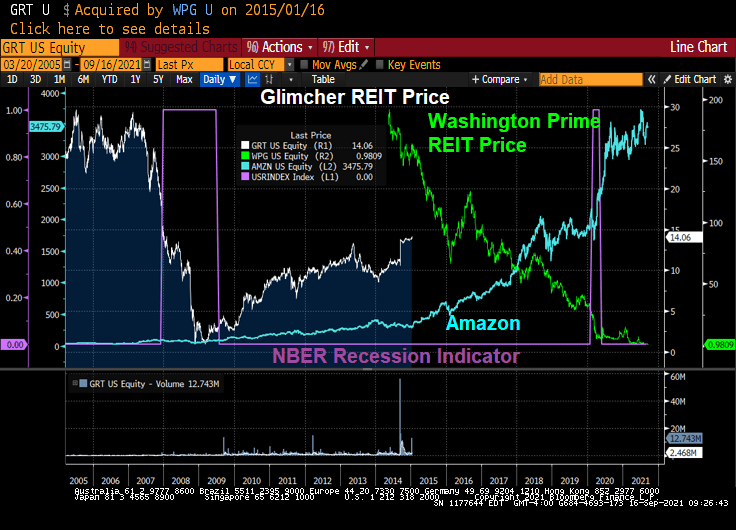

It is tough to operate a retail Real Estate Investment Trust (REIT) in the face of the triple whammy that hit retail shopping. First, there was the housing bubble/subprime crisis of 2008-2009. Then there was the advent of on-line shopping, then COVID.

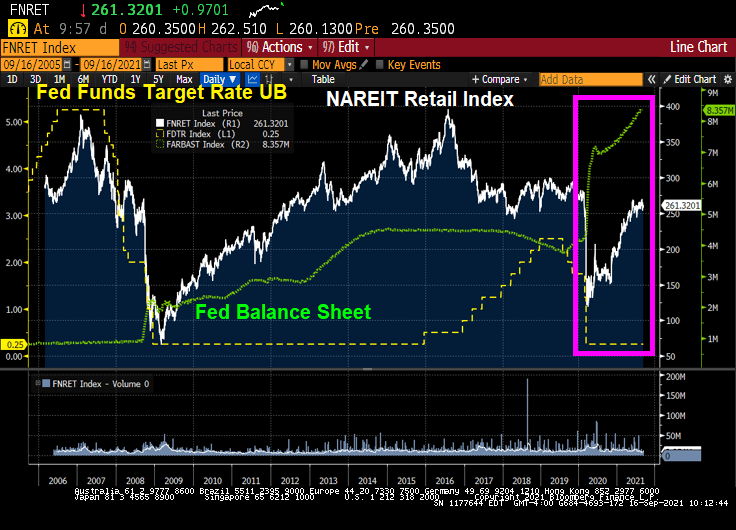

I look at the NAREIT retail index and two retail REITs for comparison: Simon Property Group and Washington REIT. And as a proxy for online shopping, I compare them to Amazon. Both Washington REIT and the NAREIT retail index were at loft valuations at the peak of the housing bubble, but crashed with the onset of the housing bubble burst and ensuing financial crisis. But following The Great Recession, both recovered by 2016 (along with Simon Property Group which actually far exceeded their pre-Great Recession peak.

ii

But then retail mall disaster struck. In the form of on-line shopping. I use Amazon to represent on-line shopping. While NAREIT Retail and Simon fell from their 2016 peak, Washington REIT got clobbered.

Then Covid struck. When combined with on-line shopping and fear mongering by Anthony Fauci, retail REITs got hit hard. But all three have rebounded slightly since their nadir in 2020.

An interesting case study is Glimcher REIT, a formerly privately-held commercial real estate development company from Columbus Ohio. Like other retail REITs, Glimcher was crushed by the financial crisis and Great Recession. Glimcher’s share price fought back to $14.06 per share (down considerably from $29.28 in February 2007).

Washington Prime Group Inc. acquired Glimcher Realty Trust for $4.3 Billion in stock and cash Including the assumption of Glimcher’s debt. Right as on-line shopping took off. And the Covid struck a death blow leaving Washington Prime trading at $0.98. Washington REIT is transforming into a multifamily REIT given the overbuilding of DC area office space and the triple whammy of retail centers.

Retail REITs have almost recovered from Covid, thanks to the massive monetary stimulus from The Federal Reserve. Not to mention fiscal stimulus from DC.

Yup, a triple whammy has hit retail REITs with some faring better than others.

But the NAREIT RESIDENTIAL Index has exploded with Fed stimulus.

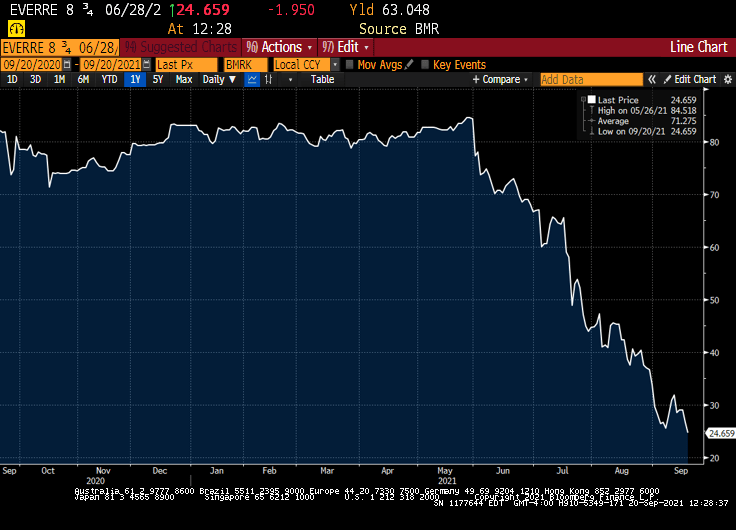

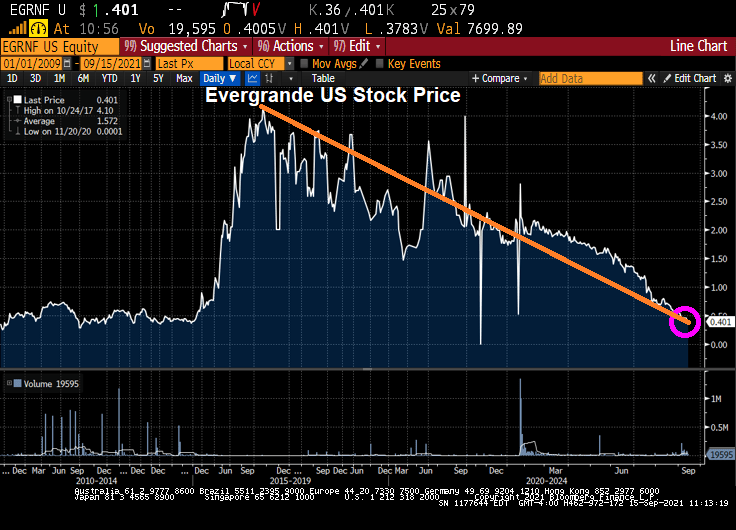

According to Bloomberg, Chinese authorities told major lenders to China Evergrande Group not to expect interest payments due next week on bank loans, which takes the cash-strapped developer a step closer the nation’s largest modern-day restructurings, and guarantees that China’s “Lehman Moment” is now just a matter of days, if not hours.

According to Bloomberg, citing unnamed sources, the Ministry of Housing and Urban-Rural Development told banks in a meeting this week that Evergrande won’t be able to pay its debt obligations due on Sept. 20, and instead most of Evergrande’s working capital in now being used to resume construction on existing projects, the housing ministry told bankers, according to a Bloomberg source.

And since nonpayment of interest and principal will represent an event of default, the company is unlikely to make any subsequent interest, or principal, payments either since it will have already default even though Bloomberg claims that “Evergrande is still discussing the possibility of getting extensions and rolling over some loans.” It won’t, especially since the developer will also miss a principal payment on at least one loan next week, which means it’s game over.

China Evergrande Group may undergo one of the country’s biggest-ever debt restructurings, if the developer’s distressed-level bond prices are any indication.

Singapore LLC, also predicts Evergrande may default and enter restructuring. That risk is being priced in, with many of Evergrande’s dollar bonds trading near 30 cents.

Debt delinquencies at developers the size of Evergrande are so rare in China that investors, analysts and regulators would only have a few case studies to go on. Kaisa Group Holdings Ltd. in 2015 became the first Chinese builder to default on dollar bonds. The restructuring of another, China Fortune Land Development Co., is currently under negotiation.

Do I detect a trend in Evergrande’s US stock price?

Update: China has a variation of the Wuhan Flu and it is spreading throughout other Chinese property developers after Evergrande’s main unit (onshore real estate) said that trading in all of its onshore bonds would be suspended on Sept 16 to ensure fair information disclosure following a downgrade to A from AA (which in China is viewed as the lowest investment grade rating) by China Chengxin International.

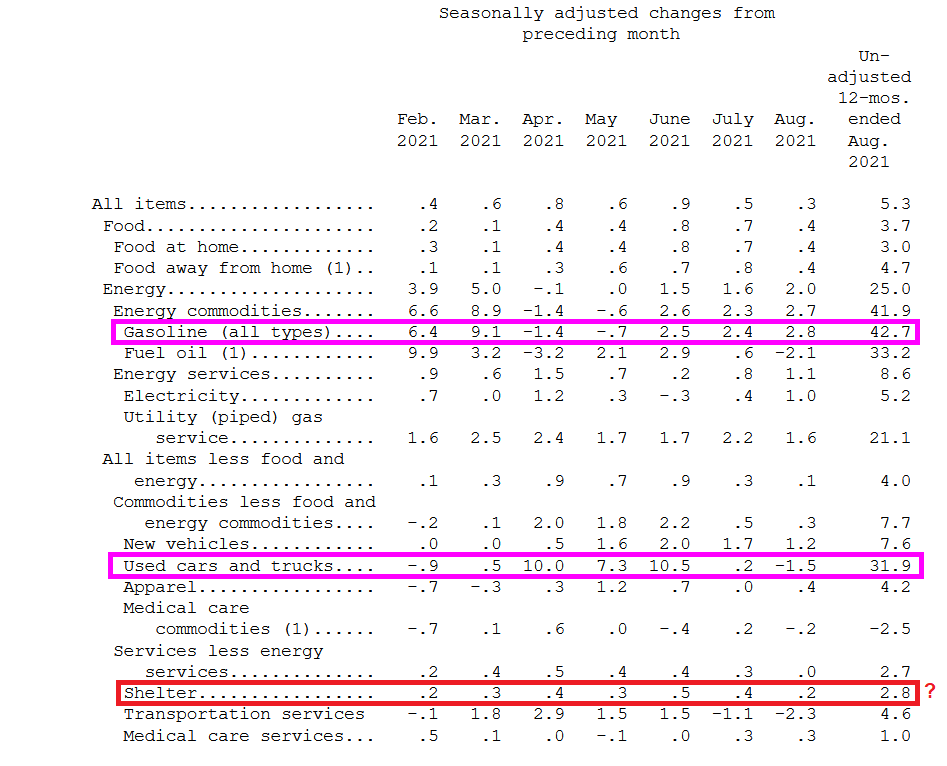

US inflation remained about the same in August as it was in July. CPI YoY fell ever so slightly from 5.4% in July to 5.3% in August. Real hourly earnings remain negative.

The source of consumer inflation? Gasoline prices rose 42.7% YoY while used cars and trucks rose 31.9% YoY.

Shelter rose 2.8% YoY. That is odd since the Case-Shiller national price index is growing at a torrid 18.61% YoY pace and the Zillow Rent Index YoY has recovered to a sizzling 9.24% YoY pace.

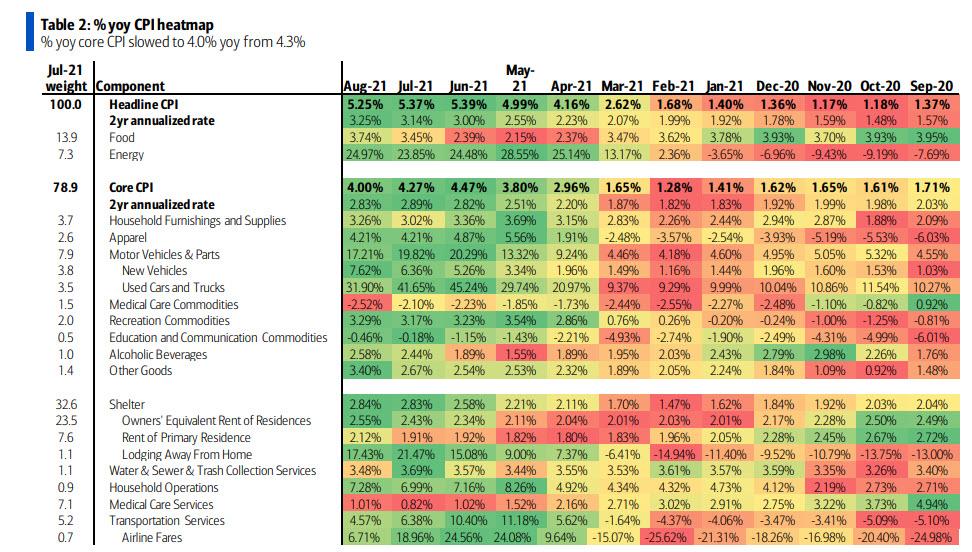

The YoY heatmap of inflation.

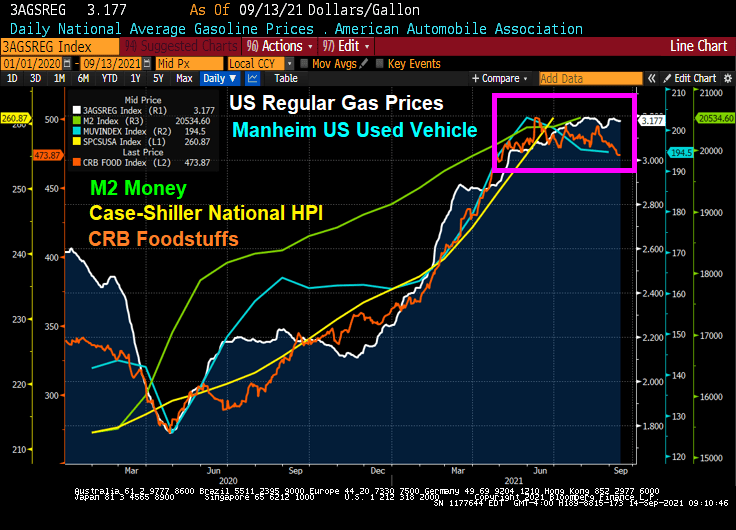

However, with the exception of home prices and rent, we are seeing a slowing of used car, foodstuffs and regular gas prices over the summer.

Since the Covid outbreak in early 2020, The Federal Reserve lowered their target rate and super-spiked their balance sheet. Helping to lower bank deposit rates to near zero.

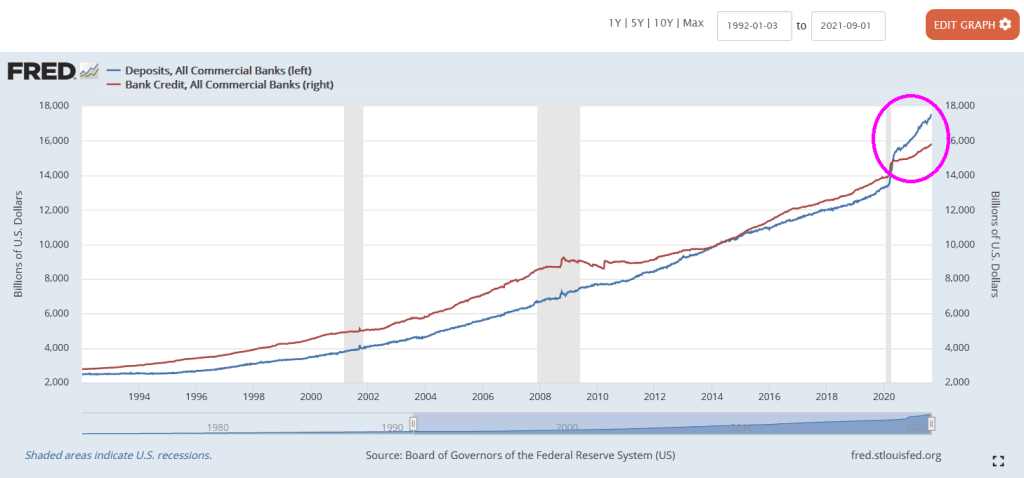

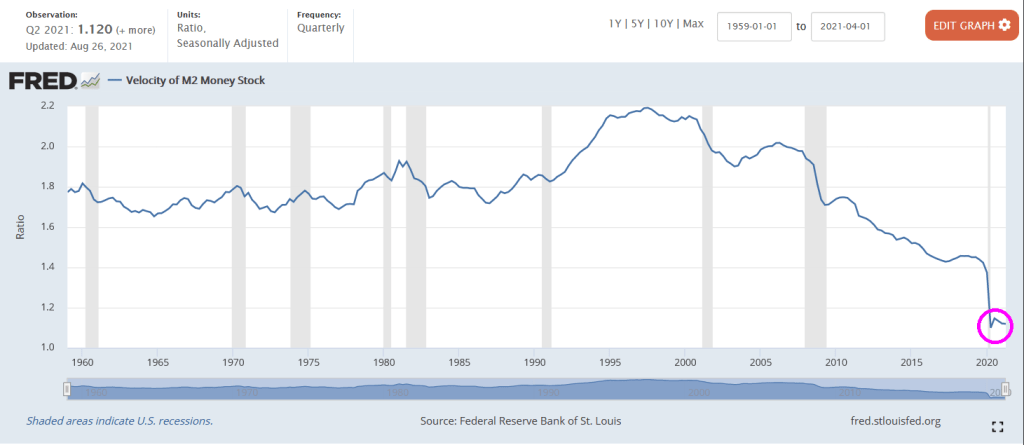

But despite near zero bank deposit rates, we seeing bank deposits are larger than bank credit such as commercial and industrial loans, residential mortgages loans, car loans, etc. Normally, bank credit EXCEEDS bank deposits.

The problem? One of them is negative growth in commercial and industrial lending. It declined 13.5% YoY in August. Of course, The Federal government extended emergency business loans that were counted as C&I loans, hence the spike in C&I loan growth in May 2020. But now we are seeing a real slowdown in C&I lending.

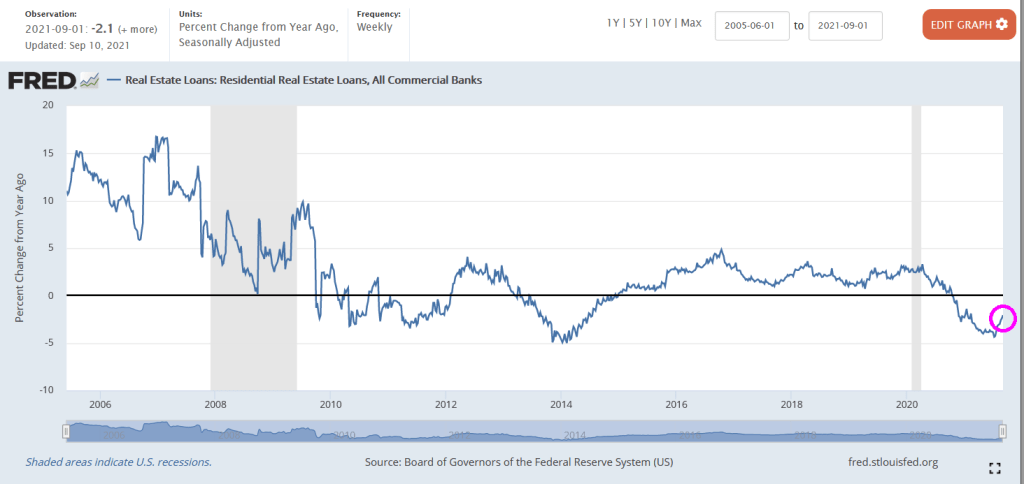

Residential lending is down 2.1% YoY as of September 10 (for August).

Commercial real estate lending? At least it is growing at a 2.9% YoY pace for August.

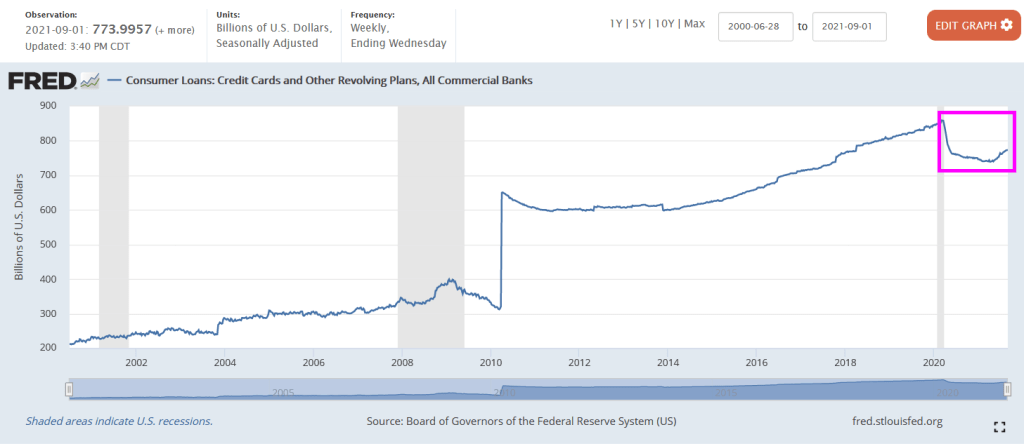

Credit cards and other revolving plans increase steadily since 2014 and then declined after the Fauci Flu struck. But credit cards and revolving credit has started to rise again.

The Fed’s massive overreaction to Covid caused a storm surge in C&I lending that has subsided. But other bank lending has slowed as well.

Lots of bank assets with nowhere to go.

No wonder M2 Money Velocity (GDP/M2 Money) is at historic lows.

Remember, Federal Reserve Chair Jerome Powell is up for reappointment and President Biden must make a decision on his reappointment.

You must be logged in to post a comment.