Its Monday! Typically we see Blue Mondays. But not with the tariff war between China and the US. We are watching a chess match between Trump and China. Dow futures are up 461 points at 9am EST.

I’ve got a whole lot of lovin’ for the markets!

Confounded Interest – Anthony B. Sanders

Financial Markets And Real Estate

Its Monday! Typically we see Blue Mondays. But not with the tariff war between China and the US. We are watching a chess match between Trump and China. Dow futures are up 461 points at 9am EST.

I’ve got a whole lot of lovin’ for the markets!

Obama/Biden/Harris/Schumer/Pelosi have let the US be the punks for China. Trump is simply trying to level the playing field and China’s Xie doesn’t like the new equilibrium.

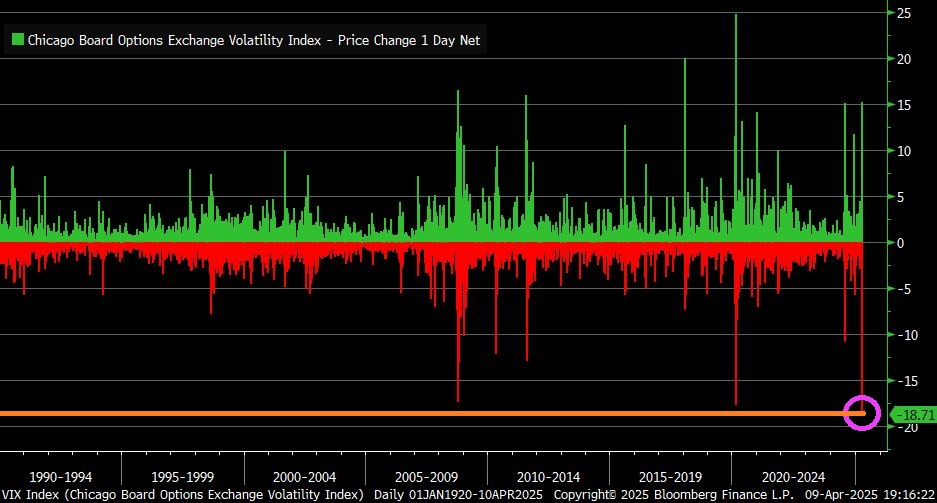

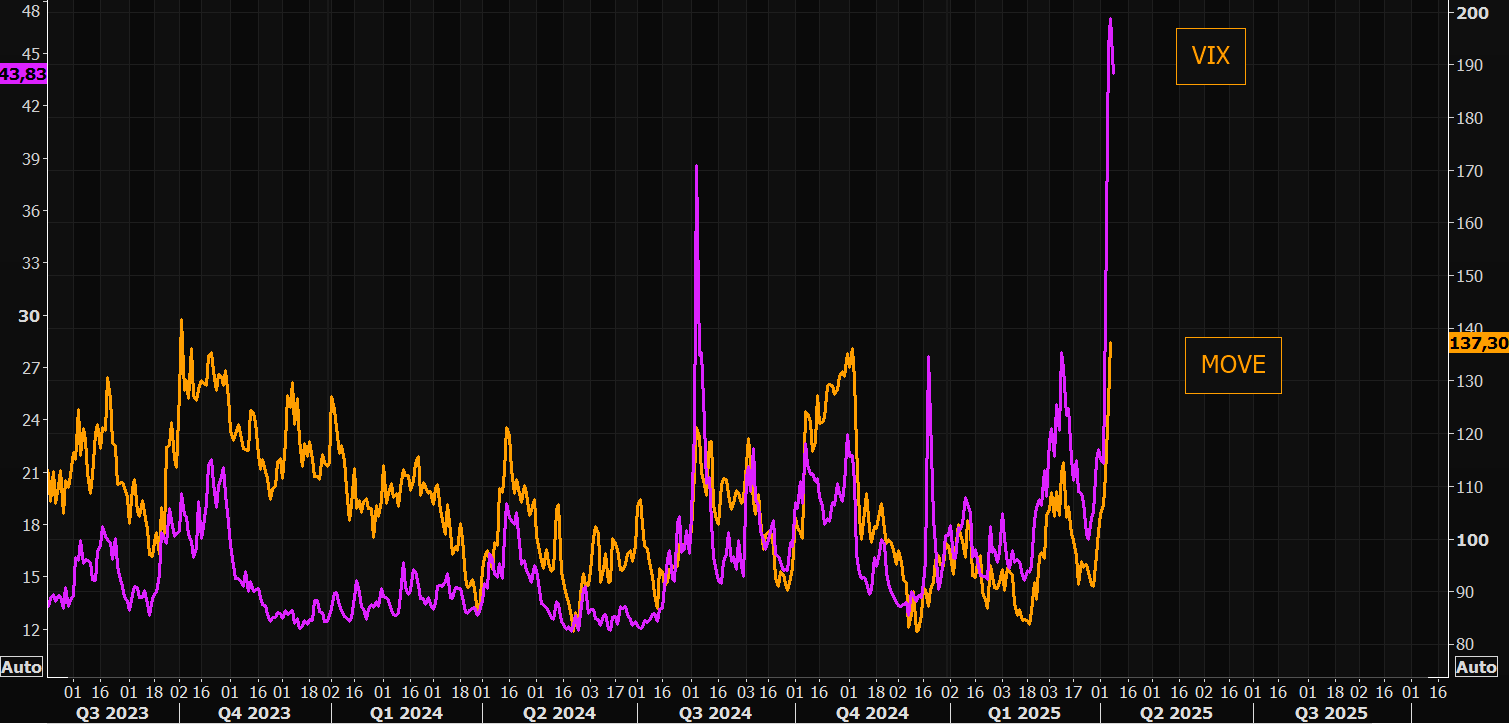

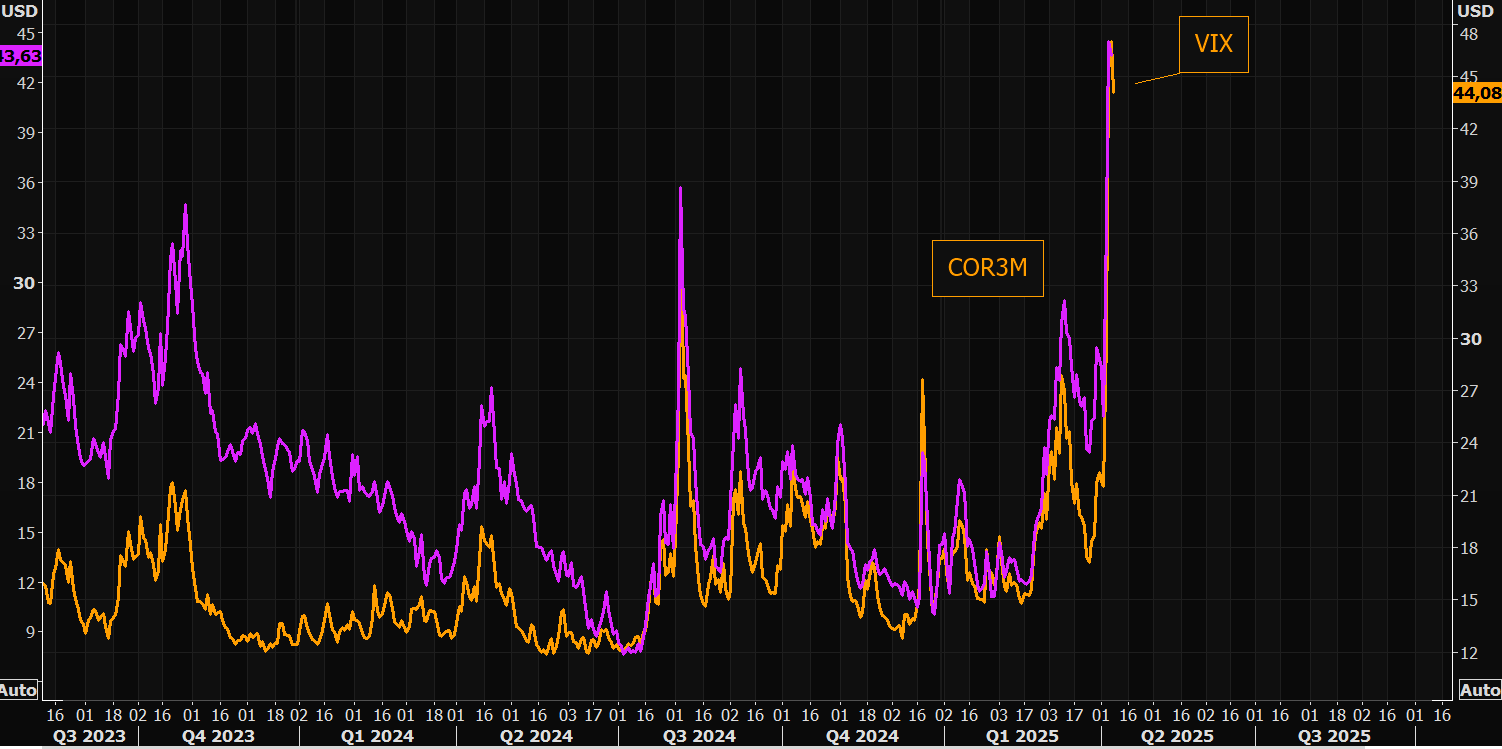

VIX Index fell by 18.7 points yesterday … largest one-day decline in history.

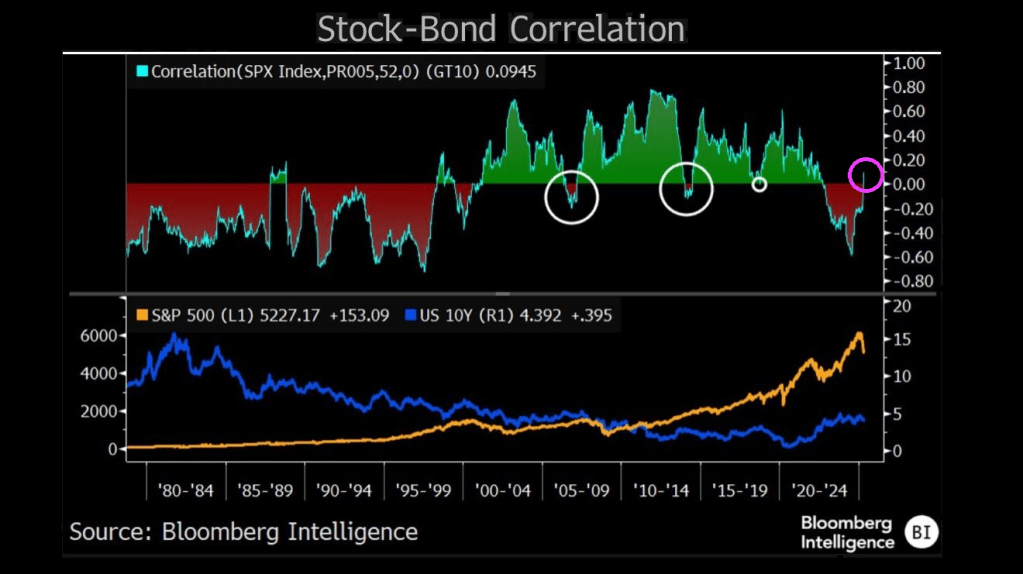

The correlation between stock prices and bond yields has returned to positive territory — hinting at a period of distress in equities and a regime shift in equity and bond markets where recession fears, rather than inflation, may be starting to drive direction of both. The correlation between the two asset classes was positive for the better part of 20 years prior to the pandemic, suggesting equities trended in the direction of yields as inflation mostly coincided with growth. Stocks held a negative correlation to yields throughout most of the 1980s and 1990s, when inflation hurt stocks — and that phenomenon returned for the 2022-24 bear market and recovery period.

Notably, major stock corrections occurred each time the correlation jumped out of its primary regime.

China’s Xi flashes a Hitler salute!

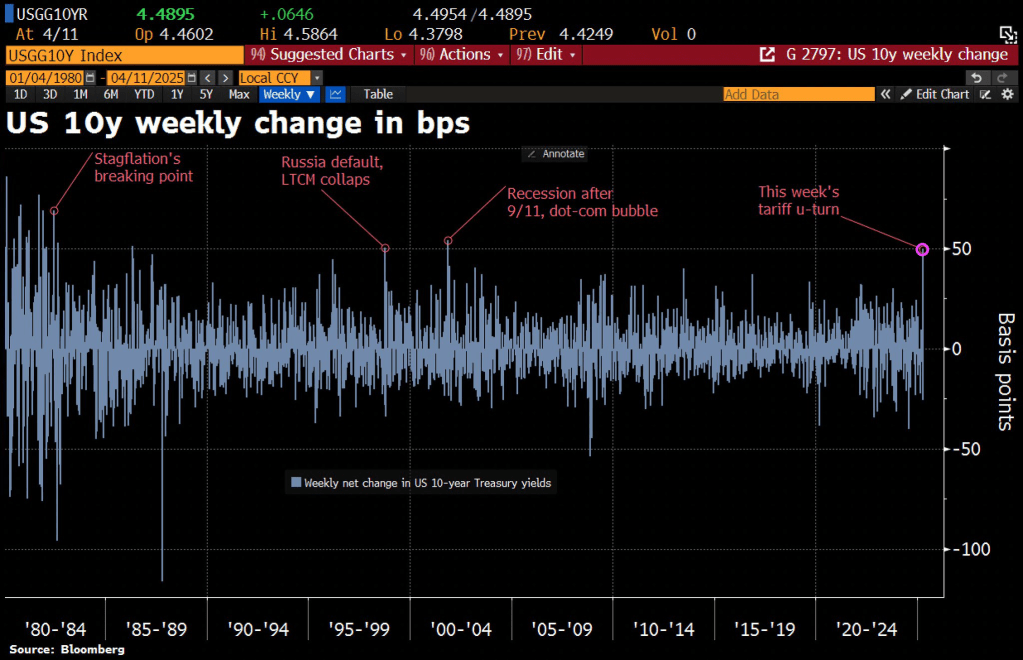

Thunderstruck! The tariff kerfuffle between the Trump Administration and China is causing turbulence in the Treasury market. The 10-year Treasury rate is soaring with China’s counterpunching.

MBS spreads are widening.

Along with volatility.

But corporate spreads are widening more than MBS spreads.

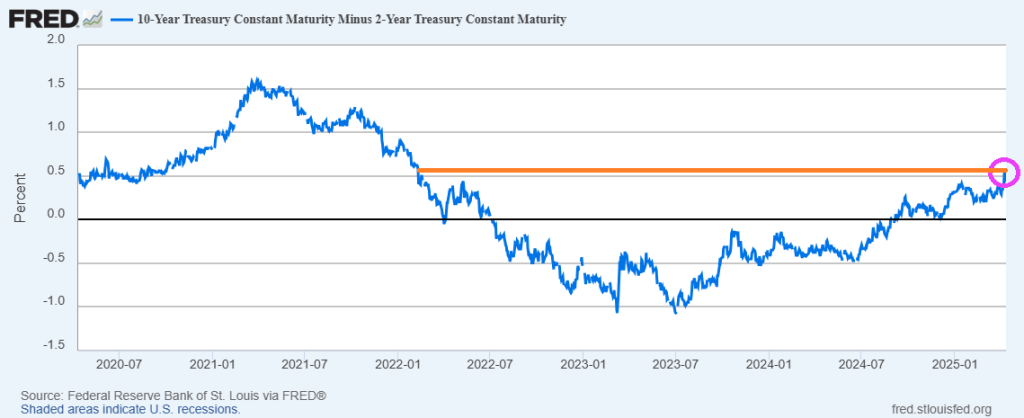

The 10Y-2Y yield curve has risen to the highest level since the early days of “China Joe” Biden.

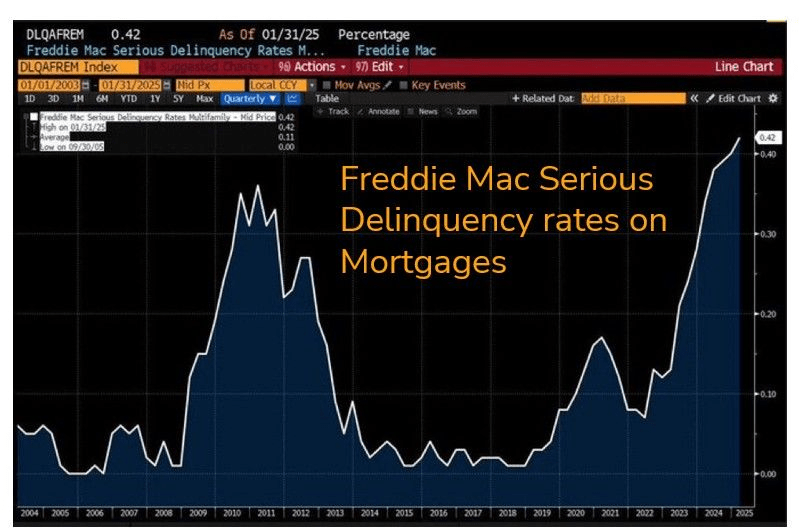

On a related note, Freddie Mac serious delinquency rates on mortgages is now the highest since the financial crisis.

Washington DC is now Tariff Town.

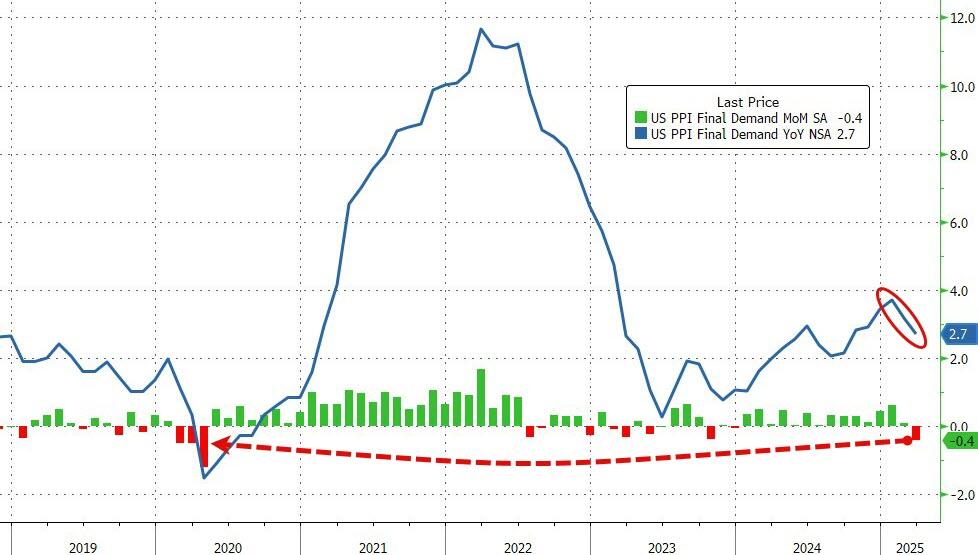

Headline PPI fell (yes fell) 0.4% MoM (dramatically cooler than the 0.2% MoM rise expected), dragging the headline index down to +2.7% YoY.

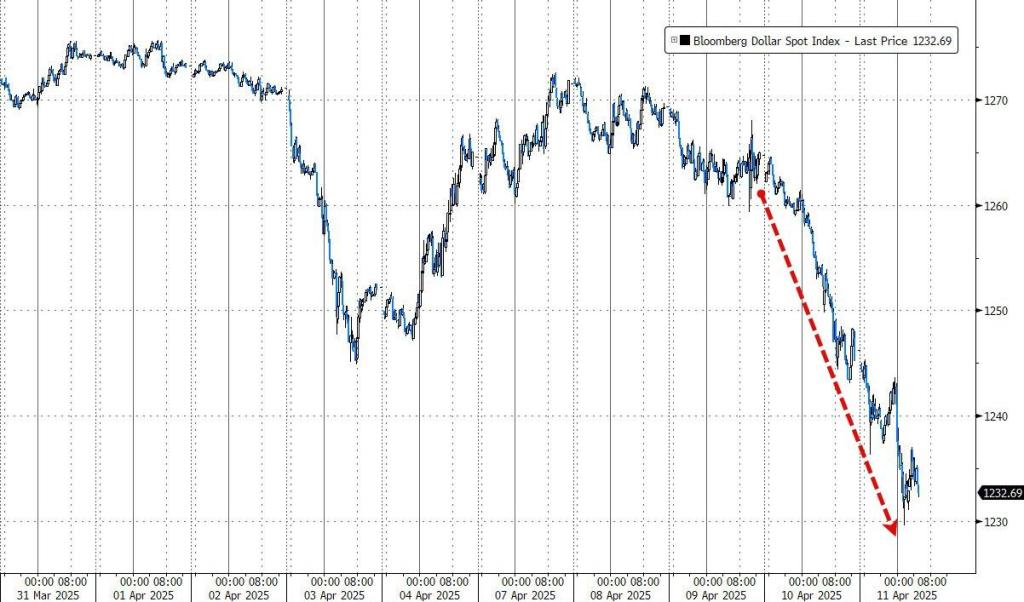

The market is re-assessing the structural attractiveness of the dollar as the world’s global reserve currency and is undergoing a process of rapid de-dollarization.

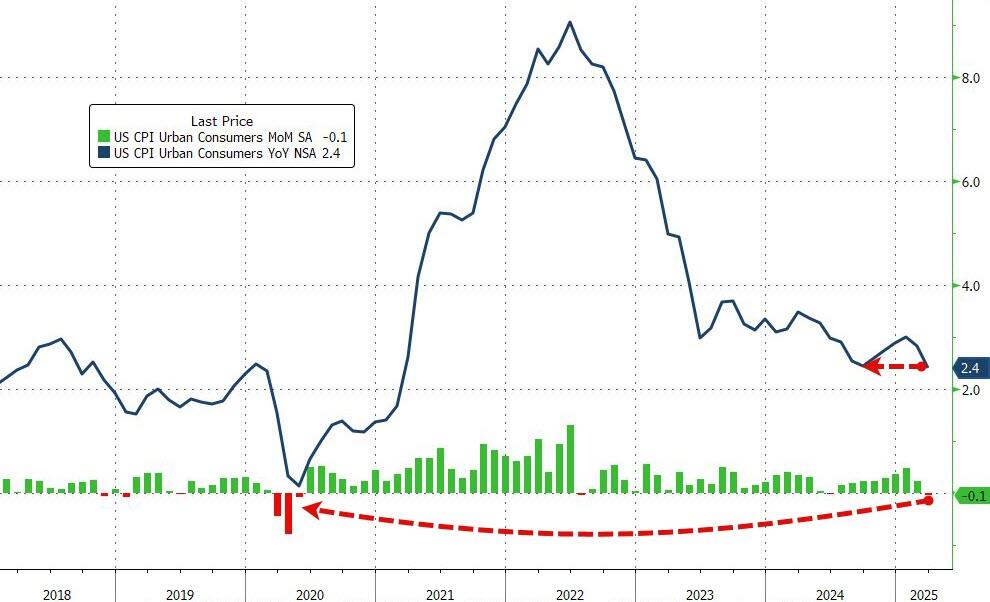

Hello Hello pre-Biden inflation levels!

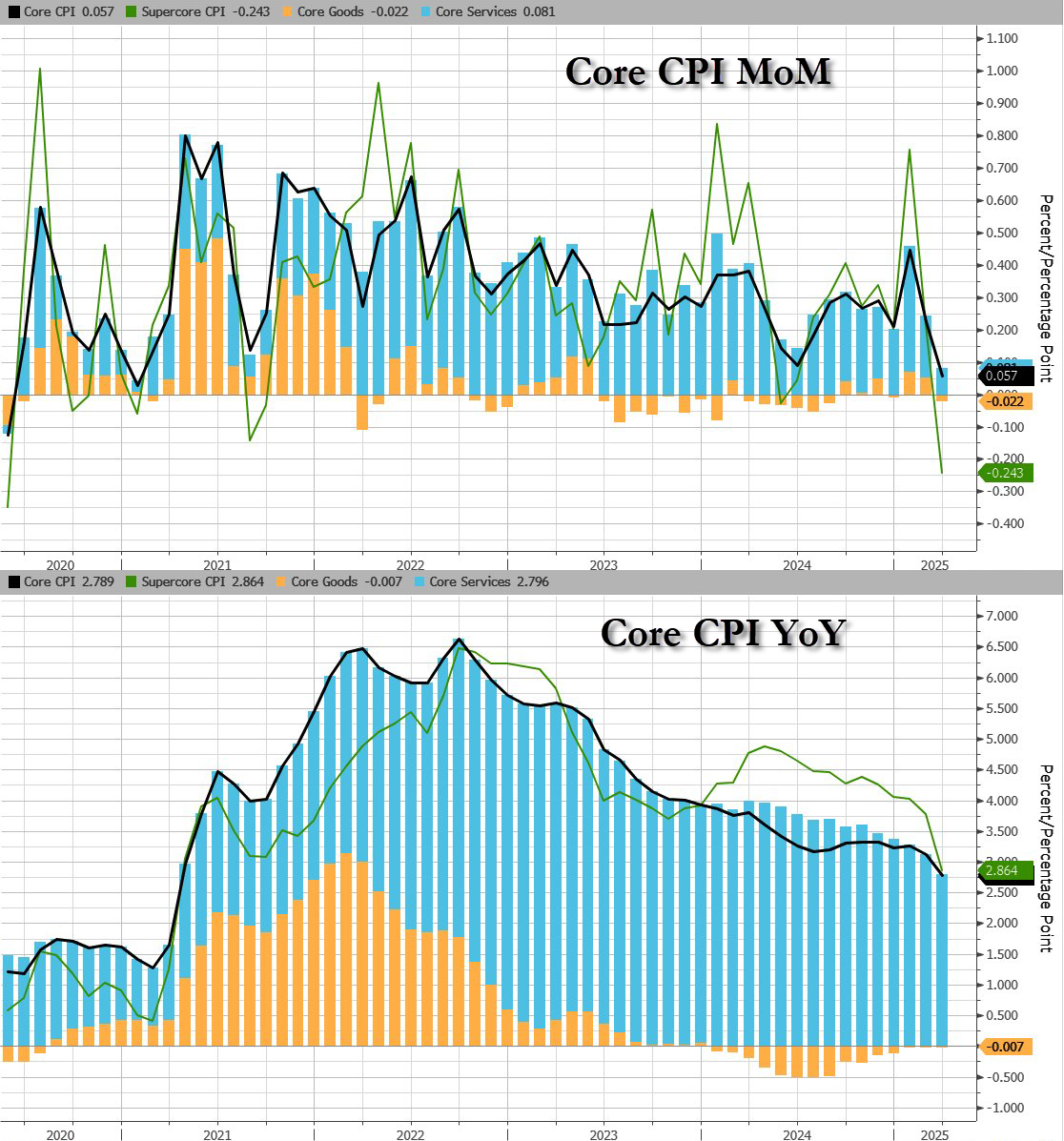

Having dipped lower in the previous month (following a few straight months of re-acceleration), expectations were for both headline and core measures to continue trending lower on a YoY basis… and they were.

Headline CPI FELL 0.1% MoM (vs +0.1% exp), which dragged the YoY CPI to +2.4%, matching the September lows…

That is the weakest MoM print since May 2020.

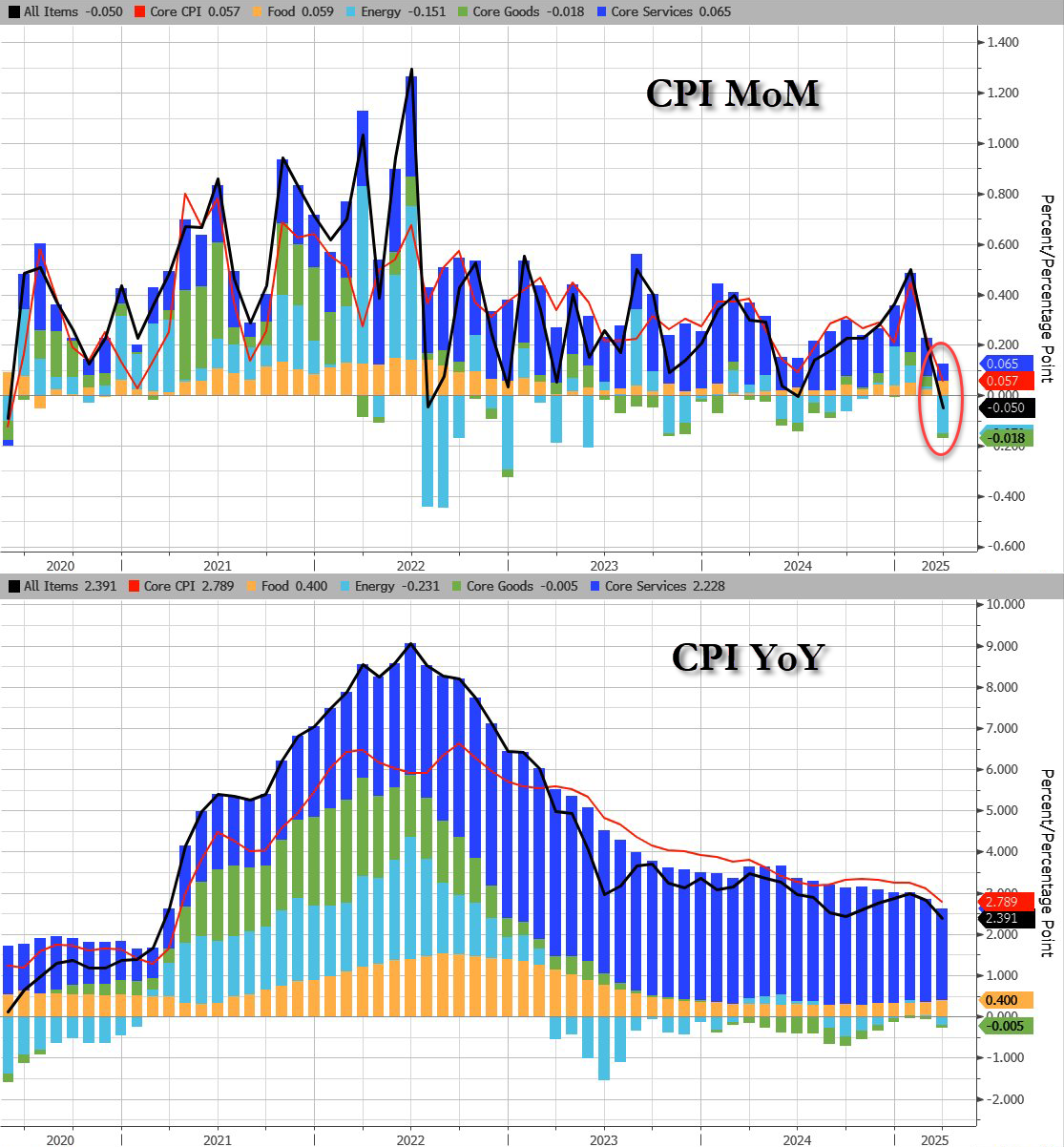

Core CPI also printed cooler than expected (+0.1% MoM vs +0.3% MoM exp), pulling the YoY print down t0 +2.8% YoY – the lowest since March 2021…

Services inflation tumbled…

Headline:

Core CPI:

Core CPI details (MoM increase):

Core CPI details (YoY increase):

While goods inflation is flat (zero-ish), services cost inflation is fading fast…

Shelter and Rent inflation is slowing fast:

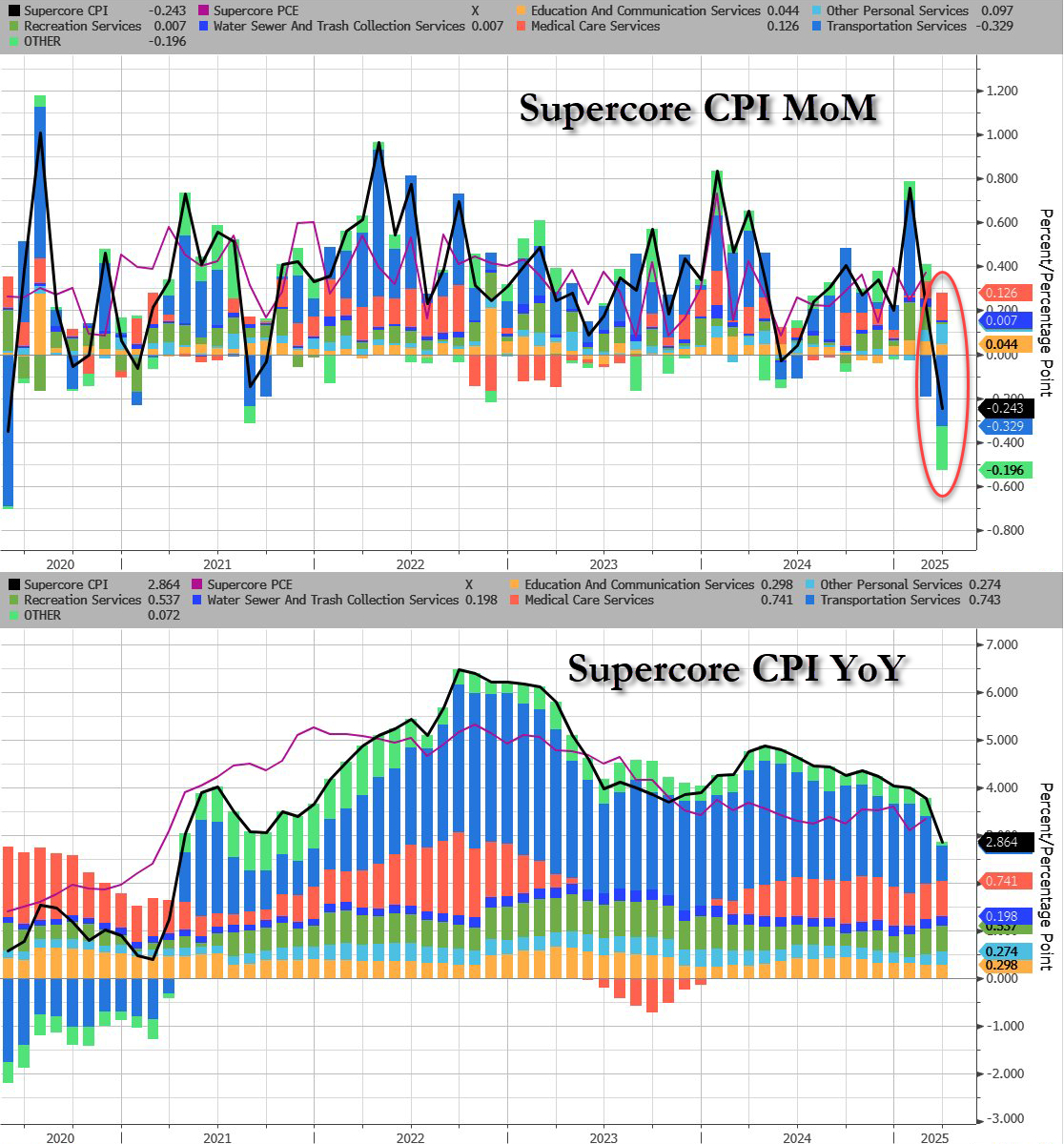

The so-called SuperCore CPI – Services Ex-Shelter – dropped 0.1% MoM dragging it down to +3.22% YoY – the lowest since Dec 2021…

Drill Baby Drill (and tariffs recession fears) have dragged energy prices lower and pulled CPI lower with it…

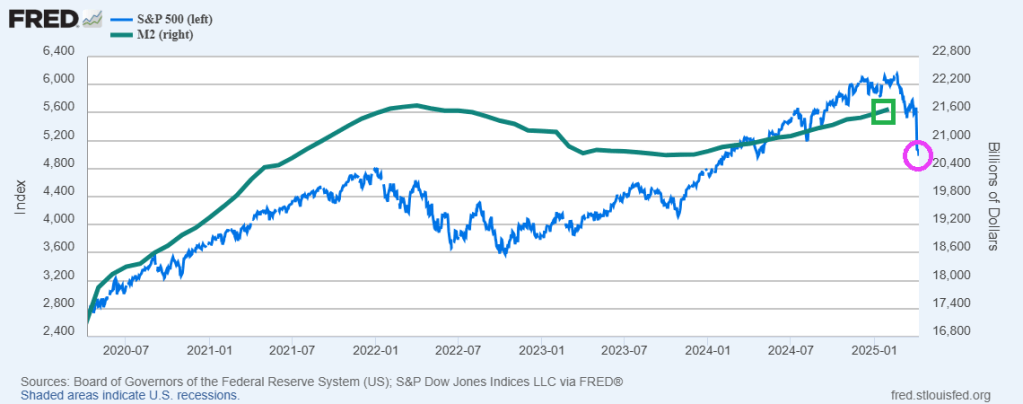

The Federal Reserve has created massive asset bubbles in financial markets. And the “tariff war” between the US and China. Since April 8, 2020, the S&P 500 index is up 81% while The Federal Reserve has printed a staggering amount of money as M2 Money is up 27.4% over the same period.

So, it is not surprising (except to Barstool Sports’ Dave Portnoy) that the stock market has declined with China’s childish petulance over Trump’s tariffs. While Trump levied a 104% tariff on Chinese goods, China counterattacked with a 84% tariff on US goods.

Markets are ranked by fear about tariffs. Particularly since China is acting like a child.

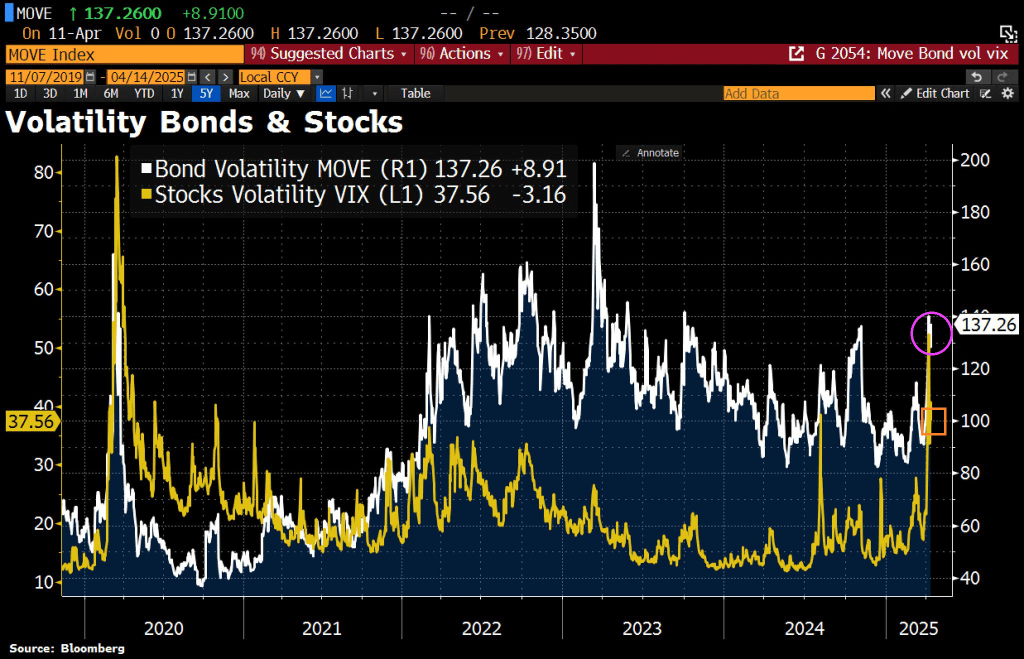

Bond volatility has shot up higher, but remains “muted” compared to the VIX move.

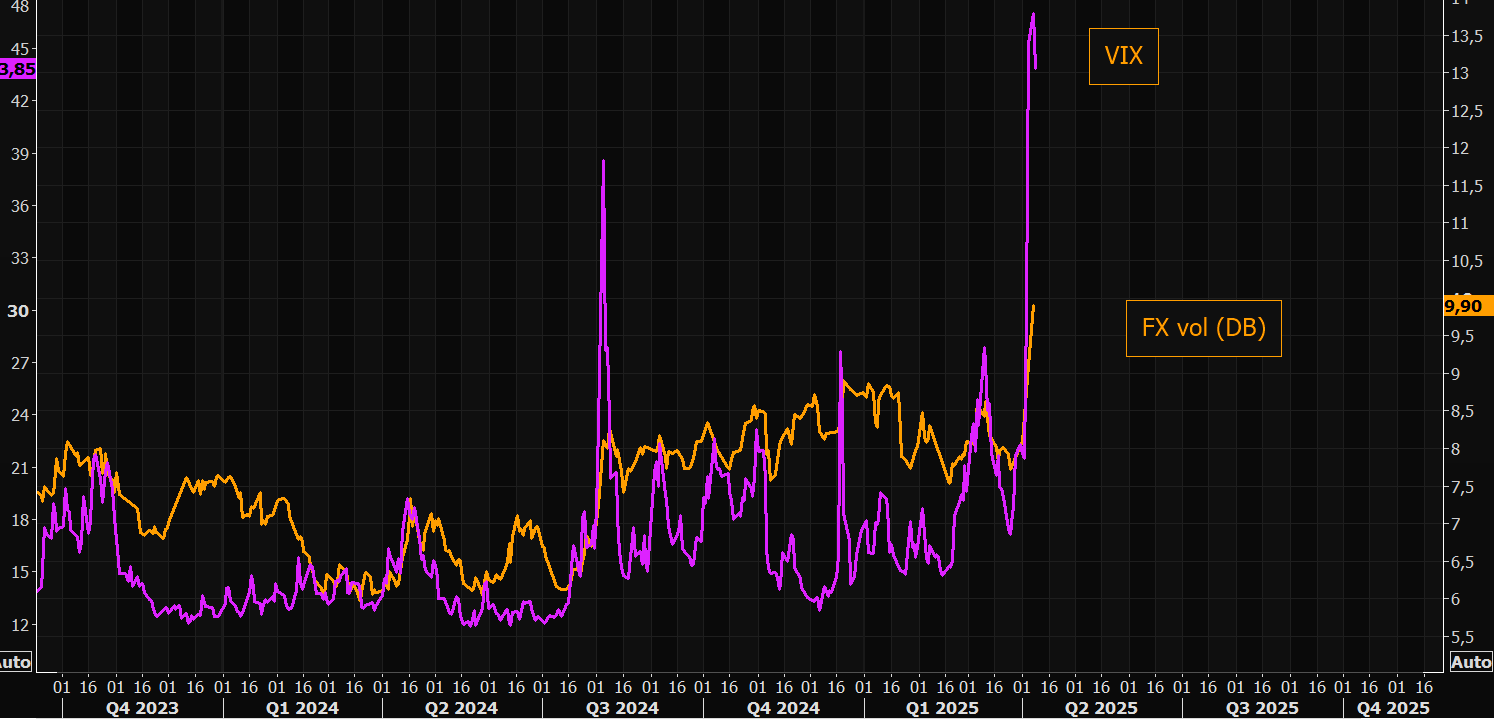

FX volatility has shot up higher as well, but is pale in comparison to the VIX move.

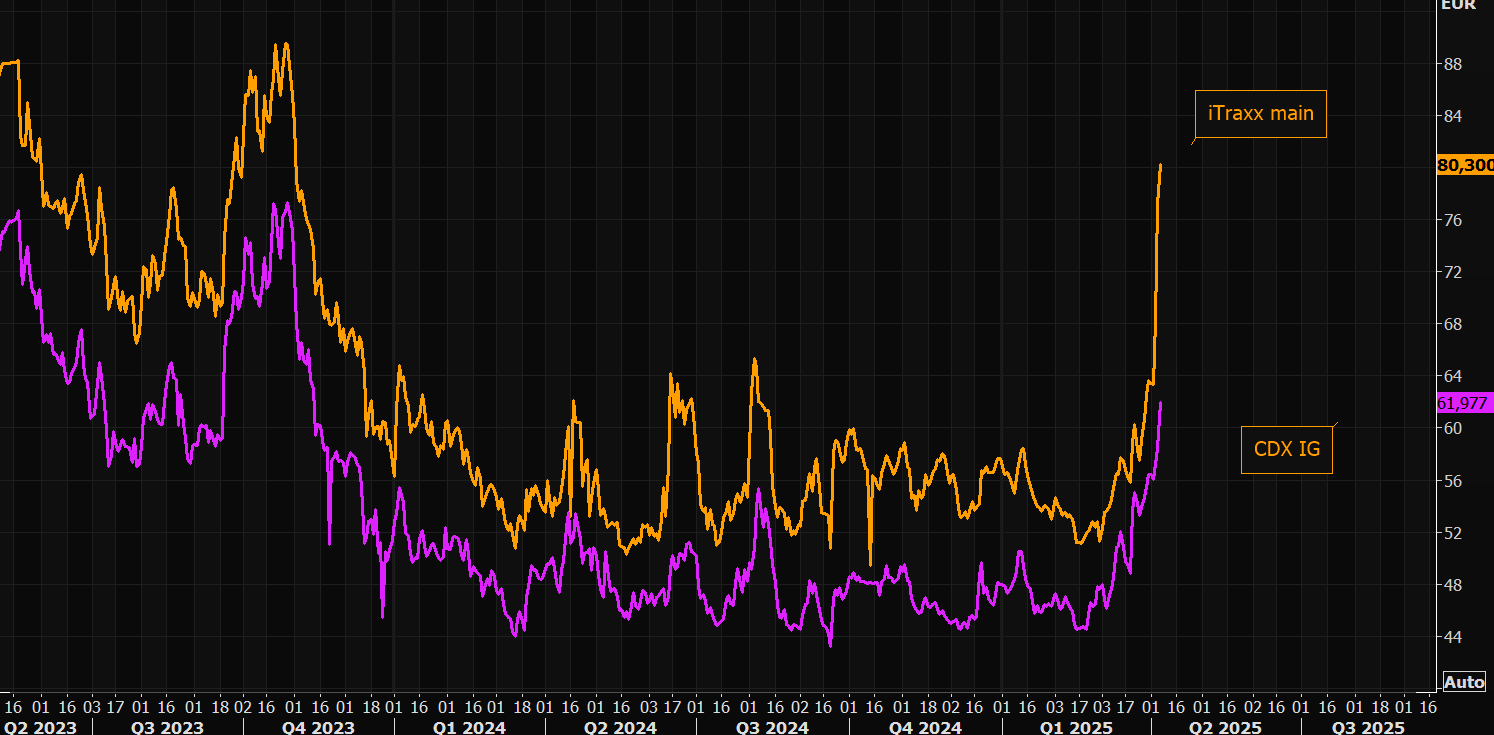

Credit protection has surged during the “chaos”. Chart shows the US and the European versions.

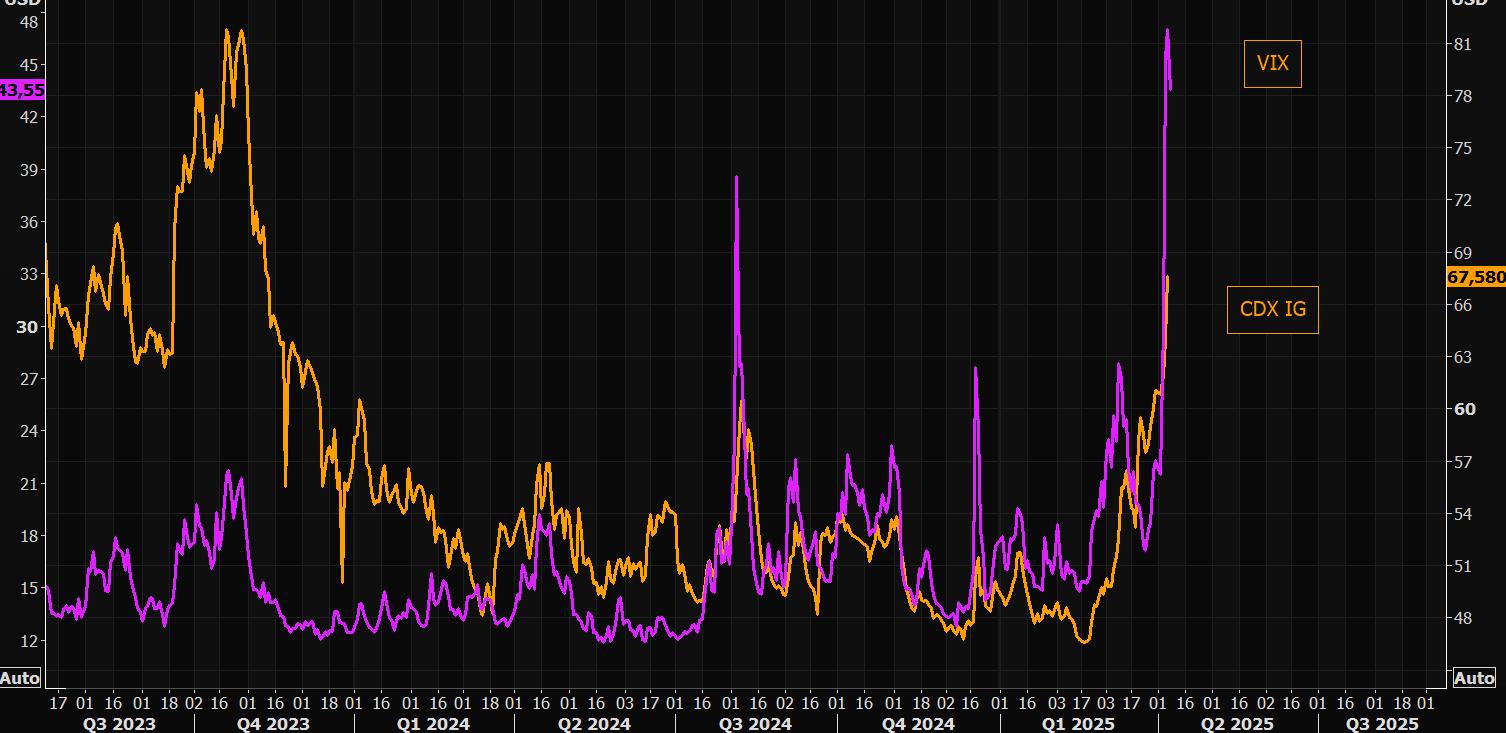

VIX vs CDX IG.

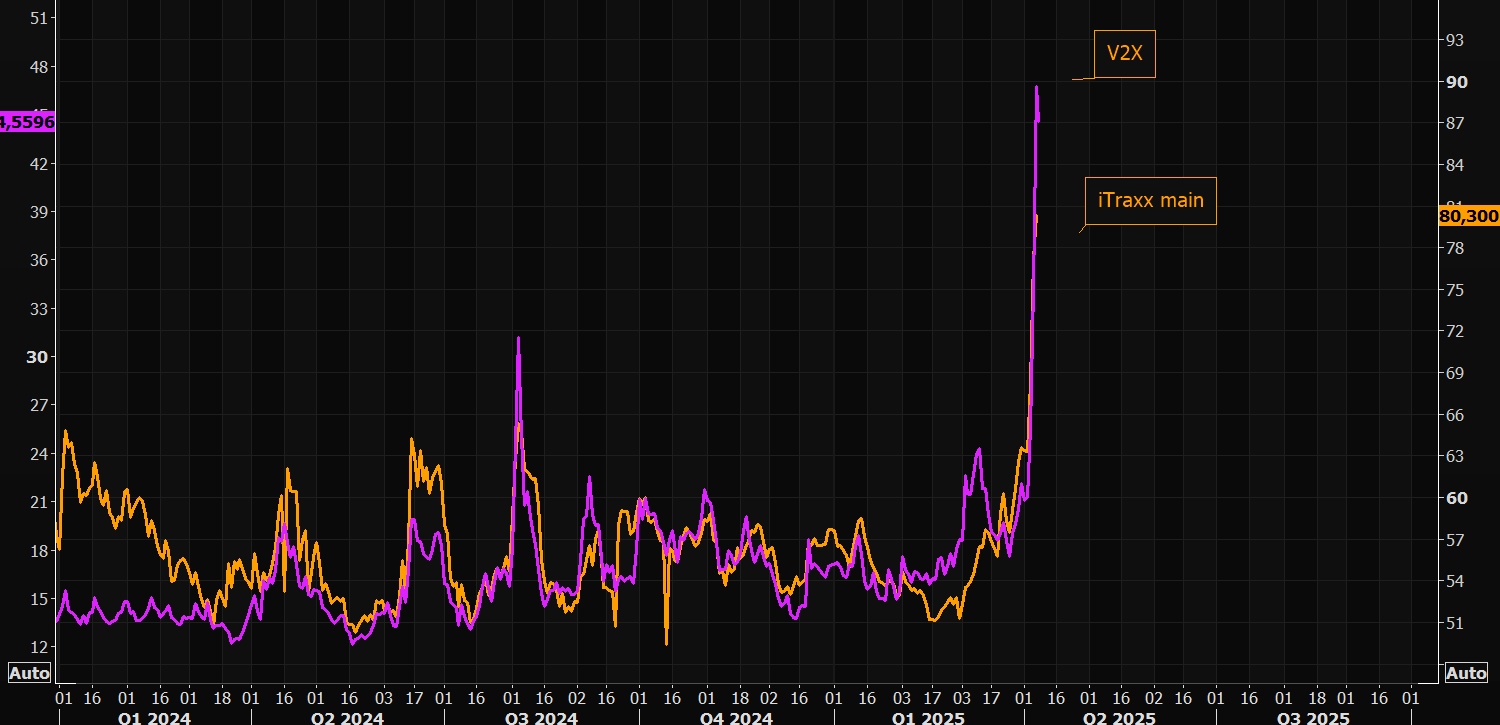

V2X vs iTraxx main.

Implied correlations showing a lot of “fear” as pretty much everything has been treated as if it were the “same” during the crash.

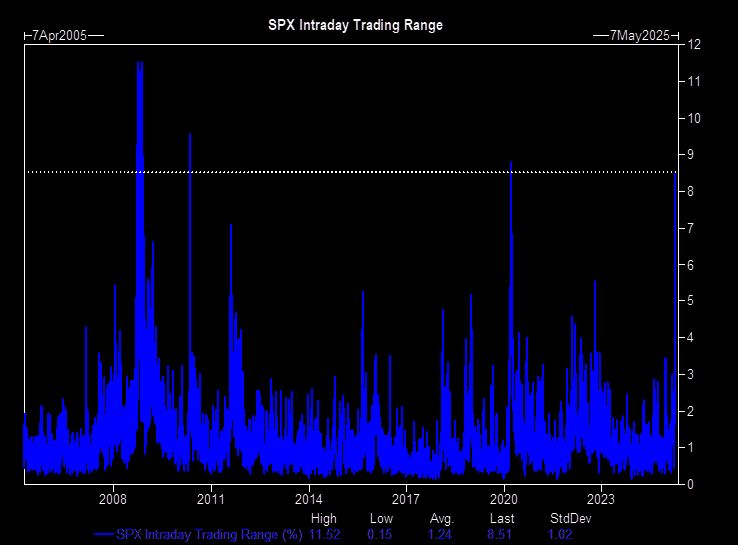

Intraday range was huge during yesterday’s session, but close to close very modest. Imagine trading short gamma….and hedging the extremes.

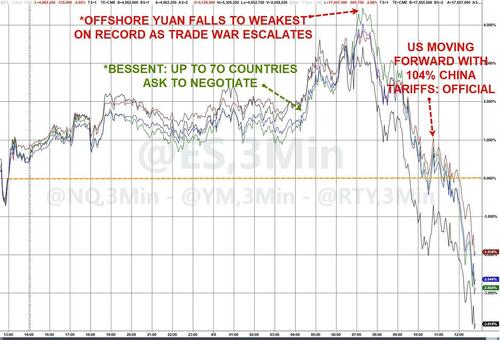

The Yuan is having a volatile day.

US tariff policies for the last 50 years represent a folly. Particularly since Presidents Obama and Biden (along with Chuck Schumer and Nancy Pelosi) did nothing to correct the enormous disparity in tariffs. Trump is trying to do something to right the ship before it sinks like The Titanic.

Victor Davis Hanson wrote in the Daily Signal, “China has prohibitive tariffs, so does Vietnam, so does South Korea, so does Japan, so does Mexico, and so does Europe. So do a lot of countries. So does India. But if tariffs are so destructive to their economies, why is China booming?

Why is Canada mad at us when it’s running a $63 billion surplus and it has tariffs on some American products at 250%. Doesn’t it seem like the people who started this asymmetrical—if I could use the word—trade war should be the culpable people, not the people who are reluctantly reacting to it?

Were tariffs leveled against countries that had no tariffs against us?

The US hasn’t run a trade surplus since 1975 or 50 years. So, it wasn’t suddenly we woke up and said, “It’s unfair. We want commercial justice.” No. We’ve been watching this happen. For 50 years it’s been going on. And no president, no administration, no Congress in the past has done anything about it.

In the postwar period, we were so affluent, so powerful—Europe, China, Russia were in shambles—that we had to take up the burdens of reviving the economy by taking great trade deficits. Fifty years later, we have been deindustrialized. And the countries who did this to us, by these unfair and asymmetrical tariffs, did not fall apart. They did not self-destruct. They apparently thought it was in their self-interest. And if anybody calibrates the recent gross domestic product growth of India or Taiwan or South Korea or Japan, they seem to have some logic to it.

There’s a final irony. The people who are warning us most vehemently about this tariff quote the Smoot-Hawley Act of 1930. But remember something, that came after the onset of the Depression—after. The stock market crashed in 1929. That law was not passed until 1930. It was not really amplified until ’31. And here’s the other thing that they were, conveniently, not reminded of: We were running a surplus. That was a preemptive punitive tariff, on our part, against other countries.

We had a trade surplus. And it was not 10% or 20%. Some of the tariffs were 40% and 50%. And again, it happened after the collapse of the stock market.

In conclusion, don’t you find it very ironic that Wall Street is blaming the Trump tariffs for heading us into a recession, if not depression, when the only great depression we’ve ever had was not caused by tariffs but by Wall Street?”

Average reciprocal tariffs could rise to 35%!

The Mag 7 index has gotten crushed under Trump’s tariffs.

Corporate bond yield has soared with Trump’s tariffs.

The market correction thus far is -17.5%, not even close to the worst correction since 2009 (-35.4% in 2020).

Most people are focused on the Great Reset in Global Trade, caused by Obama/Biden/Schumer/Pelosi letting US trading partners getting away with massive disparate tariffs against the US. Now that Trump is trying to level the playing field, we will see short-term losses in the stock market. But the jobs report for March shows that Trump’s economic policies are working.

The March jobs report ended up being far stronger than expected, as the US added a whopping 228K jobs, the highest since December and more than double the 117K in February (revised lower from 151K).

The better news? Federal government employment declined by 4,000 in March, following a loss of 11,000 jobs in February.

The mortgage market got its mind set on a recovery, but Biden’s mindless economic policies have jammed up the mortgage market. Example? Mortgage applications are down in a season where they typically increase.

Mortgage applications decreased 1.6 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending March 28, 2025.

The Market Composite Index, a measure of mortgage loan application volume, decreased 1.6 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index decreased 1 percent compared with the previous week. The seasonally adjusted Purchase Index increased 2 percent from one week earlier. The unadjusted Purchase Index increased 2 percent compared with the previous week and was 9 percent higher than the same week one year ago.

The Refinance Index decreased 6 percent from the previous week and was 57 percent higher than the same week one year ago.

Treasury yields continue to be volatile as economic uncertainty dominates markets. Most mortgage rates finished last week lower, with the 30-year fixed essentially unchanged at 6.70 percent. Last week’s level of purchase applications was its highest since the end of January, driven by a 3 percent increase in conventional purchases, while government purchase applications were down 2 percent.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) decreased to 6.70 percent from 6.71 percent, with points increasing to 0.62 from 0.60 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

Conforming 30Y mortgage rates are up 137% since Biden was elected President.

Biden was the destroyer!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

You must be logged in to post a comment.