It has been a wild and mostly negative ride under Biden’s Reign of Error. 40-year highs in inflation (caused by Biden’s fossil fuel mandates and Federal spending) have left the US mortgage market FINALLY seeing positive REAL mortgage rates (now 0.32%), even though the REAL 10yr Treasury yield is still negative (-2.50%).

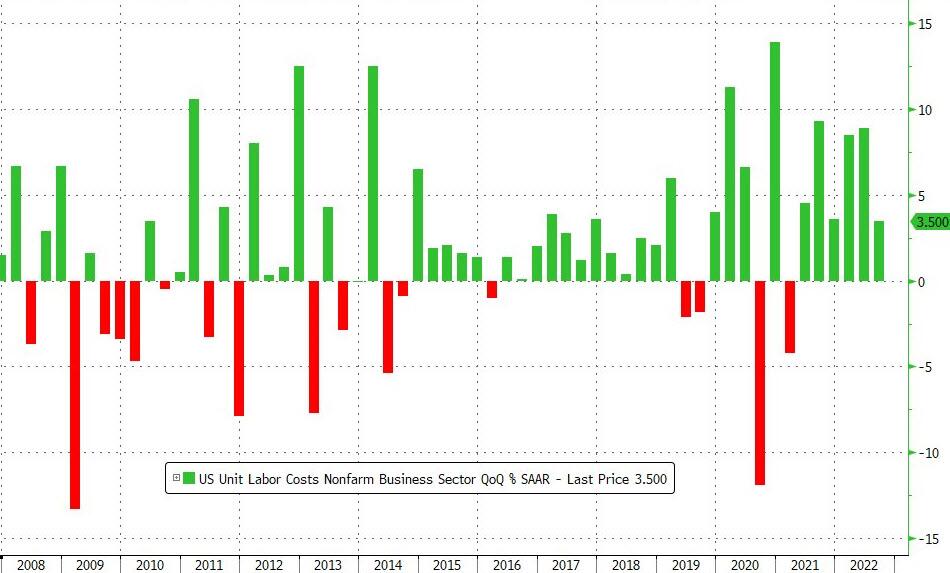

On a YoY basis, US Productivity is down for the 3rd straight quarter (and 4th quarter of the last 5).

On the mirror image of productivity, unit labor costs rose 3.5% QoQ (a notable slowing from the 8.9% QoQ growth in Q2). This was the 6th quarter in a row of rising unit labor costs (but was less than the +4.0% QoQ expected)…

However, on a YoY basis, that is the fastest growth since Q3 1982.

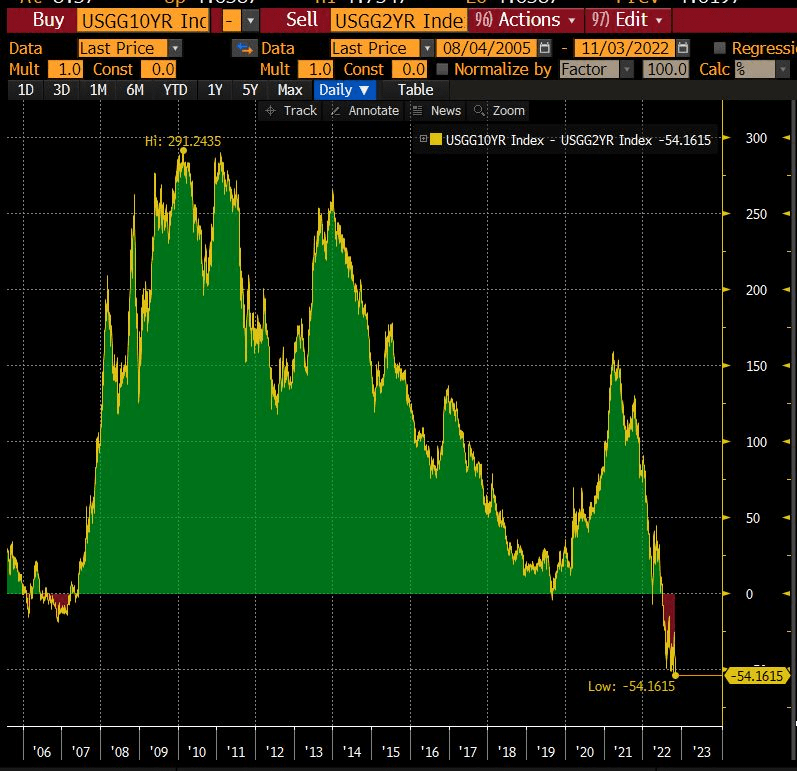

Yikes! The 2s10s Yield Curve Inversion Is the worst since the 1980s.

The Bank of England followed the Fed’s 75 basis-point increase with an equivalent hike on Thursday, but strongly pushed back against market expectations for the scale of future increases, warning that following that path would induce a two-year recession. The pound fell 1.8% to $1.1183.

Stocks and bonds fell as Jerome Powell’s warning that the Federal Reserve would raise interest rates more than previously anticipated sapped risk appetite. The dollar gained.

Futures on the S&P 500 fell 1% in the wake of Wednesday’s 2.5% drop. The selloff spread to Europe and Asia, where China’s affirmation of its Covid-Zero stance dashed hopes of a reopening. Lumen Technologies Inc., Peloton Interactive Inc., Moderna Inc. and Qualcomm Inc. tumbled in premarket trading, while Etsy Inc. and EBay Inc. rose.

So, the BofE, Fed and ECB are back to 2008/2009 era central bank rates.

But the US Fed is slow to shrink its enormous balance sheet.

The S&P 500 index tanked -2.35% after Powell and The Fed failed to pivot.

Federal Reserve Chair Jerome Powell opened a new phase in his campaign to regain control of inflation, saying US interest rates will go higher than previously projected, but the path may soon involve smaller hikes.

Addressing reporters Wednesday after the Fed raised rates by 75 basis points for the fourth time in a row, Powell said “incoming data since our last meeting suggests that ultimate level of interest rates will be higher than previously expected.”

Powell said is it would be appropriate to slow the pace of increases “as soon as the next meeting or the one after that. No decision has been made,” he said, while stressing that “we still have some ways” before rates were tight enough.

“It is very premature to be thinking about pausing,” he said.

Fed Funds Futures data point now to a June peak in the target rate of 5.055%, then a decline.

As The Federal Reserve tries to extinguished the inflation fire caused by Washington DC’s regulations and spending, The Fed has raised their target rate 75 basis points to 4%.

And the 10-year Treasury yield dropped 7 basis points on the announcement.

US mortgage applications declined for the sixth consecutive week despite a slight drop in rates.

Mortgage applications decreased 0.5 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 28, 2022. This week’s results include revised data to reflect an update to last week’s survey results.

The Refinance Index increased 0.2 percent from the previous week and was 85 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 1 percent from one week earlier. The unadjusted Purchase Index decreased 2 percent compared with the previous week and was 41 percent lower than the same week one year ago.

This morning’s WIRP (Fed Funds Futures data) is pointing to a 75 basis point increase from The FED FOMC (open market committee) at 2pm EST, rising to over 5% by the May 2023 meeting before declining again.

Since the Covid-related US mortgage foreclosure moratorium ended in June 2022, we are seeing mortgage foreclosure starts rising as The Fed tightens its monetary policy.

US 30-year mortgage rates are above 7% as The Federal Reserve slowly withdraws its Covid-related monetary stimulus and attempt to combat near 40-year highs in inflation under Biden (aka, Bidenflation).

However, the US Treasury 10-year yield is down -12 basis points this morning.

And we have an important predictor of recession, the Treasury 10yr-3mo yield curve.

And if the Republicans win The House (and maybe the Senate) at the midterms, Biden can blame Republicans for the recession.

Consumer credit outstanding soared by 8.1% YoY in August as the inflation rate soared to 8.2%. Meanwhile, the personal savings rate YoY cratered to -59.3%.

Of course, Biden is his tone-deaf manner told Americans to buy a cheaper brand of bran cereal.

{kind=link}

{kind=link}

You must be logged in to post a comment.