Is this the bubble burst many were expecting once The Federal Reserve starting raising rates?

Well, if today’s market opening is an indication, the answer is yes. The NASDAQ Composite Index is down 1.36% and West Texas Intermediate Crude Oil futures prices are down 2%.

The S&P 500 index is down over 10% since January 3rd.

Drawdown is taking place.

But if you think the US equities are deflating, look at European equities. The Euro Stoxx 50 index is down 4.04%.

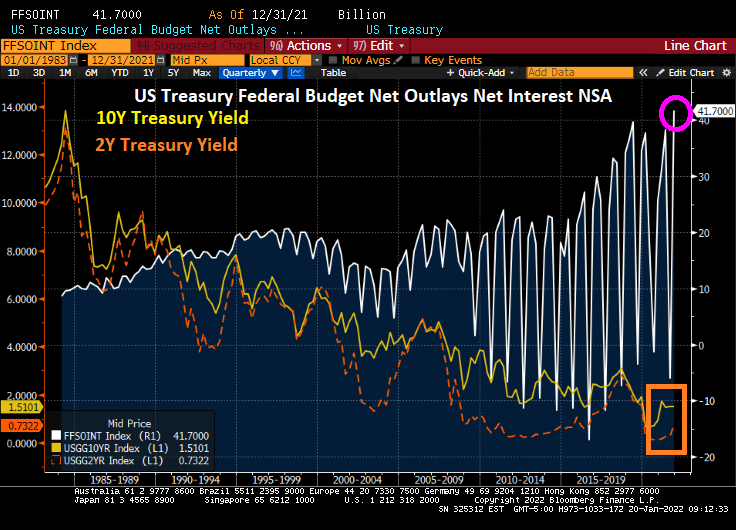

Treasury Secretary Janet Yellen is having trouble with the curve (yield curve, that is). It keeps inching up, meaning that Treasury’s cost of debt financing is inching up too.

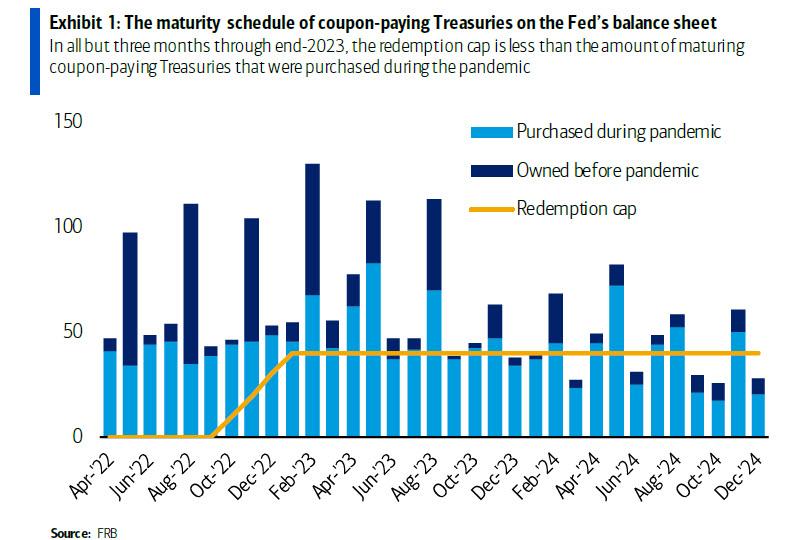

As Treasury yields keep rising, so does the problem of financing the massive Federal debt load. Here is a chart showing the interest outlays in the Federal budget against the cost of Federal funding at the 10-year and 2-year tenors.

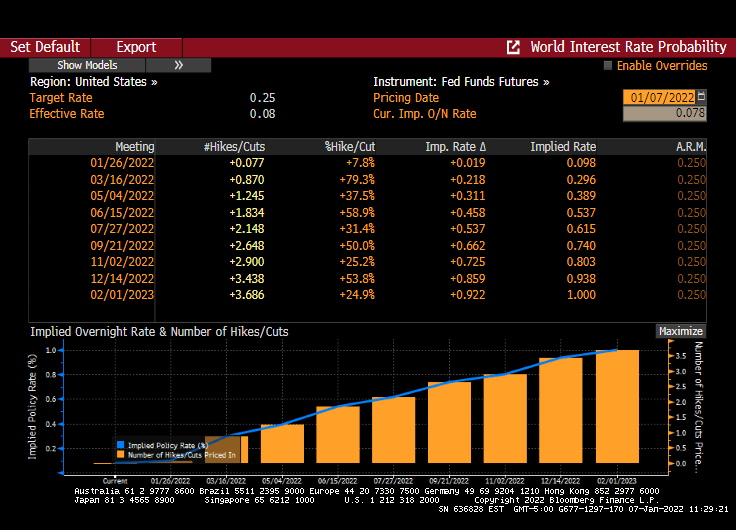

Now, The Fed is predicted to raise their target rate 4 times in 2022 (according to Fed Funds Futures data) and it looks like a whopping 100 basis points (or 1%). Holding the rest of the yield curve constant, this will considerably flatten the 10Y-3M Treasury curve. Resulting in a more expensive refinancing of the Federal Debt load.

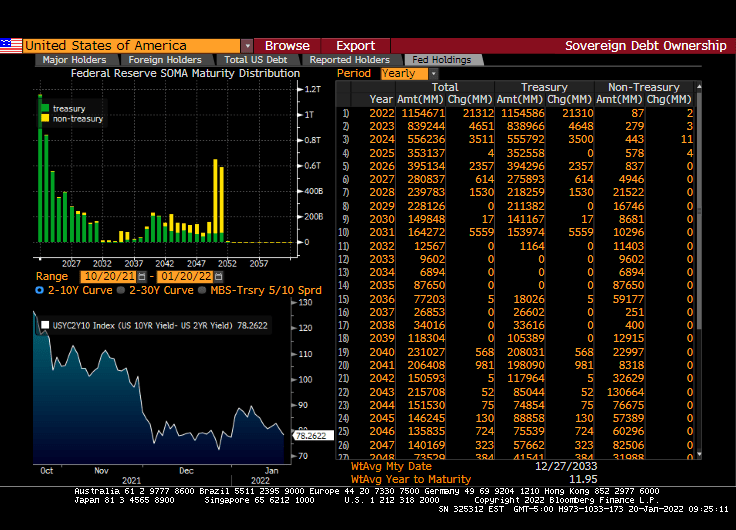

If we look at The Fed’s System Open Market Holdings (SOMH), we can see that The Fed’s holdings are primarily Treasuries with non-Treasuries (primarily agency mortgage-backed securities) not maturing (or running off) until 2050.

The majority of The Fed’s COVID expansion was picked-up by The Fed (light blue line).

How about the Treasury Inflation-protected Securities curve? Negative yields across the tenor range.

With Congress trying to spend trillions more (since Build Back Broke failed, Democrats are producing MORE spending legislation with the voting act included, of course), Treasury is going to have progressively more trouble with the (Treasury) curve.

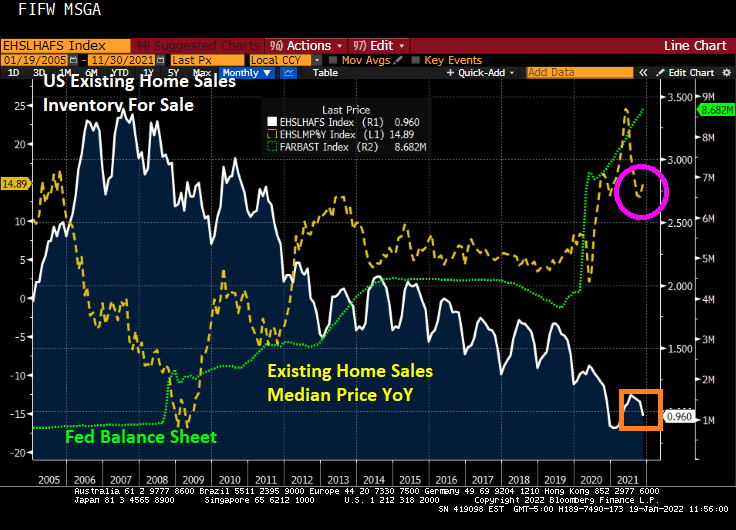

Massive Federal stimulus (both fiscal and monetary) have led to bidding wars among the wealthiest Americans. Despite clamoring for The Fed to increase rates and speed-up the shrinking of The Fed’s balance sheet, nothing has happened … yet.

(Bloomberg) — Home buyers willing to spend almost a $1 million are competing the most for a piece of the red-hot U.S. housing market.

Homes priced between $800,000 and $1 million saw the highest rate of bidding wars at 64.6%, followed by 62% for homes between $1 million to $1.5 million and 61.7% for homes above $1.5 million, according to December data from Redfin Corp.

“Buyers should anticipate that they may not win a house until their sixth or seventh bid,” Candace Evans, a Redfin team manager in New York, said in a statement. “If you’re the type of person who falls in love with a house, this is not your market.”

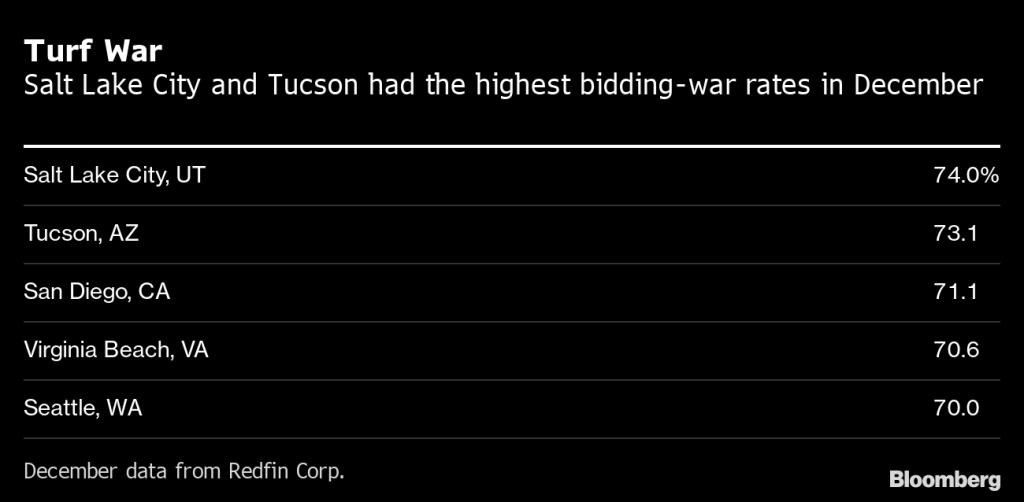

Salt Lake City had the highest bidding-war rate of 37 U.S. metropolitan areas analyzed, with 74% of offers facing competition in December, the firm said. Tucson had a 73.1% bidding-war rate and followed by 71.1% for San Diego.

Prospective buyers are competing for homes as relatively cheap mortgage rates and a proliferation of remote-working opportunities in the wake of the Covid-19 pandemic boost demand for homes in smaller cities. The number of available homes in several of the hottest markets continue to shrink.

Nearly 60% of home offers written by Redfin agents across the U.S. faced competing bids in December, the firm said. It was the lowest rate in 12 months but an increase from 54% in December 2020 as pandemic-driven demand for housing remains strong.

Vacation homes, which are often pricey and have increased in popularity due to Covid-19, may have contributed to bidding wars in the high-end market, Redfin said. Townhouses had a bidding-war rate of 62% followed by 61.3% for single-family homes, the firm said.

Now its a race against the clock as potential home buyers try to beat Powell and the Gang as they raise mortgages rates.

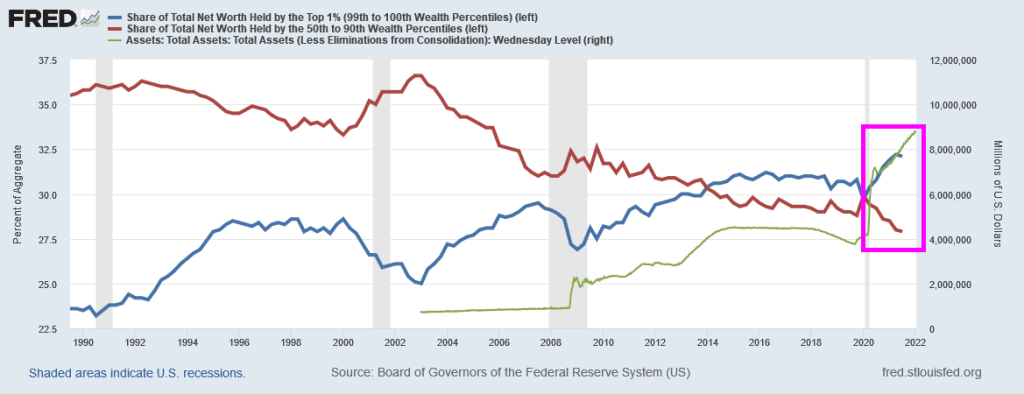

Yes, Federal stimulus has made the top 1% increase their share of total net worth that includes $800,000+ homes.

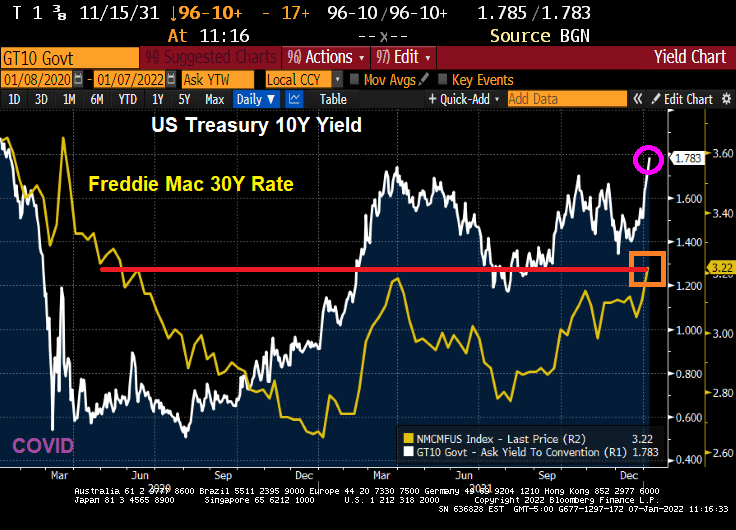

It looks like markets are buying into the prospect of The Federal Reserve raising rates three times (Bob) in 2022. And ceasing COVID monetary stimulus.

Today, the 10-year Treasury yield rose to PRE-COVID levels of 1.783%. And the Freddie Mac 30-year mortgage commitment rate rose to 3.22%, the highest since May 2020.

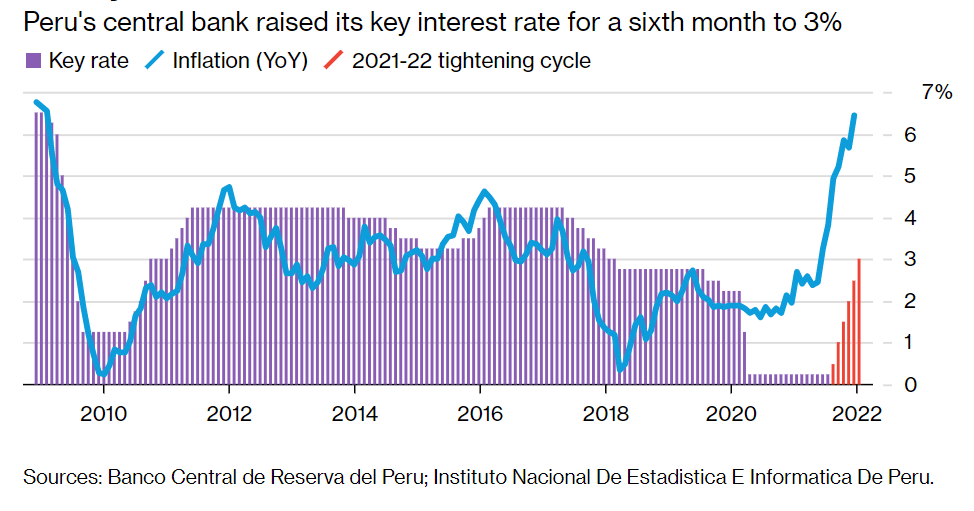

Today’s rising wage rates (although negative in terms of REAL wage rates) will likely put a Peruvian fire under The Fed’s behind. As of this morning, Fed Funds Futures are still pointing to three rate increases in 2022 (May, July and December).

And The Fed is supposed to be winding down the COVID monetary stimulus.

Why a Peruvian fire? Even Peru’s central bank is raising its key interest rate to 3% after soaring inflation.

Let’s see if Powell and The Gang follow through … or reveal themselves to be Peruvian Chickens.

When we look at the Buffett Indicator, we can see how The Federal Reserve’s loose monetary policies (or follycies) are driving up stocks to unsustainable levels that may not survive without The Fed’s “Do Ho Big Bubble Policies.”

How about the Shiller CAPE (Cyclically-adjusted Price/Earnings) ratio? While not up to dot.com levels yet, the Shiller CAPE ratio is climbing with the assistance of The Fed and their insane money printing.

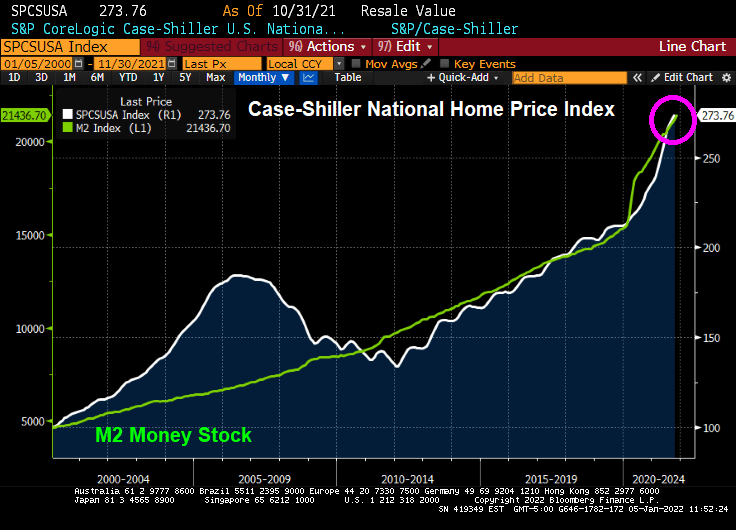

How about house prices? The Case-Shiller National home price index is far above the level last scene during the housing bubble of 2005-2007. Again, with a little help from The Federal Reserve.

I can’t wait to see how the equity market and housing market reacts IF The Fed actually follows through with reducing monetary stimulus. Probably not just adding more stimulus, just reinvesting the Treasury and MBS proceeds (aka, not shrinking the balance sheet).

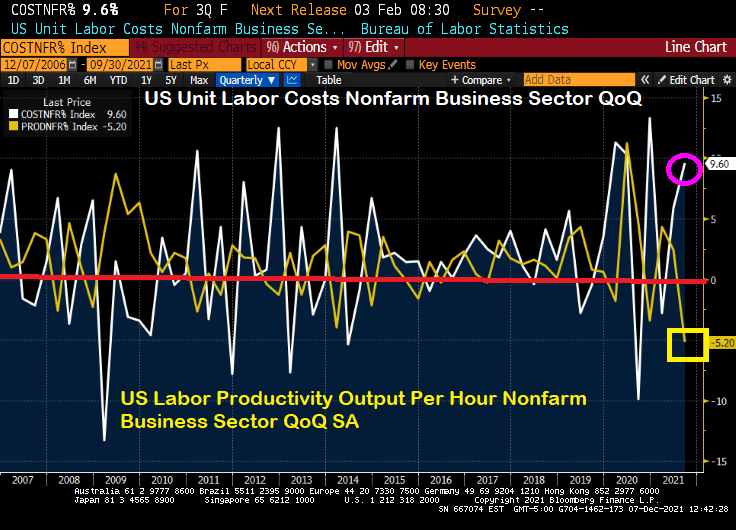

If this what the Biden Administration had in mind? Soaring labor costs at the same time that labor productivity is falling to its lowest level since 1960?

Powell and the Gang’s monetary approach doesn’t seem to be working for the labor market …

The Marty Stuart/Travis Tritt song “This One’s Gonna Hurt You (For A Long, Long Time)” seems appropriate for the plight of the middle and lower income classes in the face of high inflation. How do you spell the combination of President Biden’s policies and The Fed’s inaction on inflation? T-R-O-U-B-L-E … for the middle and lower income classes.

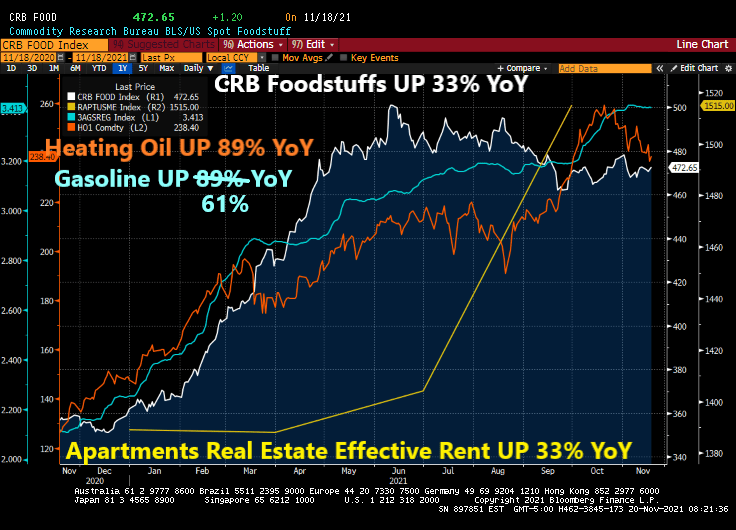

Over the past year, since the election of Joe Biden, the household consumption bundle (food, rent, heating, gasoline) have all risen dramatically in terms of prices. Food is up 33%, heating oil is up 89%, regular gasoline is up 61%, and effective apartment rents are up 33%.

Meanwhile, the 1% are sitting high on a mountain top obvious to the pain caused by The Federal Reserve and Biden Administration. Here is the growth in wealth by the 1% since the housing bubble burst and financial crisis compared with the bottom 50%.

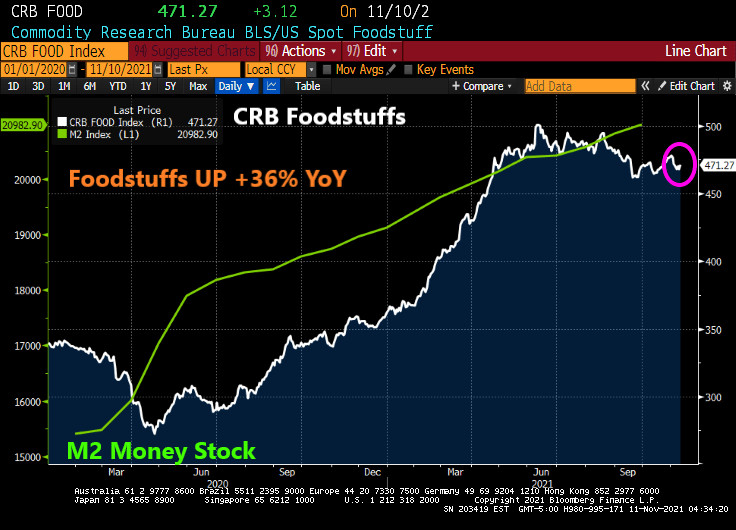

A problem facing renters is the rapid growth of home prices particularly since the COVID epidemic. At least M2 Money has “slowed” to 12.80% YoY while home prices are raging at almost 20% YoY. But hopefully home price growth will slow with declining M2 growth.

Compendium of Fed Chair Jerome Powell and President Biden on vacation.

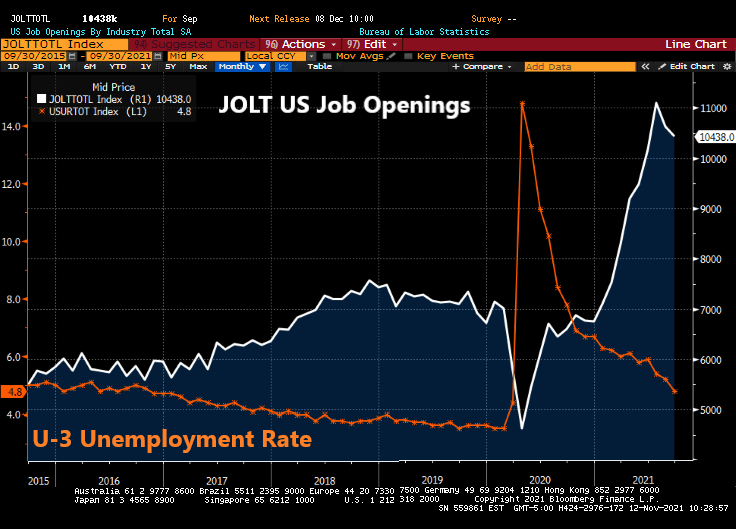

The Federal Reserve continues to JOLT markets with excessive monetary stimulus despite numerous reasons why they should back off.

For example, today’s JOLT report (US job openings) revealed that 10.4 million jobs were open in September. This is the fourth consecutive month of 1 million plus job openings, yet The Fed refuses to raise their target rate.

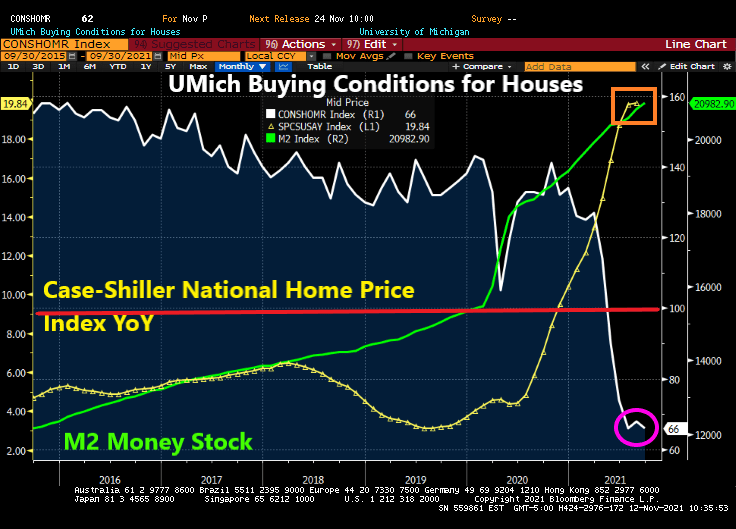

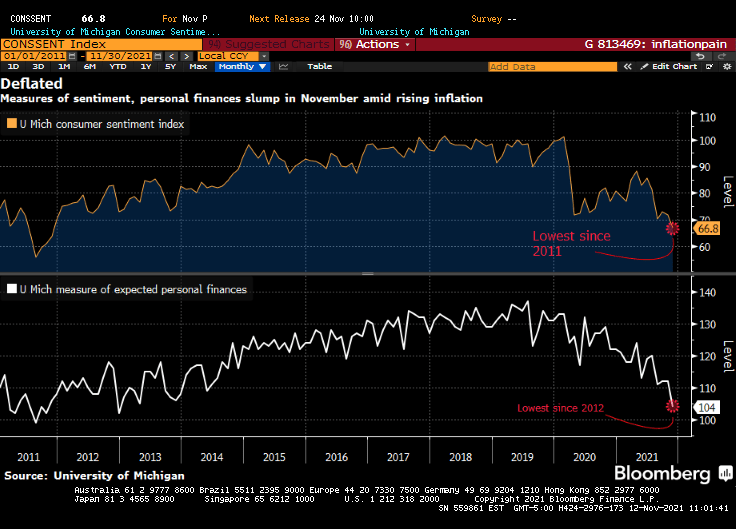

At the same time, the University of Michigan survey revealed that buying conditions for houses dropped to 66 (baseline of 100). To show how bad this is, buying conditions for houses was at 144 this time last year.

UPDATE: UMich revised their number downward to 62, the lowest since 1981.

In The Fed’s mind, they are still chasing at least 3.5% unemployment, the lowest rate under President Trump prior to COVID. But with perpetual million plus job openings GOING UNFILLED, trying to get to pre-COVID unemployment rate of 3.5% is a fool’s errand.

Of course, with The Fed helping to pump up house prices to largely unaffordable levels, it makes sense that enthusiasm for buying expensive homes has crashed.

Meanwhile, The Fed continues to JOLT the economy with excess stimulus.

Overall inflation fears are leading to lowest consumer confidence since 2011.

Combine vaccine mandates that lower the workforce and the flood of economic and monetary stimulus by the geniuses in Washington DC, and we have a Thanksgiving problem.

Supplies of food and household items are 4% to 11% lower than normal as of Oct. 31, according to data from market-research firm IRI. That figure isn’t far from the bare shelves of March 2020, when supplies were down 13%.

For grocery shoppers this holiday season, it means that someone with 20 items on their list would be out of luck on two of them.

Although U.S. supermarket operators started purchasing holiday items early, aiming to avoid shortages, many holiday essentials are already in short supply.

Turkeys are very low in stock. By the end of October turkeys were over 60% out of stock—lower than the same time last year by more than 30 percentage points. A spokesperson for Butterball LLC, one of the largest U.S. turkey processors, said the company has been experiencing similar labor and supply challenges as other organizations and industries.

Even if you can find a turkey, prices on foodstuffs in general are up 36% from last year.

And to get to the grandparents’ house of Thanksgiving, gasoline prices (regular) are up 24.5% from last year.

Biden could lower inflation by 1) stop mandating vaccines, 2) stop shutting off energy pipelines and oil exploration, 3) stop spending trillions of dollars other than Social Security, Medicare and defense.

Frankly, Thanksgiving has gotten so expensive due to Biden’s Reign of Error that I am thinking of alternatives to turkey. Like a Jersey Mike’s turkey and provolone sub.

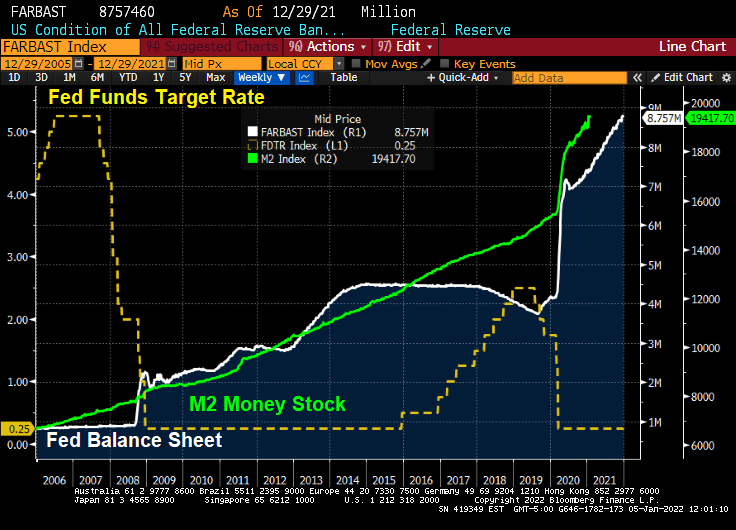

With The Federal Reserve leaving its target rate at 0.25%, but hinting at a tapering (slowdown) of asset purchases, I thought it would be good to present where The Fed sits at the moment.

You can see the rise in the effective Fed Funds rate from 2016 to early 2020, then KABOOM! COVID struck, the effective Fed Funds rate crashed while The Fed dramatically increased their purchases of Treasuries and Agency MBS. Both Treasury and Agency MBS purchases are projected to decline by mid-2022. The Fed’s target rate (purple line) is project to rise to 1% after 2023.

Where SHOULD The Fed Funds Target rate be? How about 8.80% instead of 0.25%.

So we still have over-stimulypto with The Fed projected to raise rates at a snail’s pace.

Face it, Wall Street wants interest rates low, even if inflation burns out of control.

You must be logged in to post a comment.