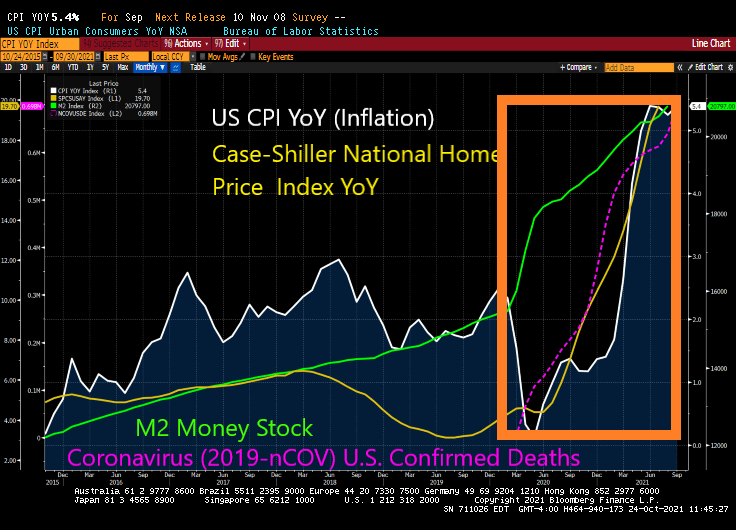

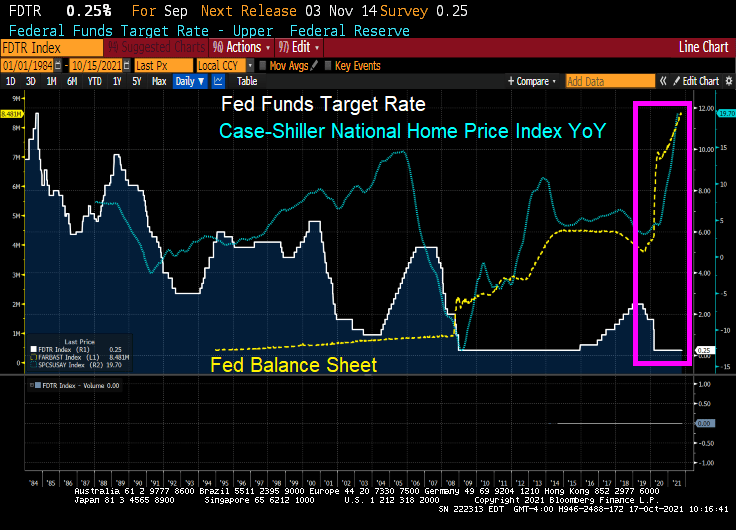

The Federal Reserve is helping to create inflation, particularly since their unorthodox surge in money supply around the Covid outbreak in early 2020. Home prices as of the latest Case-Shiller report are rising at nearly 20% year-over-year.

To add to the problem of The Fed’s overzealous money printing we have The Biden Administration (and puppy-torturer/killer Anthony Fauci) issuing Covid vaccine edicts that are wreaking havoc in labor markets further clogging the economic pipelines.

Between The Fed ZIRP policies and Biden/Fauci’s vax mandates, we are starting to see the rise (again) of the infamous MORTGAGE TILT EFFECT!

The Tilt Effect comes about as expected inflation gets priced into mortgage rates, the mortgage payment rises as the mortgage rate rises (of course), but the higher mortgage payment occurs with EXPECTED inflation in the future.

But not quite yet. Despite CPI inflation growing at 5.4% YoY, Freddie Mac’s 30-year mortgage survey rate is only 3.01% … for now.

As inflation continues to rise (thanks to ongoing Fed ZIRP policies and governments mandating Covid vaccine in order to keep your job, we should eventually see mortgage rates rise … leading to a return of THE TILT EFFECT. Which in turns make housing even MORE unaffordable.

We have tried numerous mortgage contracts in the past (mostly to offset Carter-era inflation) such as the PLAM (price-level adjusted mortgage) and the GPM (graduated payment mortgage). Now we have the PLUM (price level unadjusted mortgage) which is subject to the TILT EFFECT.

https://www.redfin.com/news/housing-market-update-pending-sales-up-47pct-from-2019/According to Redfin, forty-four percent more homes are pending sale than at this time in 2019, but only 3% more homes recently hit the market—down from 12% growth over 2019 just 7 weeks prior. As a result of the severe imbalance between the number of homes for sale and the number of buyers, the pace of the market is picking up at a time when it typically slows. A third of homes are finding buyers within a week of hitting the market, up from 30.8% at the end of the summer. This week, we’re comparing today’s market with the pre-pandemic fall market of 2019 to highlight how hot the market remains, even as most measures are settling into typical seasonal patterns.

“Comparing today’s sales and new listings numbers to the 2019 levels helps to reveal the stark shortage of supply we are facing,” said Redfin Deputy Chief Economist Taylor Marr. “The boost of housing supply that came on the market during the summer has already faded away, even as demand tapers off as we expected it to in the fall. Relative to the last ‘typical’ fall of 2019, demand remains steady and strong thanks to the increased urgency many buyers have as mortgage rates inch up. Rising rates also make buyers more price sensitive, so homes that are priced right are increasingly likely to receive offers right away.”

Shortage of supply, indeed. It is a mystery to me why the supply of homes for sale is not matching the demand.

But what happened after 2019? COVID and the entrance of massive Federal Reserve and Federal government stimulus. With limited supply hitting the market, home prices soared with the government stimulus.

We are likely to see rising prices until Federal Stimulypto stops or at least slows.

Federal Reserve Chair Jerome Powell sounded a note of heightened concern over persistently high inflation as he made clear that the central bank will begin tapering its bond purchases shortly but remain patient on raising interest rates.

“The risks are clearly now to longer and more persistent bottlenecks, and thus to higher inflation,” Powell said Friday during a virtual panel discussion hosted by the South African Reserve Bank and moderated by Bloomberg’s Francine Lacqua.

“I would say our policy is well-positioned to manage a range of plausible outcomes,” he said. “I do think it’s time to taper and I don’t think it’s time to raise rates.”

Good luck with that, Jay! You are going to raise the short-end of the yield that will lead to a flattening of the Treasury yield curve. But you are going to continue to buy Treasuries and Agency MBS in order to monetize the rampant spending by Congress and the Biden Administration? C’mon man!

You can see where Powell spoke today. It is when gold tanked along with the 10-year Treasury yield. Both rebounded a bit, but the 10-year Treasury yield continue its fall to 1.6324%.

The US dollar (green) fell when Powell opened his pie-hole. But Bitcoin (blue) fell in advance as if they knew what Powell was going to say.

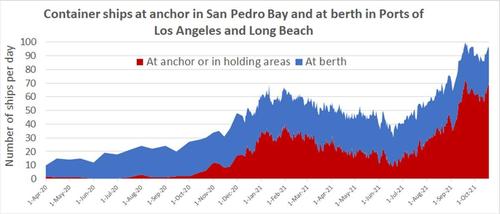

Massive Fed monetary stimulus coupled with massive Covid “relief” by the Federal government (aka. Stimulypto) has resulted in clogged ports in the US, particularly Long Beach CA. And Santa Catalina island.

Twenty-six miles across the sea Santa Catalina is a-waitin’ for me, Santa Catalina, the island of romance, romance, romance, romance. Water Cargo ships all around it ev’rywhere, tropical trees and the salty air ships dumping sewage, but for me the thing that’s a-waitin’ there’s romance.

There was fleeting hope that Southern California port congestion had turned the corner. The number of container ships waiting offshore dipped to the low 60s and high 50s from a record high of 73 on Sept. 19, trans-Pacific spot rates plateaued, the Biden administration unveiled aspirations for 24/7 port ops, and electricity shortages curbed Chinese factory output.

The reality is that the port congestion crisis in Southern California is not getting any better. Particularly if you like boating around The Catalina islands off the California shore.

The time ships are stuck waiting offshore continues to lengthen. There are simply too many vessels arriving with too much cargo for terminals, trucks, trains and warehouses to handle. There were 103 container ships at Los Angeles/Long Beach terminals or waiting offshore on Wednesday, an all-time high.

Offshore, the number of ships at anchor or in holding patterns is once again nearing record territory. According to the Marine Exchange of Southern California, 70 container ships were waiting off Los Angeles and Long Beach on Monday, 67 on Tuesday and 71 Wednesday (not including other cargo ships that are loaded with boxes).

Chart: American Shipper based on data from Marine Exchange of Southern California. Data bi-monthly April-Nov 2020; daily Dec 2020-present

The Baltic Dry Exchange (shipping) index has dropped recently, but is still up 239% since January 1, 2021.

The good news? Ships at anchor off Shanghai/Ningbo down nearly 50% over the past 18 days.

So, China port congestion is clearly as it transfers to California. And US prices soar.

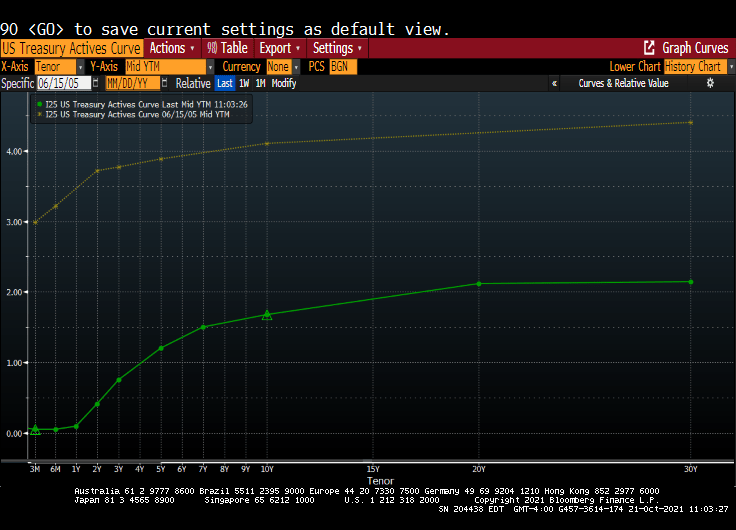

I remember my academic colleague at The Ohio State University (now at Notre Dame), Paul Schultz saying “Why do you find fixed-income and the yield curve interesting?” I have always found the yield curve to be interesting … at least until The Federal Reserve hammered down the short-end with it zero-interest rate policy (ZIRP) and tried manipulating the 10-year Treasury Note yield through Quantitative Easing (QE) meaning The Fed’s purchase of Treasuries and Agency Mortgage-backed Securities (MBS). No, I still think the manipulated yield curve is interesting.

Here is today’s Treasury actives curve (green) versus the yield curve at the peak of the previous housing bubble in 2005 yellow). That is a 300 basis point shift as the short-end. And a 243 basis point shift for the 10-year Treasury Note.

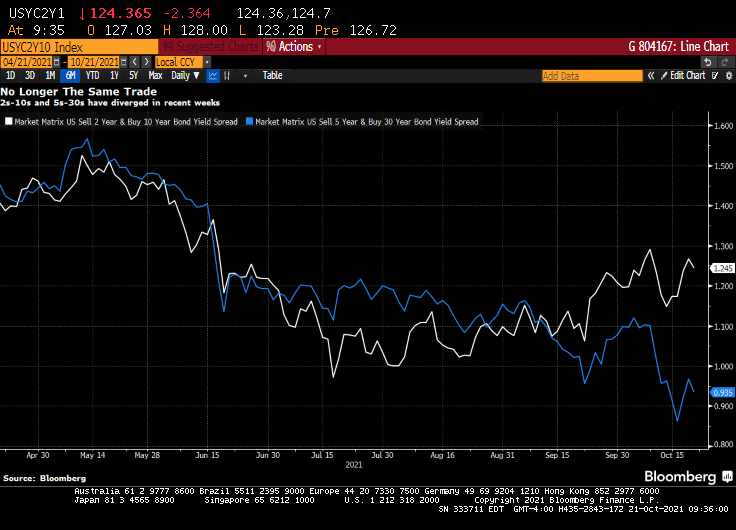

(Bloomberg) — The yield curve is one of the most-powerful forces in the observable financial universe. While much of the price action that we see on a day-to-day basis may be driven by some sort of dark energy, the curve provides a highly visible lodestone indicating the state of policy settings and the likely trajectory of the economy. That being said, the curve is often misunderstood — a bear flattening often produces plenty of hand-wringing, when it’s the bull steepening that you should really worry about. In fact, referring to “the curve” itself is something of a misnomer — while different iterations of the yield curve often travel in tandem, sometimes their paths diverge. That has been the case recently, though perhaps not for much longer. The recent rise in two-year yields looks more than justified, as various fixed income models demonstrate in a roundabout way.

For the past year and a half or so, most of the focus on the yield curve in this column has been on the 5s-30s iteration. The rationale for this has been relatively straightforward: With the Fed funds rate locked in near zero for the foreseeable future, the two-year note has been moribund. As such, 2s-10s has really just been another articulation of the 10-year yield. And much like recent price action vis-a-vis my 10-year model, the curve briefly traded where it “ought” to in March before once again becoming too flat in recent months.

At least 5s-30s has had the benefit of containing a useful forward-looking component on both legs of the spread. Yet even as I type that, it is interesting to note that 2s-10s and 5s-30s exhibited virtually identical price action at virtually identical levels earlier this year. While they remain positively correlated, of course, a clear wedge has emerged between the two curves as five-year yields have broken decisively through 1%, pricing greater conviction that a monetary tightening cycle will fully emerge over the next half-decade.

Yet I am left to wonder about the two-year note. The eurodollar strip is pricing that the bulk of monetary tightening will come by the end of 2023, a period that’s now largely captured by the shortest-maturity coupon security. To be sure, the appropriate level for 2s is a function not only of the ultimate magnitude of monetary tightening, but when it begins. After all, a 150 bp hike in Q4 of 2023 carries very different implications for the current two-year note than a 25 bp rate rise every three months from Q3 of next year onwards.

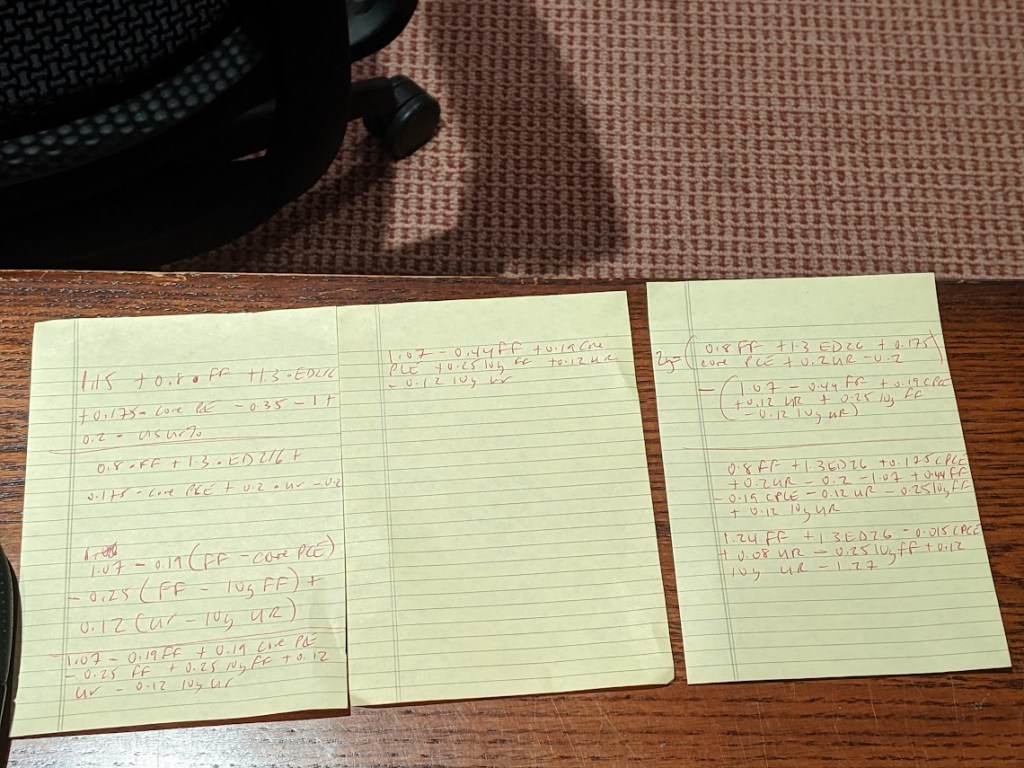

It occurred to me that I could back out a model for two-year yields by simply subtracting the output of my yield curve model from that of the 10-year model. I had no real idea of what to expect from this exercise, but even with the proviso that short-end yields rarely stray too far from the policy rate, I was pleasantly surprised at how close the fit is from this “derivative” model for the two-year.

The question then arose, naturally, of what actually went into the calculation of this “model.” After all, knowing the formulae of the two constituent models — for the 10-year and the yield curve– should allow for the distillation of a separate equation for the two-year note. Because that sort of thing is more fun than unpacking more boxes, that’s how I spent a few minutes on Wednesday night. The outcome isn’t necessarily an optimal model for the two-year, but more of an accidental one.

A bit of high school algebra

For what it’s worth, the resultant formula is 2y = 1.24 * FDTR + 1.3 * (ED2 – ED6) -0.015 PCE CYOY + 0.08 * USURTOT – 0.25 * (10y average of FDTR) + 0.12 * (10y average of USURTOT) – 1.27. I am pretty sure that one could get similar results with a simpler framework; the notion that a 2% rise in core inflation is worth just 3 bps on the two-year yield, all else being equal, leaves me simultaneously amused and bemused.

What does seem evident, however, is that henceforth there is going to be considerably more signal generated from two-year yields than has been the case in recent quarters. As such, 2s-10s are going to be worth following again, just as much if not more than 5s-30s. Both nominal yields and the curves are clearly constrained by the notion that all of this inflation kerfuffle really is transitory at its heart, and that, with r* remaining in the gutter, the long-run lid on nominal policy rates is going to be extraordinarily low.

That’s probably as good a null hypothesis as any, and possibly better than most. That being said, if we’re still having a lot of the same inflation conversations a year from now, we’re gonna need a long hard think about whether some of the post-GFC lessons need to be unlearned. In the meantime, at least fixed income is interesting again. I wonder where the yield curve and the model will eventually meet up to shake hands again… -Cameron Crise

The yield curve will become more interesting if Powell and The Gang take their foot off the monetary accelerator pedal.

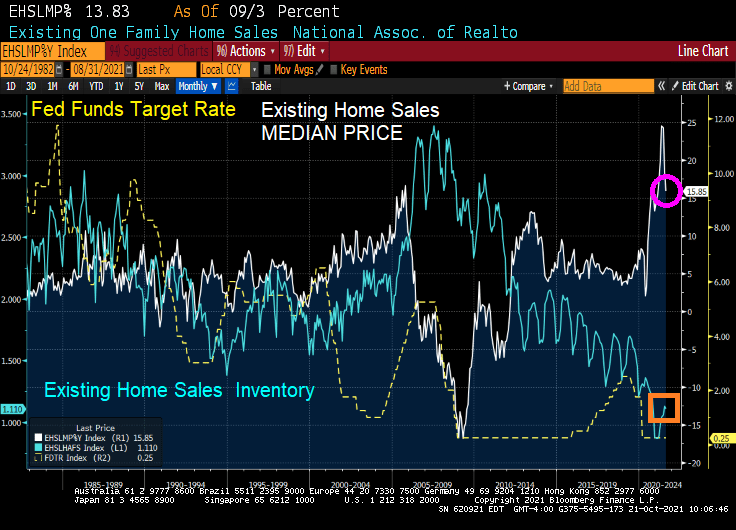

Yes, the super-heated housing market is showing signs of slowing down.

According to the Mortgage Bankers Association (MBA), mortgage purchase applications rose 1.87% from the previous week. However, purchase applications are down 10% from the same week last year.

Refinancing applications dropped -.48% from the previous week as the 30-year mortgage contract rate rose from 3.14% to 3.18%. Refi apps are up 6% from the same week last year.

As rates begin to rise, mortgage refi applications will decline.

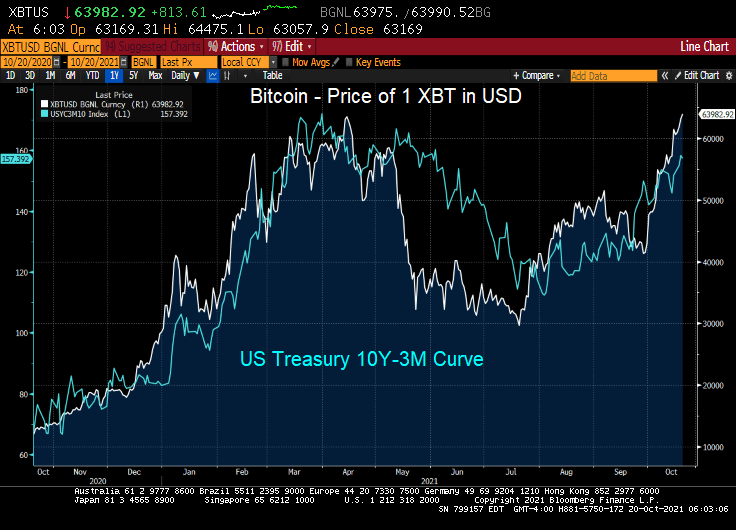

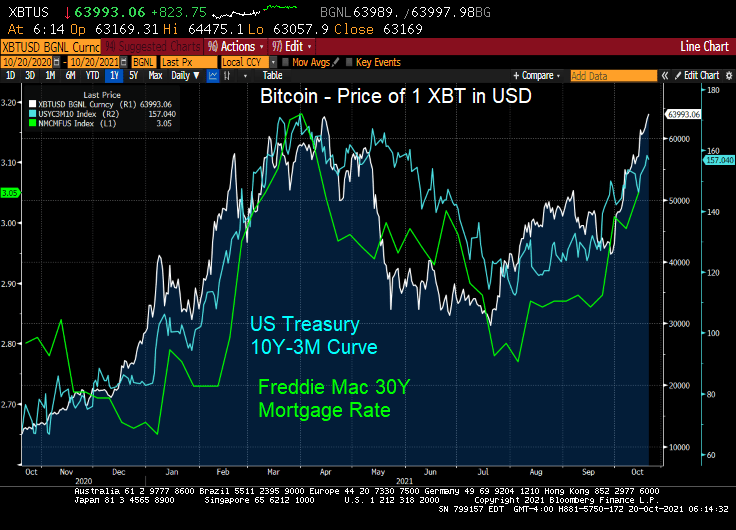

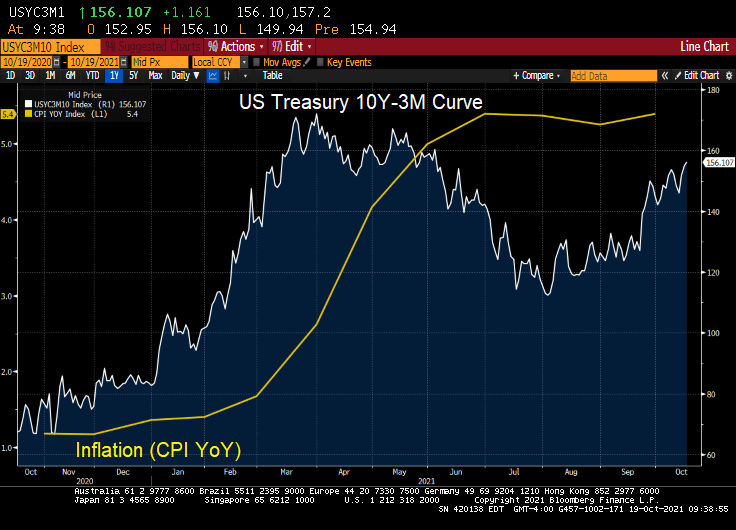

I have no idea why Jack Dorsey tweeted “705742.” But I do know that Bitcoin hit 63,982.92 this morning as the US 10Y-3M curve has been steepening.

Since the 3-month Treasury yield has been repressed to near zero, the 10Y-3M curve is pointing to rising 10-year yields. Which likely means that 30-year mortgage rates will be rising too.

UPDATE! Bitcoin hits 66,615 as Proshares Bitcoin Strategy E rises as well.

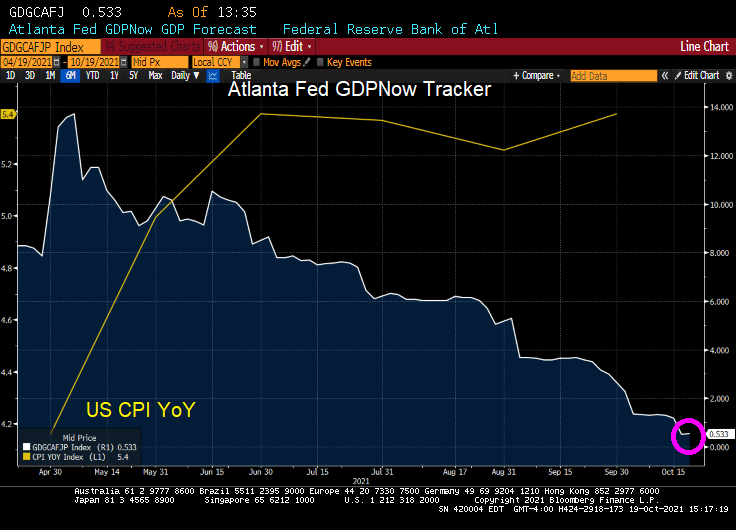

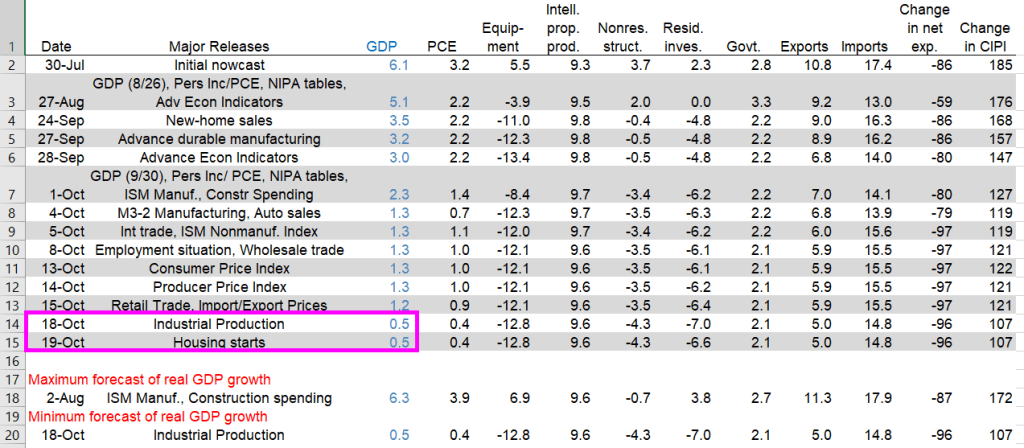

The Atlanta Fed’s GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the third quarter of 2021 is 0.5percent on October 19, down from 1.2 percent on October 15. After recent releases from the US Census Bureau and the Federal Reserve Board of Governors, the nowcasts of third-quarter real personal consumption expenditures growth and third-quarter real gross private domestic investment growth decreased from 0.9 percent and 10.6 percent, respectively, to 0.4 percent and 8.4 percent, respectively.

US real GDP nosedived to 0.5% according to the Atlanta Fed GDPNow real-time tracker.

Again, The Fed and Federal government pumped trillions of stimulus into an unprepared economy resulting in massive bottlenecks. So, we are getting declining GDP and rising inflation.

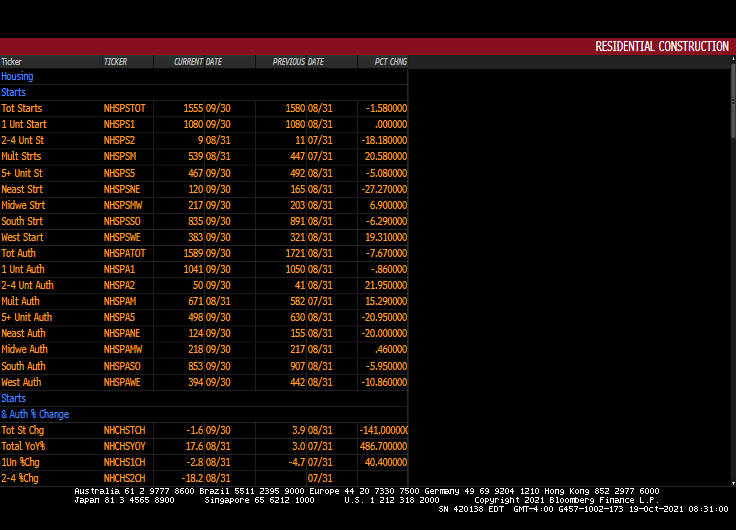

Yesterday’s industrial production dove leading to the 0.5% GDP figure. Today’s housing starts didn’t impact GDP in a meaningful way.

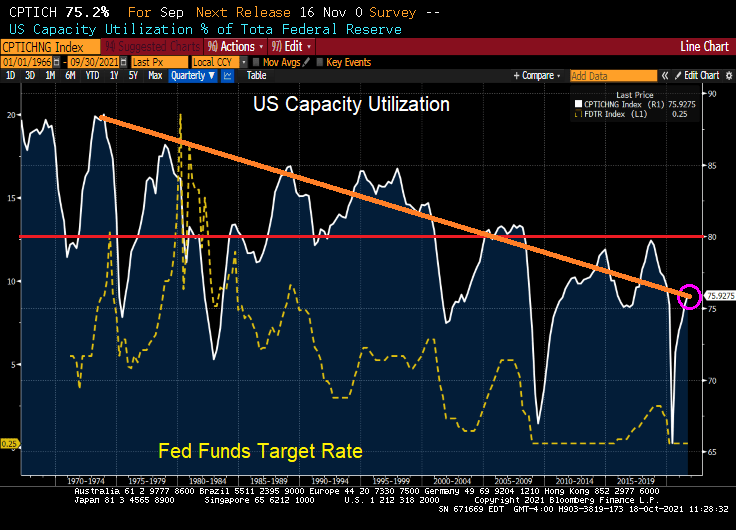

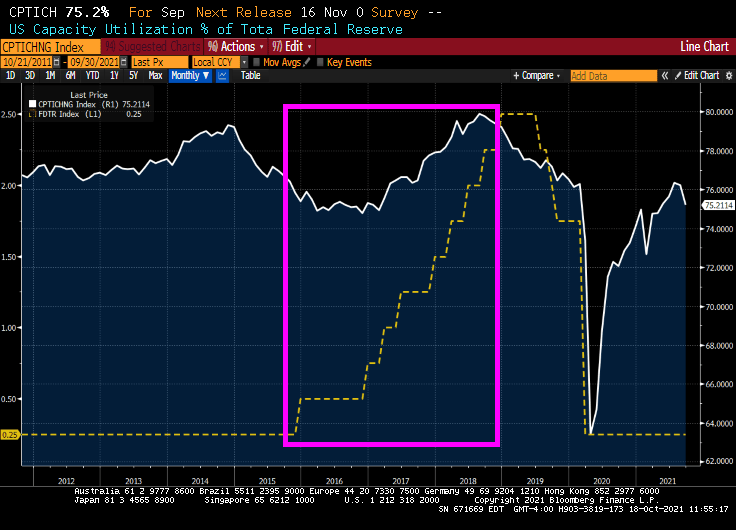

It used to be that capacity utilization was a signal for The Federal Reserve to raise or lower their key target rate. When capacity utilization rose above 80%, the economy was deemed to getting “hot” and The Fed would raise rates. And vice-versa.

But then mass outsourcing occurred, primarily to China and southeast Asia. Since the 1970s, the general trend in US capacity utilization has been downward. But the last time the US saw capacity utilization of above 80% in Q4 2007. Capacity utilization almost hit 80% in August 2018

Oddly, The Fed started raising their target rate in 2015 under Fed Chair Janet Yellen AS CAPACITY UTILIZATION WAS FALLING. Capacity utilization hit almost 80% as The Fed put the brakes on rate hikes before Covid struck.

So, capacity utilization was obviously not on the mind of Yellen and the FOMC. Call it the new abnormal.

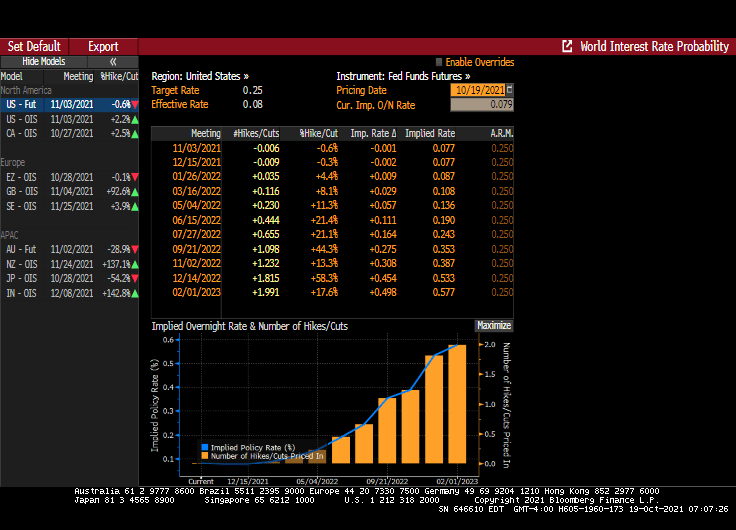

With capacity utilization falling, the path of Fed policy rate has shifted sharply over the past couple of weeks, to currently pricing first hike into the September 2022 FOMC meeting and second hike by February 2023 — there are now 100bp of rate hikes priced by the end of 2023, in line with the Fed’s dot-plot forecast.

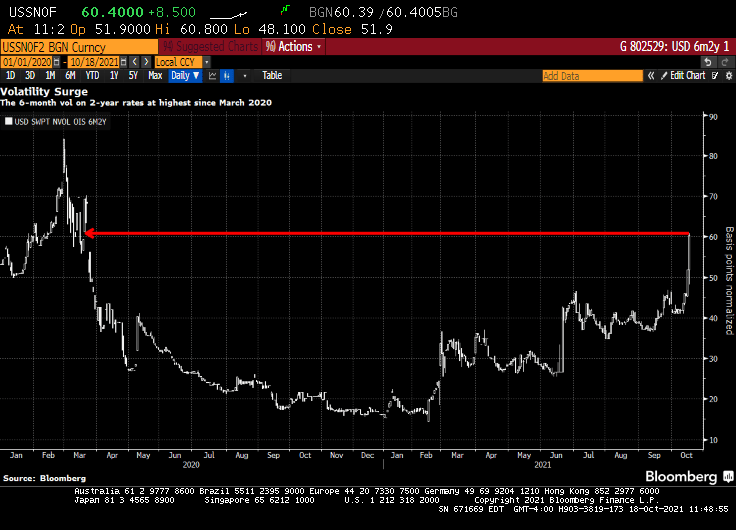

Short-dated volatility on front-end U.S. rates — known as the upper left corner of the volatility surface — continues to catch a bid over the U.S. morning session, spurred by a sharp hawkish re-pricing of the Fed’s policy stance.

You must be logged in to post a comment.